Understanding Tax Registration Cancellation in the UAE

According to Article 21 of Federal Decree-Law No. 8 of 2017 on Value Added Tax, businesses must apply for registration cancellation when specific conditions are met. This process is conducted exclusively through the EmaraTax portal and serves two critical functions: releasing businesses from tax compliance obligations when they no longer qualify, and enabling the FTA to maintain accurate records of active registrants.

Failure to cancel registration when required constitutes a breach of tax law, exposing businesses to administrative penalties of up to AED 10,000 and potential audit scrutiny.

When You Must Deregister from VAT

The Federal Tax Authority distinguishes between mandatory and voluntary cancellation scenarios based on your business circumstances.

Mandatory Deregistration Situations

You are required to apply for registration removal within 20 business days when:

- Business permanently closes – Your company undergoes liquidation, dissolution, or official closure regardless of final turnover figures.

- Turnover falls below AED 375,000 – Your taxable supplies for the preceding 12 consecutive months drop below the mandatory threshold, with no expectation of exceeding it in the next 30 days.

- Below AED 187,500 (voluntary registrants) – If you registered voluntarily and your taxable supplies fall below this amount over 12 months with no anticipated increase within 30 days.

- Shift to exempt supplies only – Your business transitions entirely to tax-exempt activities such as residential property leasing or specific financial services.

Voluntary Deregistration Eligibility

You may request voluntary cancellation if your taxable supplies remain below AED 375,000 for the preceding 12 months. However, businesses that initially registered voluntarily face a 12-month lock-in period and cannot deregister during this first year, regardless of turnover levels.

In practice, free zone entities often choose voluntary removal when mainland operations wind down while maintaining their corporate structure for administrative purposes.

| Deregistration Type | Turnover Threshold | Timeline | Lock-in Period |

| Mandatory (Standard) | Below AED 375,000 for 12 months | 20 business days | N/A |

| Mandatory (Voluntary) | Below AED 187,500 for 12 months | 20 business days | N/A |

| Voluntary | Below AED 375,000 for 12 months | 20 business days | 12 months from voluntary registration |

| Business Closure | N/A | 20 business days | N/A |

Critical Timeline and Penalty Framework

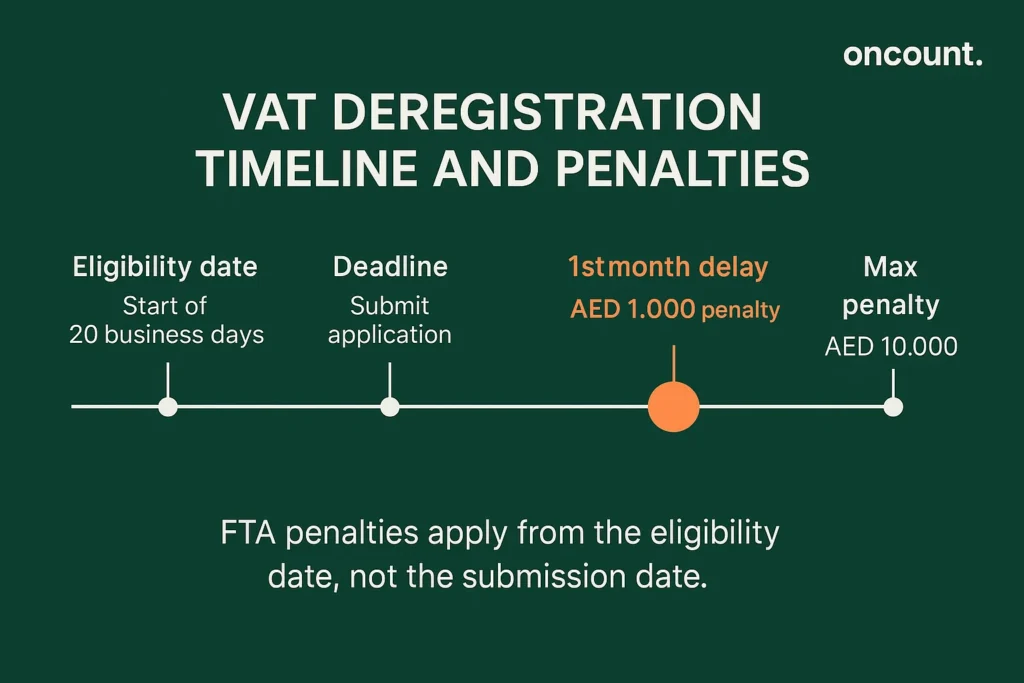

UAE tax law establishes strict deadlines for cancellation applications. You must submit your application within 20 business days from the date you become eligible for removal.

Penalty structure for late submission:

- First month of delay: AED 1,000

- Each subsequent month: AED 1,000

- Maximum cumulative penalty: AED 10,000

Based on FTA enforcement reports, approximately 18% of businesses face penalties during the cancellation process due to missed deadlines or incomplete documentation. The most common cause is incorrectly calculating the eligibility date, particularly when turnover fluctuates near threshold levels.

The 20-business-day deadline begins when you become eligible for removal, not when you decide to apply. For turnover-related cases, this means the day your trailing 12-month calculation first falls below the applicable threshold.

Step-by-Step VAT Deregistration Process

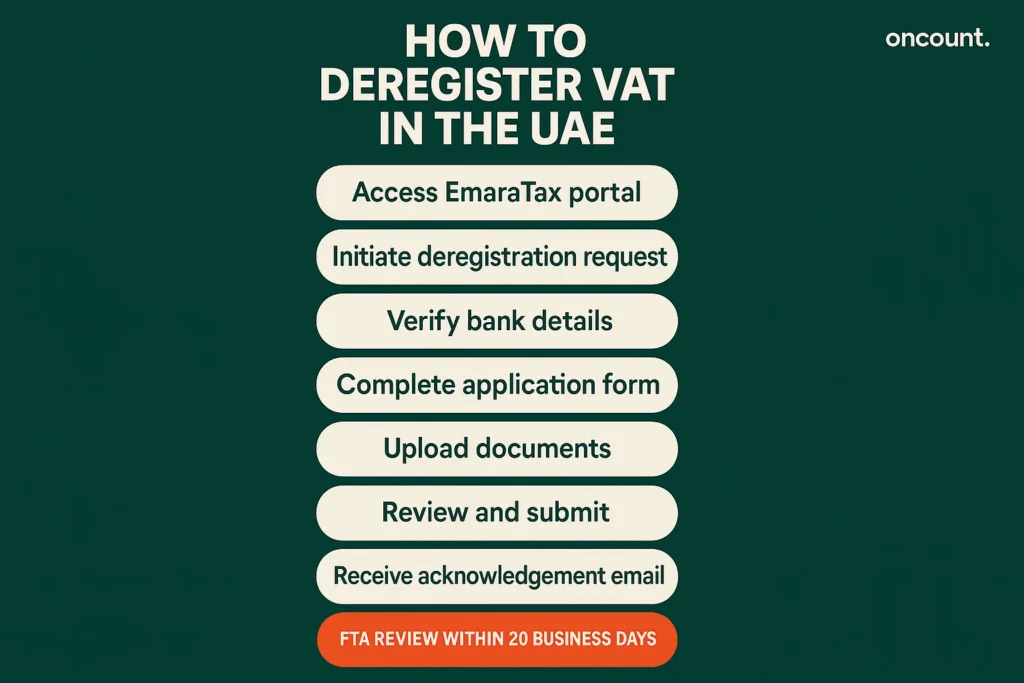

1. Access the EmaraTax Portal

Log in using your credentials or UAE PASS authentication. If two-factor authentication is enabled, enter the OTP sent to your registered email and mobile number. For businesses with multiple TRNs, select the correct taxable person profile before proceeding.

2. Initiate Your Deregistration Request

Navigate to the Value Added Tax tile on your dashboard, click “Action,” and select “Deregister.” Review the preliminary checklist outlining documents required for registration cancellation and common rejection reasons.

3. Verify Banking Information

Check your registered bank account details before completing the application. If your business holds a tax credit balance, this information determines where the FTA remits your refund after processing the final return. Click “Edit/Review” if changes are necessary.

4. Complete the Application Form

Provide comprehensive information, including:

- Reason for cancellation – Select from business closure, turnover below threshold, or shift to exempt supplies

- Business identification – Trade Licence number, TRN, and legal entity details exactly as they appear on official records

- Financial information – Detailed turnover records for 12 months, broken down by taxable, zero-rated, and exempt supplies

- Effective date – Enter the date you became eligible; EmaraTax calculates the effective date automatically

5. Upload Required Documentation

Submit all supporting documents in accepted formats (PDF, JPG, PNG). Ensure files are clear, complete, and under 5MB per file. Incomplete documentation is the primary reason for application rejection.

6. Review and Submit

Conduct a final review of all entered information, paying attention to financial figures, dates, and document completeness. Once satisfied, click “Submit” to transmit your application. You will receive an automatic acknowledgment email with a unique reference number.

Documents Required for VAT Deregistration

The FTA requires substantial documentation to verify eligibility and tax compliance. Requirements vary by cancellation reason, but the following represent standard necessities.

Always Required:

- Trade Licence copy or business closure certificate

- Value Added Tax registration certificate showing your TRN

- Emirates ID and passport copies of owner/authorized manager

- Latest financial statements (balance sheet, P&L, trial balance)

- All issued and received tax invoices during registration period

- Copies of all filed returns, including nil returns

Turnover-Related Deregistration:

- Audited or certified turnover reports proving revenue fell below AED 375,000 or AED 187,500 over 12 months

- Management accounts supporting the decline in taxable supplies

Business Closure:

- Cancelled trade licence from DED or free zone authority

- Liquidation letter or board resolution approving dissolution

- Ministry of Labour letter confirming employee status

- Signed declaration acknowledging cessation of activities within the UAE

Activity Change:

- Old and amended sales contracts

- Revised trade licence showing modified business activities

- Updated company establishment contract

| Document Category | Specific Items | When Required |

| Entity Documentation | Trade Licence, Tax Certificate, TRN, Emirates ID | Always mandatory |

| Financial Records | Balance Sheet, P&L, Invoices, Filed Returns | Always mandatory |

| Turnover Evidence | Audited Reports, Management Accounts | Threshold-based removal |

| Closure Proof | Cancelled Licence, Liquidation Letter | Business cessation only |

| Activity Modification | Amended Contracts, Revised Licence | Supply change only |

What Happens After Submission

FTA Review Process

The Federal Tax Authority reviews applications within approximately 20 business days from receipt. During this period, officials verify documentation completeness, compare financial information against filed returns, and assess eligibility.

If additional information is required, you receive email notification. Common requests include detailed turnover breakdowns, explanations for discrepancies between declared turnover and returns, or additional business cessation evidence. The processing timeline resets from the date you provide requested materials.

Application Status Updates

Monitor your application through the EmaraTax portal:

- Pre-Approved – FTA accepts your application; final approval pending settlement of liabilities and submission of final return

- Pending Information – Additional documentation required

- Under Review – Active examination by FTA officials, potentially including audit procedures

- Approved – All requirements satisfied; cancellation effective

- Rejected – Application declined with detailed reasons; may reapply once deficiencies addressed

Tax Audit Possibility

The FTA may initiate a tax audit upon receiving your request, particularly when your business has been registered beyond three years, turnover fluctuated significantly, or you are claiming substantial refunds. During audits, you must provide detailed records including general ledgers, purchase registers, and import documentation. Full cooperation minimizes delays.

Final VAT Return Requirements

Once pre-approved, file your final return covering the period from your last regular return through the cancellation date. This return requires:

- Comprehensive reconciliation of all transactions throughout registration period

- Adjustment of input tax on assets remaining at cancellation

- Verification of zero-rated and exempt supply classifications

You must settle all outstanding liabilities—including tax due from the final return and any administrative penalties—before final approval. If you hold a credit balance, the FTA processes your refund within 20 business days of approval, remitting funds to your registered bank account.

Deregistration Certificate

Upon satisfying all requirements, the FTA issues an official certificate confirming your effective cancellation date. Download this certificate from EmaraTax and retain it permanently as proof you legally cancelled your registration.

Special Considerations in the Deregistration Process

Tourist Refund System (TRS) Requirements

If registered for TRS, you must cancel this scheme before tax deregistration can be finalized. Submit a separate TRS removal application first. This dual requirement typically extends the overall timeline by 30 to 45 days.

VAT Group Registration

Members of group registrations cannot deregister individually without dissolving the entire group, unless a member genuinely ceases to qualify for group membership through business closure or sale. Consider whether group dissolution serves all members’ interests, as remaining entities may need individual registration.

Voluntary Registration Lock-In

Businesses that registered voluntarily cannot apply for removal within 12 months from registration date. This lock-in period applies regardless of turnover decline, ensuring voluntary registrants maintain compliance for a minimum period before cancelling.

Post-Deregistration Obligations

Even after your cancellation is approved, you retain continuing responsibilities under UAE tax law:

- Stop Charging VAT Immediately – Your business can no longer charge Value Added Tax on supplies. Invoices issued after the effective date must not include tax amounts.

- Maintain Records for 5 Years – Retain all accounting records, issued and received invoices, filed returns, and correspondence with the FTA for a minimum of 5 years as required by UAE tax law.

- Respond to FTA Inquiries – The Federal Tax Authority may conduct post-cancellation audits covering your registration period. You must cooperate and provide requested documentation even after removal.

- Monitor Future Registration Triggers – If your taxable supplies subsequently exceed AED 375,000 over any 12-month period, you must register for Value Added Tax again within 30 days of exceeding the threshold.

Key Takeaways for Successful VAT Deregistration in UAE

Completing the removal process successfully requires attention to regulatory timelines, comprehensive documentation, and ongoing compliance awareness. By submitting your application within 20 business days of eligibility, providing complete supporting documents, settling all liabilities promptly, and maintaining records post-cancellation, you ensure compliance with Federal Tax Authority requirements while avoiding penalties.

For complex situations involving group registrations, TRS participation, or significant credit positions, consider engaging qualified UAE tax advisors who can navigate FTA procedures and ensure your request meets all regulatory standards.