Key Takeaways

- IFRS Classification: Cryptocurrencies held for investment follow IAS 38 (intangible assets) using cost model measurement, while broker-traders apply IAS 2 (inventories) with fair value option

- VAT Exemption: Transfer and conversion of virtual assets qualify as exempt financial services under amended Executive Regulation Article 42(3)(e), effective retroactively from January 1, 2018

- Taxable Custody Services: Wallet management and custody services provided for explicit fees remain subject to 5% VAT when supplied in the UAE

- Corporate Tax Starting Point: UAE Corporate Tax calculation begins with accounting net profit per IFRS financial statements

- OCI Tax Risk: Gains recorded in Other Comprehensive Income (OCI) that will not be reclassified to profit or loss must be included in taxable income unless the realisation basis election applies

- Record Retention: UAE Commercial Companies Law mandates a minimum five-year retention period for accounting records and supporting documentation

- Impairment Testing: Indefinite-lived cryptocurrency intangible assets require frequent IAS 36 impairment assessments due to high price volatility

Overview of Accounting Requirements in the UAE

The UAE Commercial Companies Law establishes mandatory accounting record requirements for all commercial entities. Cryptocurrency companies must maintain proper books of account that accurately reflect financial position, performance, and cash flows in accordance with IFRS. The UAE Federal Tax Authority enforces a minimum five-year retention period for financial records under Federal Decree-Law No. 7 of 2017 on Tax Procedures.

UAE cryptocurrency businesses prepare financial statements following International Financial Reporting Standards (IFRS) as adopted for use in the UAE. The IFRS Foundation serves as the authoritative standard-setter. The absence of a dedicated cryptocurrency standard means digital asset accounting relies on principles-based application of existing standards, primarily IAS 38 Intangible Assets and IAS 2 Inventories.

The Federal Tax Authority requires cryptocurrency companies to maintain accounting systems capable of generating VAT-compliant records that distinguish between exempt virtual asset transfers, taxable custody services, and outside-scope activities such as proof-of-work mining. According to UAE Ministry of Finance guidance, businesses must maintain audited financial statements for accurate corporate tax determination when taxable income exceeds specified thresholds.

IFRS Application for Cryptocurrency Companies

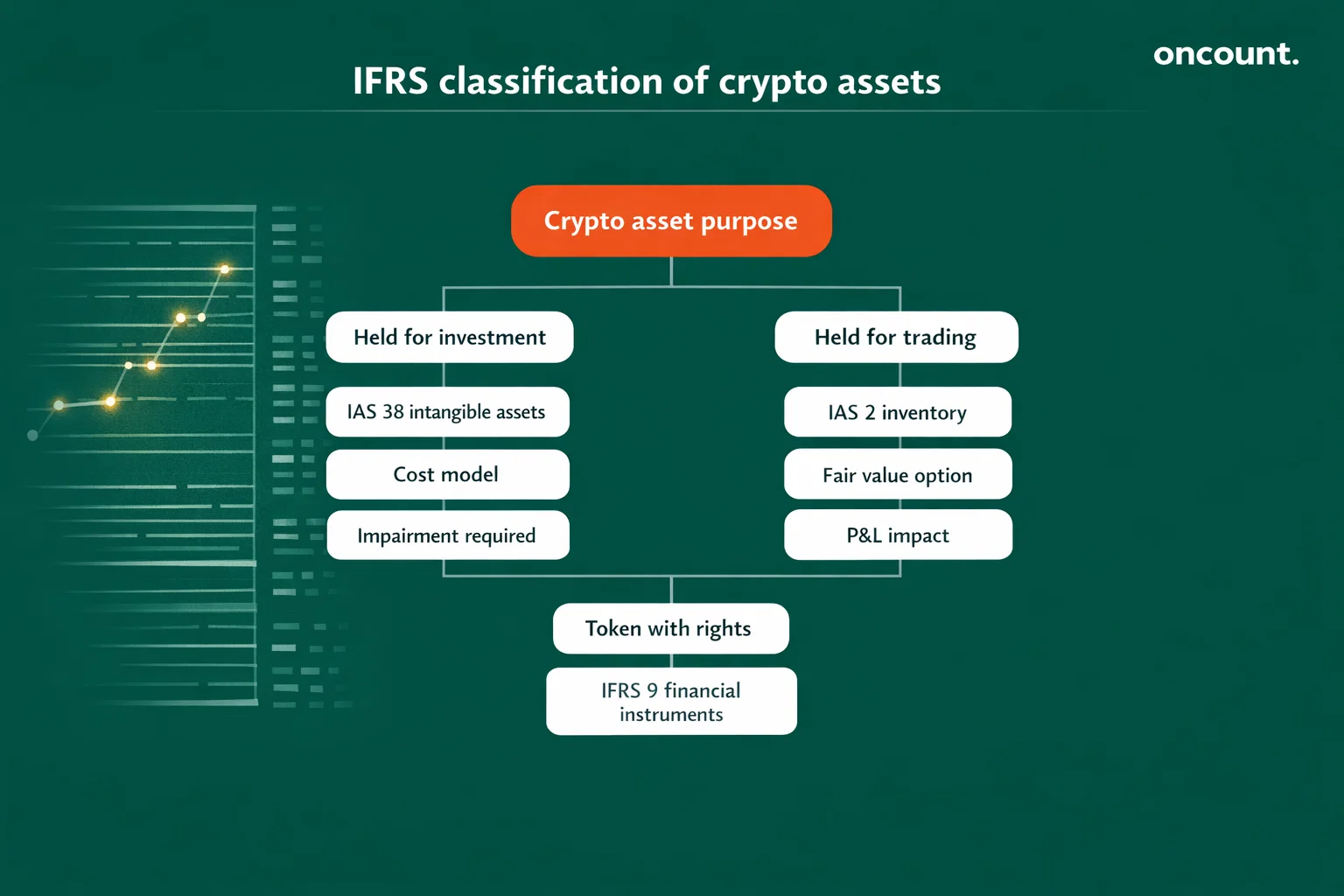

The IFRS Interpretations Committee issued an agenda decision in June 2019 addressing “Holdings of Cryptocurrencies,” which remains the primary authoritative guidance. The Committee concluded that IAS 38 Intangible Assets applies when cryptocurrencies are held other than for sale in the ordinary course of business, while IAS 2 Inventories applies to broker-trader activities.

Core IFRS Standards for Cryptocurrency Accounting

| IFRS Standard | Application Scope | Measurement Approach | Cryptocurrency Use Case |

| IAS 38 Intangible Assets | Cryptocurrencies held for investment or treasury | Cost model (cost less impairment) or revaluation model if an active market exists | Bitcoin, Ethereum holdings for capital appreciation |

| IAS 2 Inventories | Cryptocurrencies held for sale in the ordinary course | Lower of cost and NRV; broker-trader option allows FV to sell at lower costs | Exchange inventory, market-making positions |

| IFRS 9 Financial Instruments | Tokenized securities, stablecoins with contractual redemption rights | Classification-driven: amortized cost, FVOCI, or FVPL | Security tokens, stablecoins with enforceable claims |

| IFRS 15 Revenue | Exchange fees, custody services, staking-as-a-service | Five-step model: identify contract, obligations, price, allocate, recognize | Trading commissions, wallet fees |

| IAS 36 Impairment | Cryptocurrency intangible assets are measured at cost | Testing when indicators exist; indefinite-lived assets require annual testing | Write down when the market value falls below the carrying amount |

The IFRS Interpretations Committee noted that cryptocurrencies meeting its defined characteristics possess no contractual claim on an issuer and involve no contract between the holder and another party. This distinction becomes critical when analyzing stablecoins, utility tokens, and security tokens.

The IAS 38 application for cryptocurrency holdings requires determining useful life classification. Major cryptocurrencies such as Bitcoin and Ethereum typically qualify as indefinite-lived intangible assets because no contractual or legal factors limit the period over which economic benefits are expected. Indefinite useful life designation eliminates systematic amortization but elevates impairment testing requirements.

Cryptocurrency broker-traders meeting IAS 2 commodity broker-trader criteria can measure inventories at fair value less costs to sell, with changes recognized in profit or loss. Implementation requires robust valuation controls, principal market identification, and IFRS 13 Fair Value Measurement disclosure compliance.

Bookkeeping Framework and Financial Records Structure

Cryptocurrency companies must implement bookkeeping systems that capture digital asset movements with precision. The general ledger structure should accommodate cryptocurrency-specific accounts while maintaining IFRS presentation compatibility and UAE Federal Tax Authority reporting formats.

Essential Chart of Accounts Components:

Asset Accounts:

- Intangible Assets – Cryptocurrencies (Cost Model): segregated by major coin type

- Accumulated Impairment – Cryptocurrencies: contra-account tracking IAS 36 write-downs

- Inventory – Cryptocurrency Trading: for broker-dealer holdings at fair value

- Financial Assets – Tokenized Securities: IFRS 9 classification categories

- Accounts Receivable – Customer Trading Fees: IFRS 15 revenue recognition

Liability Accounts:

- Contract Liability – Deferred Revenue: when utility token issuance creates a service delivery obligation

- VAT Payable – Custody Services: 5% output VAT on wallet management fees

- VAT Receivable – Input VAT: recoverable subject to exempt activity restrictions

- Corporate Tax Payable: 9% on taxable profits exceeding AED 375,000

Revenue Accounts:

- Revenue – Trading Fees: commission income from exchange execution

- Revenue – Custody and Wallet Services: stand-ready obligation service revenue

- Revenue – Staking Services: validator operation income

- Gain on Cryptocurrency Disposal: realized gains from intangible asset sales

The UAE Federal Tax Authority requires transaction-level documentation supporting each cryptocurrency movement. Supporting documentation includes blockchain transaction hashes, wallet addresses confirming control transfer, exchange order confirmations, and market price evidence establishing fair value at the transaction date.

Electronic record-keeping systems should implement automated controls that tag each transaction by accounting classification (IAS 38 vs IAS 2 vs IFRS 9) and VAT category (exempt transfer, taxable custody service, out-of-scope mining). This dual-tagging facilitates both IFRS financial statement preparation and VAT return compilation.

Financial Statements Preparation Requirements

UAE cryptocurrency companies must prepare complete financial statements comprising a balance sheet, profit or loss statement, statement of comprehensive income, statement of changes in equity, statement of cash flows, and notes. IFRS presentation requirements apply regardless of free zone or mainland jurisdiction.

Balance Sheet Presentation

Cryptocurrency holdings classified as intangible assets under IAS 38 appear within non-current assets when held for long-term investment. IAS 1 Presentation of Financial Statements requires separate line-item disclosure when the size, nature, or function of cryptocurrency holdings makes separate presentation relevant to understanding the financial position.

The notes must include reconciliation movements showing opening balance, additions, disposals, impairment losses, reversals, and closing balance for each material cryptocurrency class. IFRS 13 Fair Value Measurement disclosure requirements apply when fair value measurement plays a significant role.

Profit or Loss Statement

Revenue recognition follows IFRS 15 principles for exchange fees, custody services, and staking arrangements. Trading fee revenue is typically recognized at the point when the trade execution service completes. Custody fee revenue is recognized over time as the stand-ready obligation is satisfied.

Gains and losses on cryptocurrency disposals appear separately from operating revenue when cryptocurrency trading does not constitute the ordinary course of business. Impairment losses on cryptocurrency intangible assets flow through profit or loss when indicators demonstrate that the carrying amount exceeds the recoverable amount.

VAT Compliance for Cryptocurrency Companies in the UAE

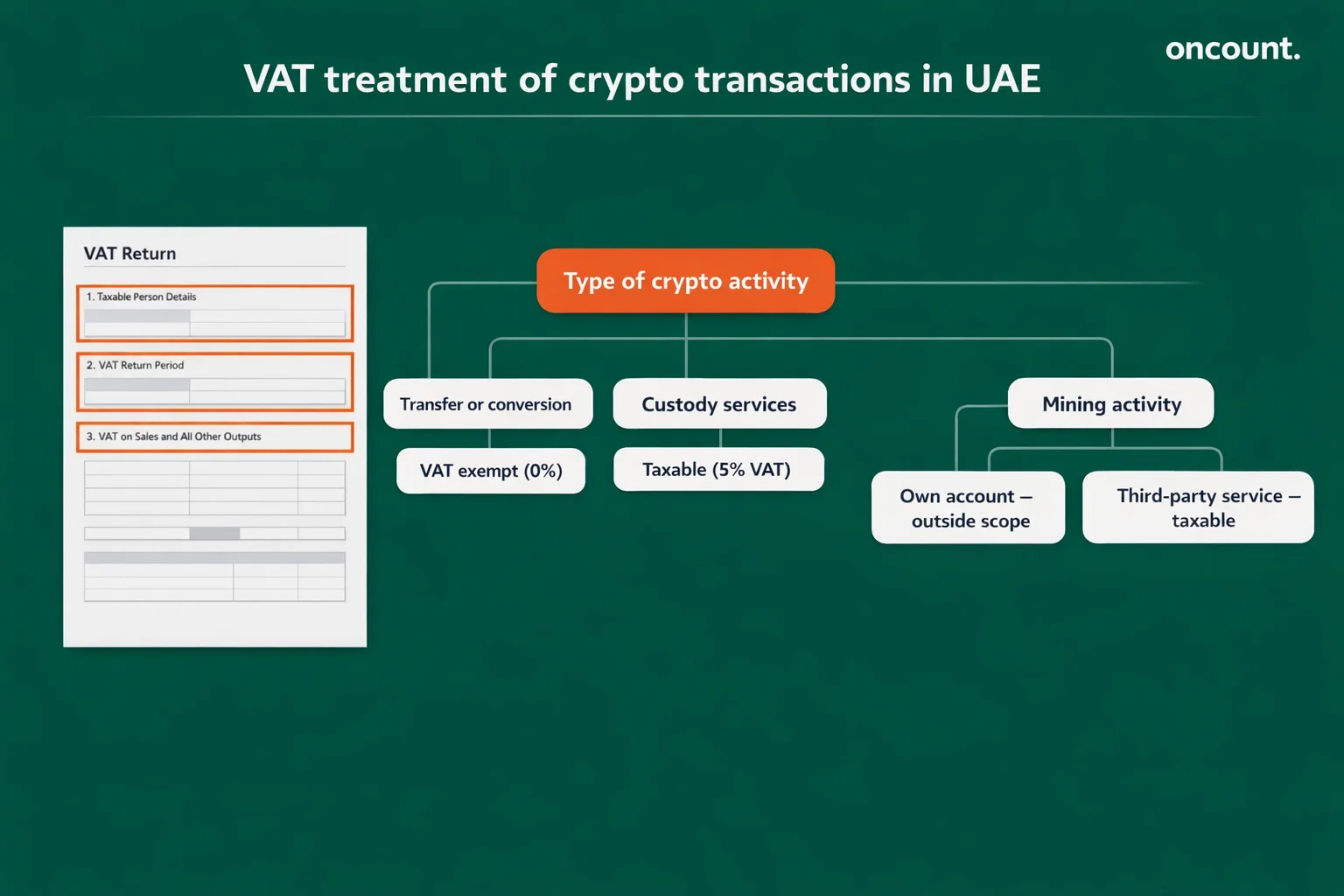

The UAE Federal Tax Authority introduced fundamental changes through Cabinet Decision No. 100 of 2024, amending the Executive Regulation of Federal Decree-Law No. 8 of 2017. The amendments define “Virtual Assets” as digital representations of value that can be digitally traded or converted and used for payment or investment, excluding digital representations of fiat currencies and financial securities.

VAT Treatment Framework Under 2024 Amendments:

| Activity Type | VAT Status | Rate | Effective Date |

| Transfer of ownership of virtual assets | Exempt financial service | 0% (exempt) | Retroactive to January 1, 2018 |

| Conversion of virtual assets | Exempt financial service | 0% (exempt) | Retroactive to January 1, 2018 |

| Custody and wallet management (explicit fee) | Taxable financial service | 5% (standard) | Prospective from amendment |

| Mining for one’s own account | Outside the scope of VAT | N/A | All periods |

| Mining services to third parties for a fee | Taxable supply | 5% or 0% (export) | All periods |

The retroactive exemption creates significant compliance implications for UAE cryptocurrency exchanges that previously charged 5% VAT on trading activities. The Federal Tax Authority VATP040 guidance instructs VAT-registered businesses to assess historical VAT treatment and consider issuing credit notes where 5% VAT was incorrectly applied to exempt virtual asset transfers from January 1, 2018 onwards.

VAT Registration Requirements

UAE cryptocurrency businesses must register for VAT when taxable supplies and imports exceed AED 375,000 in the previous twelve months or are expected to exceed AED 375,000 in the next thirty days. Voluntary registration becomes available when taxable supplies exceed AED 187,500. Registration thresholds exclude exempt supplies such as virtual asset transfers and conversions.

Input VAT Recovery Restrictions

Cryptocurrency exchanges whose primary business involves exempt virtual asset transfers face structural input VAT recovery limitations. Input VAT incurred on costs directly attributable to exempt supplies becomes non-recoverable. Businesses with mixed supplies must implement partial exemption methodologies to apportion input VAT between recoverable and non-recoverable portions.

According to FTA Public Clarification VATP039, cryptocurrency mining for own account generates no taxable supply because no identifiable recipient exists. Input VAT incurred exclusively on own-account mining becomes non-recoverable because the activity falls outside VAT scope.

Corporate Tax Framework For Crypto Companies in the UAE

UAE Corporate Tax Law (Federal Decree-Law No. 47 of 2022) applies to cryptocurrency companies operating as juridical persons resident in the UAE. The UAE Ministry of Finance implemented corporate tax effective for financial years beginning on or after June 1, 2023.

Corporate Tax Rates:

- 0% rate: Taxable income up to AED 375,000

- 9% rate: Taxable income exceeding AED 375,000

- 0% rate on Qualifying Income: Qualifying Free Zone Persons earning Qualifying Income per Cabinet Decision No. 100 of 2023

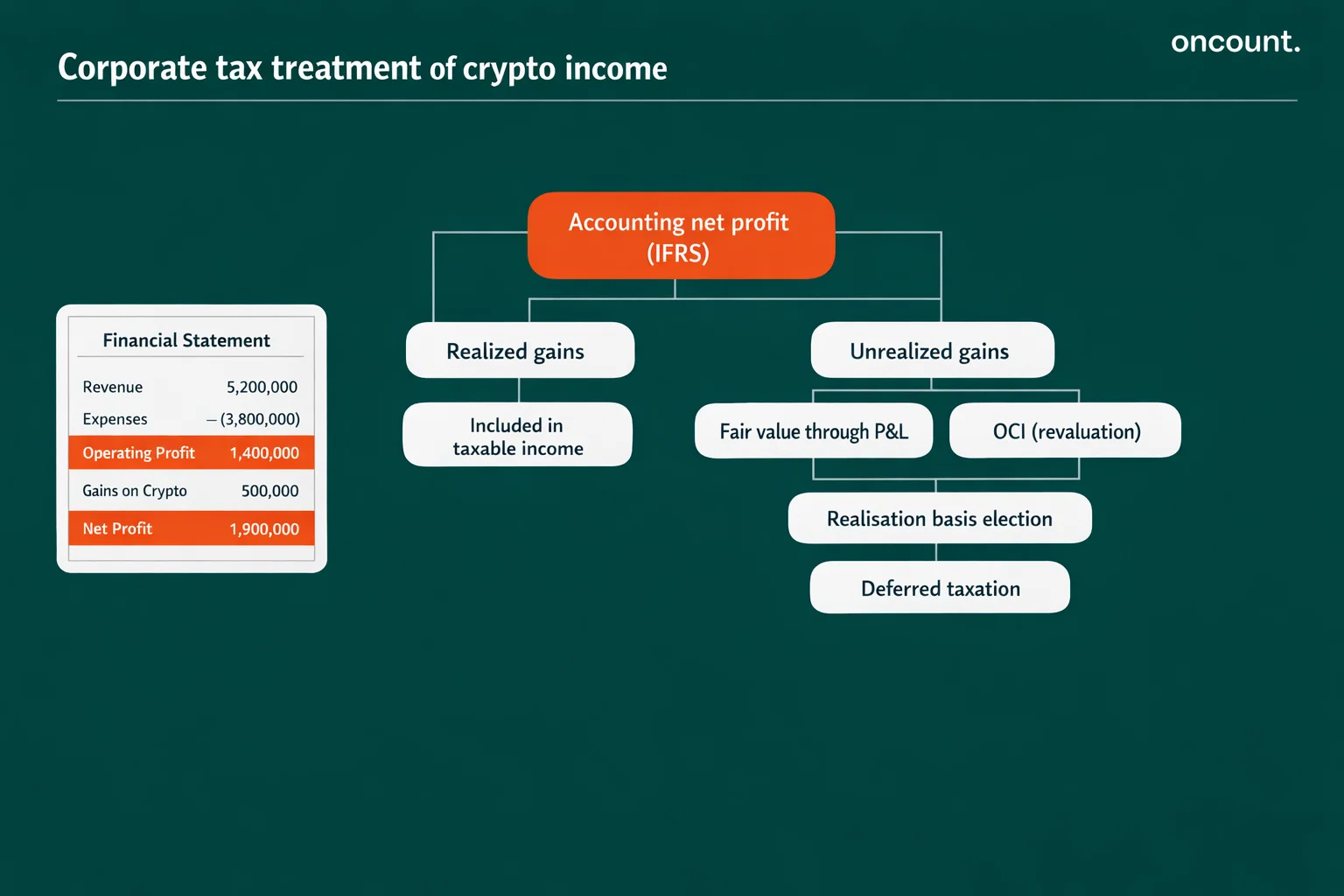

Taxable income calculation begins with accounting net profit as reported in IFRS financial statements, with statutory adjustments applied. The Federal Tax Authority Corporate Tax General Guide establishes that accounting income serves as the starting point.

Critical Tax Adjustments for Cryptocurrency Companies:

- Unrealized Gains and Losses: Cryptocurrency businesses measuring digital assets at fair value generate unrealized gains and losses in financial statements. Ministerial Decision No. 134 of 2023 allows taxable persons using accrual accounting to elect a “realisation basis” for gains and losses, preventing corporate tax liability without corresponding cash consideration.

- Other Comprehensive Income (OCI) Adjustment: The FTA Accounting Standards Guide requires taxable persons to adjust accounting income by including realized or unrealized gains and losses recognized in financial statements when those items will not be subsequently recognized in the income statement. This creates significant tax exposure for cryptocurrency businesses using IAS 38 revaluation model, because revaluation gains flow through OCI to equity rather than profit or loss, yet become immediately taxable unless realisation basis election applies.

Accounting for Revenue and Expenses in Cryptocurrency Businesses

Revenue recognition follows the IFRS 15 Revenue from Contracts with Customers five-step model. The Federal Tax Authority requires revenue accounting that distinguishes income streams because VAT treatment varies by activity type.

Revenue Stream Classification

Trading and Exchange Fees: Cryptocurrency exchanges earn commission revenue from facilitating transactions. IFRS 15 performance obligation analysis identifies trade execution as a point-in-time service satisfied at execution. Revenue recognition occurs at execution time, with the transaction price measured as a commission percentage or a fixed fee charged.

Custody and Wallet Management Fees: Digital wallet providers earn fees for maintaining secure storage. IFRS 15 characterizes custody as a stand-ready performance obligation satisfied over time. Revenue recognition follows time-based progress measurement, typically straight-line over the service period.

Staking-as-a-Service Revenue: Cryptocurrency businesses operating proof-of-stake validators earn income from protocol rewards. IFRS 15 application depends on whether stakeholder arrangements create customer contracts. When validators operate nodes on behalf of token holders for explicit fees, the service constitutes an IFRS 15 performance obligation satisfied over the staking period.

Expense Recognition

Cost of Cryptocurrency Sold: Broker-traders selling cryptocurrency inventory recognize cost of sales using FIFO (first-in, first-out) or weighted average cost formulas under IAS 2. The selected formula must be applied consistently.

Impairment Losses: Cryptocurrency holdings measured under IAS 38 cost model require impairment loss recognition when the carrying amount exceeds the recoverable amount. Impairment losses reduce profit or loss in the period recognized. Subsequent reversal becomes permitted when conditions supporting original impairment no longer exist.

Regulatory Compliance and Reporting Obligations

UAE cryptocurrency companies operate within a comprehensive regulatory framework extending beyond financial reporting and taxation.

Economic Substance Regulations (ESR)

The UAE Ministry of Finance announced the cancellation of ESR reporting requirements for financial years ending after December 31, 2022, following Cabinet Decision No. 98 of 2024. Cryptocurrency businesses conducting relevant activities during January 1, 2019 through December 31, 2022 may retain historical ESR filing obligations for those specific years.

Anti-Money Laundering (AML) Requirements

UAE cryptocurrency businesses providing wallet services, exchange operations, or virtual asset transfer services qualify as Virtual Asset Service Providers (VASPs) under UAE Cabinet Decision No. 10 of 2019. VASPs must implement comprehensive AML/CTF programs, including customer due diligence, transaction monitoring, suspicious transaction reporting, and record-keeping systems.

The accounting function supports AML compliance through maintaining transaction records that identify beneficial owners, document the source of funds, and create audit trails linking cryptocurrency movements to verified customer identities.

Ultimate Beneficial Owner (UBO) Reporting

UAE Cabinet Resolution No. 58 of 2020 requires companies to maintain registers identifying individuals who ultimately own or control the legal entity. Cryptocurrency companies must file UBO information with the relevant Commercial Registry and update filings within fifteen days of changes to the beneficial ownership structure.

Audit Requirements for Companies in the UAE

UAE audit obligations depend on jurisdiction (mainland versus free zone), company type, and revenue thresholds. The UAE Commercial Companies Law establishes baseline audit requirements, while free zone authorities may impose supplementary obligations.

Mainland Company Audit Requirements

UAE Federal Decree-Law No. 32 of 2021 (Commercial Companies Law) requires Limited Liability Companies (LLCs) and other mainland structures to appoint external auditors when specific criteria apply. Cryptocurrency companies structured as mainland LLCs typically require annual audited financial statements prepared by UAE-licensed audit firms registered with the UAE Ministry of Economy.

Free Zone Audit Requirements

Major UAE free zones hosting cryptocurrency businesses include:

- Dubai Multi Commodities Centre (DMCC): Requires annual audited financial statements for all licensed entities

- Abu Dhabi Global Market (ADGM): Audit requirements vary by license type

- Dubai International Financial Centre (DIFC): Mandatory audit for most commercial entities with limited exemptions

Auditor Expectations

External auditors examining UAE cryptocurrency businesses focus on:

- Existence and ownership verification through blockchain transaction validation

- Valuation accuracy and pricing source reliability

- Revenue recognition timing and non-cash consideration measurement

- Cryptocurrency classification based on holding purpose

- Impairment testing procedures and recoverable amount calculations

- Related party transaction transfer pricing documentation

Industry-Specific Accounting Considerations for Cryptocurrency Companies

Classification of Stablecoins and Tokenized Assets

Stablecoins present classification complexity because designs vary between fiat-backed, crypto-collateralized, and algorithmic stability mechanisms. IFRS 9 Financial Instruments applies when stablecoins create contractual rights to receive cash from an identifiable issuer. USD-pegged stablecoins offering enforceable redemption rights classify as financial assets measured under IFRS 9.

Stablecoins lacking enforceable redemption mechanisms default to IAS 38 intangible asset treatment. The distinction drives measurement approach: IFRS 9 financial assets at amortized cost accrete interest and undergo expected credit loss impairment, while IAS 38 intangibles remain at cost less impairment.

Non-Fungible Token (NFT) Accounting

NFT marketplace operators must analyze whether NFTs represent inventory for resale (IAS 2), long-term intangible holdings (IAS 38), or embedded derivatives. NFTs bundled with intellectual property rights or service access create IFRS 15 contract liability scenarios where proceeds represent advance payment for future performance obligations.

UAE VAT treatment remains uncertain for NFTs because the Federal Tax Authority guidance addresses “virtual assets” defined by tradability and investment use, potentially excluding unique non-fungible tokens from virtual asset exemption.

Mining and Staking Reward Recognition

Proof-of-work mining operations generate cryptocurrency rewards as compensation for computational work. UAE accounting practice generally treats self-mined cryptocurrency as inventory produced rather than revenue, recognizing production cost during mining and gain upon subsequent sale.

Proof-of-stake validation rewards create similar recognition questions. Conservative accounting defers income recognition until stakeholder rewards are claimed and converted to another asset or sold to third parties.

Common Accounting Challenges for Cryptocurrency Companies

| Challenge | Root Cause | Financial Impact | Tax/Compliance Risk |

| Inappropriate crypto classification | Insufficient holding purpose analysis | Incorrect measurement basis | Corporate tax timing mismatches, VAT misapplication |

| Weak wallet-to-ledger reconciliation | Manual processes, multiple wallets | Unrecorded transactions, audit failures | Incomplete VAT returns, understated tax liability |

| Inadequate fair value documentation | Lack of pricing controls | Fair value estimation challenges | Transfer pricing exposure |

| Failure to assess impairment indicators | No systematic monitoring | Overstated asset values | Overstated accounting income inflates tax |

| Incorrect VAT treatment post-2024 | Unawareness of retroactive exemption | Missed refund opportunities | Interest and penalties on incorrect returns |

Best Practices for Accounting and Financial Management

Technology Infrastructure

- Blockchain-Integrated Systems: Implement accounting platforms with native blockchain integration that automatically import transactions from wallet addresses and exchange APIs

- Automated Valuation Feeds: Configure systems to receive automated price feeds from reliable market data providers

- Multi-signature Wallet Requirements: Implement multi-party approval for cryptocurrency transfers exceeding materiality thresholds

Internal Controls

- Segregate blockchain wallet control from accounting record preparation

- Perform daily wallet reconciliation against general ledger balances

- Document pricing source hierarchy for each material cryptocurrency

- Maintain variance investigation protocols for reconciliation differences

Professional Services Engagement

Cryptocurrency businesses should engage UAE-licensed accounting firms with demonstrated cryptocurrency accounting expertise. Professional accounting services providers familiar with Federal Tax Authority cryptocurrency guidance can structure chart of accounts, design VAT compliance procedures, and prepare corporate tax computations optimizing elections such as realisation basis treatment.

Compliance Monitoring

- Monthly VAT return filing deadlines (28th of the following month)

- Annual corporate tax return filing (nine months after financial year-end)

- Quarterly impairment indicator assessments for material holdings

- UBO register updates (within 15 days of ownership changes)

- Transfer pricing documentation threshold monitoring (AED 200 million revenue test)

Comparison: Free Zone vs Mainland Accounting Requirements

| Aspect | Mainland UAE | Free Zone (DMCC, DIFC, ADGM) |

| Corporate Tax Rate | 0% on first AED 375,000; 9% on excess | 0% on Qualifying Income if QFZP status is maintained; 9% on non-qualifying |

| Qualifying Income | Not applicable | Must conduct qualifying activities, meet de minimis tests, and demonstrate adequate substance |

| Audit Requirement | Varies by company type; LLCs generally require an annual audit | Most free zones mandate an annual audit regardless of size |

| Financial Reporting | IFRS as adopted in the UAE | IFRS (DIFC/ADGM); IFRS or other accepted standards |

| VAT Treatment | Standard UAE VAT regime; exempt virtual asset transfers, taxable custody | Generally, the same VAT treatment for cryptocurrency activities |

| Client Location Restrictions | Can serve the UAE mainland and free zone clients | May face restrictions on serving mainland customers |

| Compliance Cost | Moderate audit fees; corporate tax compliance | Higher audit fees; complex qualifying income calculations |