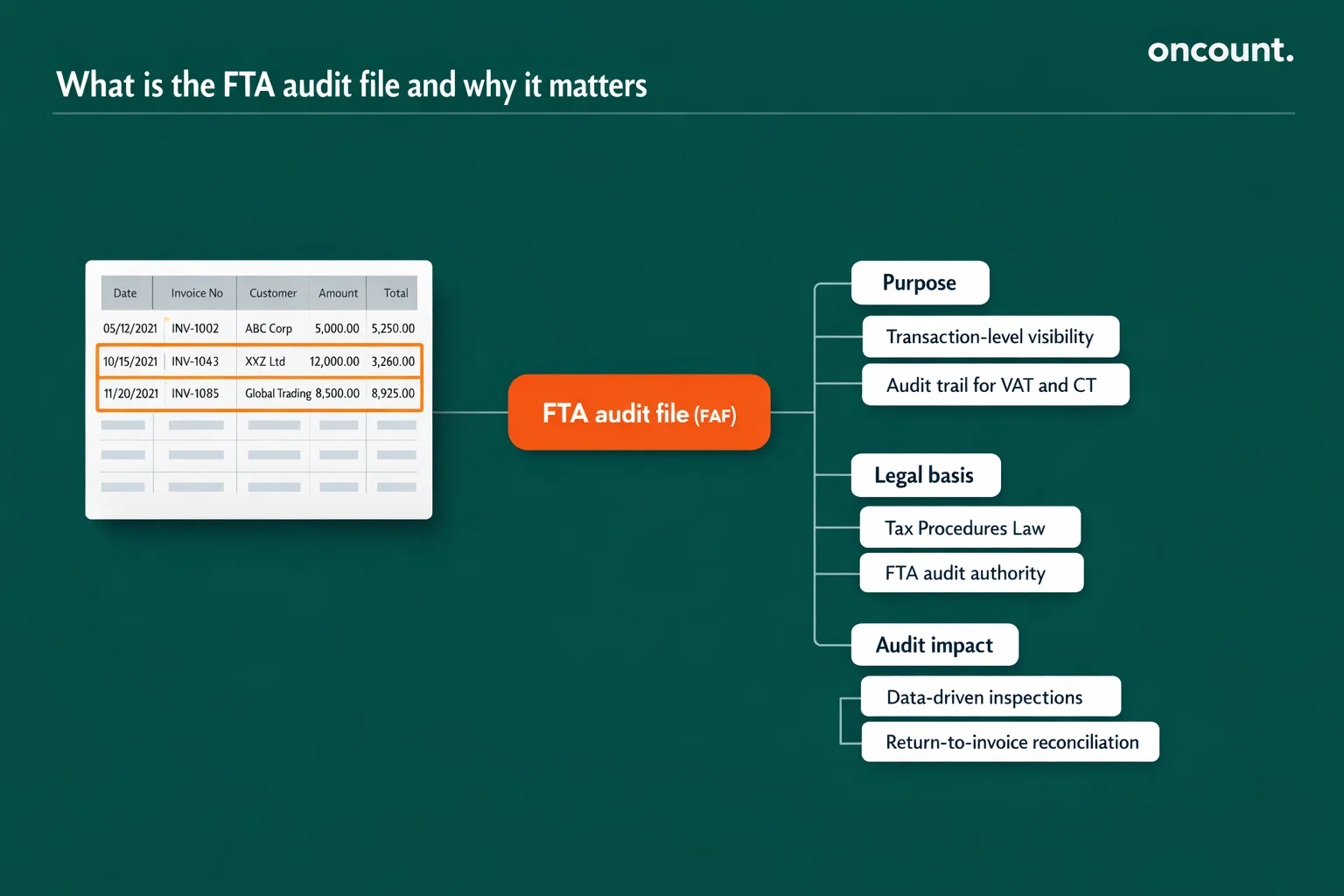

What Is the FTA Audit File and Why Does It Matter?

The FAF is a standardized electronic export of your business’s complete tax-relevant accounting history for a specific period. When the FTA initiates an audit, you will typically receive an audit notification requiring you to produce this file within a defined timeframe. The file must follow a prescribed format, most commonly a Comma Separated Value (CSV) file that meets strict technical specifications.

The legal foundation for this requirement comes from the Tax Procedures Law, which grants the FTA the power to audit any person to verify their tax obligations. The standardized format allows the authority to ingest data from thousands of different businesses into a single analytical engine, enabling advanced data analytics to identify discrepancies, anomalies, and potential tax evasion.

This level of transparency shifts the burden onto your business to ensure that every transaction is correctly categorized, calculated, and recorded. The FAF serves as your ultimate audit trail, linking the high-level figures on your tax return back to the specific source documents—invoices, credit notes, and customs declarations—that justify them.

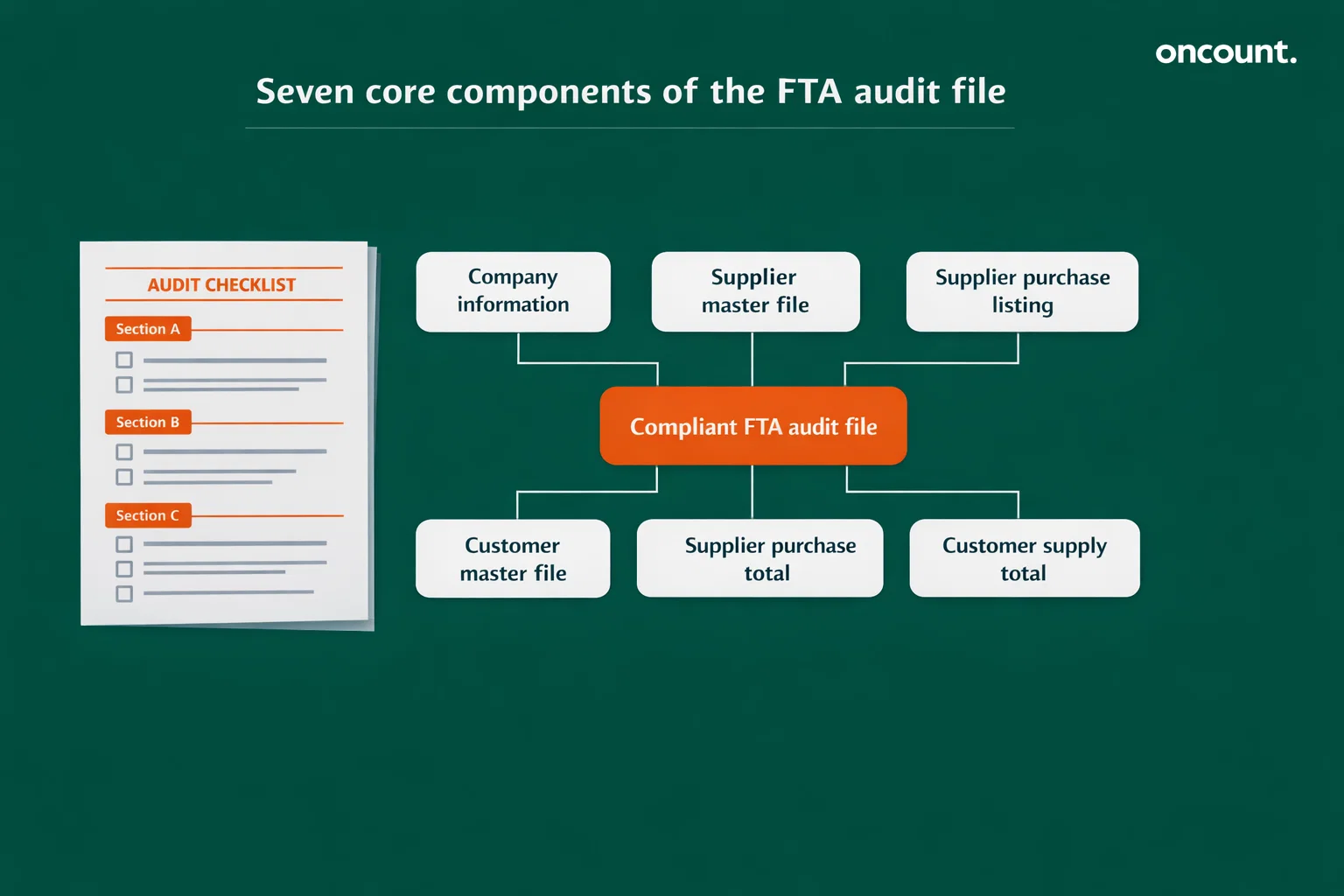

The Seven Core Components of a Compliant FTA Audit File

A compliant FAF follows a rigid schema, currently identified as version 1.0.0 in the UAE context. The file is structured into seven distinct sections that work together to provide FTA auditors with a complete view of your business activities:

| Section Name | Primary Function | Critical Data Elements |

| Company Information | Identification of the taxable entity and its authorized representatives | Legal Name (English/Arabic), TRN, Tax Agent Details (TAN/TAAN), Period Start/End, Software Version |

| Supplier Master File | A directory of all vendors with whom the business has transacted | Supplier Name, TRN, Location (Emirate/Country), Internal GL ID |

| Supplier Purchase Listing | Transaction-level details of all expenses and imports | Invoice Date, Invoice No, Line No, Description, Currency, Net Value, VAT Amount |

| Supplier Purchase Total | Aggregate totals for the purchase listing to ensure mathematical integrity | Total Purchase Value (AED), Total VAT (AED), Transaction Count |

| Customer Master File | A directory of all clients and customers | Customer Name, TRN, Location, Indicator for Zero-Rating/Out of Scope |

| Customer Supply Listing | Transaction-level details of all sales and exports | Invoice Date, Invoice No, Customer TRN, VAT Code, Converted AED values |

| Customer Supply Total | Aggregate totals for the supply listing | Total Supply Value (AED), Total VAT (AED), Transaction Count |

The Company Information section identifies your entity and authorized representatives, capturing your legal name in both English and Arabic, your Tax Registration Number (TRN), any registered tax agent details including their Tax Agent Authorization Number (TAAN), the audit period start and end dates, and the accounting software version you use.

The Supplier Master File creates a directory of all vendors with whom you have transacted. For each supplier, you must record their name, TRN if they are UAE-registered, their location by Emirate or country, and your internal General Ledger identification code for that vendor.

The Supplier Purchase Listing provides transaction-level details of all your expenses and imports. Each line must include the invoice date, invoice number, line number for multi-item invoices, description of goods or services, currency used, net value, and VAT amount. This granular detail allows auditors to verify that you are only claiming input tax recovery on eligible purchases.

Technical Requirements: Data Encoding and Formatting Standards

Because the UAE is a bilingual jurisdiction, the FAF often requires data in both English and Arabic. This necessitates the use of UTF-8 encoding for the CSV file. UTF-8 is the global standard for representing characters from multiple languages, ensuring that Arabic script is not corrupted during the export or import process.

The CSV format must comply with established standards such as RFC 4180, where records are delimited by line breaks and fields are separated by commas. A significant technical nuance in the UAE FAF is the handling of commas within text fields. If a company name or product description contains a comma, systems like Microsoft Dynamics 365 are configured to replace it with a semicolon to prevent the file structure from breaking.

Critical Field-Level Requirements That Auditors Scrutinize

The efficacy of an FTA audit often hinges on the precision of specific data fields within these tables. The UAE Federal Tax Authority looks for consistency between the FAF, the General Ledger, and the physical source documents.

In a complex ERP environment, a single invoice might contain hundreds of line items, each with different tax treatments. For example, a construction firm might purchase both taxable materials and exempt insurance on a single supplier invoice. The FAF requires a Transaction ID that serves as a unique reference to the accounting entry and a Line Number to distinguish individual items within that transaction. This level of detail allows the FTA to perform automated tests, ensuring that input tax is only claimed on items that are legally eligible for recovery.

While the UAE allows businesses to transact in any currency, all tax reporting must be in UAE Dirhams (AED). The FAF is particularly rigorous in this regard, requiring the capture of the Actual Currency and the Converted AED amount for both the net value and the VAT amount. The conversion must be based on the exchange rates published by the UAE Central Bank at the time of the supply. Any deviation from these rates can lead to under-reporting of tax and the subsequent imposition of penalties for incorrect tax returns.

Since 2023, the UAE has implemented specific reporting requirements for e-commerce and supplies made across different Emirates. The FAF captures the Location of both suppliers and customers, requiring the specific Emirate if the transaction is within the UAE. This allows the FTA to verify that the revenue is correctly allocated for economic planning and that businesses are correctly applying rules related to Designated Zones, which have unique VAT treatments.

Configuring Your Accounting Software for FTA Audit Readiness

The generation of a FAF is rarely a manual process. The complexity of the data requirements means that businesses must rely on their accounting software to produce the file automatically. The FTA maintains a list of accredited software providers, but even with compliant software, the initial configuration is critical.

For a system like Oracle NetSuite, SAP, or Microsoft Dynamics to produce a valid FAF, several essential onboarding tasks must be completed. These tasks align the internal accounting logic with the FTA’s external reporting requirements and ensure compliance with FTA regulations.

The system must enable Account Numbers, as the FAF relies on numeric Account IDs to identify lines in the General Ledger. Systems must be configured to use a standardized Chart of Accounts where every tax-relevant account is clearly numbered. GL Audit Numbering is another critical feature that ensures once an accounting period is closed, the transaction numbers remain immutable. This provides the auditor with a sealed record of the period’s activities, preventing retrospective changes that could be used to hide tax liabilities.

VAT Code Mapping requires that every transaction be tagged with a VAT code that maps to the FTA’s categories, including Standard, Zero, Exempt, and Reverse Charge. Software like TallyPrime or Zoho Books automates this by applying rates based on the item category and customer type. The system must also be capable of storing and exporting the legal name of the entity in Arabic script, utilizing the correct character encoding to ensure the FAF is readable by the FTA portal.

The Evolution Toward SAF-T Standards

As businesses look toward 2026 and 2027, the technical landscape is shifting. Microsoft Dynamics 365 has deprecated its older FAF format in favor of a “FAF in TXT (AE)” format that utilizes SAF-T (Standard Audit File for Tax) general model mapping. SAF-T is an international standard developed by the OECD for the electronic exchange of accounting data.

This transition indicates that the FTA is moving toward more complex, multi-dimensional data models that will facilitate even faster and more automated audits in the future. Businesses should work with their tax consultant or corporate tax consultant to understand how these changes will affect their audit file preparation processes.

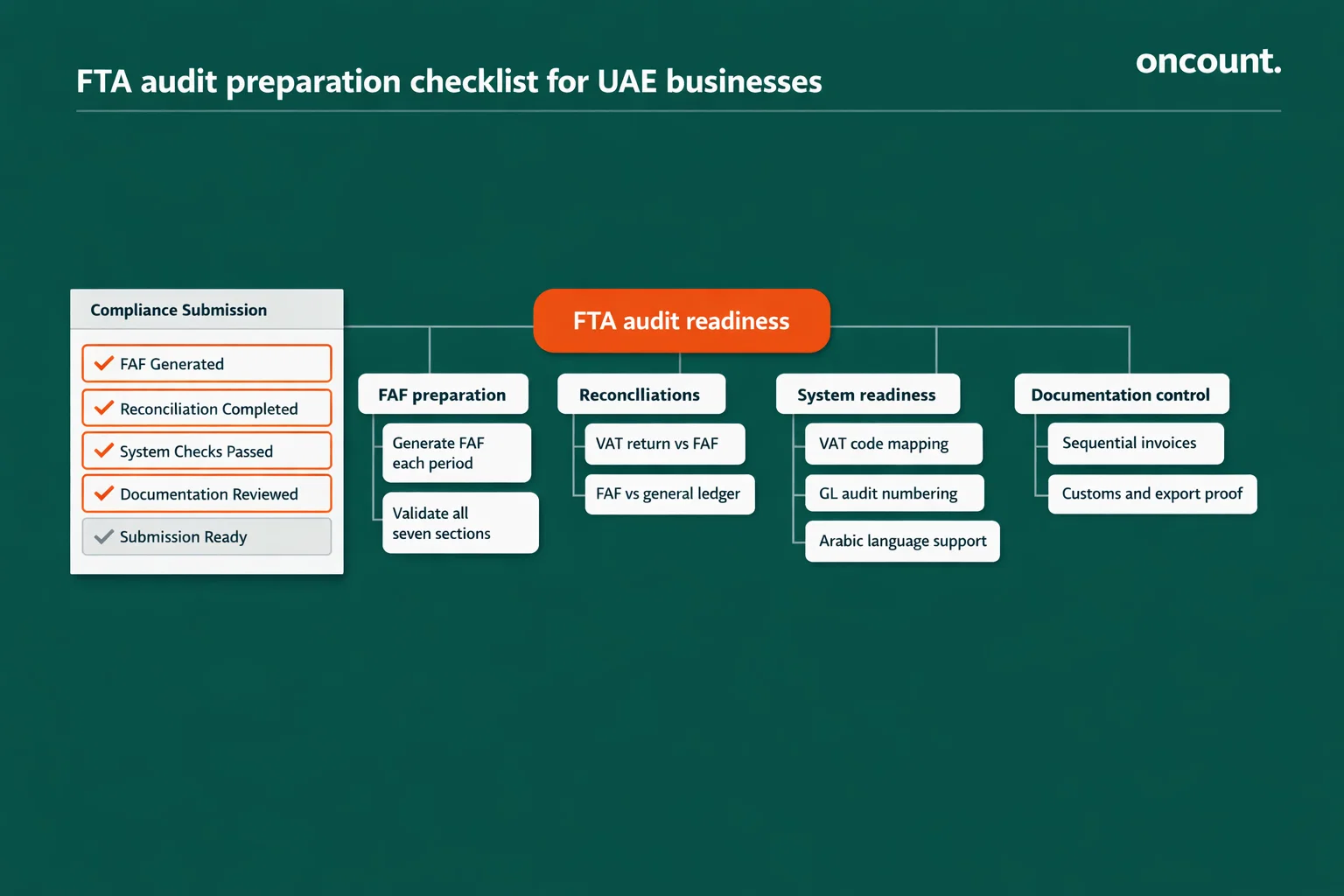

The Internal Audit Cycle: Preparing Before the FTA Notification Arrives

An audit is won or lost in the months before the notification arrives. Proactive businesses implement a closed-loop compliance cycle where the FAF is generated and reviewed internally at the end of every tax period. This approach to ensuring compliance with tax regulations transforms the audit file from a reactive requirement into a proactive diagnostic tool.

Critical Reconciliations Between VAT Return and Audit File

The most important step in preparation is the reconciliation between the summary VAT 201 return and the transaction-level FAF. This ensures that every dirham reported on the return is accounted for in the audit file:

| Reconciliation Type | Objective | Common Discrepancy Causes |

| VAT Return vs. GL | Ensure that the output tax reported in Boxes 1-5 matches the movement in the Sales Tax Payable accounts | Manual journal entries, deferred revenue, or timing differences between the invoice date and the accounting date |

| Input Tax vs. Purchase Listing | Verify that every claim for input tax recovery is supported by a valid tax invoice in the FAF | Missing supplier TRNs, non-compliant invoice formats, or RCM entries that were not reversed correctly |

| FAF Totals vs. Return Boxes | Mathematical confirmation that the sum of the Customer Supply Listing equals the values reported in the return | Rounding differences, currency conversion errors, or transactions tagged with out of scope codes mistakenly included in the return |

| VAT Return vs. P&L | Ensure consistency between the revenue reported for tax purposes and the revenue in the financial statements | Non-operating income, dividends, or adjustments made during the year-end statutory audit |

The FTA auditor will select a sample of transactions from the FAF and request the original source documents. Businesses must ensure they have sequential numbering for all sales invoices, as these must be issued in a sequential order. Gaps in the sequence can trigger a deeper investigation into potential unrecorded sales.

For zero-rated exports, the FAF entry must be supported by customs declarations, airway bills, and shipping documents. Without these, the zero percent rate will be disallowed and five percent tax will be assessed. For businesses handling goods, the FTA may perform a physical stock count and reconcile it against the inventory records and the purchase and sales listings in the FAF.

Submitting Your Audit File Through the EmaraTax Portal

The EmaraTax portal is the primary gateway for all interactions with the FTA. During an audit, the portal provides the interface for uploading the FAF and other mandatory documents. The submission process is rigorous and requires careful attention to detail to avoid technical rejections.

The user logs into EmaraTax using their credentials or UAE Pass and navigates to the relevant TRN dashboard. Under the VAT or Corporate Tax section, the user will find the audit notice. This section typically opens a submission window where the FAF and supporting schedules can be uploaded.

Documents must be in PDF, JPG, or PNG format, while the FAF must be in CSV. A critical constraint is the five megabyte file size limit for individual attachments. Large audit files may need to be compressed or split according to the auditor’s instructions. For Corporate Tax purposes, EmaraTax requires the manual input of certain financial data alongside the upload of the full audited financial statements. This data must perfectly align with the figures in the FAF.

Before the final submission, the user must review a summary of the uploaded data. This is the last chance to catch errors. The system often has built-in validation checks to identify obvious formatting issues. The FTA may request additional documentation or clarification during the FTA review process, so businesses should remain responsive throughout the audit process to ensure a clear audit outcome.

Working with a Registered Tax Agent

The FTA allows businesses to appoint a registered tax agent to handle the audit process. The tax agent acts as a professional intermediary, ensuring that the FAF is technically compliant and that the business’s positions are well-defended during the inspection. The portal requires valid proof of authorization, such as a Power of Attorney or a board resolution, for any person submitting records on behalf of the company.

A qualified tax advisor can provide invaluable support in preparing for an FTA audit, particularly for businesses with complex transactions, multiple tax registrations, or those operating in specialized sectors. They can also help with input tax apportionment calculations and ensure full compliance with FTA audit requirements.

Understanding the Penalty Landscape and How to Mitigate Risks

Non-compliance with FAF requirements or failure to facilitate an audit can result in severe financial and operational consequences. The UAE has harmonized its penalty regime to ensure consistency across VAT and Corporate Tax. These penalties are designed to be punitive for negligence while rewarding proactive disclosure.

Failure to maintain tax records results in a penalty of ten thousand dirhams for the first offense and twenty thousand dirhams for repeat violations. This applies if the business cannot produce the FAF or the underlying invoices for five or more years. Failure to facilitate an audit carries a twenty thousand dirham penalty, imposed for refusing access to premises, staff, or systems during a field audit.

The FTA has the right to demand Arabic versions of any English document. Failure to provide records in Arabic can result in penalties ranging from five thousand to twenty thousand dirhams. If the audit reveals that the FAF data does not match the return, this triggers an incorrect tax return penalty of one thousand dirhams for the first offense and two thousand dirhams for repeat violations.

If the audit results in a tax assessment showing underpaid tax, late payment penalties accrue from the original due date. For VAT, this is two percent immediately plus four percent monthly, while for Corporate Tax it is fourteen percent annually.

The Strategic Value of Voluntary Disclosure

The UAE tax system incentivizes businesses to correct their own mistakes. If an internal audit reveals an error before the FTA notifies the business of an audit, a Voluntary Disclosure should be filed. A voluntary disclosure submitted before notification attracts significantly lower percentage-based penalties, ranging from five percent to forty percent based on the time elapsed, compared to the fifty percent fixed penalty plus monthly interest applied if the FTA discovers the error during an audit.

For errors exceeding ten thousand dirhams in tax adjustments, a voluntary disclosure is mandatory and must be filed within twenty business days of the discovery. This approach demonstrates good faith and can significantly reduce the financial impact of any tax compliance issues.

What Triggers an FTA Audit? Understanding the Risk-Based Approach

The FTA does not conduct audits randomly. Instead, it uses a risk-based approach, leveraging its ISO 31000 certification for risk management. Understanding what triggers an audit allows businesses to prioritize their FAF preparation and maintain audit readiness throughout the year.

Any business requesting a large VAT refund will likely face a desk audit where the FAF for that period is closely scrutinized. Sharp fluctuations in profit margins or revenue that do not align with sector peers can trigger an investigation. Engaging in high volumes of imports and exports or related-party transactions without proper Transfer Pricing documentation is a major red flag for FTA compliance reviews.

A pattern of late returns or payments suggests poor internal controls, making the entity a prime candidate for a field audit. With the implementation of Corporate Tax, the FTA now reconciles the two tax filings. If the turnover reported for VAT does not match the accounting income for Corporate Tax, an audit is highly probable. This makes it essential for businesses to maintain consistency in their tax filings across both the VAT and UAE Corporate Tax regimes.

The FTA may conduct targeted audits focusing on specific industries or transaction types. For example, businesses in real estate, construction, or those claiming significant input tax on exempt supplies may face increased scrutiny. Understanding your risk profile helps you prepare for an FTA audit more effectively.

Advanced Considerations for Complex Business Structures

For multinational enterprises or those in specialized sectors, FAF preparation involves additional layers of complexity that require careful attention to ensure compliance with tax laws and FTA audit requirements.

Qualifying Free Zone Persons (QFZPs) are subject to a zero percent Corporate Tax rate on qualifying income, but this privilege is contingent upon maintaining adequate substance and audited financial statements. For these entities, the FAF must clearly distinguish between Qualifying and Non-Qualifying income. Auditors will look for a detailed Product File that justifies the zero percent treatment for specific supplies.

Entities in the real estate sector must maintain records for fifteen years, as tax adjustments can occur long after the initial sale or construction. The FAF for these entities must include specific Permit Numbers and land title deed details to justify the VAT treatment. For example, the first supply of residential buildings is zero-rated, and proper documentation is essential to defend this treatment during an audit.

Businesses with registrations across multiple Emirates or those utilizing e-commerce platforms must ensure their FAF is capable of breaking down sales by Emirate. This is critical for the allocation of tax revenue and for compliance with the e-commerce supply rules that mandate reporting based on the location of the customer.

For businesses that are part of tax groups, the FAF must clearly delineate transactions between group members and external parties. The FTA auditors may examine whether intra-group supplies are correctly accounted for and whether the group has properly applied the tax law provisions related to related-party transactions.

Your FTA Audit Checklist: Essential Steps to Prepare for an FTA Audit

To approach your FTA tax audit with confidence, businesses should implement a comprehensive audit checklist that covers all aspects of preparation. This detailed FTA audit checklist ensures that when the FTA notification arrives, your business is fully compliant with FTA regulations and ready to respond.

Generate your FAF internally at the end of each tax period and review it for completeness and accuracy. Verify that all seven sections are populated correctly and that the file passes basic validation checks. Reconcile your VAT return against the FAF totals to identify any discrepancies before the FTA review begins. Ensure that every transaction in the Customer Supply Listing and Supplier Purchase Listing can be traced back to a source document.

Verify that all supplier and customer TRNs are correctly recorded and that location information specifies the correct Emirate for UAE-based entities. Confirm that currency conversions use the UAE Central Bank rates applicable at the time of each transaction. Review your tax calculations to ensure that the correct VAT codes have been applied to each transaction based on the nature of the supply and the status of the customer.

Ensure that your accounting system is configured with the necessary features enabled, including account numbering, GL audit numbering, and Arabic language support. Maintain organized digital and physical files of all tax invoices, credit notes, customs declarations, and supporting documentation. Implement sequential invoice numbering and investigate any gaps in the sequence before the audit begins.

For businesses dealing with imports and exports, organize all customs documentation, airway bills, and shipping records to support zero-rated treatment claims. Conduct periodic internal audits to test the accuracy of your tax records and identify potential issues before the official FTA audit process begins. Consider engaging a corporate tax consultant or tax advisor to conduct a pre-audit review and provide recommendations for improvement.

Conclusion: Building a Culture of Tax Compliance in the UAE

Navigating an FTA inspection is a process of proving that your business’s financial reporting faithfully represents its economic reality. The FAF is the primary instrument of this proof. Successful preparation requires a multi-disciplinary approach that combines technical system configuration, rigorous accounting reconciliations, and strategic legal awareness.

By viewing the FAF not as a burden but as a diagnostic tool for internal health, businesses can identify and correct inefficiencies in their accounting processes long before an FTA auditor arrives. In an increasingly digitalized tax environment, the entities that thrive will be those that embrace the transparency of the FAF, leveraging it to build trust with the tax authorities and maintain a flawless record of compliance.

The transition to international standards like SAF-T and the integration of Corporate Tax only reinforce the necessity of a technically sound, reconciled, and bilingual audit file as the ultimate safeguard against the financial and reputational risks of non-compliance. When the audit begins, businesses that have invested in proper systems, maintained meticulous tax records, and implemented regular internal reviews will be positioned to navigate the official FTA audit process with confidence and emerge fully compliant with the tax system in the UAE.