Key Takeaways

- UAE law mandates IFRS-compliant financial statements for all dental clinic entities, regardless of size or ownership structure.

- Most dental treatment services provided by DHA-licensed practitioners are VAT zero-rated under FTA guidance; cosmetic procedures are standard-rated at 5%.

- UAE Corporate Tax (Federal Decree-Law No. 47 of 2022) applies a 9% rate to taxable profits exceeding AED 375,000.

- Dental clinics in Dubai require both a DHA Health Facility License and a DED trade license, with audited financials required for renewal of both.

- Records must be retained for a minimum of five years (seven years for corporate tax purposes).

- End-of-service gratuity for expatriate staff is a balance sheet liability that must be accrued monthly.

- Mandatory health insurance for all employees is enforced in Dubai; non-compliance risks visa and license penalties.

- VAT returns are due quarterly, within 28 days of period-end, via the EmaraTax portal.

Overview of Accounting Requirements for Dental Clinics in the UAE

Under the UAE Commercial Companies Law and FTA regulations, all business entities — including dental clinics structured as professional companies or LLCs — are legally required to maintain complete, accurate financial records. The UAE does not operate a separate local GAAP; instead, International Financial Reporting Standards (IFRS) serve as the mandatory accounting framework for all companies registered in the country.

The Federal Tax Authority requires taxable entities to retain all accounting records, tax invoices, contracts, and supporting documentation for a minimum of five years from the end of the relevant tax period. For corporate tax purposes, the UAE Ministry of Finance specifies a seven-year retention period. Dental clinics that fail to meet these retention standards are subject to administrative penalties issued by the FTA.

Minimum record-keeping requirements for Dubai dental clinics include:

- General ledger and subsidiary ledgers

- Bank statements and reconciliation records

- Patient billing records and tax invoices

- Payroll registers and GOSI contribution receipts

- Purchase invoices for dental supplies and equipment

- Lease agreements and asset registers

- Insurance policy documents

Dubai Health Authority (DHA) and Dubai Economic Department (DED) both require submission of audited financial statements at the time of license renewal. Clinics that operate without current audited accounts risk license suspension.

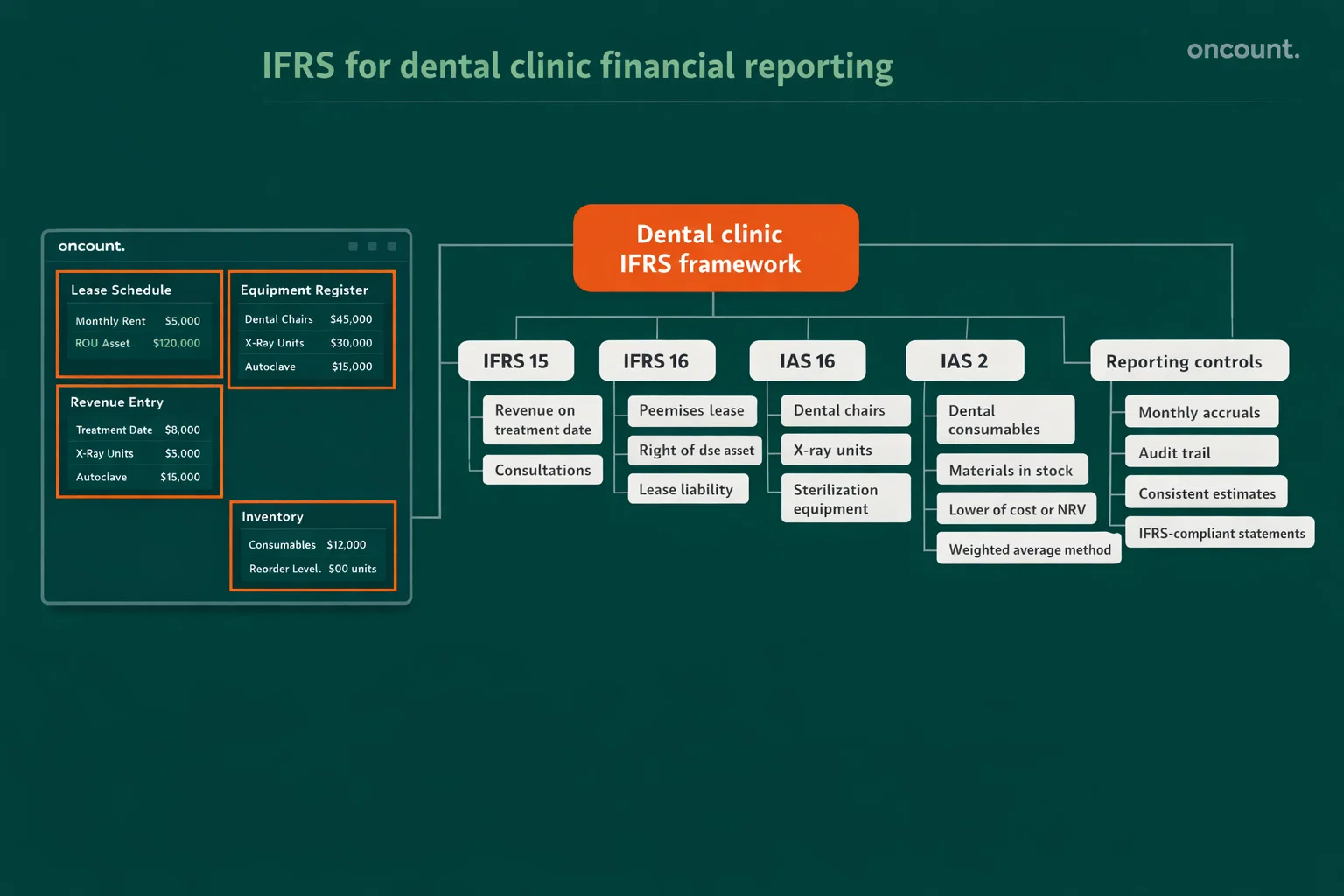

IFRS Application for Dental Clinic Financial Reporting

Dental clinics in Dubai apply IFRS across all material areas of financial reporting. The IFRS Foundation provides the technical framework that UAE-licensed auditors and accountants apply in practice.

Three standards are particularly relevant to clinic operations:

- IFRS 15 – Revenue from Contracts with Customers governs when and how dental service revenue is recognized. Each treatment — consultation, extraction, crown placement, orthodontic adjustment — constitutes a distinct performance obligation. Revenue is recognized at the point of treatment delivery, not upon invoice issuance or payment receipt. For insurance-billed services, revenue is recognized when the performance obligation is satisfied, with a receivable recorded until insurer payment is received.

- IFRS 16 – Leases requires dental clinics to capitalize most lease arrangements. A clinic leasing premises under a three-year agreement must record a right-of-use asset and a corresponding lease liability on its balance sheet. Short-term leases (under 12 months) and low-value leases (such as small diagnostic equipment) may be expensed directly to the income statement. This standard materially affects the balance sheet presentation of clinics that do not own their premises, which make up the majority of Dubai dental practices.

- IAS 16 – Property, Plant and Equipment applies to dental chairs, X-ray units, sterilization equipment, and clinic fit-out costs. These assets are capitalized at cost and depreciated over their estimated useful lives. In practice, dental chairs and major diagnostic equipment are typically depreciated over five to ten years using the straight-line method. Regular revaluation is not required but may be applied under the revaluation model with consistent policy application.

- IAS 2 – Inventories applies to dental consumables and materials held in stock. Inventories are valued at the lower of cost and net realizable value. Common methods include weighted average cost, which is practical for high-turnover consumable items.

Bookkeeping Framework and Financial Records Structure

A well-structured chart of accounts is the operational foundation of compliant dental clinic accounting. The chart should be designed to reflect the clinic’s revenue streams, cost structure, and reporting obligations under UAE corporate tax and VAT law.

| Account Category | Code Range | Example Accounts |

| Assets | 1000–1999 | Cash, Bank, Accounts Receivable, Inventory, Right-of-Use Assets, Equipment |

| Liabilities | 2000–2999 | Accounts Payable, GOSI Payable, VAT Payable, Lease Liabilities, Gratuity Provision |

| Equity | 3000–3999 | Paid-Up Capital, Retained Earnings, Owner’s Drawings |

| Revenue | 4000–4999 | Dental Service Income, Cosmetic Treatment Income, Product Sales, Other Income |

| Cost of Sales | 5000–5999 | Dental Consumables, Lab Fees, Prosthetic Materials |

| Operating Expenses | 6000–6999 | Salaries, Rent, Utilities, Depreciation, Insurance, Marketing |

| Other Expenses | 7000–7999 | Professional Fees, Training, Bank Charges, FX Losses |

Separating zero-rated dental service revenue from standard-rated cosmetic treatment income is not optional — it is an FTA compliance requirement that directly affects input VAT recovery calculations and VAT return accuracy.

Clinics should implement cloud-based accounting software (such as Zoho Books, QuickBooks Online, or Xero) with role-based access controls. All journal entries, adjustments, and write-offs must carry an audit trail that identifies the user, date, and authorization level. This supports both external audit requirements and FTA inspection readiness.

Financial Statements Preparation Requirements

Dental clinics in Dubai must prepare a complete set of IFRS-compliant financial statements at least annually. These statements form the basis for external audits, license renewals, corporate tax filings, and management decision-making.

Required financial statements:

- Statement of Financial Position (Balance Sheet) — reflects assets, liabilities, and equity as of year-end

- Statement of Comprehensive Income (P&L) — reports revenue, cost of sales, operating expenses, and net profit

- Statement of Cash Flows — details operating, investing, and financing cash movements

- Statement of Changes in Equity — tracks capital contributions, drawings, and retained earnings movements

- Notes to the Financial Statements — discloses accounting policies, significant estimates, and regulatory obligations

Monthly management accounts — abbreviated versions of the income statement and balance sheet — support ongoing performance monitoring. A dental clinic generating AED 2 million in annual revenue should maintain at a minimum a monthly P&L with budget-versus-actual variance analysis. According to the UAE Ministry of Finance Corporate Tax Guide (2023), businesses must maintain audited financial statements for accurate tax determination and compliance verification.

VAT Compliance for Dental Clinics in the UAE

VAT obligations for dental clinics are governed by Federal Decree-Law No. 8 of 2017 and FTA healthcare-specific guidance. The VAT treatment of dental services in the UAE is nuanced and requires careful classification at the service level.

VAT Registration Thresholds:

| Threshold Type | Annual Taxable Supply Value | Obligation |

| Mandatory Registration | Exceeds AED 375,000 | Must register immediately |

| Voluntary Registration | Exceeds AED 187,500 | May register; allows input VAT recovery |

| Below Threshold | Under AED 187,500 | No VAT registration required |

FTA guidance stipulates that preventive and curative dental services delivered by a DHA-licensed practitioner qualify as zero-rated supplies under Cabinet Decision No. 52 of 2017. This means no VAT is charged to the patient, but the clinic retains the right to recover input VAT on related purchases — a significant cash flow advantage.

VAT treatment by service type:

- Zero-rated (0%): Consultations, fillings, extractions, root canals, dental implants (medical necessity), prescription medications, and approved dental materials dispensed during treatment

- Standard-rated (5%): Cosmetic teeth whitening for aesthetic purposes, non-prescribed oral hygiene products sold at reception, purely cosmetic veneers not required for function

- Out of scope: Certain inter-company charges or educational activity fees

Dental clinics must issue FTA-compliant tax invoices for all standard-rated transactions, showing the clinic’s Tax Registration Number (TRN), a sequential invoice number, date, description, net amount, VAT rate, and VAT amount. Simplified tax invoices are permitted for B2C transactions under AED 10,000.

VAT returns are filed quarterly for most SMEs. The filing deadline is the 28th day following the end of each tax period. Late submissions incur a fixed penalty of AED 1,000 for the first offense, rising to AED 2,000 for subsequent late filings within 24 months. The UAE is also transitioning to mandatory e-invoicing, with phased implementation expected starting in mid-2026, requiring clinics to prepare their billing systems accordingly.

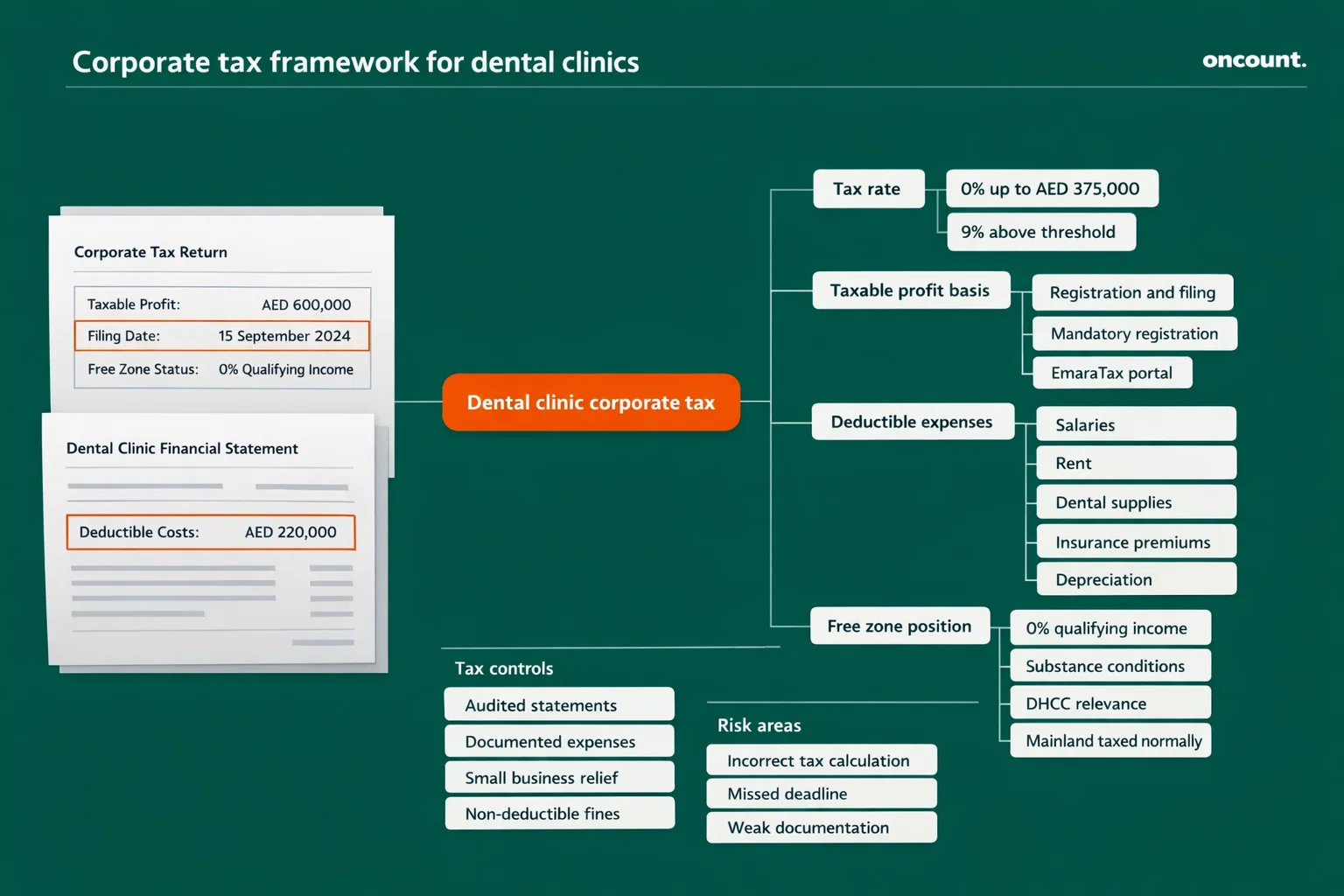

Corporate Tax Framework for Dental Clinics in the UAE

UAE Corporate Tax (Federal Decree-Law No. 47 of 2022) applies to financial years starting on or after June 1, 2023. A dental clinic structured as a Dubai mainland LLC with taxable profits of AED 600,000 would calculate its tax liability as follows: 0% on the first AED 375,000 and 9% on the remaining AED 225,000, resulting in a tax charge of AED 20,250.

Key corporate tax parameters for Dubai dental clinics:

| Parameter | Detail |

| Tax Rate | 0% up to AED 375,000; 9% above |

| Small Business Relief | Available for entities with revenue ≤ AED 3 million |

| Tax Period | Aligned with the financial year (typically the calendar year) |

| Filing Deadline | Within 9 months of the financial year-end |

| Registration | Mandatory via the EmaraTax portal |

| Deductible Expenses | Salaries, rent, supplies, depreciation, insurance premiums |

| Non-Deductible | Fines, personal expenses, and excessive interest above the safe harbor |

The UAE Ministry of Finance confirms that wages and mandatory employee benefits — including health insurance premiums and GOSI contributions for Emirati staff — are fully deductible under corporate tax rules, provided they are documented, commercially justified, and at arm’s length.

Dental clinics in free zones (such as Dubai Healthcare City) may qualify for 0% corporate tax on qualifying income, subject to substance requirements and compliance with the qualifying free zone person conditions. However, onshore mainland clinics do not have access to these concessions and are taxed at standard rates.

Accounting for Revenue and Expenses in Dental Clinic Operations

Revenue for a dental clinic flows from multiple streams, each with distinct recognition timing and VAT classification. Under IFRS 15, each patient treatment visit represents the completion of a distinct performance obligation. Revenue is recognized at the point of service delivery.

Primary revenue streams and accounting treatment:

- Fee-for-service (self-pay patients): Revenue recognized at treatment date; payment typically received on the same day.

- Insurance-billed services: Revenue recognized at treatment date; accounts receivable raised until insurer settles; an allowance for doubtful accounts (per IFRS 9) should be maintained based on historical collection rates

- Dental product sales: Revenue recognized at point of sale; COGS reflects purchase cost per IAS 2

- Treatment packages or prepayments: Revenue deferred and recognized as individual sessions are completed

Expense recognition follows the matching principle. Dental consumables used in treatment are expensed as cost of sales. Equipment is capitalized and depreciated. Monthly accruals should be posted for items such as end-of-service gratuity, audit fees, and insurance renewals to ensure accurate period-end reporting.

Regulatory Compliance and Reporting Obligations

Beyond taxation, Dubai dental clinics are subject to several cross-cutting compliance frameworks that affect accounting processes and documentation standards.

Economic Substance Regulations (ESR): Cabinet Resolution No. 57 of 2020 applies to UAE entities conducting specific “Relevant Activities.” Standard clinical dental practice is generally not a listed relevant activity; however, clinics with holding, financing, or IP arrangements should assess their ESR exposure annually.

Anti-Money Laundering (AML): Federal Decree-Law No. 20 of 2018 on AML applies to Designated Non-Financial Businesses and Professions (DNFBPs). Dental clinics processing high-value cash transactions should implement basic AML controls — customer identification for large payments, transaction monitoring, and suspicious transaction reporting to the UAE Financial Intelligence Unit (FIU) where applicable.

Ultimate Beneficial Owner (UBO) Requirements: Cabinet Decision No. 58 of 2020 requires all UAE mainland companies to maintain a UBO register identifying all natural persons holding 25% or more ownership or effective control. This register must be filed with the relevant emirate authority and updated within 15 days of any ownership change. Failure to maintain a current UBO register carries administrative penalties.

Audit Requirements for Dental Clinics in the UAE

External audits are mandatory for Dubai dental clinics operating under DED mainland licenses. The UAE Commercial Companies Law requires annually audited financial statements, and both DHA and DED enforce this requirement as a condition of license renewal.

Audit process overview for a dental clinic:

- Appoint a UAE-licensed external auditor (registered with the Ministry of Economy)

- Prepare year-end trial balance and supporting schedules

- Provide auditor access to all ledgers, invoices, bank statements, and contracts

- Address auditor queries on revenue recognition, IFRS 16 lease calculations, and gratuity provisions

- Receive signed audited financial statements

- Submit to DHA and DED as part of the annual license renewal package

Dubai Healthcare City (DHCC) free zone clinics are subject to DHCC Authority audit and reporting rules, which may differ slightly from mainland requirements but are no less stringent. All dental clinics, regardless of zone, should budget for annual audit fees as a recurring operating expense — typically ranging from AED 5,000 to AED 20,000 depending on clinic size and complexity.

Industry-Specific Accounting Considerations for Dental Clinics

DHA and DED Licensing Financial Requirements

The Dubai Health Authority requires applicants to demonstrate financial capacity during the licensing process. Specifically, applicants must submit recent bank statements confirming available funds and provide post-dated security cheques as an operational guarantee. DHA’s financial review considers projected capital needs; industry practice suggests maintaining AED 300,000–500,000 in accessible working capital.

Under the 2020 UAE Companies Law amendments, 100% foreign ownership of onshore dental practices is now permitted, removing the previous requirement for a UAE national shareholder.

Payroll, GOSI, and End-of-Service Accruals

Dental clinics employing UAE nationals must register with the General Pension and Social Security Authority (GPSSA). Employer GOSI contributions for Emirati employees are currently set at approximately 15% of basic salary, with a matching 11% employee contribution. Expatriate employees are not covered by GOSI; instead, clinics must accrue end-of-service gratuity under UAE Labour Law at 21 days’ basic salary per year for the first five years of service, rising to 30 days per year thereafter, capped at two years’ total salary.

This accrual must appear as a liability on the balance sheet. A clinic with five expatriate staff averaging AED 8,000 basic salary and two years of average tenure would carry an end-of-service liability of approximately AED 46,667 — a material figure that requires accurate monthly accrual accounting.

Mandatory Health Insurance Compliance

Dubai mandates health insurance coverage for all private-sector employees. As of 2025, employer-paid health insurance for expatriate staff is enforced, with visa applications and renewals linked to verified insurance status. Insurance premium costs are fully deductible for corporate tax purposes and should be accrued monthly rather than expensed as a lump sum at renewal.

Common Accounting Challenges for Dental Clinics in Dubai

| Challenge | Root Cause | Financial or Legal Consequence |

| VAT misclassification of cosmetic treatments | Failure to distinguish between medical and aesthetic services | FTA penalties, VAT underpayment, potential audit |

| Incomplete insurance receivables tracking | No AR aging process for insurer claims | Understated revenue, cash flow shortfalls |

| IFRS 16 non-compliance | Lease agreements not capitalized | Understated assets and liabilities; audit qualification |

| Gratuity provision omissions | Monthly accrual not posted | Understated liabilities; cash shock at staff departure |

| Late VAT filing | Manual processes, staff dependency | AED 1,000–2,000 per late filing |

| Missing UBO filings | Ownership changes not reported within 15 days | Administrative penalties per Cabinet Decision 58 |

| Weak COGS tracking | Supplies expensed without inventory reconciliation | Inaccurate gross margins; overstatement of profit |

A dental clinic that treats cosmetic teeth whitening as a zero-rated supply — rather than standard-rated — will underreport output VAT. The FTA can assess backdated VAT, interest, and penalties across the full five-year lookback period. The financial exposure on AED 500,000 of misclassified cosmetic revenue over three years at 5% VAT would be AED 25,000 in tax alone, before penalties.

Best Practices for Dental Clinics Accounting and Financial Management

Implementing structured financial controls from the clinic’s first operating month is significantly less costly than remediation following an FTA audit or license renewal rejection.

Recommended best practices:

- Use cloud accounting software with a chart of accounts configured to separate zero-rated and standard-rated revenues from day one

- Reconcile bank accounts weekly, not monthly — cash gaps compound quickly in high-transaction clinical environments

- Post monthly accruals for gratuity, audit fees, insurance, and depreciation without exception

- Track insurance receivables by payer and aging bucket — insurers in the UAE regularly dispute or delay claims

- Conduct a quarterly VAT review — verify that all new services are correctly classified before being added to the billing system

- Maintain a fixed asset register updated at every acquisition or disposal, with depreciation schedules reconciled to the ledger

- Engage a UAE-qualified accountant or accounting firm with healthcare sector experience for monthly bookkeeping and annual statutory work

- Brief all clinical and reception staff on invoice issuance requirements — an unsigned or incomplete invoice can invalidate a VAT claim

Comparison: Free Zone vs. Mainland Accounting Requirements for Dental Clinics

| Feature | Dubai Mainland (DED) | Free Zone (e.g., DHCC) |

| Regulator | DED + DHA | DHCC Authority + DHA |

| Corporate Tax Rate | 9% on profits >AED 375,000 | 0% on qualifying income (conditions apply) |

| Foreign Ownership | 100% permitted | 100% permitted |

| Audit Requirement | Mandatory annually | Mandatory (DHCC rules) |

| VAT Obligations | Standard FTA rules apply | Standard FTA rules apply |

| UBO Filing | Required | Required |

| ESR Applicability | Generally not applicable for clinical activity | Assess based on entity structure |

| License Renewal Financials | Audited accounts required | Audited accounts required |

| Patient Catchment | Unrestricted across the UAE | Primarily zone-based; some restrictions |

Dubai Healthcare City (DHCC) is the primary free zone for medical and dental clinics in Dubai. While the 0% corporate tax rate on qualifying income is an incentive, DHCC clinics must satisfy substance requirements and DHCC Authority compliance conditions. Mainland clinics offer greater geographic flexibility, unrestricted patient access, and simpler entity structures for most dental practitioners.