Essential VAT Bookkeeping Tips for UAE Businesses

Adopt a Comprehensive Record Retention Strategy

The first critical bookkeeping tip for entrepreneurs in UAE involves establishing a robust record retention framework that satisfies both VAT and Corporate Tax requirements. While UAE VAT regulations traditionally mandate a five-year retention period from the end of the tax period, the introduction of Corporate Tax has established a seven-year minimum for related documentation. Since most accounting records such as general ledgers, bank statements, and purchase invoices serve both tax types, adopting a universal seven-year retention policy represents the most prudent approach for any business in Dubai or elsewhere in the country.

Retention requirements vary significantly by document category and transaction type. Real estate records demand the longest retention period at fifteen years, driven by the long-term adjustment cycles of the Capital Asset Scheme. For properties exceeding AED 5 million in value, the initial VAT recovery remains subject to annual use-of-asset reviews over a ten-year period. Accurate bookkeeping for real estate must therefore track not only the purchase price and VAT paid but also the annual percentage of taxable versus exempt usage for the entire decade following acquisition.

Key Retention Periods by Document Type:

| Record Category | Retention Period | Impacted Documents |

| Standard Accounting | 7 Years | Ledger, Balance Sheet, P&L, Bank Statements |

| VAT Transactions | 5 Years | Tax Invoices, Credit/Debit Notes, Import Docs |

| Real Estate Records | 15 Years | Property contracts, Title deeds, CAS adjustments |

| Capital Assets | 10 Years | Fixed Asset Register, Depreciation logs |

| Payroll & WPS | 7 Years | Salary slips, WPS files, EOSB calculations |

Implement Secure Digital Documentation Systems

Effective bookkeeping in 2026 requires more than filing cabinets or simple PDF storage. The Federal Tax Authority permits electronic record-keeping, but businesses must establish secure document management systems featuring role-based access controls and unalterable audit trails. These systems should preserve document integrity throughout the retention period while allowing authorized personnel to retrieve specific records within minutes during an FTA inspection.

A critical consideration often overlooked by UAE businesses involves the language requirements for VAT records. While day-to-day books may be maintained in English, the FTA retains statutory authority to request Arabic translations for any document during a VAT audit process in Dubai. For high-stakes documents such as complex commercial contracts or long-term real estate agreements, maintaining a bilingual version or pre-translated Arabic summary can help businesses avoid penalties during investigations. This proactive approach demonstrates good faith compliance and can significantly simplify VAT processes when dealing with the tax authority.

For businesses without dedicated internal accounting teams, partnering with professional accounting and bookkeeping services can ensure that document management systems are properly configured and maintained to meet both VAT and Corporate Tax requirements while satisfying FTA language and accessibility standards.

Establish a Credit Aging Schedule to Prevent Expiry

One of the most financially consequential changes in 2026 involves the introduction of a strict five-year limitation period for reclaiming refundable VAT or using credit balances to offset other liabilities. Effective January 1, 2026, the Tax Procedures Law creates a “use-it-or-lose-it” dynamic for input tax credits. Any credit balance remaining after the five-year window expires permanently unless a refund application is submitted within the prescribed timeframe.

For businesses that have carried forward balances since 2018, the 2026 calendar year serves as a critical transitional window. A company in Dubai that overpaid VAT in the first quarter of 2021 has until the end of the first quarter of 2026 to either utilize that credit or request a formal refund. Proactive bookkeeping must therefore include a detailed credit aging schedule that tracks when each credit balance arose and calculates the exact expiry date.

VAT Credit Refund Time Limits:

| Time Limit Category | Duration | Commencement Trigger |

| Standard Refund Claim | 5 Years | End of the tax period where credit arose |

| Exception for FTA Decisions | 1 Year | Date the balance arises from the decision |

| Late-Cycle Credits | 90 Days | Credits arising in the last 90 days of year 5 |

| Transitional Grace Period | Until Dec 31, 2026 | Credits older than 5 years as of Jan 1, 2026 |

The transitional grace period extends only until December 31, 2026, for credits older than five years as of January 1, 2026. Businesses must maintain accurate VAT records that clearly document the origin and age of every credit balance. Finance teams should prioritize utilizing the oldest credits first and consider filing for refunds on amounts unlikely to be absorbed through regular business operations.

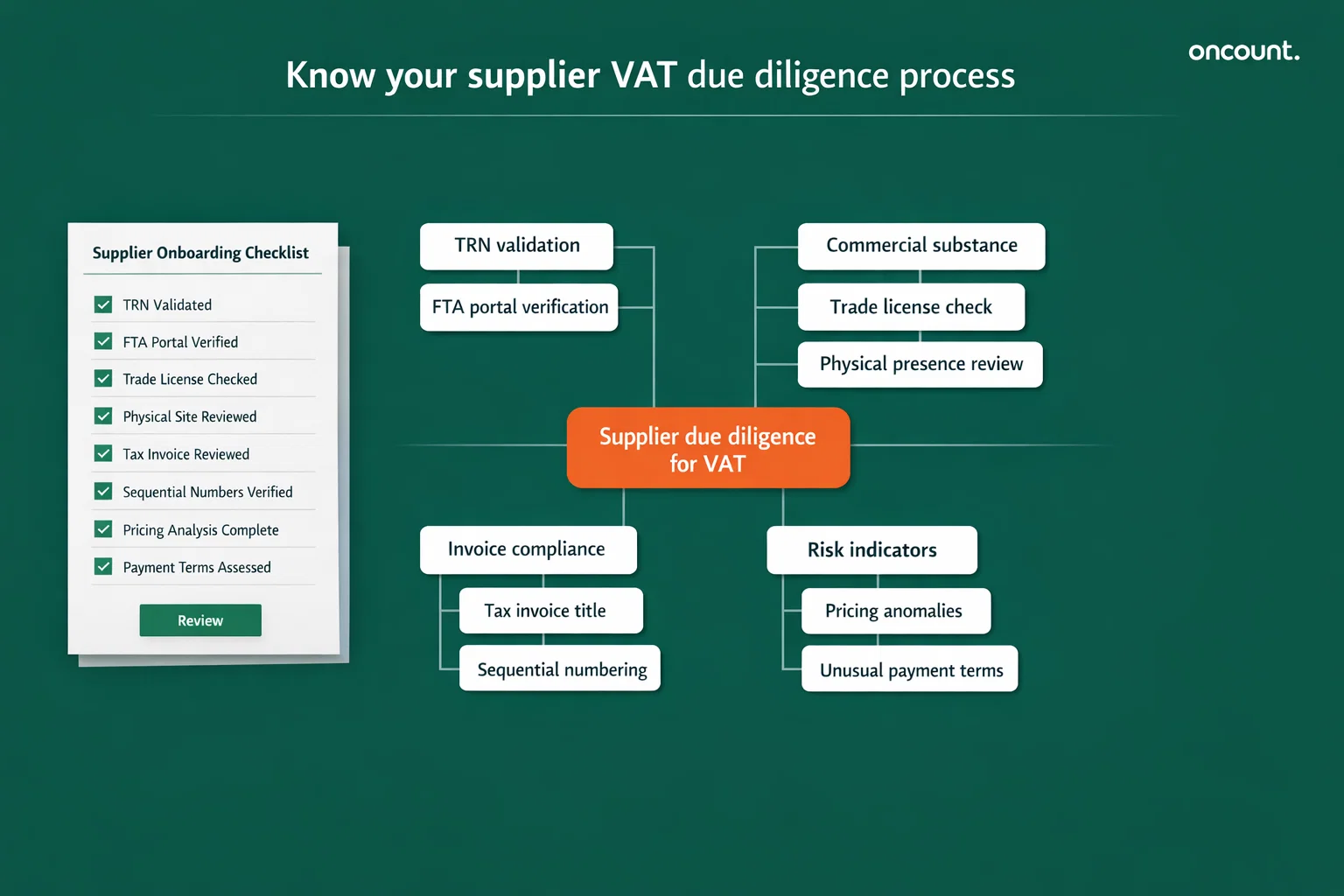

Implement a Know Your Supplier Protocol

As the constructive knowledge standard comes into force, the bookkeeping department must function as the first line of defense against supply chain fraud. Simple Tax Registration Number verification through the FTA portal is no longer sufficient for high-value transactions. Progressive UAE businesses are implementing comprehensive supplier vetting procedures that must be completed before any supplier is onboarded and before any significant input tax is recovered on their tax invoices.

The Know Your Supplier protocol should include several verification steps. First, confirm the validity of the supplier’s TRN through the official Federal Tax Authority portal to ensure they are properly registered and compliant. Second, conduct a commercial substance review verifying that the supplier maintains a legitimate physical presence, holds appropriate trade licensing for the services in Dubai or goods they provide, and demonstrates the economic capacity to fulfill the contract terms.

Essential Supplier Due Diligence Checklist:

- TRN Validation: Confirm the validity of the supplier’s TRN through the official FTA portal

- Commercial Substance Review: Verify legitimate physical presence and appropriate trade licensing

- Invoice Compliance Audit: Ensure received invoices contain all mandatory elements including “Tax Invoice” title and sequential numbering

- Pricing Anomalies: Document commercial rationale for transactions with significantly below-market pricing

- Payment Terms Review: Investigate any unusual requests for cash payments or non-standard settlement methods

By maintaining detailed documentation of these verification steps, businesses can demonstrate to auditors that they exercised appropriate due diligence and had no constructive knowledge of any supply chain irregularities. This becomes particularly important when claiming input VAT on high-value purchases where the risk of connection to tax evasion schemes is elevated.

Master the Reverse Charge Mechanism Documentation

The removal of the self-invoicing requirement for imports of concerned goods or services under the reverse charge mechanism represents an administrative simplification introduced by Federal Decree-Law No. 16 of 2025. However, this change does not reduce the complexity of proper bookkeeping for cross-border transactions. The substantive liability remains unchanged, as importers must still account for output VAT and corresponding input VAT within their VAT return.

In the absence of a self-invoice, auditors will rely on underlying business documents to verify the value, nature, and source of the supply. For bookkeeping purposes, this means that contracts, foreign supplier invoices, and import declarations must be linked with high precision to ledger entries. Each cross-border service import file should contain the foreign supplier’s invoice showing the value in the original currency, the Central Bank of the UAE exchange rate for the date of supply, proof of payment through bank SWIFT or remittance advice, and evidence that the service was used for business purposes.

The bookkeeping process must ensure that the exchange rate used is the “Date of Supply” rate published by the Central Bank, not the “Date of Payment” or “Date of Invoice” rate unless they coincide. Consistent application of this methodology across all transactions is vital for passing an FTA review and demonstrates proper bookkeeping practices that align with UAE tax law requirements.

Classify Supply Types Accurately for Filing VAT Returns

Accurate VAT reporting is built upon the meticulous classification of every transaction. Errors in classification such as recovering input tax on an exempt supply or failing to charge VAT on a deemed supply are primary triggers for FTA audits. Businesses must train their bookkeeping staff to apply the correct hierarchy of classification for all goods or services supplied.

Supply Classification Framework:

| Supply Type | VAT Rate | Input Tax Recovery | Common Scenarios |

| Standard Rated | 5% | Fully Recoverable | Commercial rent, consulting, electronics |

| Zero-Rated | 0% | Fully Recoverable | Exports, international transport, healthcare |

| Exempt | 0% | Non-Recoverable | Residential rent (after 3 years), local transport |

| Out of Scope | N/A | Non-Recoverable | Intra-group transfers, passive dividends |

A common bookkeeping error involves “mixed supplies” where a single invoice contains both taxable and exempt elements. In these cases, the input tax must be apportioned according to the ratio of taxable use. Advanced ERP systems with FTA approval can automate this calculation, ensuring that only the eligible portion of VAT is claimed on the return. This automated approach helps businesses maintain compliant VAT calculations while reducing the administrative burden on accounting staff.

Conduct Monthly Reconciliation Before Return Filing

A high-performing bookkeeping function should follow a controlled close process every month to catch discrepancies before the VAT return filing deadline. This monthly discipline helps businesses avoid penalties and ensures that all VAT amounts are correctly reported. The reconciliation should begin immediately after month-end and be completed at least three business days before the return filing deadline to allow time for corrections.

The monthly reconciliation cycle should include four critical verification steps. Revenue reconciliation involves matching the total sales in the general ledger with the output VAT reported on the return to ensure all taxable supplies have been captured. Purchase reconciliation ensures every input tax claim is supported by a valid tax invoice stored in the document management system. Bank-to-books audit verifies that the VAT amounts recorded match the actual payments made to suppliers and received from customers. EmaraTax sync cross-references the internal import records with the import data automatically populated by UAE Customs on the EmaraTax portal.

This systematic approach to monthly reconciliation helps identify errors when they occur rather than discovering them during an audit process months or years later. Early detection allows businesses to file voluntary disclosures for errors exceeding AED 10,000, which significantly reduces the penalty exposure compared to discovery during an FTA inspection.

Prepare for Electronic Invoicing System Requirements

The implementation of the Electronic Invoicing System beginning with a pilot in July 2026 marks the end of the unstructured data era. The move to machine-readable formats like XML and JSON using PEPPOL PINT standards represents a technological leap that will automate VAT reporting and audit selection. Businesses must begin preparation immediately to ensure they can generate VAT compliant e-invoices when the mandatory rollout reaches their sector.

The UAE has adopted a “5-corner” model for e-invoicing that ensures transaction data is reported to the FTA simultaneously with its exchange between buyer and seller. Under this model, the supplier generates invoice data within their ERP system, which is then validated by their Accredited Service Provider. The ASP converts the data to mandatory XML format, adds a digital signature and UUID, and transmits it to the receiver’s ASP while reporting a Tax Data Document to the FTA. This real-time reporting enables the tax authority to immediately cross-verify VAT returns against actual transaction data.

Mandatory E-Invoice Technical Fields:

- UUID: A Universally Unique Identifier for every document

- TIN/TRN: For B2B transactions, the first 10 digits of the Tax Registration Number are mandatory

- Supply Category Codes: Precise codes for standard, zero-rated, exempt, or reverse charge supplies

- Date/Time Metadata: The issue date and time must be recorded in UTC

- Digital Signature: Provided by the ASP to ensure document integrity and authenticity

Preparation for EIS requires an immediate audit of the business’s master data. Invoices that do not meet the technical specifications defined in the FTA’s Data Dictionary will be rejected by the system, potentially resulting in penalties of AED 100 per non-compliant invoice. Businesses should work with their accounting software providers or specialized VAT consultants to ensure their systems can meet these requirements.

Invest in FTA-Approved Accounting Software

As the FTA moves toward real-time transaction monitoring, the reliance on manual spreadsheets is becoming a significant compliance risk. Using software from the FTA’s Accredited Tax Accounting Software list provides several bookkeeping advantages that can help businesses ensure compliance while reducing administrative burden. These systems are specifically designed to align with UAE’s VAT compliance in the UAE requirements and regulatory expectations.

FTA-approved accounting software comes pre-configured to generate the UAE VAT201 return and the Emirate-wise sales breakdown required for return filing. The systems can generate the FTA Audit File instantly, which is the first document requested during an investigation, significantly reducing response time and demonstrating audit readiness. Built-in validation features can flag TRN errors, identify missing mandatory invoice fields, and alert the team to potential reverse charge mechanism or Capital Asset Scheme adjustment requirements before submission.

Perhaps most importantly, accredited software is designed to integrate seamlessly with Accredited Service Providers for the e-invoicing system. This ensures that the transition to electronic invoicing does not require a complete system overhaul, protecting the business’s technology investment while enabling compliance with the new digital requirements. The software helps simplify VAT processes and reduces the likelihood of errors that could result in penalties.

Understand the New Penalty Framework to Avoid Penalties

The UAE Cabinet Resolution No. 129 of 2025 and Cabinet Decision No. 75 of 2023 have introduced a significant shift in the penalty regime, effective April 14, 2026. The new structure moves away from punitive initial fines toward a model that encourages the rapid correction of errors through Voluntary Disclosures. Understanding VAT penalties and the new framework is essential for managing financial risk.

2026 Penalty Framework Comparison:

| Violation Type | Old Penalty Regime | New Penalty Regime (Post-April 2026) |

| Late Payment of Tax | 2% initial + 4% monthly (max 300%) | 14% per annum, calculated monthly |

| Incorrect Tax Return | AED 1,000 (1st) / AED 2,000 (Repeat) | AED 500 (unless corrected promptly) |

| Voluntary Disclosure | 5% to 40% (Time-based brackets) | 1% monthly interest on tax difference |

| Undisclosed Evasion (Audit) | 50% fixed + 4% monthly | 15% fixed + 1% monthly |

Under the 2026 rules, the cost of delay is precisely 1.16% per month for late payment of tax. This means that the cost of compliance for a business that discovers an error and files a Voluntary Disclosure is significantly lower than the cost of discovery during an audit. Bookkeeping teams must be aware of the AED 10,000 threshold for error correction. Errors below AED 10,000 can typically be corrected in the current tax return period through the EmaraTax portal, while errors exceeding this amount require the filing of a formal Voluntary Disclosure using Form 211.

Filing a VD before an audit notice is received is the most effective way to manage financial risk, as the fixed 15% penalty is waived entirely. This creates a strong incentive for businesses to maintain robust internal VAT audit procedures that can identify errors quickly, allowing for prompt correction before the FTA discovers the discrepancy. Businesses must maintain vigilance to pay VAT on time and file accurate returns to minimize exposure to these penalties for non-compliance.

Maintain an Audit-Ready Documentation System

An FTA audit in 2026 is a risk-based examination of the behavioral reality of the business. Preparation must therefore go beyond mere documentation to include systematic organization and instant retrievability of all supporting records. The FTA’s systems are programmed to flag unusual patterns such as turnover mismatches where VAT turnover does not reconcile with Corporate Tax revenue, frequent adjustments involving a high volume of credit notes or post-filing corrections, and negative returns where input tax consistently exceeds output tax particularly in sectors that are typically standard-rated.

To maintain an audit-ready state, the bookkeeping function should maintain a digital “Audit Box” containing comprehensive documentation for every tax period. For sales, this includes tax invoices, credit notes, export proof, and delivery notes to enable revenue verification. For purchases, valid tax invoices, reverse charge mechanism supporting documents, and bank transfers provide input tax justification. Inventory documentation with stock logs, disposal records, and deemed supply records ensures physical inventory matches paper records.

Key Audit Triggers to Monitor:

- Turnover Mismatches: VAT turnover not reconciling with Corporate Tax revenue

- Frequent Adjustments: High volume of credit notes or post-filing corrections

- Negative Returns: Consistent filing where input tax exceeds output tax

- Supply Chain Links: Major receipts from suppliers under FTA investigation

- Classification Errors: Patterns of incorrect supply categorization

Corporate documentation including trade license, TRN certificate, and organizational chart validates entity status, while financial records such as trial balance, general ledger, audited financial statements, and bank reconciliations demonstrate data integrity. For businesses involved in international trade, logistics documentation including customs declarations, bills of lading, and airway bills provides zero-rate verification essential for defending export claims.

Wrapping up on VAT Bookkeeping Tips

The 2026 UAE VAT environment represents a fundamental shift from passive accounting to active governance. The introduction of the constructive knowledge standard, the five-year limitation on credit balances, and the mandatory Electronic Invoicing System collectively demand that businesses transform their bookkeeping from a historical record-keeping function into a real-time compliance and risk management operation. Success in this era depends on three pillars: technical readiness, procedural rigor, and proactive credit management.

Businesses must utilize the 2026 transitional window to reconcile and claim legacy credits before they expire permanently on December 31, 2026. They must migrate toward FTA-approved accounting systems that can generate FAF files and interface with the 5-corner e-invoicing model. Most importantly, they must institutionalize a culture of due diligence where input tax recovery is contingent upon forensic verification of the supply chain. By embracing these principles and implementing the bookkeeping tips outlined in this guide, UAE businesses can navigate the complexities of the 2026 reforms, minimize the risk of costly VAT penalties, and ensure seamless integration into the nation’s advanced digital economy.