Excise Tax in the UAE: Scope and Application

The excise tax is an indirect charge, meaning it is ultimately intended to be passed on to the end consumer through the final retail price. It is imposed on designated products at specific trigger points, such as the moment of their importation, production, or release into the UAE market for consumption.

The imposition focuses on a targeted list including tobacco products, carbonated beverages, energy drinks, and sweetened drinks, with the uae government aiming to influence consumer behavior, promote healthier lifestyles, and reduce environmental harm. In contrast to the broad-based VAT in UAE, which applies at multiple stages across the supply chain, excise tax obligations arise at very specific transactional points for entities that are registered for excise tax.

The rate of excise tax structure clearly reflects the government’s public health priorities. To ensure clarity for businesses, the FTA has established a straightforward framework of rates. The following table provides a comprehensive overview of each excise good and its corresponding charge:

| Good Category | Rate | Examples | Key Considerations |

| Tobacco and tobacco products | 100% | Cigarettes, cigars, pipe tobacco, water-pipe tobacco | Rate applies to all tobacco forms regardless of packaging |

| Energy drinks | 100% | Beverages containing stimulants (caffeine, taurine, guarana) | Marketing as “energy” product triggers classification |

| Carbonated drinks | 50% | Soft drinks, carbonated water with flavoring | Sugar-free variants may be exempt under specific conditions |

| Sweetened drinks | 50% | Juices with added sugar, flavored milk, sports drinks | The distinction between natural vs. added sugars is critical |

| Electronic smoking devices | 100% | E-cigarettes, vaping devices, heated tobacco devices | Applies per individual device unit |

| Liquids used in electronic smoking devices | 100% per ml | E-liquids, vaping solutions | Calculated based on the volume of the liquid |

This structure demonstrates a firm commitment to public health objectives while generating revenue. Businesses handling these items must accurately classify their products to apply the correct tax rate during the tax calculation and payment processes, as errors can lead to significant financial discrepancies.

Key Activities Triggering Registration Requirements:

- Importing any excise good into the UAE from international markets.

- Manufacturing or producing excise goods within the UAE’s territory.

- Stockpiling such goods for commercial purposes beyond specified limits.

- Operating designated zones or warehouses where these items are stored.

- Releasing regulated goods from designated zones into free circulation for consumption.

Mandatory Registration for Excise Tax: Who Must Register

An obligation to register for excise with the FTA portal arises for any business whose activities involve handling regulated goods at any stage defined by the official excise tax regulations. The registration threshold for excise tax is fundamentally different from VAT criteria; it is activity-based rather than revenue-based. This means any entity engaged in production, importation, or stockpiling activities must register for excise tax, irrespective of its transaction volume or annual revenue.

FTA guidance stipulates that excise tax registration applications must be submitted before commencing any relevant activities. The portal facilitates the online submission of all necessary documents, including trade licenses, Emirates ID copies, and customs details. Businesses involved with these goods must obtain their Tax Registration Number (TRN), a unique identifier for all interactions with the authority. The EmaraTax platform functions as the unified interface for all federal tax obligations, including corporate tax and VAT in UAE.

Foreign entities without a permanent establishment but importing regulated goods must appoint a local agent or register directly. Entities in free zones that release goods into the UAE mainland for consumption trigger excise tax liabilities and corresponding filing requirements, as the liability is tied to the entry into the local economy, not the place of storage.

Excise Tax Return Filing Requirements and Deadlines

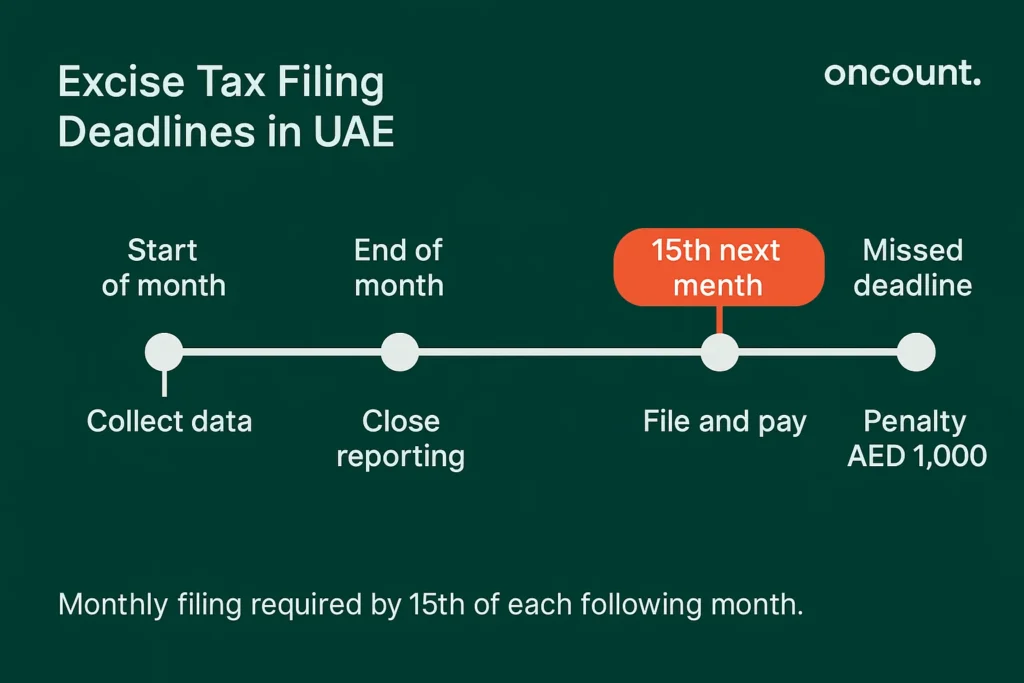

Excise tax returns must be filed on a monthly basis through the EmaraTax portal, representing one of the more frequent and demanding compliance obligations in the uae tax system. The filing deadline is strictly set for the 15th day of the month that follows each tax period. For instance, a business must file an excise tax return covering its activities in October by no later than November 15th.

This monthly tax cadence necessitates rigorous and disciplined financial management. Unlike the more lenient quarterly VAT filing schedule for some businesses, the monthly tax period for this declaration creates continuous compliance pressure. Returns by the 15th must contain comprehensive and accurate data on all regulated goods handled during the preceding month, regardless of whether a payable liability was generated. The deadline is at the end of each tax period.

Monthly Filing Calendar Overview:

| Period | Activities Covered | Filing Deadline | Payment Deadline | Penalty for Late Submission |

| January | 1 Jan – 31 Jan | 15 February | 15 February | AED 1,000 (first offense) |

| February | 1 Feb – 28/29 Feb | 15 March | 15 March | AED 1,000 (first offense) |

| March | 1 Mar – 31 Mar | 15 April | 15 April | AED 1,000 (first offense) |

| April | 1 Apr – 30 Apr | 15 May | 15 May | AED 1,000 (first offense) |

| May | 1 May – 31 May | 15 June | 15 June | AED 1,000 (first offense) |

| June | 1 Jun – 30 Jun | 15 July | 15 July | AED 1,000 (first offense) |

| July | 1 Jul – 31 Jul | 15 August | 15 August | AED 1,000 (first offense) |

| August | 1 Aug – 31 Aug | 15 September | 15 September | AED 1,000 (first offense) |

| September | 1 Sep – 30 Sep | 15 October | 15 October | AED 1,000 (first offense) |

| October | 1 Oct – 31 Oct | 15 November | 15 November | AED 1,000 (first offense) |

| November | 1 Nov – 30 Nov | 15 December | 15 December | AED 1,000 (first offense) |

| December | 1 Dec – 31 Dec | 15 January (next year) | 15 January (next year) | AED 1,000 (first offense) |

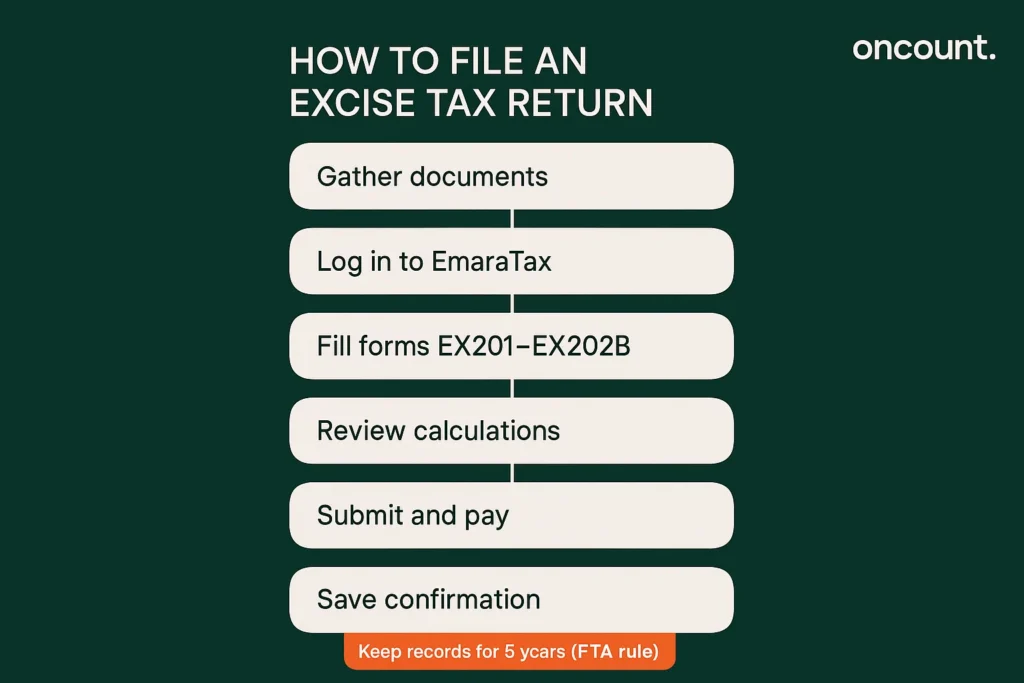

The submission process involves completing specific forms based on the nature of the business activities:

- Form EX201 is for import declarations. Importers must reconcile the excise tax paid at customs with their monthly submissions.

- Form EX202A covers releases from designated zones. Operators must report quantities and values of goods leaving these controlled areas.

- Form EX202B applies to producers calculating the tax due on their goods. Manufacturers must provide a full accounting of production volumes and inventory.

The requirements for stockpilers involve direct data entry into the portal, declaring the amount due on goods held for commercial purposes. The FTA defines stockpiling as holding regulated goods in excess of specified quantities, an activity that triggers immediate registration and ongoing filing obligations.

Calculating the Excise Tax Due: Methodology and Precision

Accurately calculating the excise tax liability is a critical step that requires a clear understanding of how the tax amount is determined. The tax is calculated by applying the prescribed excise tax rate to the “dutiable price,” which is the base value upon which the charge is calculated. This price can vary depending on whether goods are imported, produced, or released from designated zones.

For imported goods, the dutiable price is the customs value plus any applicable customs duties. The amount of excise tax is computed before the application of VAT. When businesses must pay the tax due on their goods, this tax calculation must meticulously reflect the correct classification and the current rate.

Producers determine the dutiable price based on the standard retail price at which the goods are sold to consumers, minus the applicable VAT. This methodology ensures fairness and consistency in how the liability is calculated. The FTA provides detailed guidance on calculating the excise tax due for various scenarios, including deemed supply situations where goods are consumed internally by the business.

Common Calculation Errors to Avoid:

- Misclassifying goods between categories that have different rates, a frequent source of error.

- Utilizing incorrect methods for determining the dutiable price for locally produced goods.

- Failing to make necessary adjustments for returns, damages, or officially destroyed goods.

- Omitting customs duties from the calculation base for imported items.

- Inadvertently double-counting liabilities on re-imported items that were previously charged.

Managing excise tax filings requires robust and reliable systems for tracking inventory, production data, and import documentation. Businesses must submit the excise tax return with complete accuracy, as the portal calculates liabilities automatically based on the entered data. Any discrepancy creates significant audit exposure.

Step-by-Step Process to File Your Excise Tax Return

Successfully managing your filings requires a methodical and well-documented execution across multiple stages. The following comprehensive process guides businesses through each critical step of the filing of excise tax returns on the EmaraTax portal.

Step 1: Assemble All Necessary Data and Documents

This foundational step is crucial for an efficient and accurate filing. Before accessing the portal, compile all necessary documentation, including your TRN, trade license, customs credentials, and comprehensive transaction records for the reporting period, such as purchase invoices, sales documentation, import declarations, production records, and inventory reports. This preparation is critical for determining the correct excise tax due.

Step 2: Access the EmaraTax Portal

Navigate to the FTA’s official portal at tax.gov.ae and authenticate using your registered credentials. The system’s integration with UAE Pass provides enhanced security for accessing sensitive data.

Step 3: Initiate a New Return Submission

Select the “Create New Return” option for the relevant reporting period. The system will automatically identify which month requires filing. It is essential to confirm the correct period before entering any data to avoid misallocations.

Step 4: Complete Form EX201 (Import Declarations)

For businesses importing regulated goods, this form is the primary tool for reconciling imported items. Enter customs-related information, including the declaration reference number, date of clearance, quantity imported, customs value, and the liability calculated at entry. The portal cross-references this information with customs databases.

Step 5: Complete Form EX202A (Designated Zone Releases)

Warehouse keepers and operators releasing goods into the mainland must complete this form. Required information includes the release authorization number, date, destination, quantity, and the calculated payable amount for that specific release.

Step 6: Complete Form EX202B (Producer Declarations)

Manufacturing entities use this form to declare their production-related liabilities. It captures facility details, production quantities, the retail price methodology used for the calculation, and the amount due based on any deemed supply rules.

Step 7: Enter Stockpile Data (Direct Entry)

Businesses that are stockpiling goods must directly enter their monthly declarations. This includes detailing the opening stock, any acquisitions, disposals, and the final closing stock at the end of the tax period.

Step 8: Review the Automated Calculations

This is a critical checkpoint. The EmaraTax portal automatically computes the total amount of excise tax due. You must review the summary carefully, verifying all rates, quantities, and classifications before you finalize the submission.

Step 9: Submit the Excise Tax Return

After confirming the accuracy of all information, formally submit the excise declaration through the portal. The system will generate a unique confirmation receipt, which should be saved for your records.

Step 10: Process the Payment of the Amount Due

Immediately proceed to pay your excise tax liabilities through the portal’s integrated payment module. It is advisable not to wait until the last day, as payment processing times can vary.

Step 11: Obtain Payment Confirmation

The system generates a payment receipt upon successful settlement. Maintain this confirmation with your submission documentation as definitive proof that businesses must pay the tax due within the prescribed timeframes.

Step 12: Archive Documentation for Audit Readiness

Complete the filing cycle by archiving all supporting documentation for the legally required five-year retention period. You must maintain excise tax records in an organized manner to ensure rapid retrieval during potential FTA audits.

Common Pitfalls in Monthly Filings

Even with a clear understanding, businesses can encounter common challenges. Based on FTA enforcement patterns, several recurring errors can jeopardize compliance:

- Deadline Mismanagement: Missing the 15th-day submission deadline, even by hours, triggers automatic penalties. These deadlines are strictly enforced.

- Incomplete Activity Declaration: Businesses must file excise tax returns for every single period, even if no regulated goods were handled. Nil returns are mandatory for all registered entities.

- Classification Confusion: Misclassification directly affects the rate applied and the final amount calculated, leading to incorrect payments.

- Stockpile Threshold Miscalculation: Businesses can inadvertently exceed quantity limits without recognizing their obligation to register and file.

- Free Zone Misconceptions: When regulated goods move from free zones into the UAE mainland for consumption, full tax liabilities arise.

Integration with Other UAE Fiscal Obligations

Effective compliance requires a holistic view of a company’s entire fiscal footprint. This levy operates within a broader framework that includes VAT and corporate liabilities.

- VAT Considerations: This charge forms part of the value base for the VAT calculation. The consumer pays the levy plus VAT on that amount.

- Corporate Implications: The amount paid or collected affects corporate calculations, impacting the taxable profit that is subject to the 9% rate.

- Customs Integration: Import activities trigger simultaneous customs duties and other obligations. Businesses must reconcile customs declarations with their monthly filings.

Leveraging Professional Tax Services in the UAE

The technical complexity of calculating the excise liability and managing monthly submissions makes professional tax services in the uae a valuable resource. Tax professionals who are familiar with FTA requirements can ensure full compliance with tax regulations. They can assist with registration, ongoing return preparation, and representation during audits.

Penalties and Enforcement: Understanding FTA Actions

The FTA enforces these regulations rigorously, with a clear and escalating penalty structure. Violations can lead to significant consequences:

- Late Filing Penalties: A minimum AED 1,000 penalty for first offenses, with repeated violations facing escalating fines.

- Late Payment Penalties: Daily penalties accrue on any unpaid liabilities, making even short delays costly.

- Inaccurate Declaration Penalties: Misstatements can trigger penalties calculated as percentages of the unpaid amount. Deliberate evasion may lead to severe penalties and prosecution under tax law.

- Failure to Register: This is a serious violation that may result in back-payments for unreported periods and maximum penalties.

The framework is designed to encourage voluntary compliance. Businesses that proactively correct errors typically receive more favorable treatment.

Refunds and Adjustments

Certain circumstances may warrant a claim for an excise tax refund. Businesses may seek refunds in situations where:

- Regulated goods are exported outside the uae.

- Goods are officially destroyed under FTA supervision.

- Overpayments have occurred due to calculation errors.

- Goods are reclassified as non-dutiable following official FTA guidance.

The refund application process requires comprehensive documentation to prove eligibility. Businesses cannot unilaterally offset claims against future liabilities; the FTA must formally approve them first.

Conclusion: Sustaining Long-Term Compliance

Filing an excise return accurately and punctually is an ongoing obligation that requires systematic processes, technical knowledge, and operational discipline. The monthly tax filing cycle creates continuous pressure that must be managed effectively. The FTA is increasing its enforcement capabilities, so businesses that establish strong compliance foundations are well-positioned for the broader UAE fiscal environment. Compliance with tax regulations in the uae is a fundamental aspect of good corporate citizenship and operational integrity.