Key Takeaways

- UAE logistics companies must maintain accounting records for a minimum of five years under Federal Tax Authority regulations

- IFRS 15 governs revenue recognition for freight forwarding, warehousing, and logistics service contracts

- VAT registration becomes mandatory when taxable supplies exceed AED 375,000 within 12 months

- UAE Corporate Tax applies a 9% rate to taxable profits exceeding AED 375,000 annually

- Free zone logistics entities may qualify for 0% corporate tax on qualifying income meeting specific conditions

- Logistics accounting requires specialized treatment for customs duties, freight charges, and cross-border transactions

- Economic Substance Regulations apply to logistics companies claiming tax benefits or operating in free zones

- Accurate accounts payable and receivable management is crucial for logistics companies to manage cash flow effectively

Overview of Accounting Requirements in the UAE for Logistics Companies

The UAE Commercial Companies Law mandates that all logistics companies operating in Dubai and the wider UAE maintain complete and accurate accounting records reflecting their financial position. According to Federal Tax Authority guidance, logistics businesses must preserve financial documentation for a minimum period of five years from the end of the relevant tax period.

Logistics companies in the UAE must structure their accounting systems to comply with International Financial Reporting Standards (IFRS) as adopted by the UAE Ministry of Finance. The Federal Tax Authority requires logistics operators to maintain detailed records of all transactions, including freight invoicing, customs clearance documentation, warehousing contracts, and transportation agreements.

The UAE logistics sector encompasses diverse business models, including freight forwarding, third-party logistics (3PL), warehousing operations, customs brokerage, and last-mile delivery services. Each operational model presents specific accounting requirements related to revenue recognition timing, expense allocation, and regulatory reporting. Dubai mainland logistics companies face different compliance obligations compared to free zone entities, particularly regarding audit requirements and corporate tax treatment.

Logistics companies cannot operate effectively without implementing proper financial controls covering accounts payable, accounts receivable, inventory management for warehoused goods, and fixed asset tracking for vehicles and equipment. The role of accounting extends beyond compliance to provide real-time financial data supporting strategic decisions about route optimization, fleet management, and operational efficiency improvements.

IFRS Application for Logistics Companies

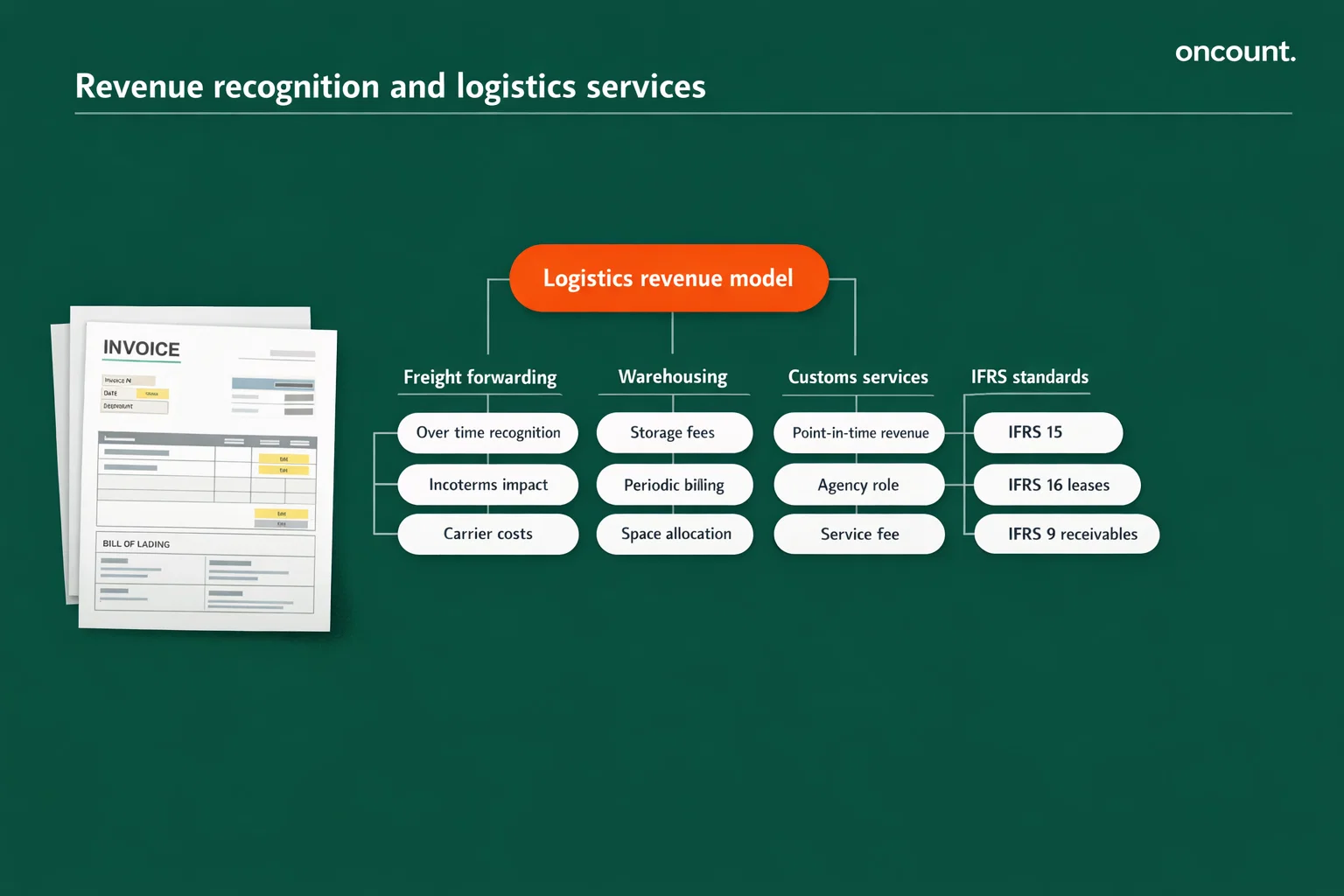

International Financial Reporting Standards provide the accounting framework for logistics companies in the UAE, with several standards having particular relevance to freight forwarding and supply chain operations. IFRS 15 (Revenue from Contracts with Customers) establishes the foundation for recognizing revenue from logistics services, requiring companies to identify performance obligations and recognize revenue when control of services transfers to customers.

Logistics companies must apply IFRS 15’s five-step model when accounting for freight forwarding contracts: identify the contract, identify performance obligations (such as pickup, transportation, customs clearance, and delivery), determine transaction price, allocate price to performance obligations, and recognize revenue as obligations are satisfied. A Dubai-based freight forwarder handling a shipment from Jebel Ali Port to European destinations must determine whether revenue recognition occurs upon departure, upon arrival, or progressively during transit.

IFRS 16 (Leases) significantly impacts logistics accounting due to the sector’s reliance on leased warehouses, distribution centers, and vehicle fleets. Logistics companies operating in the UAE must recognize right-of-use assets and lease liabilities for operating leases exceeding 12 months, fundamentally changing balance sheet presentation compared to pre-2019 standards. A logistics operator leasing a 50,000 square foot warehouse in Dubai South must capitalize the lease arrangement, recognizing both an asset and corresponding liability.

IFRS 9 (Financial Instruments) governs the treatment of trade receivables, which constitute a substantial portion of logistics companies’ working capital. The expected credit loss model under IFRS 9 requires logistics businesses to assess credit risk and recognize provisions for potential customer defaults, particularly important given extended payment terms common in freight forwarding relationships.

Bookkeeping Framework and Financial Records Structure

Effective bookkeeping for logistics companies requires a comprehensive chart of accounts tailored to capture industry-specific transaction types and operational complexity. The general ledger structure must accommodate multiple revenue streams, including freight charges, handling fees, customs clearance fees, warehousing charges, fuel surcharges, and ancillary services.

Essential Components of Bookkeeping Systems:

- Revenue Accounts – Segregated by service type (air freight, sea freight, road transport, warehousing, customs brokerage)

- Direct Cost Accounts – Carrier costs, fuel expenses, driver wages, warehouse rent, equipment maintenance

- Accounts Receivable Subsidiary Ledgers – Tracking customer invoices with aging analysis

- Accounts Payable Systems – Managing payments to carriers, suppliers, and subcontractors

- Fixed Asset Registers – Recording vehicles, warehouse equipment, handling machinery, IT systems

- Prepayment and Accrual Accounts – Handling timing differences in freight charges and service delivery

Logistics companies in Dubai must maintain supporting documentation for every financial transaction, including commercial invoices, bills of lading, airway bills, customs declarations, warehouse receipts, proof of delivery, and payment confirmations. The Federal Tax Authority requires these documents to substantiate VAT treatment and corporate tax deductions.

Accounting software implementation is essential for logistics businesses to streamline operations and ensure compliance. Cloud-based platforms enable real-time financial visibility across multiple locations, automated invoice generation, integration with customs systems, and seamless VAT reporting. Leading logistics companies in the UAE utilize specialized accounting solutions that interface with transportation management systems (TMS) and warehouse management systems (WMS) to ensure data accuracy.

Proper segregation of duties within the bookkeeping function protects logistics companies from fraud and errors. The finance team should separate transaction authorization, recording, and reconciliation responsibilities, with regular management review of financial processes.

Financial Statements Preparation Requirements

Logistics companies in the UAE must prepare comprehensive financial statements adhering to IFRS presentation requirements and meeting Federal Tax Authority expectations. The core financial statements include the balance sheet (statement of financial position), profit and loss statement (income statement), cash flow statement, and notes to financial statements providing detailed disclosures.

The balance sheet for logistics operators must clearly present current assets, including trade receivables from customers, prepaid freight charges, and inventory of packaging materials. Non-current assets typically include vehicle fleets, warehouse facilities (if owned), handling equipment, and right-of-use assets from lease arrangements. The liabilities section must distinguish between current obligations to carriers and suppliers versus long-term financing for equipment purchases.

The profit and loss statement should segregate revenue by service line, enabling profitability analysis across freight forwarding, warehousing, and value-added services. Cost of services sold must include direct carrier costs, customs duties paid on behalf of clients, fuel expenses, and labor costs for handling operations. Operating expenses encompass administrative salaries, facility costs, insurance, and depreciation of logistics assets.

The cash flow statement holds particular importance for logistics companies given the capital-intensive nature of fleet operations and working capital requirements. Cash flow from operations reflects the conversion of receivables into cash, a critical metric for assessing financial health given extended payment terms common in freight relationships. Cash flow from investing activities captures vehicle purchases and warehouse investments, while financing activities show debt servicing and equity transactions.

Notes to financial statements must disclose accounting policies for revenue recognition, significant estimates and judgments, related party transactions (common in family-owned logistics businesses), lease commitments, contingent liabilities from customs guarantees, and post-balance sheet events affecting logistics operations.

Accurate financial reporting supports multiple stakeholders, including investors evaluating profitability, lenders assessing creditworthiness, customs authorities verifying financial standing, and the Federal Tax Authority determining tax obligations.

VAT Compliance for Logistics Companies in the UAE

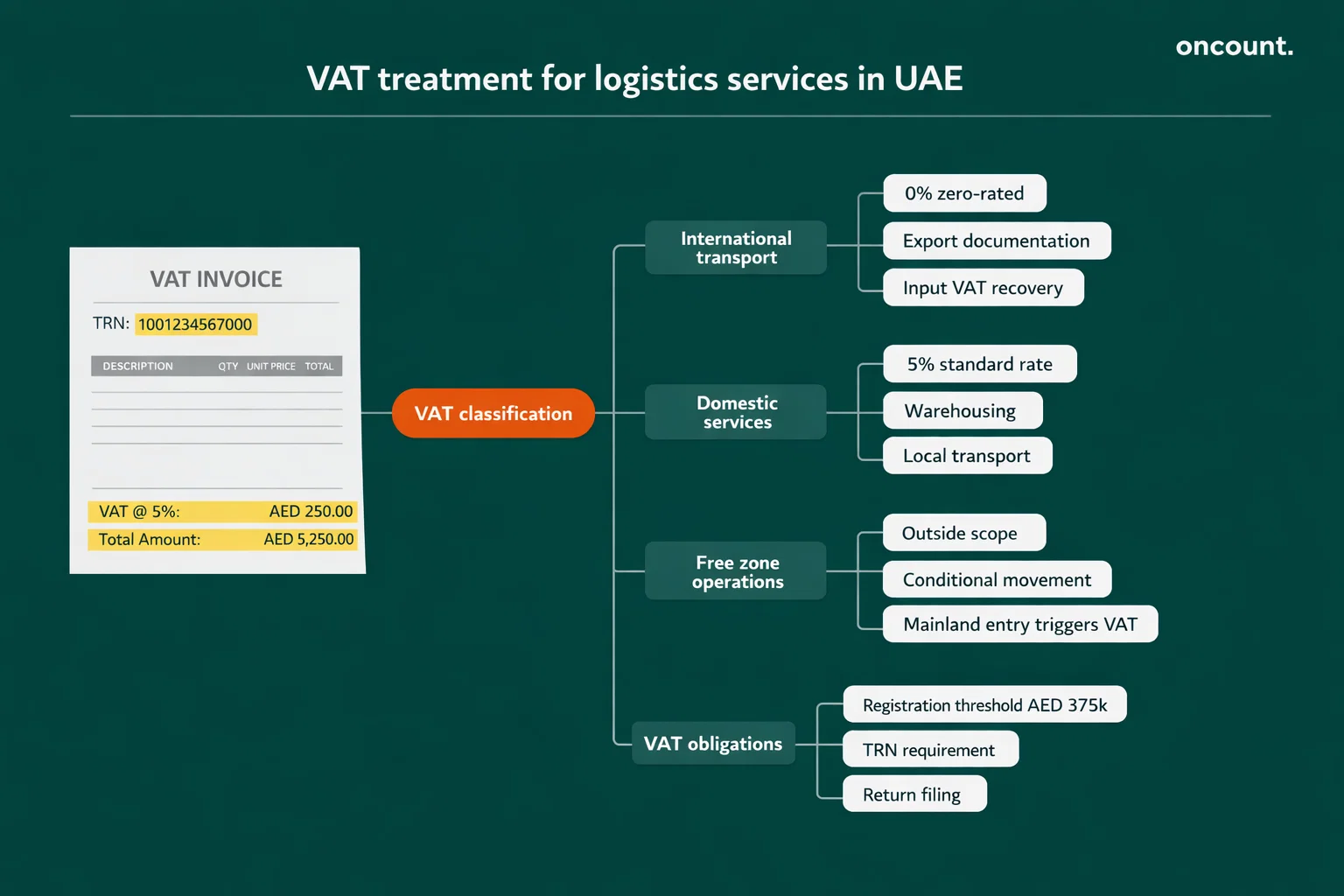

Value Added Tax compliance presents complex challenges for logistics companies in the UAE due to the diverse nature of freight forwarding transactions and special VAT treatment applicable to international transportation. Federal Decree-Law No. 8 of 2017 established the UAE VAT framework, with the Federal Tax Authority providing sector-specific guidance for logistics operators.

VAT Registration Requirements for Logistics Businesses:

| Threshold Type | Annual Taxable Supplies | Registration Obligation |

| Mandatory Registration | Exceeds AED 375,000 | Must register within 30 days |

| Voluntary Registration | Exceeds AED 187,500 | May apply for registration |

| Freight Forwarding Specifics | International transport services | Zero-rated supplies increase threshold consideration |

Logistics companies in Dubai must distinguish between zero-rated supplies (0% VAT charged but input VAT recoverable), exempt supplies (no VAT charged and input VAT non-recoverable), and standard-rated supplies (5% VAT) when calculating registration thresholds and preparing VAT returns.

International transportation of goods and passengers qualifies for zero-rating under UAE VAT law, meaning freight forwarding companies providing cross-border logistics services charge 0% VAT to customers while recovering input VAT on related expenses. A Dubai-based freight forwarder transporting goods from Jebel Ali Port to European destinations applies zero-rating to freight charges, while domestic warehousing services within the UAE attract standard 5% VAT.

VAT Treatment of Common Logistics Services:

- Air and Sea Freight (International) – Zero-rated at 0%

- Domestic Transportation within UAE – Standard-rated at 5%

- Warehousing and Storage – Standard-rated at 5%

- Customs Brokerage Services – Standard-rated at 5%

- Designated Zone Services – Specific rules apply based on location and customer status

Logistics companies must implement robust systems to track the geographic location of services provided, customer tax status, and nature of supplies to ensure accurate VAT treatment. Errors in VAT classification can result in penalties from the Federal Tax Authority and cash flow implications from incorrect input VAT recovery.

VAT return filing frequency depends on annual turnover, with logistics companies exceeding AED 150 million filing monthly returns while smaller operators file quarterly. The EmaraTax portal, administered by the Federal Tax Authority, enables electronic submission of VAT returns, payment processing, and correspondence with tax authorities.

Input VAT recovery for logistics companies encompasses fuel costs, vehicle maintenance, warehouse rent, handling equipment purchases, insurance premiums, and professional fees. Proper documentation, including tax invoices showing supplier Tax Registration Number (TRN), transaction details, and VAT amount, is essential to substantiate input VAT claims.

Corporate Tax Framework in the UAE

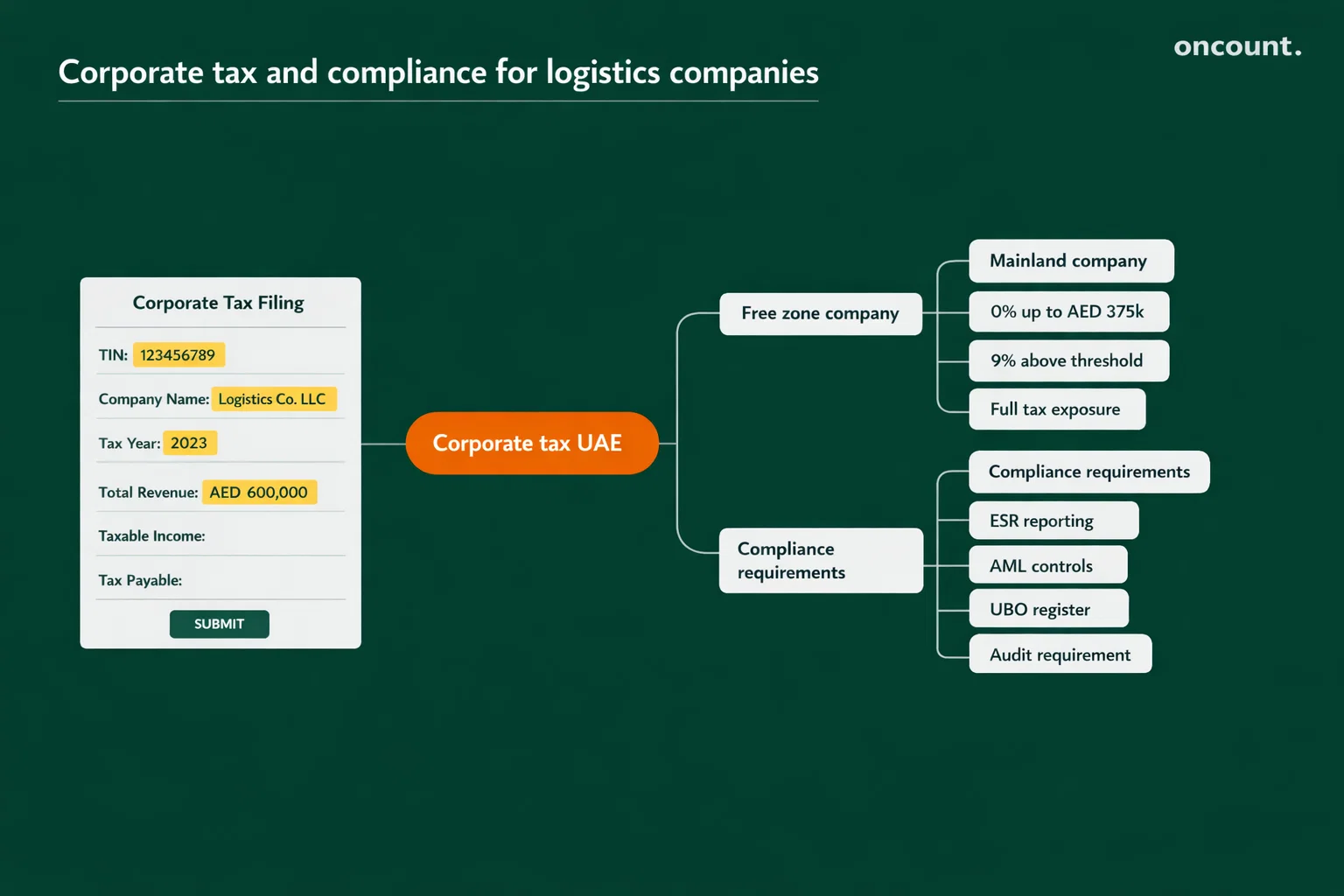

The UAE Corporate Tax Law (Federal Decree-Law No. 47 of 2022) introduced corporate taxation effective for financial years beginning on or after June 1, 2023, fundamentally changing the tax landscape for logistics companies operating in Dubai and across the UAE. Understanding UAE corporate tax requirements is crucial for logistics companies to ensure compliance and optimize tax positions.

UAE Corporate Tax Rates Applicable to Logistics Companies

| Taxable Income Threshold | Tax Rate | Application |

| Up to AED 375,000 | 0% | Small business relief threshold |

| Above AED 375,000 | 9% | Standard corporate tax rate |

| Qualifying Free Zone Income | 0% | Subject to meeting specific conditions |

Logistics companies must calculate taxable income by adjusting accounting profits for tax purposes, adding back non-deductible expenses and subtracting exempt income. The UAE Ministry of Finance Corporate Tax Guide (2023) clarifies that businesses must maintain audited financial statements for accurate tax determination.

Deductible Expenses for Logistics Operations:

- Employee salaries and benefits for drivers, warehouse staff, and administrative personnel

- Carrier costs paid to airlines, shipping lines, and road transport providers

- Fuel and vehicle maintenance expenses for the company-owned fleet

- Warehouse rental payments and facility operating costs

- Depreciation of logistics assets, including vehicles and handling equipment

- Insurance premiums for cargo, vehicles, and liability coverage

- Professional fees for accounting, legal, and compliance services

Non-Deductible Expenses:

- Entertainment expenses exceeding regulatory limits

- Penalties and fines imposed by customs or regulatory authorities

- Provisions for doubtful debts not meeting specific write-off criteria

- Transactions with related parties not conducted at arm’s length

Free zone logistics companies may qualify for 0% corporate tax on qualifying income provided they maintain adequate substance, conduct qualifying activities, and comply with transfer pricing requirements when dealing with related parties. Dubai Airport Freezone (DAFZA), Jebel Ali Free Zone (JAFZA), and Dubai South Free Zone host numerous logistics operators potentially eligible for preferential tax treatment.

Logistics companies in the UAE must register for corporate tax through the EmaraTax portal, obtain a Tax Registration Number, and file annual corporate tax returns within nine months of the financial year-end. Late registration, filing failures, or payment delays result in penalties calculated as a percentage of the unpaid tax amounts.

Transfer pricing regulations under the UAE Corporate Tax Law require logistics companies with related party transactions to maintain documentation demonstrating arm’s length pricing. International logistics groups with UAE subsidiaries must prepare master files, local files, and potentially country-by-country reports depending on revenue thresholds.

Accounting for Revenue and Expenses in Logistics Operations

Revenue recognition for logistics companies requires careful analysis of contractual arrangements and application of IFRS 15 principles to diverse service offerings. Freight forwarding revenue recognition timing depends on whether the logistics company acts as principal or agent in the transaction.

When logistics companies in Dubai operate as principals, controlling services before transfer to customers, they recognize gross revenue including carrier costs. A freight forwarder arranging sea transportation, customs clearance, and final delivery while assuming responsibility for service completion recognizes total freight charges as revenue with carrier payments recorded as cost of sales.

Conversely, when logistics companies act as agents, merely facilitating connections between customers and carriers, they recognize net commission revenue. Customs brokerage services often fall into this category, with the logistics company earning fees for documentation and regulatory submissions while passing through customs duties without including them in revenue.

Revenue Recognition Patterns for Logistics Services:

- Point-in-Time Recognition – Customs clearance fees, handling charges, documentation services

- Over-Time Recognition – Long-haul freight transportation, warehousing contracts, logistics management

- Variable Consideration – Fuel surcharges, detention charges, performance bonuses

Expense classification for logistics companies must distinguish between the cost of services (directly attributable to revenue generation) and operating expenses (supporting overall business operations). Fuel costs, carrier payments, and customs duties paid on behalf of clients represent direct costs, while administrative salaries, office rent, and marketing expenses constitute operating costs.

Logistics companies operating in the UAE must account for foreign currency transactions, given the international nature of freight forwarding. The UAE Dirham (AED) is pegged to the US Dollar, providing stability for US dollar transactions, but logistics companies dealing with European, Asian, or other markets face currency exposure requiring proper hedge accounting under IFRS 9.

Profitability analysis by service line, customer segment, and trade lane enables logistics management to guide strategic decisions about resource allocation and business development. A Dubai logistics company may discover that air freight operations generate higher margins than sea freight despite lower volumes, informing sales strategy and operational focus.

Regulatory Compliance and Reporting Obligations

Logistics companies in the UAE navigate multiple regulatory frameworks beyond tax compliance, including Economic Substance Regulations, Anti-Money Laundering requirements, and Ultimate Beneficial Owner disclosure obligations. These frameworks impact accounting processes, documentation requirements, and governance structures.

Economic Substance Regulations (ESR)

Apply to UAE logistics companies engaged in relevant activities and claiming tax benefits. Cabinet Resolution No. 31 of 2019 requires qualifying entities to demonstrate adequate substance through sufficient employees, adequate operating expenditure, and physical presence in the UAE. Logistics companies must submit annual ESR notifications and reports to the UAE Ministry of Finance, with financial data supporting substantiated claims.

ESR compliance for logistics operators requires documentation showing UAE-based decision-making, adequate staff with necessary qualifications managing logistics operations, and physical infrastructure, including warehouses and offices. Failure to meet substance requirements can result in penalties starting at AED 10,000 for notification failures and escalating to AED 50,000 for repeated non-compliance.

Anti-Money Laundering (AML)

Regulations under Federal Decree-Law No. 20 of 2018 impose obligations on logistics companies to implement customer due diligence procedures, monitor transactions for suspicious activity, and report to the Financial Intelligence Unit when required. Logistics accounting systems must flag unusual transaction patterns, verify customer identities, and maintain audit trails for regulatory inspection.

The freight forwarding sector faces particular AML risks given cross-border transaction flows, cash-intensive operations in certain markets, and potential use of logistics networks for trade-based money laundering. Logistics companies in Dubai must implement risk-based AML frameworks proportionate to their business model and customer profile.

Ultimate Beneficial Owner (UBO)

reporting requirements mandate that UAE logistics companies disclose individuals who ultimately own or control the business entity. Cabinet Resolution No. 58 of 2020 requires companies to maintain UBO registers and submit information to relevant authorities, with financial penalties for non-compliance.

Customs compliance represents another critical regulatory area for freight forwarders, requiring accurate declaration of goods values, tariff classifications, and origin documentation. Logistics companies must maintain detailed records supporting customs declarations, as errors can trigger audits, duty reassessments, and penalties affecting financial performance.

Audit Requirements for Logistics Companies in the UAE

Statutory audit requirements for logistics companies in the UAE depend on legal structure, location (mainland versus free zone), and business size. Understanding when audits are mandatory helps logistics operators ensure compliance and avoid penalties while benefiting from enhanced financial credibility.

Mainland UAE logistics companies structured as Limited Liability Companies (LLCs) must obtain annual audits conducted by UAE-licensed auditors registered with the appropriate regulatory authorities. The UAE Commercial Companies Law requires LLCs to appoint auditors at general assembly meetings, with auditors examining financial statements and issuing opinions on whether accounts present fairly in all material respects.

Free zone logistics entities face varying audit requirements depending on the specific free zone jurisdiction. Jebel Ali Free Zone (JAFZA) requires annual audits for all companies, while Dubai Airport Freezone (DAFZA) mandates audits based on revenue thresholds. Logistics companies operating in Dubai South Free Zone must comply with that authority’s specific audit regulations.

| Entity Type | Location | Audit Requirement | Filing Deadline |

| LLC | Mainland Dubai | Mandatory annual audit | Within the specified period after the year-end |

| Free Zone Company | JAFZA | Mandatory annual audit | Per free zone regulations |

| Free Zone Company | DAFZA | based on revenue | Per free zone regulations |

| Branch of Foreign Company | Mainland | Mandatory annual audit | Regulatory requirement |

Corporate tax implementation increased audit importance for logistics companies, as the Federal Tax Authority relies on audited financial statements when assessing tax positions. Logistics businesses claiming free zone benefits or deductions must provide audited accounts supporting their corporate tax returns.

Specialized Accounting Practices for Freight Forwarding and Logistics

Multi-Currency Transaction Management

Logistics companies in the UAE routinely handle transactions in multiple currencies given their role in global trade. Freight invoices may be denominated in US Dollars, Euros, British Pounds, or other currencies, depending on trade lanes and customer preferences. Accounting systems must capture foreign exchange gains and losses resulting from currency fluctuations between transaction dates and settlement dates.

The UAE Dirham’s peg to the US Dollar at approximately 3.67 AED per USD provides stability for dollar-denominated freight contracts, but logistics companies dealing with European or Asian markets face exchange rate volatility. IFRS requires recognition of foreign exchange differences in profit or loss, impacting reported profitability for logistics operations.

Customs Duty and Tax Accounting

Freight forwarders frequently advance customs duties and import taxes on behalf of clients, creating complex accounting for amounts paid and subsequently recovered. Logistics companies must clearly distinguish between customs charges that represent pass-through items (not recognized as revenue) versus handling fees for customs clearance services (recognized as revenue).

A Dubai freight forwarder clearing imported goods through Dubai Customs may advance AED 50,000 in customs duties plus AED 2,500 in handling fees. The accounting treatment records AED 50,000 as a receivable from the customer (offset by the payment to customs) while recognizing AED 2,500 as logistics service revenue.

Fleet and Equipment Depreciation

Logistics companies operating vehicle fleets must implement appropriate depreciation policies reflecting asset useful lives and residual values. Trucks, delivery vans, and handling equipment require systematic depreciation allocation over expected service periods, typically 5-10 years for commercial vehicles, depending on usage intensity.

Accounting standards require logistics companies to assess residual values annually, adjusting depreciation rates when disposal values change due to market conditions. The UAE’s used vehicle market influences residual value estimates for logistics fleet assets.

Warehousing Cost Allocation

Third-party logistics providers offering warehousing services must allocate facility costs across multiple customers utilizing shared space. Accounting systems should track occupancy by customer, duration of storage, and value-added services provided to support accurate profitability analysis and pricing decisions.

Cloud-based accounting software enables logistics companies to integrate warehouse management systems with financial platforms, automatically capturing storage duration, handling activities, and associated costs for billing and financial reporting purposes.

Common Accounting Challenges for Logistics Companies in the UAE

Revenue Recognition Complexity

Logistics companies face significant challenges in determining appropriate revenue recognition timing for complex service arrangements involving multiple performance obligations. A comprehensive logistics contract covering pickup, international freight, customs clearance, warehousing, and final delivery requires careful analysis to identify distinct performance obligations and allocate the transaction price appropriately.

Misapplication of IFRS 15 can result in premature or delayed revenue recognition, distorting financial performance and potentially triggering audit qualifications. Logistics companies operating in the UAE should engage professional accounting advisors to establish proper revenue recognition policies and train finance teams on the correct application.

VAT Classification Errors

The distinction between zero-rated international transportation and standard-rated domestic services creates frequent VAT compliance errors for logistics companies. Incorrectly applying zero-rating to domestic portions of multi-leg journeys, or failing to identify when international transportation rules apply, leads to VAT underpayment and potential penalties.

A logistics company transporting goods from Dubai to Abu Dhabi for subsequent export must charge 5% VAT on the domestic leg, despite the goods’ ultimate international destination. Failure to recognize this treatment results in VAT compliance failures discoverable during Federal Tax Authority audits.

Cash Flow Management Difficulties

Extended payment terms common in logistics relationships create cash flow pressures, particularly when logistics companies must advance carrier costs and customs duties before collecting from customers. The aging of accounts receivable to 60-90 days, while accounts payable require 30-day settlement, strains working capital.

Inadequate cash flow management forces logistics companies to rely on expensive short-term financing, eroding profit margins. Professional accounting services help implement cash flow forecasting, credit control procedures, and working capital optimization strategies.

Related Party Transaction Documentation

Family-owned logistics businesses and international logistics groups with UAE subsidiaries face challenges documenting related party transactions at arm’s length prices. Transfer pricing regulations under the UAE Corporate Tax Law require contemporaneous documentation supporting pricing of services between related entities.

A Dubai logistics subsidiary providing warehousing services to a parent company in Europe must establish fees comparable to charges for unrelated customers, maintaining documentation demonstrating commercial rationale. Failure to meet transfer pricing requirements can result in tax adjustments and penalties.

Inadequate Internal Controls

Rapid growth in the UAE logistics sector sometimes outpaces the development of proper internal financial controls. Weak segregation of duties, lack of approval hierarchies, and insufficient reconciliation procedures increase risks of errors and fraud.

Logistics companies must implement control frameworks covering purchase order authorization, invoice verification, payment approval, bank reconciliations, and management review of financial results. Regular internal audits identify control deficiencies requiring remediation.

Best Practices for Logistics Accounting and Financial Management

Implement Industry-Specific Accounting Software

Logistics companies should deploy specialized accounting solutions designed for freight forwarding, warehousing, and supply chain operations. Cloud-based platforms offer real-time financial visibility, automated invoice generation, seamless integration with transportation management systems, and compliance with UAE regulations.

Leading accounting software for logistics businesses includes modules for:

- Multi-currency transaction processing

- Automated freight invoice generation

- Integration with customs systems

- VAT calculation and reporting

- Corporate tax compliance

- Real-time profitability analysis by customer and trade lane

Automation reduces manual data entry errors, streamlines operations, and enables finance teams to focus on analysis rather than transaction processing.

Establish a Robust Internal Control Framework

Professional accounting practices require logistics companies to implement controls separating transaction authorization, recording, and reconciliation functions. Management should review financial performance monthly, investigate variances from budgets, and ensure compliance with accounting policies.

Key internal controls include:

- Approval hierarchies for vendor payments and customer credits

- Regular bank reconciliations are completed within five business days

- Monthly accounts receivable aging reviews with collection follow-up

- Physical inventory counts for warehouse operations

- Segregation between customer invoicing and cash receipt functions

Engage Qualified Accounting Professionals

Logistics companies benefit from retaining experienced accountants and auditors familiar with UAE regulations and logistics industry practices. Professional accounting firms provide services including:

- Monthly bookkeeping and financial statement preparation

- VAT compliance and return filing

- Corporate tax planning and return preparation

- Economic Substance Regulations reporting

- Audit coordination and financial statement attestation

- Management reporting and profitability analysis

Outsourcing accounting functions to specialized providers enables logistics management to focus on core operations while ensuring compliance and financial accuracy.

Conduct Regular Financial Reviews and Forecasting

Proactive financial management requires logistics companies to prepare monthly management accounts, compare actual results against budgets, and forecast cash flows for upcoming periods. Regular financial reviews identify emerging issues before they become critical problems.

Management dashboards should display key performance indicators, including:

- Gross profit margin by service line

- Days’ sales outstanding in accounts receivable

- Operating expense ratio as a percentage of revenue

- EBITDA and net profit trends

- Cash position and working capital adequacy

Maintain Comprehensive Documentation

Regulatory compliance depends on maintaining complete records supporting financial transactions, tax positions, and customs declarations. Logistics companies should implement document management systems capturing:

- Commercial invoices and bills of lading

- Proof of delivery documentation

- Customs clearance records

- VAT tax invoices from suppliers

- Customer contracts and rate agreements

- Board minutes documenting significant decisions

Digital document retention systems enable efficient retrieval during audits and regulatory inquiries while meeting the Federal Tax Authority’s five-year record retention requirement.

Comparison: Free Zone vs Mainland Accounting Requirements

Logistics companies deciding between a free zone and a mainland establishment in Dubai must understand the different accounting, tax, and compliance requirements affecting each jurisdiction.

| Aspect | Mainland Company | Free Zone Company |

| Corporate Tax Rate | 9% on taxable profits above AED 375,000 | Potentially 0% on qualifying income meeting conditions |

| Audit Requirement | Mandatory annual audit for LLCs | Varies by free zone; often mandatory |

| VAT Registration | Required if exceeding thresholds | Required if exceeding thresholds |

| Economic Substance | Generally not applicable unless claiming benefits | Required for companies claiming tax benefits |

| Transfer Pricing | Required for related party transactions | Required for related party transactions |

| License Flexibility | Can operate anywhere in the UAE mainland | Typically restricted to free zones and international operations |

| Ownership Structure | Requires a UAE national partner or ownership under certain conditions | 100% foreign ownership permitted |

| Banking Requirements | Standard UAE banking procedures | May have enhanced requirements |

Logistics companies should evaluate operational requirements, target markets, tax positions, and long-term growth plans when selecting a jurisdiction. Professional advisors can model financial implications under different scenarios to guide strategic decisions.