Understanding the UAE AML Regulatory Framework and KYC Requirements

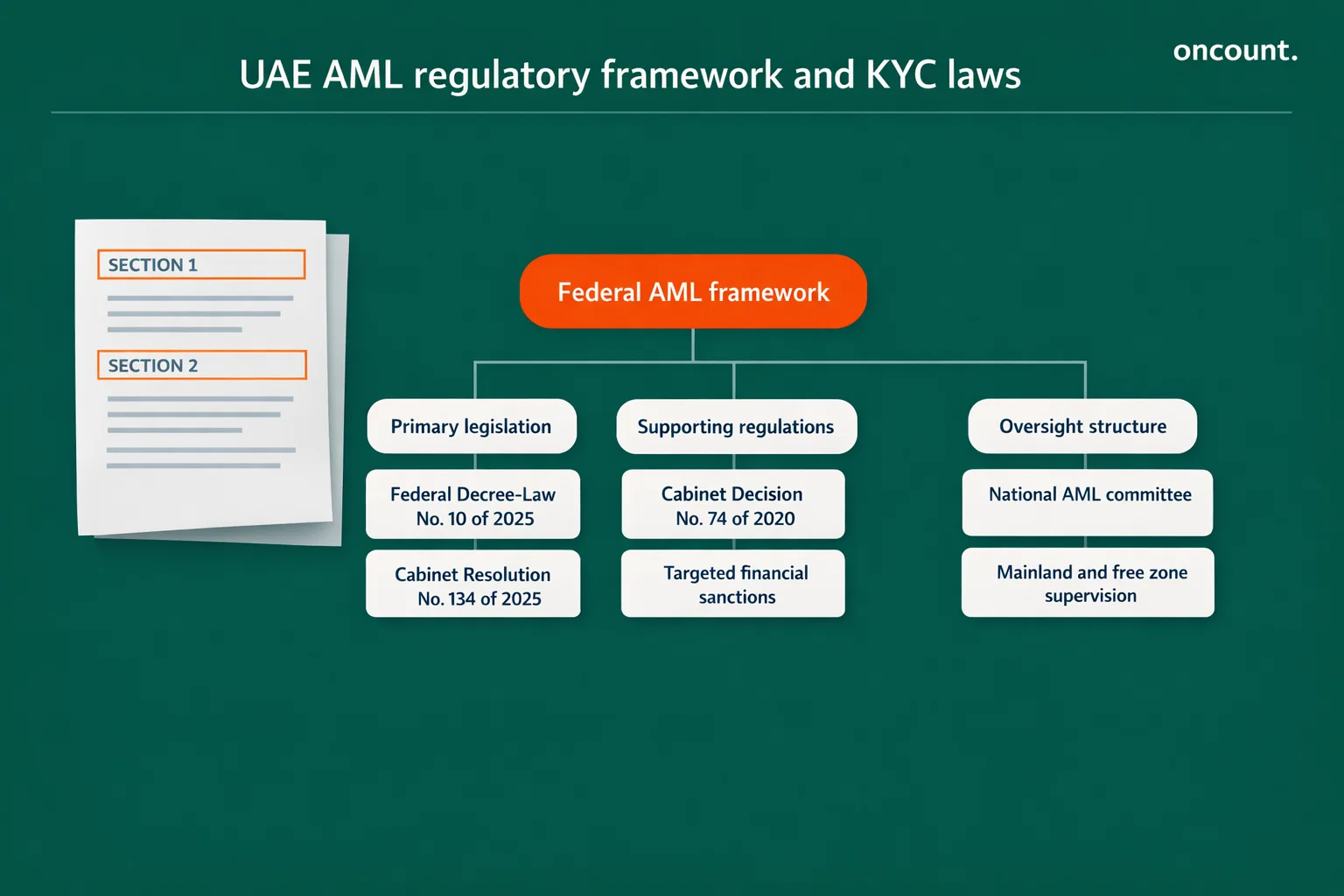

The current compliance architecture rests on multiple layers of federal legislation and executive regulations. Federal Decree-Law No. 10 of 2025 serves as the principal law governing anti-money laundering, combating the financing of terrorism, and counter-proliferation financing. This legislation works in conjunction with Cabinet Resolution No. 134 of 2025, which provides detailed implementation procedures, and Cabinet Decision No. 74 of 2020, which specifically governs targeted financial sanctions and adherence to United Nations lists.

Federal Decree-Law No. 7 of 2024 established critical governance structures including the National Committee to Combat Money Laundering and the Higher Committee Overseeing the National Strategy. These bodies coordinate federal efforts across all emirates and ensure consistent application of regulations in the UAE. The UAE employs a bifurcated oversight model that distinguishes between mainland entities and those operating within specialized financial free zones, ensuring that every business falls under appropriate regulatory supervision.

Key Federal AML/CFT Legislation Timeline:

| Legal Instrument | Effective Date | Current Status | Key Implications |

| Federal Law No. 4 of 2002 | 2002 | Repealed | Established early definitions of financial crimes |

| Federal Decree-Law No. 20 of 2018 | October 2018 | Repealed by 10/2025 | Introduced goAML system and DNFBP definitions |

| Cabinet Decision No. 74 of 2020 | 2020 | In Force | Governs Targeted Financial Sanctions |

| Federal Decree-Law No. 7 of 2024 | 2024 | In Force | Established Supreme Committee for AML/CFT |

| Federal Decree-Law No. 10 of 2025 | October 2025 | In Force | Principal law governing AML, CFT, and CPF |

| Cabinet Resolution No. 134 of 2025 | December 2025 | In Force | Implementing regulation for 2025 Federal Law |

For businesses seeking professional assistance in navigating these complex requirements in the UAE, expert business setup and compliance services can help businesses establish robust frameworks that meet all regulatory standards while streamlining the implementation process.

Identifying Your Supervisory Authority and Classification

A critical first step in the KYC process for businesses in the UAE is identifying the specific supervisory authority that regulates your operations. The Central Bank of the UAE maintains primary jurisdiction over Licensed Financial Institutions, including commercial banks, exchange houses, finance companies, and insurance providers. For entities involved in securities, the Securities and Commodities Authority oversees markets, listed companies, and brokerage firms.

The Ministry of Economy serves as the federal supervisor for the vast sector of Designated Non-Financial Businesses and Professions, ensuring that industries such as real estate, auditing, legal services, and corporate service providers adhere to national standards. These DNFBPs represent a particularly broad category designed to prevent the use of non-financial conduits for money laundering and terrorism financing.

Within the financial free zone areas, independent regulators operate under their own rulebooks while enforcing overarching federal laws and regulations. The Dubai Financial Services Authority regulates the Dubai International Financial Centre, and the Financial Services Regulatory Authority oversees the Abu Dhabi Global Market. Both authorities have developed sophisticated compliance frameworks that align with international best practices. The Virtual Asset Regulatory Authority represents a newer addition to the regulatory landscape, standardizing compliance for the rapidly expanding cryptocurrency and fintech sectors.

Reporting Entity Classifications:

Compliance requirements are categorized by the nature of business operations. Financial Institutions include banks, exchange houses, insurance companies, and money transfer operators licensed to conduct financial services. Designated Non-Financial Businesses and Professions encompass real estate brokers and agents when they facilitate property transactions, dealers in precious metals and stones when they engage in monetary transactions equal to or exceeding AED 55,000, independent legal professionals and notaries when they prepare transactions involving client funds, and Trust and Company Service Providers when they offer services such as company formation or nominee services. Virtual Asset Service Providers must comply when they facilitate the exchange, transfer, or management of digital assets.

Mandatory Registration on goAML and ARS: The First Step in the KYC Process

A fundamental requirement for every reporting entity in the UAE is registration on two critical national platforms: the goAML portal operated by the Financial Intelligence Unit and the Automatic Reporting System for Sanctions. Failure to complete these registrations is considered a material breach of federal law and can result in significant administrative fines ranging from AED 50,000 to AED 1 million, alongside potential license revocation.

The goAML system, developed by the United Nations Office on Drugs and Crime, is the primary integrated platform used by the FIU to receive, analyze, and disseminate Suspicious Transaction Reports and Suspicious Activity Reports. Registration is a two-stage technical process that requires precision to avoid rejection by the regulator.

Step-by-Step Guide to goAML Registration

The first stage is the Sanctions and Compliance Monitoring registration, which provides the gateway to the network. The entity must visit the official FIU website and select the appropriate registration type, usually designated as “Reporting Entity.” This stage requires the submission of a single PDF document not exceeding 5MB, which must include the entity’s trade license, an authorization letter for the appointed Money Laundering Reporting Officer, and copies of the MLRO’s passport, Emirates ID, and resident visa. Upon approval, the MLRO receives an email with a One-Time Password and a link to generate a Secret Key.

The second stage involves configuring the Google Authenticator application on a mobile device using the Secret Key. This application generates a rotating six-digit passcode that serves as the password for all future logins to the goAML portal. Once the Authenticator is set, the user proceeds to the final entity registration on the goAML website by selecting “Register New Organisation” and filling in exhaustive details about the business and its compliance structure. Successful registration results in the issuance of a unique Organisation ID, which must be safely stored for all subsequent regulatory filings.

Automatic Reporting System Registration for Sanctions Compliance

In parallel with goAML, entities must register with the Automatic Reporting System operated by the Executive Office for Control and Non-Proliferation. The ARS ensures that businesses receive immediate, automated notifications when names are added to or removed from the UAE Local Terrorist List or the UN Consolidated List. Registration involves subscribing to the Executive Office mailing list via their official website. The process is mandatory for all financial institutions and DNFBPs under Cabinet Decision No. 74 of 2020. By subscribing, the entity ensures it can conduct the legally required daily screening of its customer database against real-time data, thereby preventing the processing of financial transactions for sanctioned individuals or groups.

Implementing the Risk-Based Approach: Business and Customer Risk Assessment

The modern UAE compliance framework is predicated on the Risk-Based Approach, which requires entities to move away from checkbox compliance and toward a dynamic model where controls are proportionate to identified risks. This approach is enacted through two distinct assessment layers: the Business Risk Assessment and the Customer Risk Assessment.

The Business Risk Assessment, often termed the Enterprise-Wide Risk Assessment, is the foundational pillar that defines an organization’s overall risk profile. It involves a systematic evaluation of the inherent risk the business faces before any controls are considered. This assessment must be documented and reviewed annually or upon major regulatory changes. The methodology must analyze risks associated with the entity’s products and services, customer demographics, geographic exposure including operations in high-risk or sanctioned jurisdictions, and delivery channels such as non-face-to-face onboarding.

The assessment must take into account the findings of the UAE National Risk Assessment and relevant Sectoral Risk Assessments issued by the Ministry of Economy or other supervisors. After identifying inherent risks, the entity evaluates the effectiveness of its internal controls to determine the residual risk. If the residual risk exceeds the firm’s defined risk appetite, senior management must authorize additional mitigation measures to stay compliant with regulatory expectations.

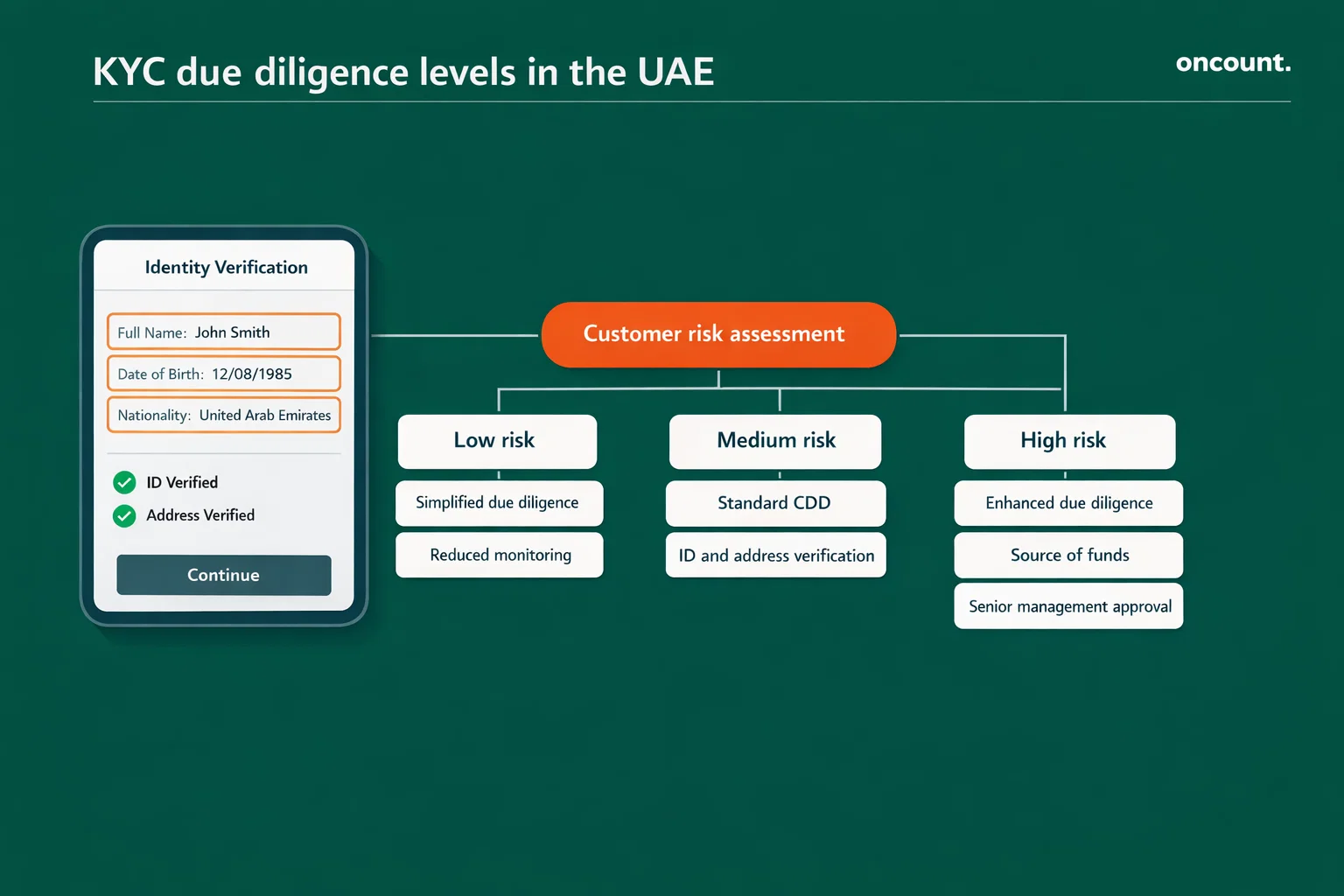

Customer Risk Assessment and KYC Verification

While the Business Risk Assessment evaluates the firm, the Customer Risk Assessment examines the individual or corporate client at the point of onboarding and throughout the business relationship. The assessment process results in a risk rating such as Low, Medium, or High that dictates the level of due diligence required.

The evaluation considers multiple risk factors. Customer-related factors include whether the client is a Politically Exposed Person, a non-resident, or a legal person with a complex ownership structure. Geographic factors involve checking if the client originates from a country on the FATF Grey or Black lists. Transactional factors examine whether the client engages in cash-intensive activities or unusually complex, large-value transactions that lack an apparent economic purpose. UAE businesses are required to maintain a scoring matrix to standardize these ratings and ensure consistency across their compliance operations.

Risk Parameter Framework:

| Risk Category | Examples of High-Risk Indicators | Expected Mitigation Measures |

| Geographic Risk | FATF blacklisted countries, sanctioned regions | Enhanced Due Diligence, transaction freezing |

| Customer Risk | PEPs, non-residents, high-net-worth individuals | Source of Wealth verification, management approval |

| Product/Service Risk | Virtual assets, high-value real estate, cash transactions | Strict threshold monitoring, blockchain forensics |

| Delivery Channel | Non-face-to-face onboarding, third-party introducers | Advanced liveness checks, biometric verification |

Customer Due Diligence: KYC Compliance and Verification Tiers

Customer Due Diligence represents the operational process of verifying the identity of customers and their beneficial owners. In the UAE, the intensity of CDD is scaled according to the risk rating assigned during the Customer Risk Assessment. Specialized jurisdictions like the Abu Dhabi Global Market explicitly define a three-tier system of due diligence that helps businesses verify customer identities in accordance with the requirements.

Standard KYC Procedures and Identity Verification

Standard Customer Due Diligence is the baseline requirement for all business relationships. For natural persons, this involves obtaining and verifying original, government-issued identification such as a passport or Emirates ID. The verification process must confirm the authenticity of these documents and match the information against the individual presenting them. Additionally, businesses must collect proof of address through utility bills, bank statements, or other official correspondence dated within the past three months.

For legal persons and arrangements, the entity must decode the legal form, verify the memorandum of association, and identify all relevant persons in senior management. This includes understanding the nature of the customer’s business or occupation, verifying the registered office address, and confirming the purpose and intended nature of the business relationship. These steps form part of their compliance obligations and ensure that only legitimate clients are onboarded.

Simplified Due Diligence is permissible only for customers assessed as Low Risk. Under this approach, entities may adopt reduced verification measures, such as verifying the identity after the relationship is established or conducting less frequent monitoring of transactions. However, Simplified Due Diligence is never allowed if there is a suspicion of money laundering or if the customer is from a high-risk jurisdiction. UAE regulations require businesses to document the rationale for applying simplified measures and obtain appropriate management approval.

Enhanced Due Diligence for High-Risk Customers and Politically Exposed Persons

Enhanced Due Diligence is mandatory for any customer rated as high-risk, including all Politically Exposed Persons, their family members, and close associates. EDD requires the entity to take extra steps to manage the heightened risk. These measures include obtaining senior management approval before establishing the relationship, identifying and verifying the Source of Wealth and Source of Funds through comprehensive documentation such as bank statements, tax returns, business ownership records, or inheritance documents, and conducting ongoing, intensified monitoring of the business relationship.

For Politically Exposed Persons, ongoing monitoring must be continuous to detect any changes in risk profile or transaction behavior. The enhanced scrutiny extends to understanding the origin of assets and wealth accumulation over time, particularly where the individual’s known income sources may not align with their transaction patterns. This level of diligence helps combat money laundering and terrorism by ensuring that bad actors cannot exploit the financial system through complex ownership structures or opaque transactions.

Ultimate Beneficial Ownership: Transparency Requirements for UAE Businesses

The identification of Ultimate Beneficial Owners is central to preventing the misuse of corporate vehicles for concealing illicit funds. Cabinet Decision No. 109 of 2023 on Regulation of Procedures Related to Real Beneficiaries provides the comprehensive framework for all mainland and commercial free zone companies. This regulation mandates that ownership must be traced through every layer of a corporate chain until the natural persons who ultimately own or control the entity are identified.

A UBO is defined as any natural person who directly or indirectly owns or controls twenty-five percent or more of the company’s capital or voting rights, or who has the right to appoint or dismiss the majority of the board of directors. If no person fits these criteria, the individual who exercises ultimate control through other means is designated as the UBO. If no natural person is identified after all reasonable steps, the natural person who serves as the senior manager is designated as the UBO.

Register Maintenance and Submission Requirements

Entities must maintain three distinct registers: a Register of Beneficial Owners, a Register of Partners or Shareholders, and a Register of Nominee Directors. These registers must be submitted to the registrar or licensing authority within sixty days of the company’s incorporation or the enactment of the law. Furthermore, any change to UBO information must be filed with the authority within fifteen days of the change occurring. Registrars such as the Dubai Department of Economy and Tourism, the DMCC, and the JAFZA utilize integrated e-services portals for these filings.

The registers must contain comprehensive information including the full name, nationality, date of birth, residential address, and Emirates ID or passport number of each beneficial owner. For corporate shareholders, the register must trace ownership through all intermediate entities until natural persons are identified. The failure to maintain accurate UBO registers or to update them within the prescribed timeline constitutes a serious violation that can result in penalties and potential license suspension.

The Money Laundering Reporting Officer: Qualifications and Responsibilities

The appointment of a Money Laundering Reporting Officer or AML Compliance Officer is a mandatory requirement for all reporting entities in the UAE. This individual is personally responsible for the organization’s adherence to AML laws and serves as the primary point of contact for the Financial Intelligence Unit and supervisory authorities.

The MLRO must be a natural person with sufficient seniority, authority, and independence to perform their duties without undue influence. For banks and financial institutions, the Central Bank of the UAE mandates specific experience thresholds: a minimum of three years for Category A licenses, and up to eight years or five years with professional certification for Categories B and C. Certifications such as Certified Anti-Money Laundering Specialist and International Compliance Association Diplomas are highly regarded benchmarks for expertise that help businesses implement KYC procedures effectively.

Legal Liabilities and Mandatory Reporting

Legal liability for the MLRO is significant. Under the 2025 federal law, if an MLRO knowingly fails to report a suspicious transaction or neglects to implement adequate AML systems, they may face personal criminal charges including imprisonment and hefty fines. The role requires a high degree of professional judgment and good faith in detecting transactions that may be linked to any felony or misdemeanor.

The MLRO is responsible for filing various reports via the goAML portal, including Suspicious Transaction Reports, Suspicious Activity Reports, and specialized reports such as the Funds Freeze Report and the Partial Name Match Report. Additionally, the MLRO must prepare an annual or semi-annual MLRO Report for senior management. This report must consolidate the firm’s AML risk profile, details of training sessions held, statistics on suspicious activity filings, and outcomes of internal compliance monitoring. In the Abu Dhabi Global Market and Dubai International Financial Centre, these reports are critical for regulatory reviews and are often requested during thematic inspections.

Targeted Financial Sanctions and Counter-Proliferation Financing

The UAE’s commitment to international security is codified in Cabinet Resolution No. 74 of 2020, which governs Targeted Financial Sanctions related to terrorism and the Counter-Proliferation Financing of weapons of mass destruction. Proliferation financing is explicitly recognized as an AML offense under Federal Decree-Law No. 10 of 2025, in line with FATF standards.

Reporting entities must continuously monitor their customer and supplier databases against the UN Consolidated List and the UAE Local Terrorist List. This screening is mandatory before customer onboarding and daily thereafter to regulate financial crime exposure. If a match is identified, the entity must immediately freeze all funds and assets of the listed person or entity without prior notice.

Freezing actions must be completed within twenty-four hours of a listing, and the entity must notify the supervisory authority within five business days. Reporting is done through the Funds Freeze Report on the goAML portal. The legislation prohibits tipping off, meaning the entity must not inform the customer that their assets have been frozen or that they are under investigation, as this is a criminal offense. This ensures that regulatory authorities can conduct proper investigations without alerting potential suspects.

Proliferation Financing Controls for Trade Businesses

For entities involved in trade and logistics, the Executive Office for Control and Non-Proliferation manages permits for strategic and dual-use goods. Compliance involves classifying goods against national control lists and ensuring that financial transactions do not facilitate the transfer of items to prohibited end-users in jurisdictions such as North Korea or Iran. AML frameworks must be integrated with export controls to identify red flags such as complex transshipment routes or end-uses that seem inconsistent with the client’s stated business.

Specialized Free Zone Requirements: DIFC and ADGM KYC Compliance

While federal law provides the baseline, the financial free zones of the Dubai International Financial Centre and Abu Dhabi Global Market have additional specific requirements and deadlines that businesses must navigate to maintain their licenses and stay compliant with local regulations.

Dubai International Financial Centre Requirements

Designated Non-Financial Businesses and Professions operating in the DIFC must register with the Dubai Financial Services Authority using the DNF1 Form and pay an annual registration fee, typically USD 3,000 for law firms, accounting firms, and company service providers. A paramount obligation is the submission of the Annual AML Return by September 30th each year. This return covers the period from August 1st of the previous year to July 31st and provides the DFSA with a comprehensive overview of the firm’s AML controls, customer risk profiles, and geographic exposure. Late submission results in a fixed penalty notice under Article 91 of the Regulatory Law.

Abu Dhabi Global Market Requirements

The ADGM’s Financial Services Regulatory Authority requires entities to maintain a Record of Beneficial Owners and file a Confirmation Statement annually via the ADGM Online Registry Solution. The ADGM mandates a strict twenty-five percent threshold for UBO identification and requires entities to assign a numerical or descriptive risk rating to every customer. Furthermore, ADGM entities must annually renew their Data Protection obligations and renew their commercial licenses by uploading valid office lease agreements and paying the required fees.

Key Filing Deadlines and Portals:

| Requirement | Jurisdiction | Deadline | Filing Portal |

| Annual AML Return | DIFC (DFSA) | September 30 | DFSA ePortal |

| Confirmation Statement | ADGM (FSRA) | Annual (within 28 days of anniversary) | ADGM Online Registry |

| UBO Change Update | Federal / All | Within 15 days of change | Local Registrar |

| goAML Registration | Federal / All | Immediate upon licensing | goAML (FIU) |

| Sanctions Screening | Federal / All | Daily | EOCN / Internal Software |

Training, Record Keeping, and Internal Controls to Help Businesses Stay Compliant

A robust AML program is not merely a paper policy but an active operational culture that ensures that businesses can combat money laundering and terrorism effectively. Regulatory authorities emphasize that training must be recurring and role-specific. New employees must receive anti-money laundering and combating terrorist financing training within thirty days of joining, and they are prohibited from serving customers independently until they complete this induction. Training materials must be updated regularly to reflect changes in laws, such as the transition to the 2025 Decree-Law.

Record keeping is equally critical for UAE financial institutions and DNFBPs. All identification data, transaction records, risk assessments, and internal investigation notes must be retained for a minimum of at least five years, or six years in the Dubai International Financial Centre. These records must be readily available to examiners during inspections and must be organized in a manner that facilitates efficient retrieval.

Entities are encouraged to perform regular independent audits or reviews of their AML and CFT compliance function to validate the effectiveness of their controls. These audits should assess whether the KYC process is being followed consistently, whether risk assessments are accurate and updated, and whether the MLRO has adequate resources and authority to perform their duties. The audit findings should be reported to senior management and the board of directors, with action plans developed to address any identified deficiencies.

Enforcement and the Cost of Non-Compliance in the UAE

The United Arab Emirates has adopted a robust enforcement stance, with supervisors increasingly utilizing financial sanctions and public reprimands to deter violations. The scale of penalties is designed to ensure that compliance is more cost-effective than violation, thereby incentivizing businesses operating in the UAE to maintain rigorous standards.

Under Federal Decree-Law No. 10 of 2025, corporations found guilty of money laundering can face fines up to AED 100 million. For administrative failings, the Central Bank of the UAE and Ministry of Economy have recently imposed fines ranging from AED 3 million to AED 5.9 million on financial institutions for material breaches in sanctions compliance and customer monitoring. For Designated Non-Financial Businesses and Professions, the unified list of violations under Cabinet Decision No. 16 of 2021 provides for fines from AED 50,000 to AED 1 million for offenses such as failure to appoint an MLRO, failure to register on goAML, or inadequate Customer Due Diligence procedures.

Beyond financial penalties, non-compliant entities face existential risks. Regulatory authorities have the power to suspend or revoke commercial licenses, remove senior management, and impose restrictions on the business’s operations. In 2024, the Ministry of Economy revoked the licenses of several gold and precious metal dealers for persistent breaches of legal requirements. Additionally, non-compliance can lead to the termination of banking relationships, as UAE banks and international financial institutions increasingly de-risk and refuse to serve entities with weak AML frameworks. This can effectively render a business unable to operate, as access to banking services is essential for conducting legitimate business activities.

Strategic Outlook: Future of KYC Regulations and UAE AML Compliance

The UAE’s regulatory environment will continue to evolve and tighten as the state prepares for the fifth-round mutual evaluation by the Financial Action Task Force in 2026. The 2024-2027 National AML and CFT Strategy prioritizes the fight against cybercrime, digital asset exploitation, and trade-based money laundering. UAE businesses must remain agile, moving beyond static policies to embrace technology-enabled compliance solutions such as blockchain forensics for virtual asset service providers and automated name-screening software for all reporting entities.

The integration of Proliferation Financing into the core AML law signifies a shift toward broader geopolitical security responsibilities for the private sector. This expansion reflects the UAE’s recognition that financial crime extends beyond traditional money laundering and terrorism financing to include the financing of weapons proliferation and other threats to international security. Businesses need to follow these evolving standards and adapt their compliance frameworks accordingly.

Investment in digital KYC platforms and automated monitoring systems is becoming increasingly essential. These technologies can simplify KYC verification processes, reduce human error, and provide real-time alerts for suspicious activity. Advanced analytics and artificial intelligence can help businesses verify customer identities more efficiently while maintaining robust controls that meet regulatory expectations. Such systems also facilitate the daily sanctions screening required under UAE compliance obligations, ensuring that businesses remain vigilant against emerging threats.

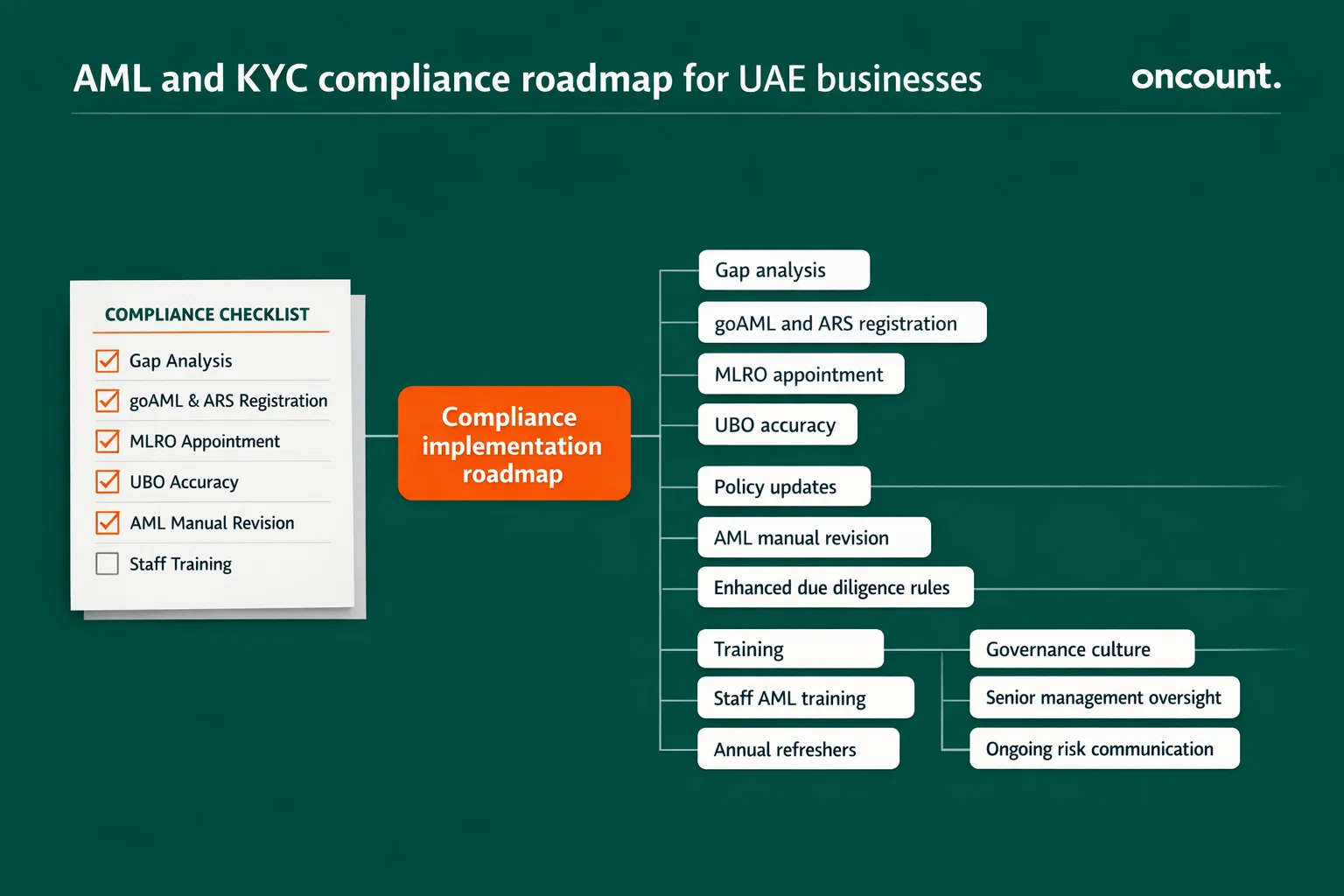

Practical Roadmap for UAE Businesses to Achieve Full Compliance

Companies should begin by conducting a comprehensive gap analysis to assess the current compliance posture against the new requirements. This assessment should focus on the following elements:

- Registration status on goAML and the Automatic Reporting System

- Appointment, qualifications, and decision-making authority of the MLRO

- Accuracy and timeliness of the Ultimate Beneficial Owner registers

- Alignment of enterprise-wide risk assessments with the updated regulatory environment

The next priority involves ensuring that all internal policies and procedures reflect Federal Decree-Law No. 10 of 2025 and Cabinet Resolution No. 134 of 2025. This stage includes revising the internal AML manual, updating customer onboarding documentation to capture mandatory data points, implementing enhanced due diligence measures for high-risk customers, and formalizing escalation and reporting protocols for suspicious transactions. Comprehensive documentation remains essential, as supervisory authorities rely on these materials to assess the effectiveness of implemented controls during inspections.

Training constitutes another critical pillar of the compliance roadmap. Employees engaged in customer interaction or financial transaction processing must fully understand obligations arising under UAE AML and CFT legislation. Training programs should address identification of red flags, customer identity verification requirements, reporting procedures for suspicious activity, and legal consequences of non-compliance. Refresher sessions should occur at least annually and following any material regulatory amendments.

Finally, organizations should foster a compliance-oriented culture that extends beyond technical adherence to statutory requirements. Senior management commitment is required to ensure integrity and transparency, supported by adequate resourcing of the compliance function and consistent backing of the MLRO. Ongoing internal communication regarding AML and CFT risks, detection outcomes, and lessons derived from compliance deficiencies supports institutional resilience and positions UAE businesses for sustained operation within an increasingly regulated international framework.