Understanding the Legislative Framework for Bookkeeping Audits

The necessity for a bookkeeping audit is fundamentally anchored in several key pieces of legislation that form the bedrock of the UAE corporate governance framework. Federal Decree-Law No. 32 of 2021, known as the Commercial Companies Law, explicitly requires all companies whether operating on the mainland or within free zones to maintain systematic accounting books that accurately reflect their financial position and transactions.

These records must typically be kept at the company’s registered office for a minimum of five years, though the introduction of Corporate Tax has extended certain requirements. Under Article 56 of the Corporate Tax Law, taxable persons are legally obligated to maintain financial records and supporting documentation for seven years following the end of the relevant tax period.

The regulatory framework is not merely concerned with the existence of records but with their qualitative integrity. The transition to International Financial Reporting Standards has become mandatory for most entities, ensuring transparency and consistency in financial reporting. When a business finds its internal records diverging from these global standards, or when it struggles to reconcile historical data with current transactional realities, it has reached a critical juncture where professional accounting and bookkeeping services become essential.

Key Regulatory Requirements for UAE Businesses:

| Regulatory Framework | Legal Reference | Retention Period | Primary Requirement |

| Commercial Companies Law | Federal Decree-Law No. 32 of 2021 | 5 Years minimum | Accurately reflect financial position |

| UAE VAT Law | Federal Decree-Law No. 8 of 2017 | 5 Years (15 for Real Estate) | Retain all tax invoices and ledgers |

| Corporate Tax Law | Federal Decree-Law No. 47 of 2022 | 7 Years | Support all tax return information |

| Anti-Money Laundering | Federal Decree-Law No. 20 of 2018 | 5 Years minimum | Evidence of risk management and KYC |

Ten Critical Signs Your Business Needs a Bookkeeping Audit

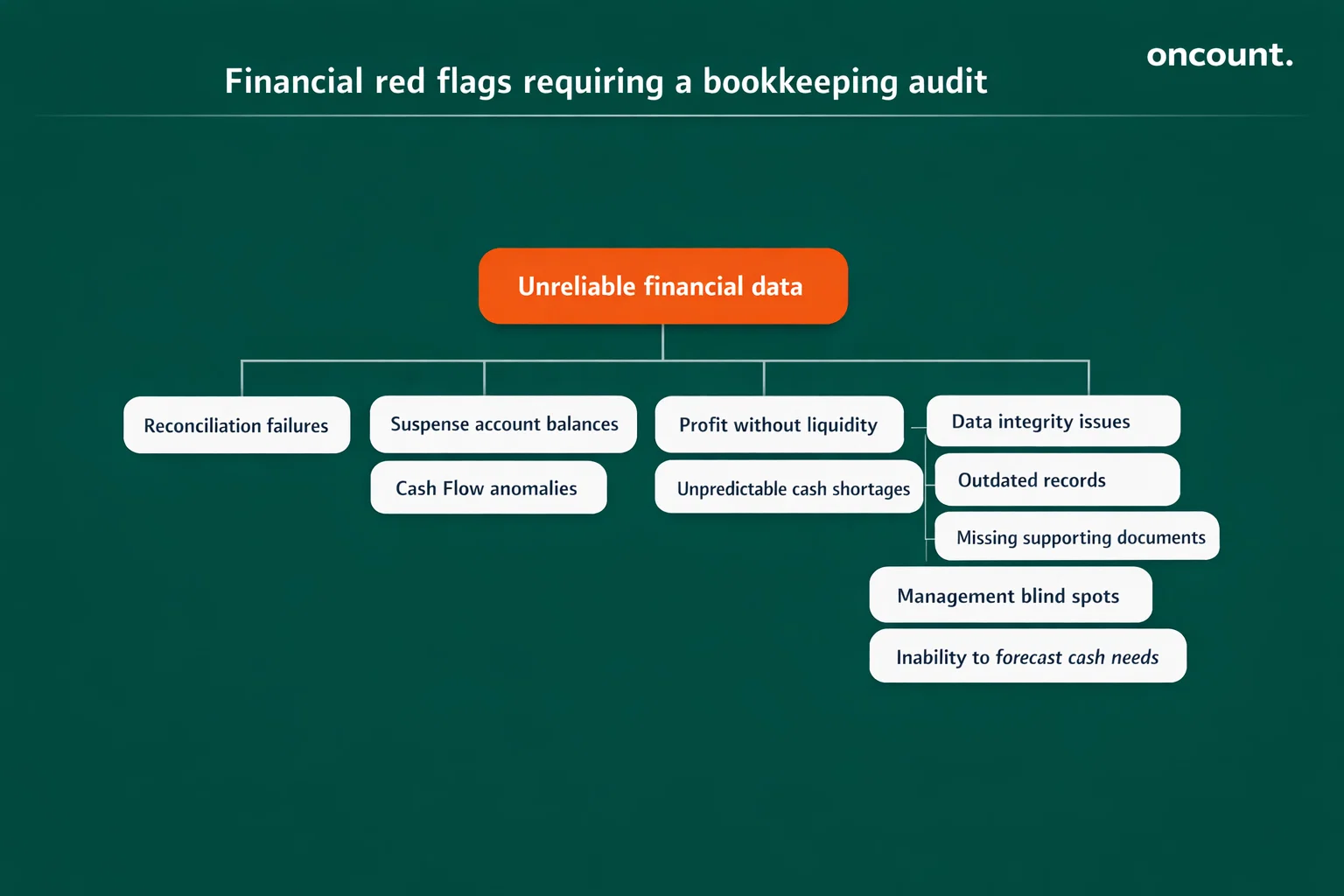

Persistent Unexplained Financial Discrepancies

When your company’s financial statements begin to exhibit unexplained variances such as mismatches between the general ledger and bank statements or discrepancies in asset valuations, it indicates a fundamental breakdown in the reconciliation process. In the UAE context, where businesses in Dubai and across the Emirates often handle high-value transactions across multiple currencies and bank accounts, these gaps can widen rapidly and create compounding errors that become increasingly difficult to unravel over time.

A lack of accuracy in the trial balance or balance sheet represents a clear signal that a comprehensive review is necessary to identify the root cause of these inconsistencies. These errors frequently accumulate in general or miscellaneous expense accounts, which become repositories for transactions that staff members do not know how to categorize properly. The presence of significant unexplained balances in suspense accounts or clearing accounts that remain unresolved for extended periods serves as a definitive indicator that your accounting infrastructure requires professional intervention.

The mathematical integrity of financial statements depends on a rigorous reconciliation process that verifies every transaction against supporting documentation. When this process breaks down, the resulting discrepancy can manifest in multiple ways including inventory valuation errors, unrecorded liabilities, or misstatement of accounts receivable. For any business owner facing these challenges, it is time to engage professional bookkeeping services in Dubai to restore order and ensure that your financial records are accurate and compliant with UAE tax laws.

Chronic Cash Flow Volatility Despite Apparent Profitability

A business that appears profitable on paper but consistently faces unexpected cash shortages suffers from a fundamental disconnect between its accounting records and its financial reality. This situation typically arises from unrecorded expenses, improper accruals, or a failure to track accounts receivable effectively. The confusion between profit and cash flow is particularly prevalent among small business operators and startups that neglect monthly reconciliations and fail to implement robust cash management protocols.

Poor cash flow management manifests in bounced checks, overdraft charges, and strained relationships with suppliers. These operational symptoms represent common bookkeeping mistakes that signify the need for professional oversight and systematic correction. When management cannot accurately predict cash requirements for the upcoming month or quarter, it suggests that the accounting system fails to capture the timing of cash inflows and outflows with sufficient precision.

This predictive failure often stems from inadequate accrual accounting practices, failure to maintain an aged receivables report, or inconsistent recording of credit terms with suppliers. The mathematical relationship between liquid assets and short-term obligations is expressed through the current ratio, where a declining trend despite stable sales indicates underlying problems. Many businesses in the UAE find that partnering with experienced accountants in Dubai helps them establish the cash flow and financial controls necessary to maintain operational stability while running your business efficiently.

Outdated or Incomplete Record-Keeping Systems

As businesses evolve and expand their operations, their bookkeeping infrastructure must align with their growth trajectory. If records are incomplete, outdated, or lack proper reconciliation, an audit becomes crucial to bring the books up to current operational standards. Inaccurate records not only impact internal decision-making but also jeopardize tax filings under the new Corporate Tax regime, which demands strict adherence to IFRS standards for financial instruments and revenue recognition.

The transition from manual record-keeping or basic spreadsheet systems to proper accounting software represents a critical evolution point for growing businesses. However, many companies in Dubai continue operating with legacy systems that cannot generate the comprehensive financial data required by modern regulators. When a business finds itself struggling to locate supporting documents for transactions that occurred even a year ago, it signals that the audit trail has been compromised and that immediate remediation is necessary.

For businesses without dedicated internal accounting teams, the challenge of maintaining current and compliant records becomes even more acute. Professional accounting and bookkeeping services can implement systematic record-keeping protocols that ensure all financial records remain accessible, organized, and compliant with both VAT and Corporate Tax requirements while supporting effective business decisions based on reliable financial information.

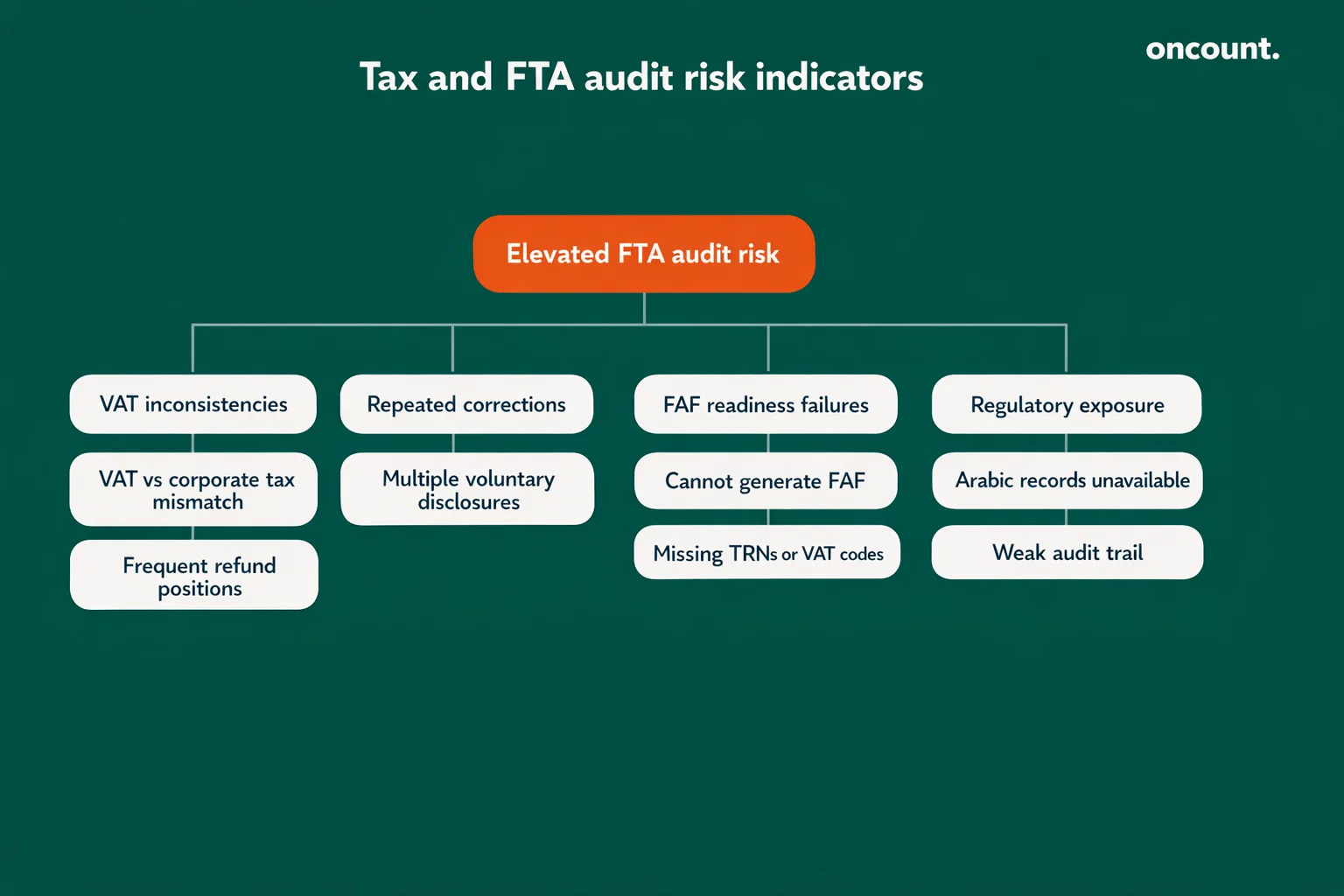

Inconsistencies Across Different Tax Filings

A major red flag for the Federal Tax Authority is the presence of mismatched data between VAT returns and Corporate Tax filings. If the revenue reported in quarterly VAT filings does not align with the annual turnover declared for Corporate Tax, the FTA’s automated risk-assessment systems will prioritize that entity for an inspection. These discrepancies often arise from incorrect revenue recognition or a failure to properly account for intercompany transactions and related-party deals, which must always follow the arm’s length principle.

The legal burden of proof remains with the taxpayer during any FTA inspection. The inability to produce organized, verifiable records can lead to tax assessments based on estimates, which are almost invariably to the business’s disadvantage. When your business operations span multiple tax regimes and filing requirements, maintaining consistency across all submissions becomes paramount to avoiding regulatory scrutiny and potential penalties.

Common VAT Audit Triggers and Solutions:

| Audit Trigger | Bookkeeping Root Cause | Strategic Mitigation |

| Frequent Refund Positions | Improper input VAT recovery | Quarterly internal VAT health checks |

| Mismatched Customs Data | Failure to reconcile imports | Link Customs TRN with ledger entries |

| Blocked Input Claims | Misclassified entertainment expenses | Strict expense policy and chart of accounts mapping |

| Zero-Rated Supply Gaps | Missing export documentation | Digital archiving of shipping documents |

High Frequency of Voluntary Disclosures and Amendments

While the UAE allows businesses to correct errors through Voluntary Disclosures, a pattern of multiple submissions across different tax periods suggests systemic issues in the accounting process. Frequent amendments imply that the internal review procedures are inadequate and that the finance team is operating without a standardized closing process at the end of each month or quarter.

Under the new penalty regime of Cabinet Decision No. 129 of 2025, while some Voluntary Disclosure penalties have been lowered to encourage compliance, the administrative burden of repeatedly correcting the books remains a significant hidden cost. Each correction requires staff time, disrupts normal business operations, and signals to regulators that your internal controls may be insufficient to ensure accuracy in the first instance.

When your business consistently discovers errors after filing returns, it indicates that pre-filing review procedures are either absent or ineffective. This pattern represents one of the top 5 signs your business needs professional intervention to establish robust month-end closing procedures and pre-filing verification protocols that catch errors before they reach regulatory authorities.

Concentration of Financial Authority Without Proper Segregation

When a single individual has exclusive control over the entire financial workflow from initiating payments to recording transactions and reconciling the bank accounts, the risk of internal fraud increases significantly. A bookkeeping audit is necessary to evaluate the internal control environment and ensure proper segregation of duties exists. This fundamental principle of accounting in the UAE requires that no single person should have complete control over all aspects of any financial transaction.

A key behavioral red flag in this context is an employee who refuses to take their annual leave or is overly protective of their work, as these are common tactics used to prevent the discovery of unrecorded transactions or ghost employees on the payroll. The concentration of authority creates opportunities for asset misappropriation that may go undetected for extended periods, causing significant financial damage to the organization.

High turnover in the finance function represents another major operational warning sign. A revolving door of staff in key management or accounting positions often points to toxic work culture, poor management, or inadequate compensation, but it also disrupts the institutional memory of the company’s finances. High turnover makes it difficult to maintain consistent record-keeping and leads to gaps in documentation that only surface during a tax audit or due diligence review. Professional accounting services in Dubai can provide the stability and oversight necessary to maintain proper internal controls even during periods of staff transition.

Inability to Generate Required FTA Audit Files

A critical technical indicator that a business needs a bookkeeping audit is its inability to generate an accurate FTA Audit File. The Federal Tax Authority may request this electronic file during a tax audit, and it must be provided in a specific CSV or XML format. The FAF serves as a consolidated digital record of all tax-related transactions, including invoices, payments, and credit notes.

If a business’s accounting software cannot generate a FAF that passes the FTA’s validation checks, it indicates that the underlying data is fragmented or missing essential metadata, such as supplier TRNs or correct tax codes. This technical failure is often a precursor to administrative penalties, which can start at AED 10,000 for failure to keep required records and escalate for repeated violations.

Critical FAF Data Requirements:

| Data Requirement | Common Failure | Resulting Audit Risk |

| Sequential Invoice Numbers | Manual entry outside the software | Suspicion of unrecorded revenue |

| TRN of Suppliers/Customers | Failure to collect certificates | Disallowed input VAT claims |

| Transaction ID Alignment | Inconsistent bank transfer naming | Inability to prove audit trail |

| Arabic Descriptions | Data stored only in English | Penalties up to AED 5,000 |

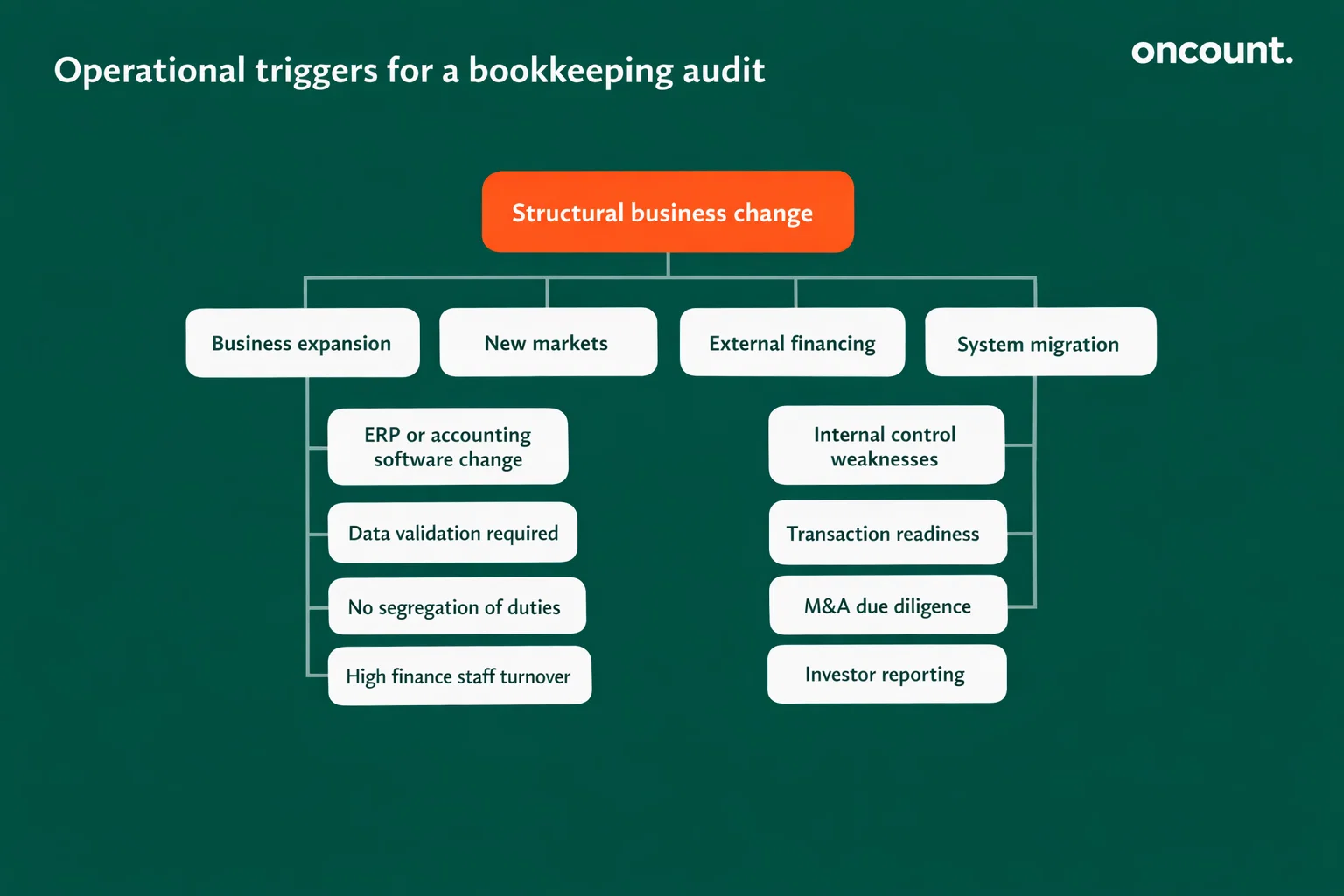

Planning Business Expansion Without Updated Financial Records

If a business is planning to scale operations or enter new markets within the Emirates without updating its financial records, it faces significant risk of financial mismanagement. Business expansion often requires substantial capital, and lenders or investors will invariably demand audited financial statements that depict the true state of the business. A bookkeeping audit assesses whether current processes are robust enough to support growth and provides the transparency needed to secure external funding.

Growing your business successfully requires reliable financial information that accurately reflects your current position and future capacity. When financial records lag behind operational reality, management makes decisions based on incomplete or inaccurate data, potentially committing resources to expansion initiatives that the business cannot sustain. This misalignment between ambition and financial capacity represents a critical juncture where professional audit services become essential.

The success of your business during expansion phases depends heavily on your ability to demonstrate financial health and operational capability to stakeholders. Banks, investors, and strategic partners all require confidence that your financial management systems can support increased transaction volumes and operational complexity. Engaging one of the top audit firms in UAE before embarking on significant expansion ensures that your foundation is solid and that growth initiatives are built on accurate financial information.

Migration to New Accounting Systems or Software

The decision to migrate from manual spreadsheets or basic accounting software to advanced cloud-based ERP systems represents a critical trigger for an audit. Migrating dirty data from an old system to a new one merely automates historical errors and embeds them deeper into your operational infrastructure. An audit before the migration ensures that opening balances are correct, historical transactions are properly categorized, and VAT codes are mapped according to current FTA guidelines.

Many businesses in the UAE underestimate the complexity of system migrations and the importance of data cleanliness. When you use accounting software to manage your business finances, the system’s output can only be as accurate as the input data it receives. Unreconciled bank feeds, duplicate vendor masters, inventory mismatches, and incorrect VAT mapping all represent technical red flags that must be addressed before committing to a new platform.

Software Migration Audit Requirements:

- Full bank reconciliation of the past twelve months to eliminate discrepancies

- Data deduplication and TRN verification for all vendor and customer masters

- Physical stock count and ledger alignment to correct inventory values

- Comprehensive mapping check of VAT codes including standard, zero-rated, and exempt categories

Professional accountants handle these complex migrations systematically, ensuring that the transition to new technology enhances rather than compromises your financial integrity. The investment in pre-migration audit work protects your business from embedding errors that could take years to identify and correct.

Sector-Specific Operational Anomalies

Certain industries face unique bookkeeping challenges that serve as specific warning signs. In real estate, discrepancies in escrow account management or failures in IFRS 15 revenue recognition represent critical audit triggers. Real estate developers and brokers operate in a complex regulatory environment governed by RERA and the FTA, where customer advances must be used solely for their intended projects and revenue recognition must align with the transfer of control to buyers.

In the hospitality sector, recurring variances between Point of Sale system recordings and actual bank deposits signal operational leakage or internal theft. Significant differences between recorded inventory and physical counts, known as inventory shrinkage, should immediately trigger a bookkeeping audit to evaluate mismanagement or theft in the supply chain. These high-volume cash environments require specialized controls that many businesses lack.

Professional services firms often struggle with project-based cost tracking and inconsistent billing practices. If revenue is recognized before it is earned such as recording the full value of a long-term project at the start, it inflates profits and misleads stakeholders. An audit helps align these recognition practices with IFRS standards and ensures that payroll and staff costs are correctly allocated to specific projects, providing accurate profitability analysis for business decisions.

Preparing for Mergers, Acquisitions, or Investment

In the UAE’s active mergers and acquisitions market, bookkeeping audits are frequently triggered during the due diligence phase. A buyer conducting due diligence will probe the target company’s financial integrity, earnings quality, and hidden legal exposures. Many businesses assume that if they have a standard statutory audit, their books are clean. However, a deeper bookkeeping audit often reveals hidden liabilities such as undisclosed guarantees, personal loans mixed with company funds, or unfunded End of Service Gratuity obligations.

For an acquirer, discovering these liabilities post-closing can trigger clawbacks or litigation that destroy the value of the transaction. Due diligence reviews now routinely test Ultimate Beneficial Owner transparency and corporate governance alignment. If the target company’s shareholder registers and Board resolutions do not align with the actual control structures of the firm, it represents a clear red flag that can derail transactions or significantly reduce valuations.

Whether you are selling your business, seeking investment, or planning a merger, the financial transparency provided by a comprehensive bookkeeping audit significantly enhances your negotiating position and transaction value. Investors and acquirers pay premium valuations for businesses with clean books and robust financial controls, while discounting or walking away from opportunities where financial records raise concerns about underlying business health or compliance risk.

Taking Action to Protect Your Business

The decision to conduct a bookkeeping audit should not be viewed as a reaction to crisis but as a proactive component of strategic financial management. For businesses operating in the UAE’s increasingly regulated landscape, the signs that indicate professional review is needed are often present long before the first penalty notice arrives. Recognizing these warning signs early and taking decisive action protects your business from escalating compliance risks while positioning you for sustainable growth.

An audit for structural integrity becomes essential when your business has experienced rapid growth or management changes. These transitions often disrupt established financial processes, requiring a comprehensive reset of the chart of accounts and verification of IFRS standards compliance. An audit for compliance readiness ensures that VAT returns reconcile with annual financial statements, avoiding the automated flags that trigger FTA scrutiny. An audit for technological reliability before system migrations prevents the automation of historical errors that could compromise financial reporting for years.

Most critically, an audit for fraud prevention in sectors with high transaction volumes or cash handling provides the most effective defense against financial leakage and asset misappropriation. In the contemporary UAE business environment, financial transparency serves as the primary currency of trust, and an audited ledger provides the foundation upon which sustainable growth is built. Whether you choose to engage an audit firm in Dubai or work with specialized bookkeeping services, the investment in professional review ensures that your financial records are accurate, your compliance posture is strong, and your business operations rest on a solid foundation of reliable financial information.