Understanding Company Liquidation in the UAE

Company liquidation refers to the formal process of closing a business entity and removing it from the commercial register. During liquidation, the company ceases operations, converts its assets into cash, pays off creditors, and distributes any remaining funds to shareholders before being struck off the register.

The legal framework for liquidation in the UAE is primarily established under Federal Decree-Law No. 32/2021 on Commercial Companies for mainland entities. Free zones operate under their own autonomous regulations, though they generally align with federal principles.

The UAE Bankruptcy Law (Federal Law No. 9 of 2016) governs insolvent scenarios, while the UAE Labour Law (Federal Decree-Law No. 33 of 2021) protects employee rights during business closure.

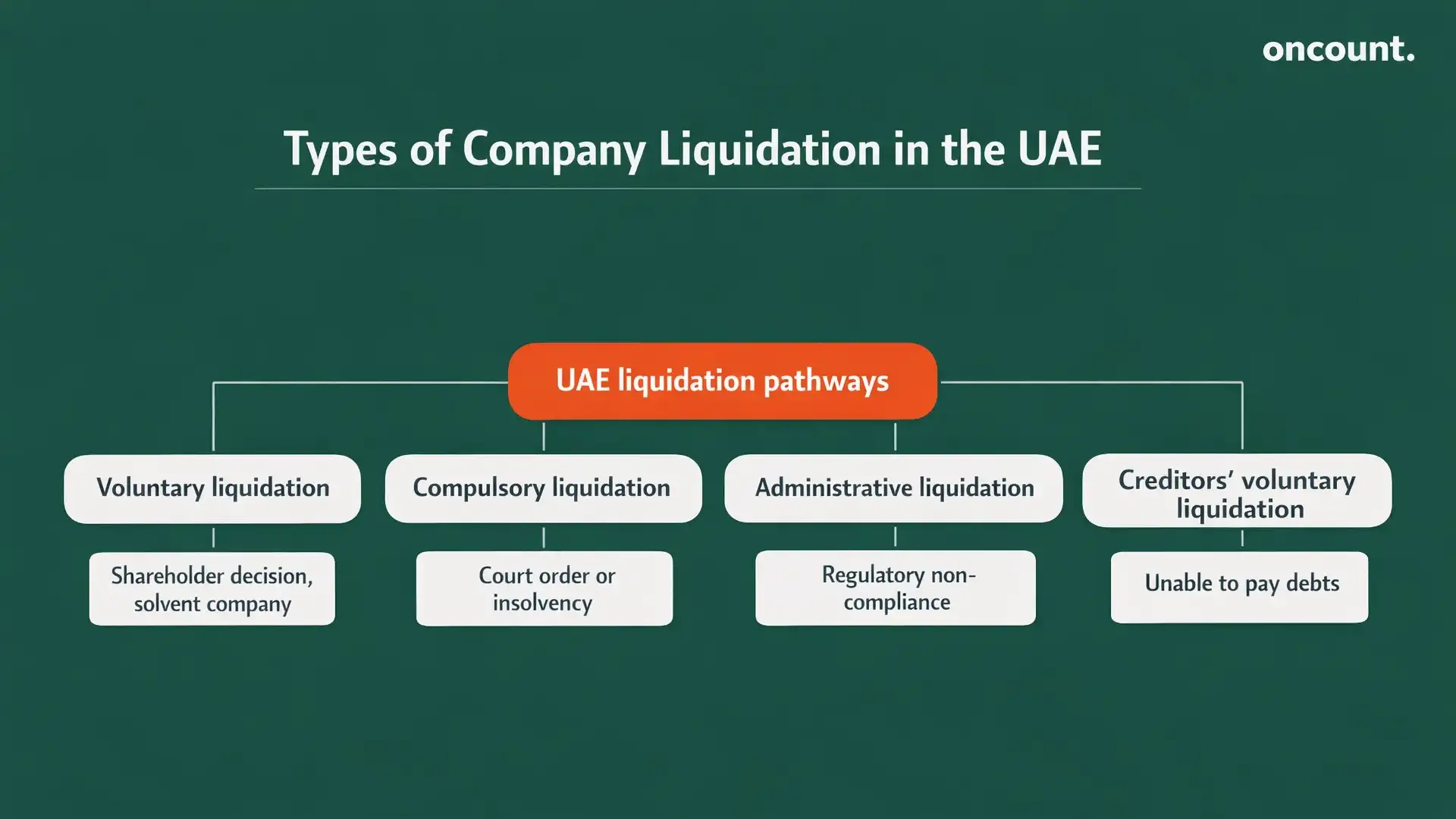

Types of Company Liquidation

The liquidation process varies depending on your company’s financial position and the circumstances driving the closure. Understanding these distinctions helps business owners choose the appropriate path and manage potential liabilities.

Liquidation Types in the UAE:

| Liquidation Type | Trigger | Primary Purpose | Supervising Authority |

| Voluntary Liquidation | Shareholder decision | Orderly closure of solvent operations | Licensing Authority (DET, FZA) |

| Compulsory Liquidation | Court order | Judicial enforcement due to insolvency or violations | UAE Courts |

| Administrative Liquidation | Regulatory action | Removal of non-compliant or inactive entities | Free Zone Authority |

| Creditors’ Voluntary Liquidation | Director declaration | Managed exit when unable to pay debts | Licensed Insolvency Practitioner |

Voluntary liquidation is the most common route for businesses that have completed their objectives or reached the end of their planned term. This process gives business owners control over the timing and manner of closure while maintaining their professional reputation.

Compulsory liquidation typically occurs when creditors petition the court following unpaid debts, or when a company commits serious violations of commercial law. Under Article 308 of the Commercial Companies Law, if a Limited Liability Company’s losses reach 50% of its share capital, managers must present the matter to shareholders.

If losses exceed 75% of capital, the company may face forced liquidation unless shareholders approve a capital injection.

Reasons for Liquidating a Company

Business owners may decide to liquidate for various strategic and operational reasons. Some companies reach the natural end of their business lifecycle or complete their intended purpose.

Others face challenging market conditions that make continued operations unsustainable. Shareholder disputes, restructuring initiatives, or a decision to relocate operations outside the UAE can also prompt the closure of the company.

Even if the company remains financially solvent, changes in business strategy or regulatory requirements may make liquidation the most prudent option. According to UAE regulations, understanding your specific circumstances helps determine the appropriate liquidation pathway and timeline.

The Role of the Licensed Liquidator

The appointment of a liquidator represents a critical requirement across all UAE jurisdictions. Once liquidation begins, the authority of the company’s board of directors effectively ends, and the liquidator assumes complete control of the entity’s affairs.

The liquidator serves as a fiduciary agent responsible for protecting the interests of both creditors and shareholders throughout the process. For Limited Liability Companies, Joint Stock Companies, and most free zone entities, the liquidator must be a registered audit firm approved by the relevant authority.

In Dubai, this means approval by the Department of Economy and Tourism. The liquidator cannot be someone who served as the company’s auditor within the previous five years, ensuring independence and impartiality.

The company and the appointment of a liquidator must be formalized through a board or shareholder resolution. This resolution requires notarization before submission to the licensing authority to issue a liquidation certificate.

Key Responsibilities of the Liquidator

The liquidator’s mandate involves several high-stakes financial and legal tasks. They conduct an exhaustive inventory and valuation of all company assets, including intellectual property and real estate.

They manage the public notification process and verify creditor claims during the statutory notice period. The liquidator also handles asset realization, converting company property into cash at fair market value to generate funds for debt settlement.

Finally, they prepare the Statement of Affairs and the final liquidation report, which must receive shareholder approval before submission to the registrar. The liquidator to manage the process must maintain detailed records and ensure compliance with all UAE authorities throughout the liquidation procedure.

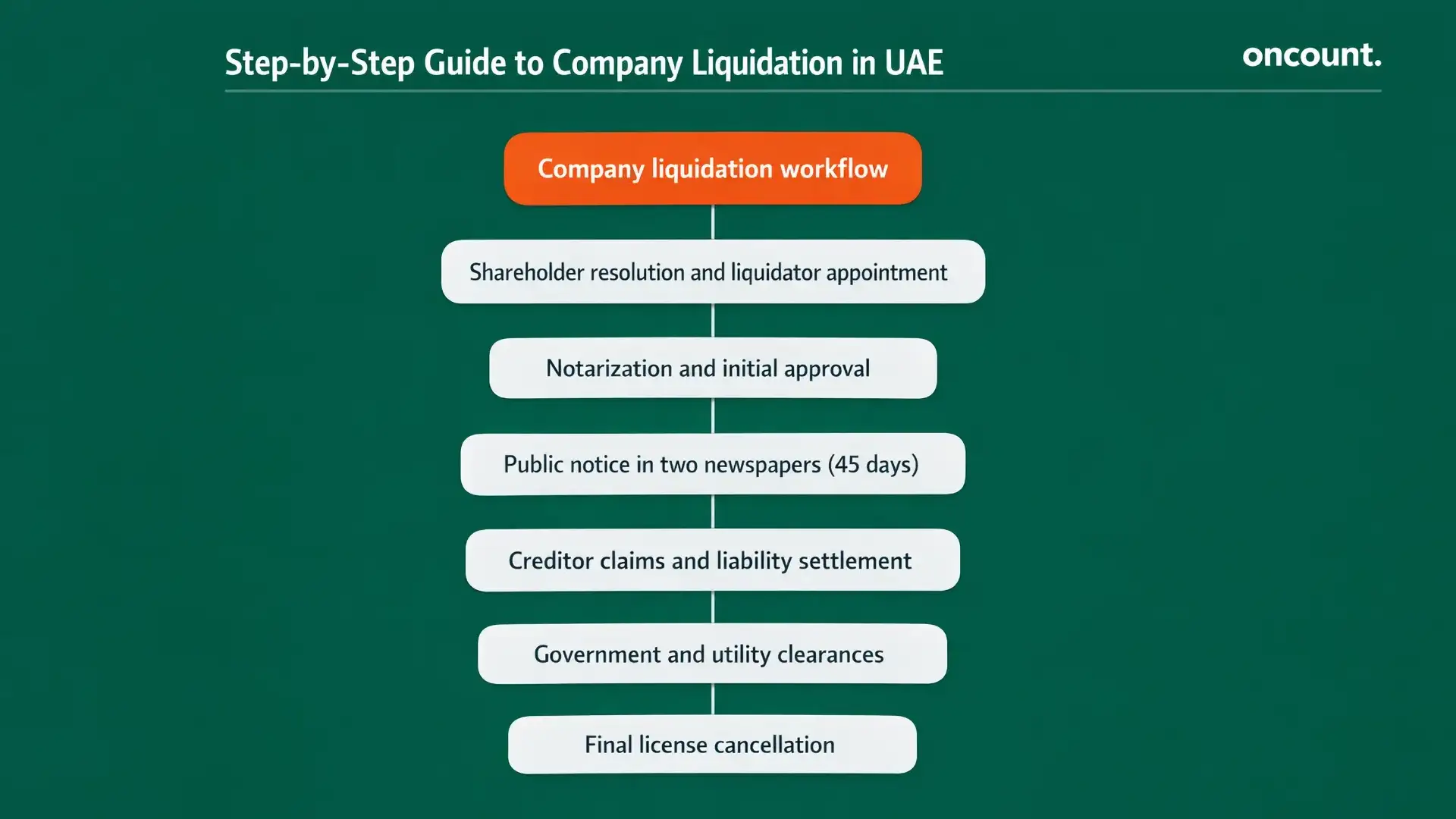

Step-by-Step Guide to Company Liquidation in UAE

The liquidation process for a mainland entity, particularly an LLC licensed by the Department of Economy and Tourism in Dubai, follows a structured two-phase approach. Understanding each phase helps business owners plan effectively and avoid common delays.

Phase 1: Initiation and Initial Approval

The process begins with a General Assembly meeting where shareholders pass a resolution approving the liquidation and appointing a liquidator. This decision to liquidate the company must be documented in a formal resolution and notarized by a UAE Public Notary.

If shareholders are located abroad, the resolution requires attestation at the UAE Embassy in their respective country. Further legalization by the UAE Ministry of Foreign Affairs and Ministry of Justice is then necessary.

Once you have the notarized resolution, you submit it to the DET along with the liquidator’s acceptance letter and the relevant fees, typically around AED 520. The DET then issues a Certificate of Dissolution, which provides the legal foundation for proceeding with the formal wind-down.

This certificate enables the company to begin the process of newspaper advertisements and visa cancellations. Business owners should obtain a copy of your business license and all company formation documents at this stage for reference throughout the liquidation process in the UAE.

Phase 2: Public Notification and Objections

After receiving the dissolution certificate, the company must publish a notice of liquidation in two local daily newspapers. One advertisement must appear in Arabic and one in English.

This publication initiates a mandatory 45-day liquidation notice period. This window protects third-party rights by allowing creditors to submit their claims to the liquidator.

During this 45-day period, the company must refrain from initiating new business activities. The focus must shift exclusively to clearing existing debts and liabilities.

The liquidator manages all incoming creditor claims, verifying their legitimacy and preparing for settlement according to the statutory priority order. This liquidation notice period is critical for ensuring all parties have adequate time to assert their rights.

Phase 3: Administrative Clearances and Final Cancellation

Following the expiration of the 45-day notice period, assuming no unresolved objections remain, the liquidator compiles and submits clearances from various government and utility departments. These clearances demonstrate that all obligations have been satisfied.

Required Clearances for Final Cancellation:

| Authority | Clearance Type | Purpose |

| MOHRE | Labor Clearance | Confirms all employee contracts terminated and dues paid |

| GDRFA | Visa Cancellation | Proves all company-sponsored residency visas cancelled |

| FTA | VAT & CT Deregistration | Verifies all tax returns filed and liabilities settled |

| DEWA/FEWA/ADDC | Utility Clearance | Confirms final bills paid and accounts closed |

| Customs | Customs Clearance | Required for trading licenses to ensure no outstanding duties |

| Commercial Banks | Bank Closure Letter | Official confirmation that corporate accounts are closed |

The final business license cancellation fee, approximately AED 1,020 in Dubai, is paid after all clearances are obtained. The DET then issues the final License Cancellation Certificate, officially striking the entity from the Commercial Register.

This completes the closure of the company and the final cancellation of all registrations. The company is officially removed from all public records, and the liquidation of the company is complete.

Free Zone Company Liquidation Procedures

UAE free zones operate under autonomous regulatory frameworks. While they align with federal principles, their specific procedural requirements for liquidation can vary significantly from mainland processes.

Each UAE free zone has developed its own administrative requirements, though the fundamental principles of asset realization and creditor protection remain consistent. Business owners operating in free zones must carefully review their specific jurisdiction’s regulations.

Dubai Multi Commodities Centre (DMCC)

Liquidation in the DMCC follows a highly structured approach with multiple modes of winding up based on the company’s solvency and required timeframe. Summary Winding-Up applies to solvent companies capable of concluding the process within six months.

Solvent Winding-Up accommodates companies requiring up to 12 months to liquidate assets and settle liabilities. Insolvent Voluntary Winding-Up involves the appointment of a liquidation committee by creditors when the company cannot meet its debts.

The DMCC manages the process through its digital portal, but original legal documents must be physically returned. These include the trade license, Memorandum of Association, and share certificates, which must be submitted to the DMCC Client Service Centre.

A unique feature of DMCC is the requirement for two separate 14-day publication periods. One period covers the termination notice, while another addresses the deregistration notice.

Jebel Ali Free Zone Authority (JAFZA)

In JAFZA, the liquidation of Free Zone Establishments and Free Zone Companies follows a specific sequence. The shareholder resolution must be signed in person at the JAFZA head office.

JAFZA mandates an Exit Interview with Customer Relations as a prerequisite for deregistration. This interview ensures all outstanding matters are addressed before proceeding with the company termination application.

Financial obligations in JAFZA include a deregistration fee ranging from approximately AED 5,000 to AED 6,500. An additional advertisement fee of AED 1,500 applies to all liquidations.

Entities with physical facilities such as warehouses or plots must provide three to six months’ notice to the leasing department. A Property Clearance must be obtained confirming the premises have been vacated and keys returned.

Financial Free Zones: DIFC and ADGM

The Dubai International Financial Centre and Abu Dhabi Global Market operate under legal systems based on English Common Law. These jurisdictions introduce distinct insolvency concepts and procedures not found in other UAE commercial jurisdictions.

In the DIFC, liquidation is governed by the DIFC Companies Law No. 5 of 2018 and the Insolvency Law No. 1 of 2019. For a solvent voluntary liquidation, directors must file a Declaration of Solvency with the Registrar of Companies.

This declaration affirms that the company can pay all debts in full within 12 months. The liquidator must be a DIFC-registered insolvency practitioner with specialized qualifications.

If the entity is regulated by the Dubai Financial Services Authority, explicit regulatory clearance is required before the company can be struck off. This additional layer of oversight ensures financial institutions are properly wound down.

ADGM provides entities with two main pathways for closure: formal liquidation or a Voluntary Strike Off. The strike-off is a simplified procedure for entities that have not traded, changed their name, or disposed of property in the preceding three months.

Strike Off with Notice requires notifying all relevant parties within seven days of filing. Strike Off with Prescribed Statement offers a streamlined option for small companies with turnover not exceeding USD 13.5 million and no more than 35 employees.

Offshore Company Liquidation

Offshore entities, designed for international holding or investment purposes, follow a liquidation process that is primarily document-driven. These companies typically do not maintain physical offices or local employees in the UAE.

The RAK International Corporate Centre requires the appointment of a licensed liquidator who manages the strike-off through the registered agent. A Declaration of No Assets and No Liabilities is a critical document in this process.

The declaration letter from the liquidator must confirm that any international bank accounts have been closed and all obligations settled. The liquidator must provide a final report demonstrating complete asset distribution and liability settlement.

The timeframe for offshore liquidation is typically the most efficient in the UAE, often concluding within 20 to 45 days. This expedited timeline reflects the simpler operational structure of offshore entities compared to mainland or free zone companies.

Tax Compliance: VAT and Corporate Tax Deregistration

The modern UAE liquidation process is inseparable from tax compliance. Following the introduction of Corporate Tax in June 2023, the Federal Tax Authority has implemented rigorous deregistration timelines.

Missing these deadlines results in significant financial penalties that can substantially increase the cost of closing a company. Business must ensure all tax obligations are addressed before final cancellation can proceed.

Value Added Tax (VAT) Deregistration

A VAT-registered entity must apply for deregistration via the EmaraTax portal within 20 business days of ceasing taxable operations. The FTA will not approve the request until a Final VAT Return is filed and all outstanding taxes are settled.

All administrative penalties must also be cleared before deregistration approval. The penalty for late VAT deregistration is a flat AED 10,000, making timely compliance essential.

Corporate Tax (CT) Deregistration

Under the Corporate Tax Law, an entity must apply for deregistration within three months of the date it ceases to exist or ceases its business activity. This is known as the three-month rule.

Even if a company has not earned income above the AED 375,000 threshold, it must still register for CT, file its final return, and then apply for deregistration. This requirement applies to all commercial entities regardless of profitability.

CT Deregistration Penalties:

| Penalty Type | Amount | Maximum Cap |

| Initial Late Fee | AED 1,000 (first month) | N/A |

| Recurring Late Fee | AED 1,000 per subsequent month | AED 10,000 |

Entities must provide the FTA with a Trade License Cancellation Certificate and a Final Audit Report to confirm the cessation of business. The FTA generally processes these applications within 30 business days, though complex cases may require additional review time.

Labor Compliance and Employee Entitlements

The protection of worker rights is a fundamental principle of UAE liquidation law. The settlement of all employee dues is a prerequisite for obtaining labor and immigration clearances from MOHRE and GDRFA.

Failure to properly settle employee entitlements can result in labor disputes, financial penalties, and potential travel bans for company directors. These consequences make labor compliance one of the most critical aspects of the liquidation process in UAE.

Gratuity Calculation

Expatriate employees with more than one year of continuous service are entitled to End of Service gratuity. Under Federal Decree-Law No. 33 of 2021, the calculation follows a specific formula.

For the first five years of service, employees receive 21 days of basic salary per year. For service exceeding five years, employees receive 30 days of basic salary for each additional year.

The total gratuity cannot exceed two years of basic salary. This calculation is based strictly on the basic wage stipulated in the contract, excluding allowances such as housing or transport.

Final Settlement Timeline

Employers are legally required to pay all end-of-service entitlements within 14 days of contract termination. These entitlements include gratuity, accrued but unused annual leave pay, and any unpaid salary.

Failure to meet this deadline can lead to labor disputes at MOHRE. Directors may also face potential travel bans until all employee claims are fully satisfied.

The process of closing a business requires careful attention to these labor obligations. Companies should prepare detailed calculations and ensure sufficient funds are available to settle all employee claims promptly.

Operational Closeout and Financial Finalization

Beyond the legal and tax filings, the operational wind-down requires the termination of all commercial contracts and utility accounts. These practical steps are essential to wind up the business completely.

Bank Account Closure Protocol

Closing corporate bank accounts is often the most time-consuming operational step. Banks require the primary liquidation certificate and a board resolution to initiate closure.

The liquidator must obtain a Bank Account Closure Letter and a final statement for the last financial year. These documents must be included in the final liquidation report submitted to the licensing authority.

It is advisable to maintain the account until the final asset realization is complete. However, the account should be closed before the final DET cancellation to ensure no legacy transactions occur.

Premature bank closure can freeze the entire process if additional fees or refunds need to be processed. Strategic timing of bank account closure is therefore essential for a smooth liquidation.

Asset Realization and Distribution Priority

The liquidator must realize company assets, including property, vehicles, and equipment. The proceeds are then distributed according to the statutory order of priority established by UAE commercial law.

Liquidation expenses come first, covering costs incurred by the liquidator and legal professionals. Employee claims for unpaid wages and end-of-service gratuity follow as the second priority.

Preferential creditors, including government dues for VAT and Corporate Tax, are paid third. Secured creditors with debts backed by mortgages or specific pledges receive payment fourth.

Unsecured creditors, such as general commercial suppliers and service providers, are paid fifth. Finally, shareholders receive distribution of any remaining surplus according to their shareholding percentages.

This hierarchy ensures that employees and government obligations are protected before shareholders receive any residual value from the liquidation of a company.

Common Challenges and How to Avoid Them

Liquidation is often complicated by potential delays and liabilities. Understanding common pitfalls helps business owners plan proactively and avoid costly mistakes.

Many companies attempt to liquidate while behind on their annual audits, which are mandatory for free zone deregistration. Catching up on audit backlogs before beginning the liquidation procedure can prevent significant delays.

Closing bank accounts before receiving final refunds or paying final government fees can freeze the process entirely. Maintaining accounts until all financial transactions are complete is essential.

Using an unlicensed liquidator or failing to notarize resolutions correctly can lead to rejection of the entire application. Ensuring proper documentation from the outset saves time and expense.

Strategies for a Smooth Liquidation

To achieve a smooth liquidation, entities should conduct a Pre-Liquidation Audit. This audit identifies all outstanding liabilities and ensures all Economic Substance Regulations and Ultimate Beneficial Owner filings are current.

Parallel execution of visa cancellations and utility clearances during the 45-day newspaper notice period can reduce the total timeline significantly. This approach maximizes efficiency rather than handling tasks sequentially.

Engaging with tax professionals early to prepare the final tax return ensures the three-month FTA deadline is met. This prevents the accumulation of monthly fines that can reach AED 10,000.

Working with experienced liquidators in Dubai who understand the nuances of local regulations can expedite the entire process. Professional company liquidation services provide valuable expertise in navigating complex administrative requirements.

Timeline and Cost Considerations

The timeline for liquidating a company in Dubai varies based on jurisdiction and complexity. Mainland liquidations typically require three to six months from the initial shareholder resolution to final cancellation.

Free zone liquidations can range from two to twelve months depending on the specific authority and whether the company has outstanding obligations. Offshore liquidations are generally the fastest, often completed within 20 to 45 days.

The cost of closing a company in the UAE includes multiple components. Government fees, liquidator fees, newspaper publication costs, and clearance expenses all contribute to the total.

Mainland liquidations in Dubai typically incur costs between AED 15,000 and AED 30,000 for straightforward cases. More complex situations involving multiple locations, significant assets, or employee disputes can increase costs substantially.

Free zone costs vary widely by jurisdiction. DMCC liquidations may cost between AED 10,000 and AED 25,000, while JAFZA fees range from AED 15,000 to AED 35,000.

Additional costs may include outstanding tax liabilities, employee settlements, and legal fees for resolving disputes. Company owners should budget conservatively and maintain adequate reserves to cover all liquidation expenses.

Navigating the Liquidation Process Successfully

The liquidation of a UAE company is a multifaceted legal and financial journey that extends far beyond the mere cessation of business activities. It represents a structured process requiring synchronization of federal tax filings, jurisdictional labor clearances, and municipal utility cancellations.

Following the 2023-2024 tax reforms, the margin for error has narrowed significantly. The Federal Tax Authority now plays a central role in the final deregistration of all commercial entities operating in the UAE.

By appointing a qualified liquidator and adhering to a methodical step-by-step framework, directors can ensure a compliant exit. This approach protects their professional reputation and preserves the possibility of future entrepreneurial endeavors in the region.

Whether closing a mainland company in Dubai, liquidating a company in a UAE free zone, or winding up an offshore entity, understanding the specific requirements of your jurisdiction is essential. Professional guidance, careful planning, and attention to regulatory timelines are the keys to achieving a smooth liquidation and successful business closure in the UAE.