Key Takeaways

- UAE Corporate Tax applies a 9% rate to taxable profits exceeding AED 375,000 under Federal Decree-Law No. 47 of 2022

- VAT registration is mandatory when taxable supplies exceed AED 375,000 within any 12-month period

- All UAE companies must prepare financial statements aligned with IFRS or IFRS for SMEs

- VAT returns are filed quarterly, with payment due by the 28th of the following month

- Corporate tax returns must be submitted within 9 months of the fiscal year-end

- Audited financial statements are mandatory for entities with UAE revenue exceeding AED 50 million, or any qualifying free zone person

- Emirati employee social insurance contributions are the employer’s responsibility at approximately 12.5% of pensionable salary

- Records must be retained for a minimum of 7 years for corporate tax and 5 years for VAT purposes

Overview of Accounting Requirements in the UAE for Startup Companies

The UAE Commercial Companies Law (Federal Decree-Law No. 32 of 2021) requires all registered companies to maintain complete and accurate accounting records from the date of incorporation. This obligation applies regardless of revenue size, legal structure, or free zone jurisdiction. The Federal Tax Authority reinforces this requirement: businesses that fail to maintain adequate records face administrative penalties starting at AED 10,000 per violation.

Startups operating as mainland LLCs, free zone entities, or branch offices must retain financial documentation — including invoices, contracts, bank statements, and ledger records — for a minimum of five years under UAE VAT law, and seven years under the Corporate Tax Law. Where these obligations overlap, the longer retention period takes precedence.

The UAE Ministry of Finance mandates that all taxable persons prepare accounts on an accrual basis unless annual revenue remains below AED 3 million, in which case the FTA may permit cash-basis accounting upon formal approval. Startups projecting early-stage growth beyond this threshold should adopt accrual accounting immediately to avoid the administrative burden of transitioning systems mid-year.

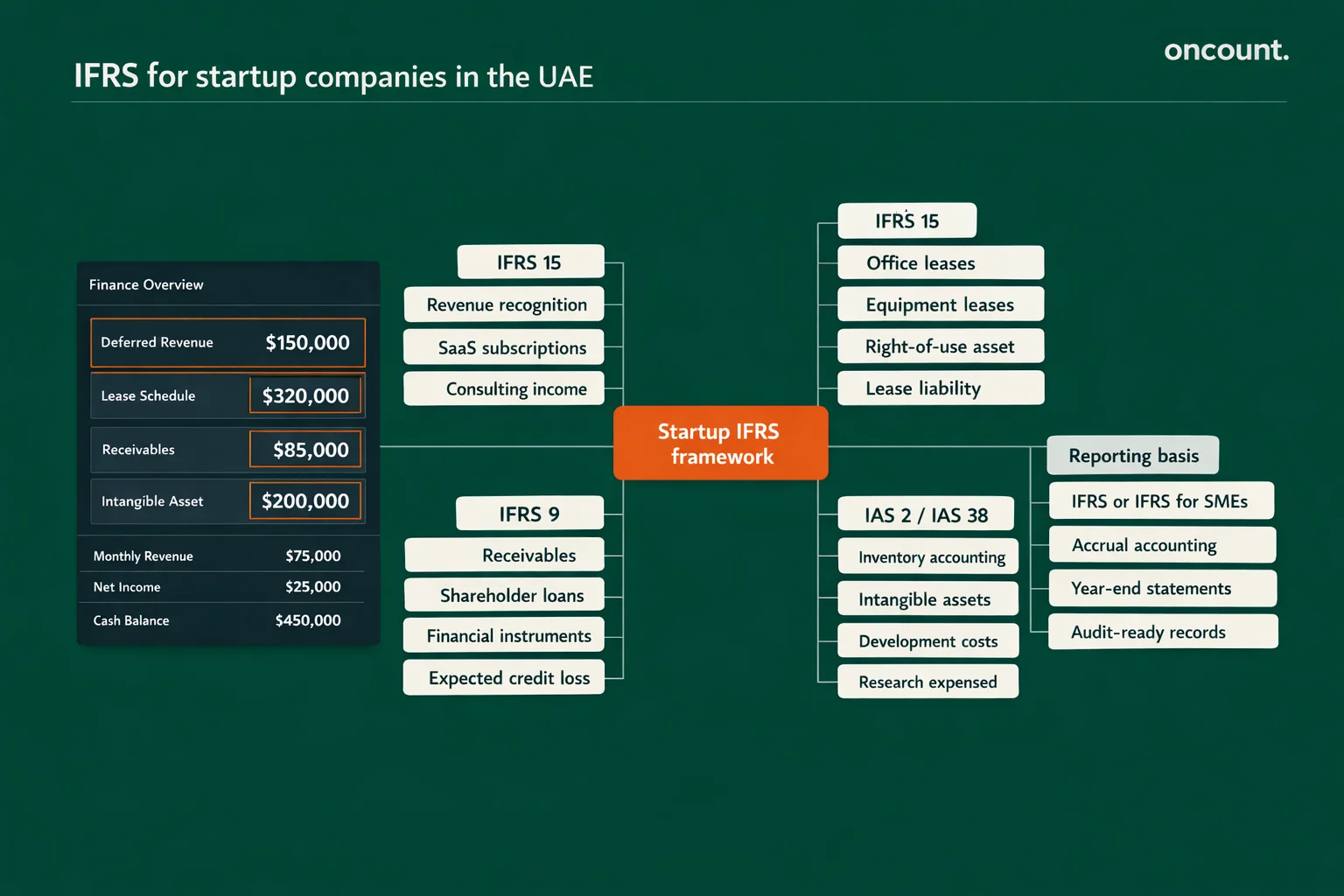

IFRS Application for Startup Companies in the UAE

UAE companies are legally required to prepare financial statements in accordance with International Financial Reporting Standards (IFRS) as issued by the IFRS Foundation. The UAE Securities and Commodities Authority, the UAE Central Bank, and stock exchange regulators all mandate IFRS compliance for reporting entities. Smaller startups may apply IFRS for SMEs, a simplified framework designed to reduce reporting complexity while maintaining international credibility.

Key IFRS standards with direct relevance to UAE startups include:

- IFRS 15 (Revenue from Contracts with Customers) — governs when and how startup revenue is recognized, particularly for SaaS, consulting, or service-based businesses

- IFRS 16 (Leases) — requires capitalization of operating leases, directly impacting startups that lease office space or equipment

- IFRS 9 (Financial Instruments) — applies to startups holding receivables, loans, or investment instruments

- IAS 2 (Inventories) — relevant for product-based startups managing stock

DIFC and ADGM-registered companies face an additional layer of IFRS enforcement: the Dubai Financial Services Authority (DFSA) and ADGM Financial Services Regulatory Authority both require IFRS-compliant accounts as a condition of licensing and renewal.

Bookkeeping Framework and Financial Records Structure

A structured bookkeeping framework enables UAE startups to meet FTA audit requirements, generate management reports, and support investor due diligence. Professional accountants in UAE typically recommend establishing a chart of accounts aligned with IFRS classifications from the first month of operations.

Core components of a startup bookkeeping framework:

- General ledger organized by asset, liability, equity, revenue, and expense categories

- Chart of accounts with numbered codes (e.g., 1000-series for assets, 2000-series for liabilities)

- Supporting documentation for every transaction: tax invoices, delivery notes, payment confirmations, and signed contracts

- Bank reconciliation performed monthly to verify ledger accuracy against official bank statements

- Payroll records maintained per the Wage Protection System (WPS) requirements of the UAE Ministry of Human Resources and Emiratization

| Account Range | Category | Examples |

| 1000–1999 | Current & Fixed Assets | Cash, receivables, equipment |

| 2000–2999 | Liabilities | Payables, VAT payable, GOSI contributions |

| 3000–3999 | Equity | Share capital, retained earnings |

| 4000–4999 | Revenue | Sales, service fees, interest income |

| 5000–6999 | Expenses | Salaries, rent, depreciation, professional fees |

Cloud accounting platforms such as Wafeq (FTA-accredited), Xero, and Zoho Books support multi-currency transactions, VAT return preparation, and direct integration with UAE banking systems. Startups selecting accounting software should prioritize FTA-accredited platforms to ensure VAT reports meet EmaraTax submission standards.

Financial Statements Preparation Requirements

UAE startups must prepare a complete set of IFRS-compliant financial statements at each fiscal year-end. These statements serve multiple regulatory purposes: supporting the corporate tax return, satisfying free zone renewal requirements, and providing auditors with the basis for their opinion.

Mandatory financial statement components:

- Statement of Financial Position (Balance Sheet) — reflects assets, liabilities, and equity at year-end

- Statement of Profit or Loss — summarizes revenue, costs, and net income for the reporting period

- Statement of Cash Flows — categorizes cash movements into operating, investing, and financing activities

- Statement of Changes in Equity — tracks movements in share capital and retained earnings

- Notes to Financial Statements — discloses accounting policies, significant estimates, and regulatory disclosures

According to Ministerial Decision No. 84 of 2025 issued by the UAE Ministry of Finance, any single entity generating UAE revenue above AED 50 million must submit audited financial statements alongside its corporate tax return. All corporate tax groups, regardless of size, are also subject to mandatory audit requirements. Qualifying Free Zone Persons must maintain audited accounts to demonstrate economic substance compliance, as required under Cabinet Decision No. 55 of 2023.

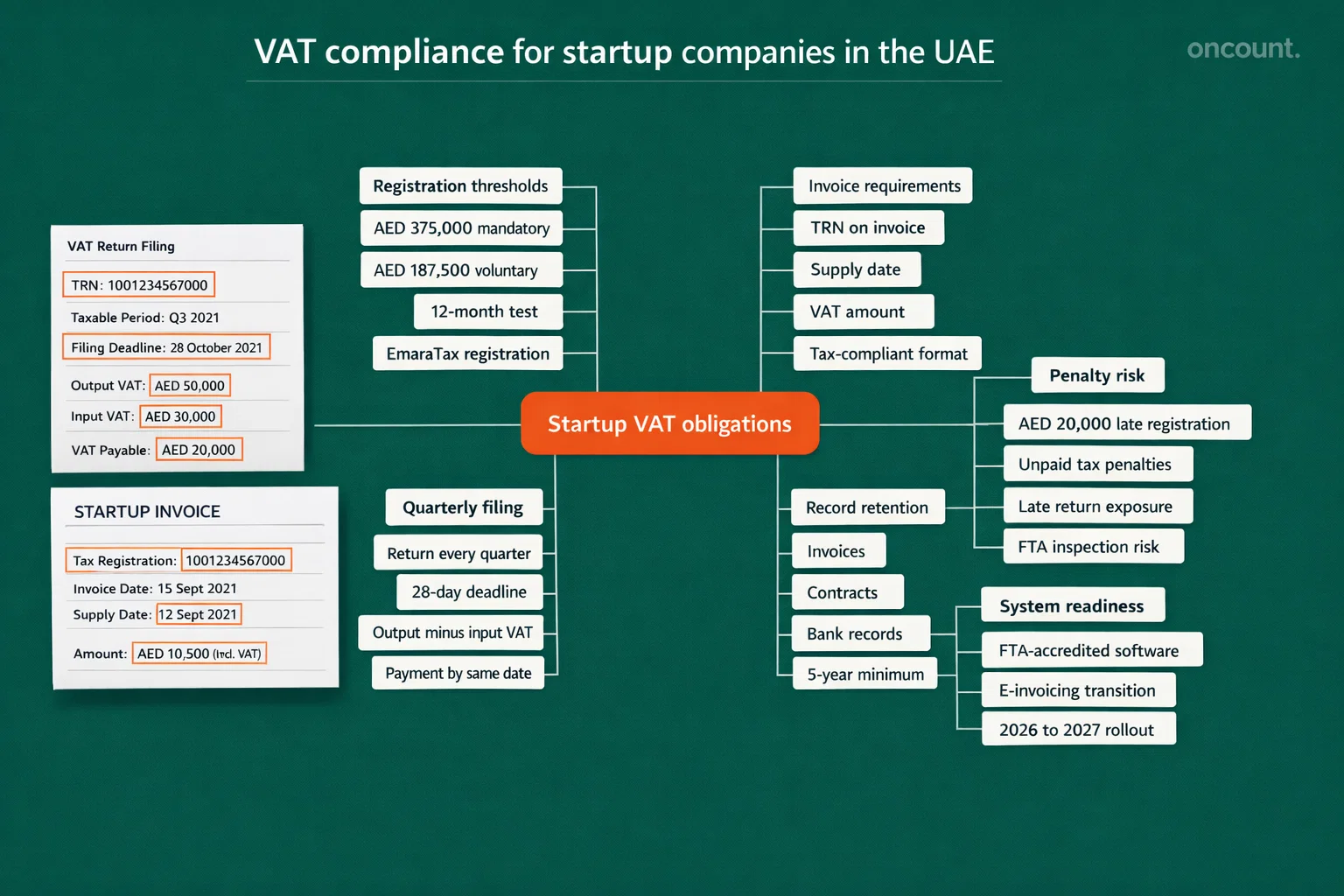

VAT Compliance for Startup Companies in the UAE

UAE Value-Added Tax is governed by Federal Decree-Law No. 8 of 2017, which established a standard 5% rate on most goods and services supplied within the UAE. Mandatory VAT registration applies when a startup’s taxable supplies and imports exceed AED 375,000 within any consecutive 12-month period. A voluntary registration threshold of AED 187,500 is also available, which many startups utilize to reclaim input VAT on early-stage expenses.

VAT registration and filing obligations:

- Register with the Federal Tax Authority through the EmaraTax portal within 30 days of surpassing the mandatory threshold

- Assign a VAT-registered accountant or tax agent to manage filings

- Issue tax-compliant invoices that include the supplier’s TRN, VAT amount, and supply date

- File quarterly VAT returns no later than the 28th day of the month following each tax period

- Remit net VAT due (output VAT minus input VAT) by the same deadline

| VAT Obligation | Threshold / Deadline | Penalty for Non-Compliance |

| Mandatory registration | AED 375,000 in 12 months | AED 20,000 late registration penalty |

| Voluntary registration | AED 187,500 | N/A |

| Quarterly return filing | 28th of following month | 2%–300% of unpaid tax |

| Record retention | 5 years minimum | AED 10,000–50,000 per violation |

The UAE Federal Tax Authority is implementing mandatory e-invoicing by 2027. Businesses with annual revenue of AED 50 million or more must engage an accredited e-invoicing provider by July 2026 and go live by January 2027. Smaller startups must comply by mid-2027, making early system integration a strategic priority rather than a deferred obligation.

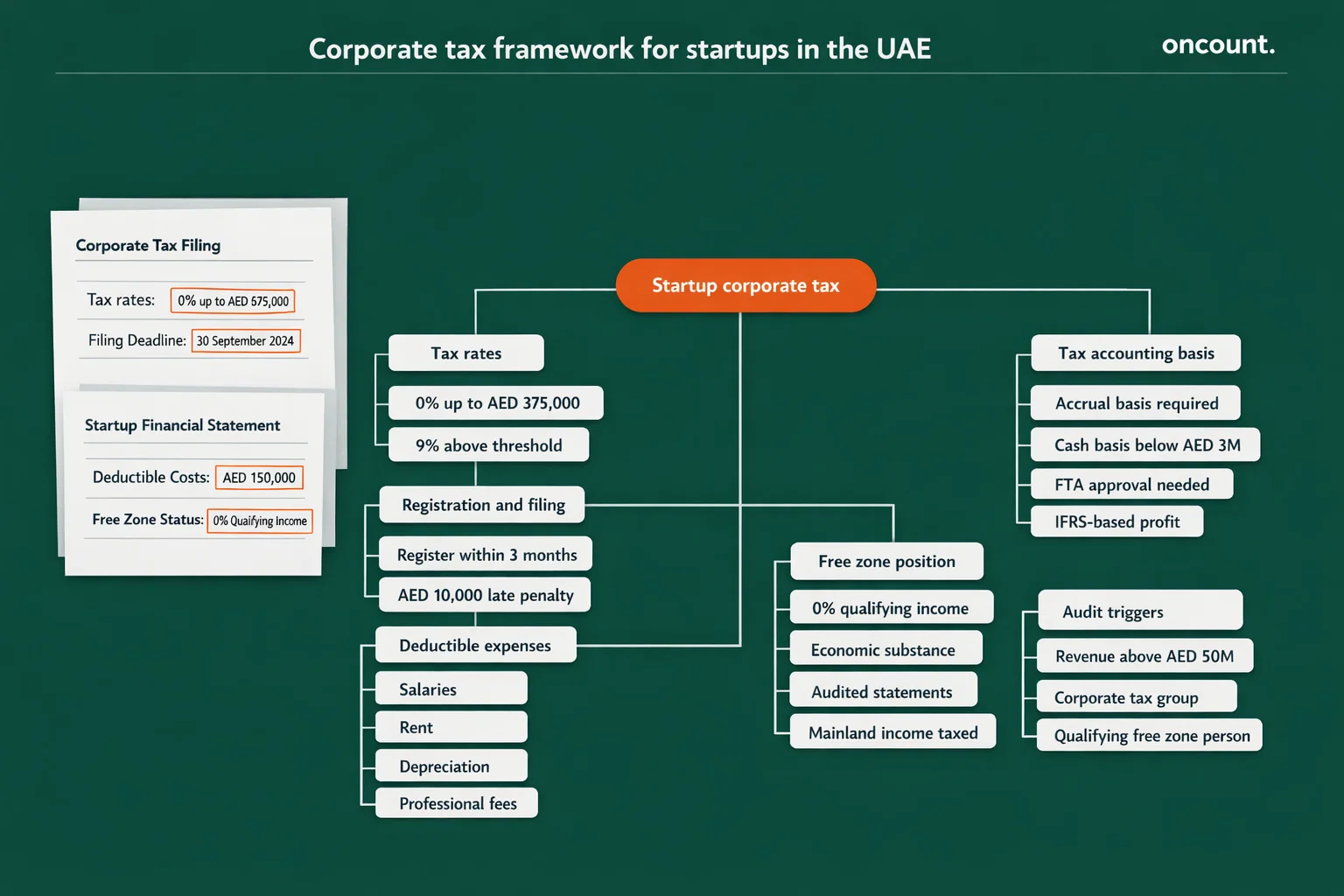

Corporate Tax Framework for Startups in the UAE

UAE Corporate Tax under Federal Decree-Law No. 47 of 2022 applies to all UAE-resident juridical persons and foreign entities with a UAE permanent establishment. The standard rate structure is:

- 0% on taxable profits up to AED 375,000

- 9% on taxable profits exceeding AED 375,000

- 0% on qualifying income earned by Qualifying Free Zone Persons, subject to substance requirements

Corporate tax registration is mandatory for all taxable persons. Newly incorporated companies must register with the Federal Tax Authority within three months of incorporation. Late registration incurs a fixed penalty of AED 10,000. As of March 2024, existing businesses were assigned staggered registration cohorts based on their trade license issuance date.

The corporate tax return is filed annually, within nine months of the fiscal year-end, alongside payment of any tax liability. Startups maintaining revenue below AED 3 million may request FTA approval to use cash-basis accounting; all others must use accrual-basis IFRS accounts as the foundation for taxable income calculation. Deductible expenses include salaries, rent, depreciation, and professional fees — provided they are incurred wholly for business purposes and supported by documentation.

Free zone entities are not automatically exempt. To benefit from the 0% qualifying income rate, a free zone entity must:

- Maintain adequate economic substance in the UAE

- Derive income exclusively from qualifying activities

- Not elect to be treated as a taxable mainland entity

- Submit audited financial statements confirming compliance

Accounting for Revenue and Expenses in Startup Operations

Revenue recognition for UAE startups must follow IFRS 15, which requires income to be recorded when performance obligations are satisfied — not simply when cash is received. A software-as-a-service startup, for example, recognizes subscription revenue ratably over the subscription period, regardless of whether the client pays annually in advance. This distinction has direct implications for VAT invoicing and corporate tax base calculations.

Common startup expense categories and accounting treatment:

- Salaries and benefits — expensed monthly; GOSI contributions for UAE nationals accrued as employer liability

- Office rent — capitalized under IFRS 16 if lease term exceeds 12 months; short-term leases may be expensed directly

- Depreciation — charged monthly on fixed assets using the straight-line method; rates must be consistently applied

- End-of-service gratuity — accrued monthly as a liability for expatriate employees; approximately 21 days’ salary per year of service under UAE Labor Law

- Prepaid expenses — recorded as assets and amortized over the benefit period

Startups receiving investor funding must distinguish between equity (recorded in share capital and share premium) and debt (recorded as a financial liability under IFRS 9). Mixing these classifications creates misstatements in the balance sheet and can affect tax deductibility of associated financing costs.

Regulatory Compliance and Reporting Obligations

Beyond VAT and corporate tax, UAE startups are subject to several additional compliance frameworks that directly affect accounting processes and documentation requirements.

Economic Substance Regulations (ESR): Cabinet Resolution No. 57 of 2020 requires UAE entities conducting relevant activities — including finance, leasing, intellectual property, and distribution — to demonstrate genuine economic substance within the UAE. ESR notifications and reports must be submitted annually. Non-compliance results in penalties starting at AED 50,000 for the first year.

Anti-Money Laundering (AML): Federal Decree-Law No. 20 of 2018 on Anti-Money Laundering imposes transaction monitoring, suspicious activity reporting, and customer due diligence obligations on designated non-financial businesses and professions (DNFBPs), which can include accountants and auditors serving UAE companies. Startups working with professional service providers should confirm those providers maintain AML-compliant procedures.

Ultimate Beneficial Owner (UBO) Reporting: Cabinet Decision No. 58 of 2020 requires all UAE mainland and free zone companies to maintain an internal register of ultimate beneficial owners and submit this information to their relevant licensing authority. UBO records must be updated within 15 days of any ownership change. Failure to maintain an accurate UBO register carries penalties of up to AED 100,000.

These compliance layers require startups to integrate regulatory reporting into their monthly and annual accounting workflows — not treat them as standalone administrative tasks.

Audit Requirements for Startups in the UAE

Audit obligations for UAE startups depend on entity type, revenue size, and jurisdictional registration:

| Entity Type | Audit Requirement | Triggering Condition |

| Mainland LLC | Mandatory if revenue > AED 50M | Ministerial Decision No. 84 of 2025 |

| Corporate Tax Group | Mandatory regardless of size | All group members must audit |

| Qualifying Free Zone Person | Mandatory | Required to maintain 0% tax status |

| DIFC / ADGM entity | Mandatory | Within 4 months of fiscal year-end |

| IFZA entity | Mandatory if turnover > AED 3M | Required at license renewal |

| Very small entity | Simplified statements permitted | Revenue < AED 3M, fewer than 10 staff |

Auditors engaged by UAE startups must be licensed by the relevant authority: mainland auditors require UAE Ministry of Economy registration, while DIFC and ADGM auditors must be approved by their respective regulators. The audit process validates whether financial statements present a true and fair view under IFRS, and auditors will test internal controls, verify transaction documentation, and confirm VAT and payroll records.

Startups preparing for their first audit should ensure all bank reconciliations, fixed asset schedules, payroll records, and VAT return workings are complete and traceable to source documents. Engaging accounting and bookkeeping outsourcing professionals with UAE audit preparation experience significantly reduces first-year audit risk.

Industry-Specific Accounting Considerations for Startup Companies

Revenue Recognition for Service and Technology Startups

SaaS, consulting, and subscription-based startups must apply IFRS 15’s five-step revenue recognition model. Deferred revenue — payments received in advance of service delivery — must be recorded as a liability and recognized progressively. A Dubai-based SaaS company billing clients quarterly in advance must split that receipt across three accounting periods.

Treatment of Intangible Assets and Intellectual Property

Startups investing in software development, brand creation, or patent registration must determine whether internally generated intangible assets meet the IAS 38 capitalization criteria. Development-phase costs that meet specific technical and commercial feasibility criteria may be capitalized; research-phase costs are expensed. Misclassifying these items inflates assets and understates expenses, directly distorting taxable income.

Emiratisation and Payroll Compliance for Startups

Mainland startups with between 20 and 49 employees in targeted sectors must employ at least one UAE national by the end of the relevant compliance year. The General Pension and Social Security Authority (GPSSA) requires employer contributions of approximately 12.5% and employee contributions of 5% on pensionable salary for UAE nationals. Expatriate staff receive end-of-service gratuity accrued at approximately 21 days’ basic salary per year — a recurring liability that must be reflected in the balance sheet.

Common Accounting Challenges for UAE Startup Companies

- Delayed VAT registration is among the most frequent compliance failures. Startups crossing the AED 375,000 taxable supply threshold without registering immediately face backdated VAT liability plus penalties. The Federal Tax Authority does not grant retrospective exemptions.

- Mixing personal and business transactions is a structural problem in early-stage companies where founders use personal accounts for business expenses. This practice invalidates input VAT claims and complicates corporate tax calculations, as personal expenditure is non-deductible.

- Improper IFRS 16 application causes understated liabilities in startups leasing office space. Failing to capitalize long-term lease obligations misrepresents the company’s financial position and may lead to audit qualifications.

- Gratuity under-accrual is a common error in startups that treat end-of-service benefits as a future cash outflow rather than a monthly accrual. When employees resign or are terminated, the liability can represent a significant unplanned cash drain.

- Inadequate documentation for related-party transactions attracts FTA scrutiny. Startups receiving loans or services from shareholders must document these transactions at arm’s length pricing and ensure proper disclosure in the financial statement notes.

Best Practices for Accounting and Financial Management

Implementing structured financial management from incorporation reduces the risk of regulatory penalties and supports investor confidence. The following practices reflect the standard recommended by UAE accounting professionals:

- Adopt cloud accounting software accredited by the FTA (Wafeq, QuickBooks Online, or Xero) to automate VAT return preparation and integrate with UAE banking systems

- Establish a monthly close process that includes bank reconciliation, accruals review, payroll confirmation, and VAT control account verification

- Engage qualified accounting professionals — whether in-house or through an outsourced bookkeeping firm — with demonstrated UAE regulatory expertise

- Maintain a compliance calendar tracking VAT filing deadlines, corporate tax registration, ESR notifications, and license renewals

- Conduct quarterly management account reviews comparing actual results against budget to identify variances before they escalate

- Segregate financial duties so that the person approving payments is not the same person preparing bank reconciliations — a basic internal control critical in small teams

- Plan for audit readiness by retaining all source documents, maintaining a fixed asset register, and reconciling all balance sheet accounts at year-end

Comparison: Free Zone vs Mainland Accounting Requirements

| Requirement | Mainland LLC | Free Zone Entity |

| Corporate tax rate | 9% above AED 375,000 | 0% on qualifying income (substance required) |

| Mandatory audit threshold | Revenue > AED 50M or tax group | Required for all qualifying free zone persons |

| IFRS compliance | Mandatory | Mandatory |

| VAT registration | Mandatory above AED 375,000 | Mandatory above AED 375,000 |

| Emiratisation | Applies (20+ staff) | Gradually aligning, primarily mainland rule |

| Local trading rights | Unrestricted | Through a distributor only (generally) |

| ESR obligations | Applicable for relevant activities | Applicable for relevant activities |

| UBO registration | Required | Required |

| Free zone authority reporting | Not applicable | Annual FS submission at renewal |

Free zone entities often carry a compliance perception advantage, but the audit and substance requirements under the current corporate tax framework mean that administrative obligations are substantially equivalent for most startups.