Key Takeaways

- All UAE manufacturing companies must maintain financial records under IFRS or IFRS for SMEs, depending on annual revenue thresholds.

- Federal corporate tax of 9% applies to taxable income above AED 375,000, with a 0% rate available to Qualifying Free Zone Persons (QFZPs) engaged in manufacturing activities.

- VAT at 5% applies to most domestic supplies; exports are zero-rated if supported by strict customs documentation.

- The Reverse Charge Mechanism (RCM) applies to imported machinery, raw materials, and, since February 2025, precious metals used in production.

- Audited financial statements are mandatory for mainland LLCs, all free zone entities seeking QFZP status, and any company with annual revenue exceeding AED 50 million.

- Economic Substance Regulations (ESR), Anti-Money Laundering (AML) obligations, and Ultimate Beneficial Owner (UBO) reporting apply to most manufacturing entities regardless of jurisdiction.

- Customs duty exemptions on production inputs are available to industrial license holders on the mainland and under certain free zone national industrial licenses.

Overview of Accounting Requirements in the UAE for Manufacturing Companies

The legal obligation for UAE manufacturing companies to maintain proper accounting records is established under Federal Law No. 2 of 2015 (UAE Commercial Companies Law), specifically Article 237, which mandates compliance with international accounting standards for both interim and annual financial statements. The UAE Ministry of Economy and the UAE Ministry of Finance jointly oversee this framework, ensuring that financial reporting supports transparency, investor confidence, and accurate tax assessment.

Manufacturing companies must retain all financial records, supporting documents, contracts, invoices, and production data for a minimum of five years. The Federal Tax Authority (FTA) reinforces this requirement under UAE VAT Law (Federal Decree-Law No. 8 of 2017), which independently mandates a five-year retention period for all tax-relevant documents.

The UAE Federal Tax Authority administers VAT and corporate tax registrations and conducts compliance audits. Manufacturing entities that fail to maintain adequate records face administrative penalties, tax reassessments, and potential loss of preferential tax status — including the 0% QFZP corporate tax rate.

IFRS Application for Manufacturing Companies

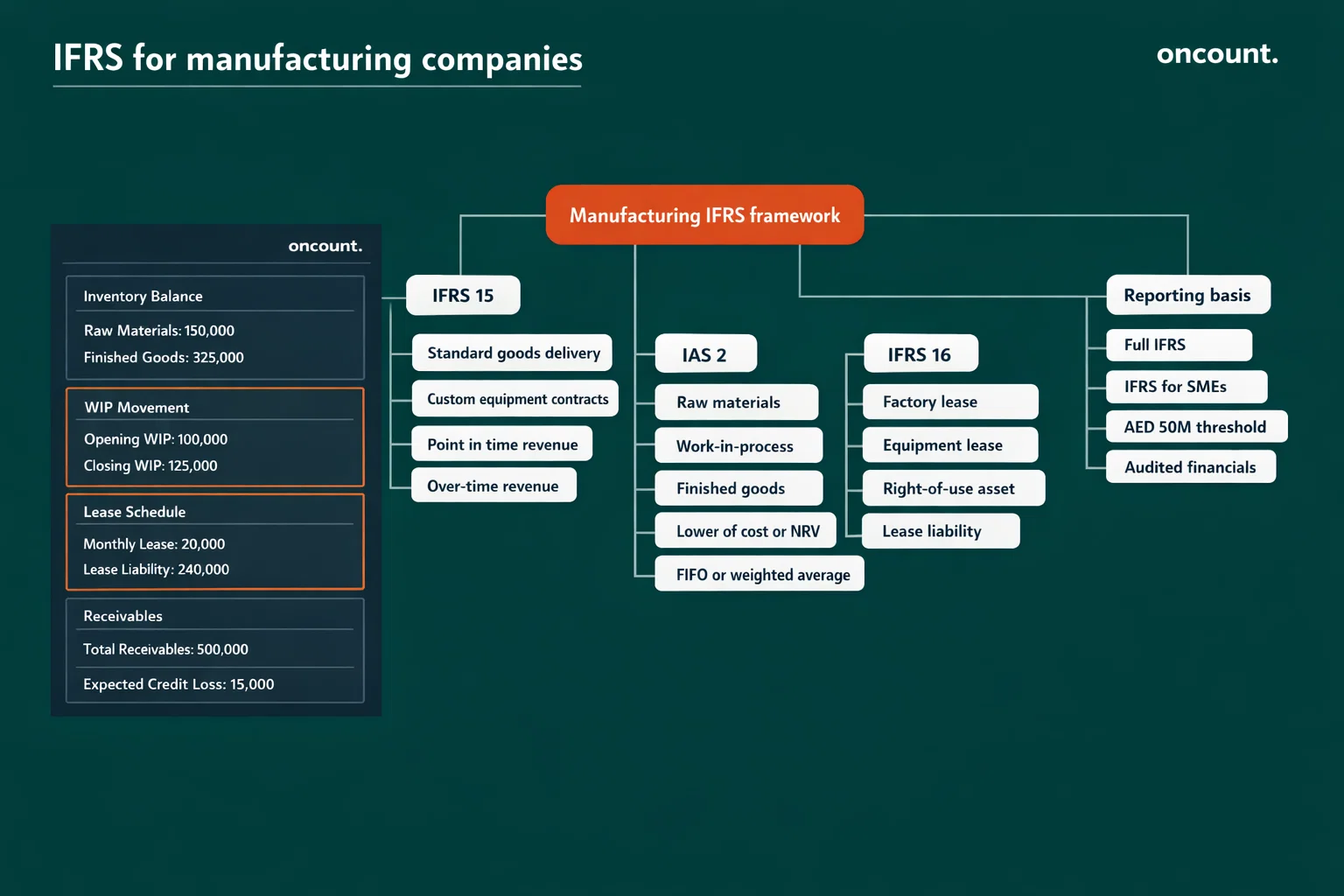

In the absence of a domestic GAAP framework, International Financial Reporting Standards (IFRS) serve as the mandatory accounting basis for all commercial entities in the UAE. Ministerial Decision No. 114 of 2023 clarifies that for UAE corporate tax purposes, only Full IFRS and IFRS for SMEs are recognized as acceptable accounting standards.

The selection between these two frameworks depends on the manufacturer’s annual revenue:

| Standard | Revenue Threshold | Key Characteristics |

| Full IFRS | Revenue > AED 50 million | Extensive disclosures; complex asset measurement; mandatory for listed entities |

| IFRS for SMEs | Revenue ≤ AED 50 million | Simplified measurement; reduced disclosure burden; streamlined presentation |

| AAOIFI Standards | N/A (Islamic transactions only) | Required for Sharia-compliant financing structures |

Several IFRS standards carry particular weight for manufacturing entities. IFRS 15 (Revenue from Contracts with Customers) governs when and how revenue is recognized — a critical issue for manufacturers of custom industrial equipment, where revenue may be recognized progressively over a construction period rather than at a single delivery point. IAS 2 (Inventories) dictates how raw materials, work-in-process, and finished goods are measured and written down. IFRS 16 (Leases) requires manufacturers leasing factory space or production equipment to capitalize right-of-use assets on the balance sheet, increasing both reported assets and liabilities.

IFRS 9 (Financial Instruments) applies where manufacturers extend credit to customers or hold financial assets, requiring expected credit loss provisions that impact reported profits. The practical application of these standards demands professional judgment and robust data systems — particularly in the UAE, where multi-currency procurement, cross-border sales, and diverse ownership structures are common.

Bookkeeping Framework and Financial Records Structure

A manufacturing company’s bookkeeping framework must reflect the complexity of its production environment. The chart of accounts should be structured to separately track raw material purchases, direct labor, fixed and variable production overheads, work-in-process movements, and finished goods transfers — each aligned with IAS 2 cost accumulation requirements.

The general ledger of a UAE manufacturer typically includes the following core modules:

- Raw materials inventory — tracking receipt, consumption, and closing balances by material category

- Work-in-process (WIP) — accumulating conversion costs as production progresses through defined stages

- Finished goods — recording completed units at cost until sale is recognized

- Cost of goods sold (COGS) — capturing the full production cost of units sold in each period

- VAT control accounts — separately recording output VAT, input VAT, RCM self-assessed VAT, and deferred input credits

Supporting documentation must include purchase orders, goods received notes, production orders, bills of materials, direct labor timesheets, overhead allocation schedules, customs entry declarations, and export clearance certificates. ERP systems that integrate shop-floor data with financial accounts substantially reduce the risk of IAS 2 misstatement and VAT filing errors.

Financial Statements Preparation Requirements

UAE manufacturing companies must prepare a complete set of financial statements at each reporting period. These include the balance sheet (statement of financial position), income statement (profit or loss), statement of changes in equity, cash flow statement, and notes to the financial statements.

For a manufacturer, the balance sheet typically carries inventory as the most significant asset, making accurate IAS 2 valuation central to fair presentation. The income statement must clearly present cost of goods sold separately from administrative and selling expenses, allowing meaningful gross margin analysis. The cash flow statement — particularly the operating section — reveals the working capital dynamics of the production cycle: how efficiently the company converts raw material purchases into collected cash.

Notes to the financial statements must disclose accounting policies for inventory valuation (FIFO or weighted average), revenue recognition under IFRS 15, depreciation methods for production machinery, and the basis of overhead allocation. For free zone entities claiming the 0% QFZP corporate tax rate, the notes must also disclose the entity’s tax status and the nature of qualifying income.

The UAE Ministry of Finance has issued detailed corporate tax guides confirming that businesses must base their tax filings on audited or reviewed financial statements that comply with IFRS.

VAT Compliance for Manufacturing Companies in the UAE

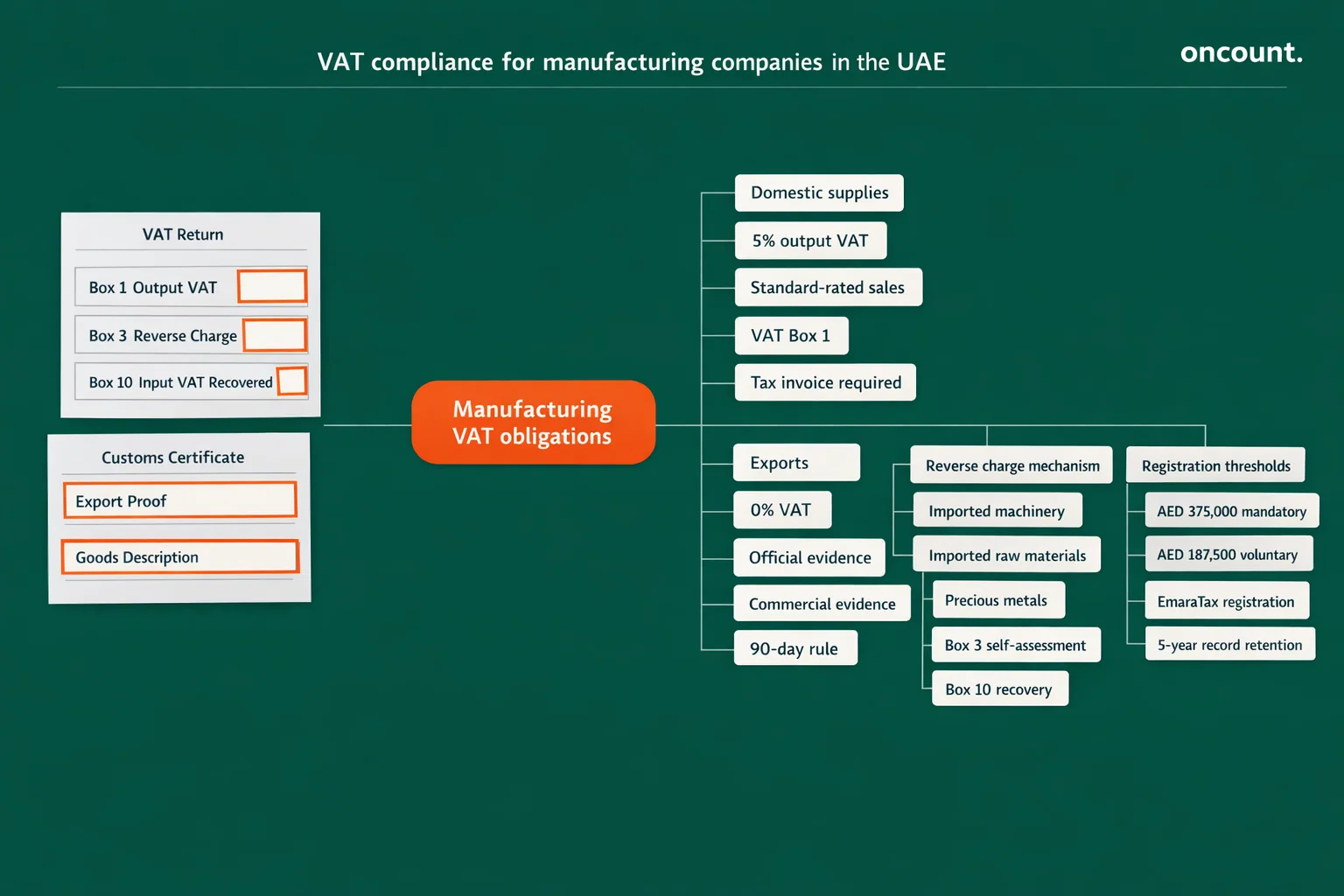

VAT at a standard rate of 5% was introduced under Federal Decree-Law No. 8 of 2017, effective January 1, 2018. Manufacturing companies whose taxable turnover exceeds AED 375,000 per annum must register for VAT with the Federal Tax Authority via the EmaraTax platform. Voluntary registration is permitted once turnover exceeds AED 187,500.

The VAT treatment of manufacturing operations involves several distinct mechanisms:

| VAT Return Box | Transaction Type | Manufacturer’s Obligation |

| Box 1 | Standard-rated domestic supplies | Charge 5% output VAT and report |

| Box 3 | Imports and supplies are subject to RCM | Self-assess 5% output VAT |

| Box 6 | Goods moved from the Designated Zone to the mainland | Account for import VAT on entry |

| Box 10 | Recoverable input VAT | Claim against all taxable business expenses |

Reverse Charge Mechanism (RCM): When a manufacturer imports specialized machinery or raw materials from a supplier not registered for UAE VAT, the obligation to account for that VAT shifts to the manufacturer. The FTA requires the manufacturer to report 5% output VAT in Box 3 of VAT return Form 201 and simultaneously recover the same amount in Box 10, assuming the goods are used exclusively for taxable activities. Domestic RCM was extended on October 30, 2023, to cover electronic devices and components traded between VAT-registered entities for manufacturing or resale. Since February 26, 2025, the FTA expanded domestic RCM to include precious metals — gold, silver, and platinum — when purchased for use in industrial production. Manufacturers acquiring these materials must provide their supplier with a formal declaration confirming VAT registration status and intended manufacturing use.

Export zero-rating allows manufacturers to apply a 0% VAT rate to goods exported outside the UAE while retaining the right to recover all input VAT on associated production costs. To qualify, Article 30 of the VAT Executive Regulations requires retention of both official evidence (FTA exit certificate or emirate customs clearance certificate) and commercial evidence (airway bill, bill of lading, or land manifest) confirming that the goods left the UAE within 90 days of supply. Failure to retain this documentation during an FTA audit results in reclassification of the export as a standard-rated supply, triggering a 5% liability plus administrative penalties.

FTA Public Clarification VATP031 further stipulates that input tax recovery requires not only a valid tax invoice but also a documented intention to make payment within six months of the agreed payment date. Manufacturing finance teams must ensure accounts payable workflows are integrated with VAT reporting to avoid inadvertent input tax reversals.

Corporate Tax Framework for Manufacturing Companies in the UAE

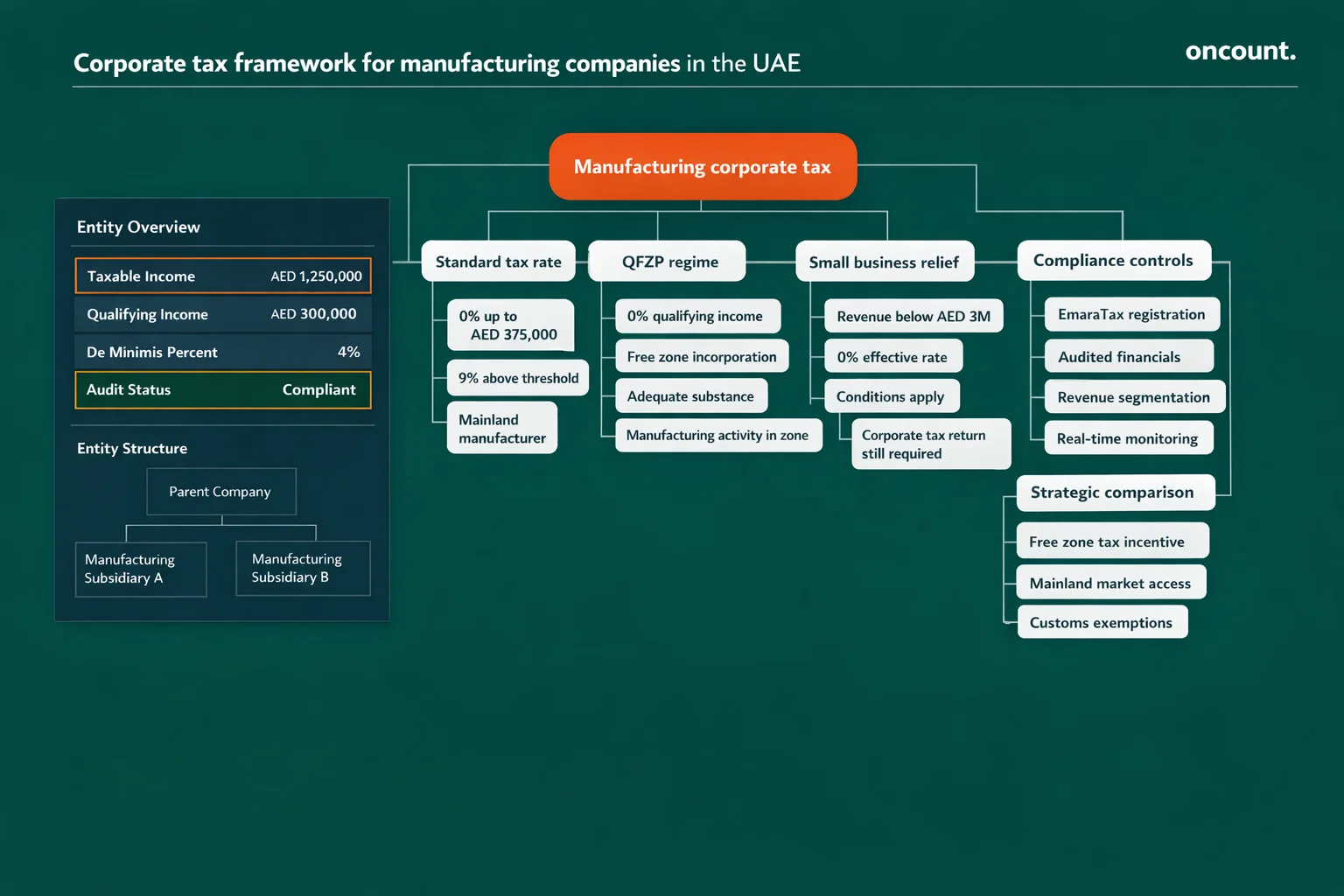

The UAE introduced federal corporate tax under Federal Decree-Law No. 47 of 2022, effective for financial years beginning on or after June 1, 2023. The UAE Federal Tax Authority administers corporate tax registration and compliance through the EmaraTax portal.

The tax rate structure is as follows:

| Taxable Income Band | Applicable Rate |

| Up to AED 375,000 | 0% |

| Above AED 375,000 | 9% |

| Qualifying Free Zone income (QFZP) | 0% |

| Small Business Relief (revenue < AED 3 million, conditions apply) | 0% effective rate |

Qualifying Free Zone Person (QFZP) regime: A manufacturing entity registered in a UAE free zone can access the 0% corporate tax rate on qualifying income if it satisfies the following concurrent conditions: it is a juridical person incorporated in a recognized free zone; it maintains adequate substance within that zone (physical presence, qualified employees, sufficient operating expenditure); and its core income-generating activity — the actual fabrication or processing of goods — occurs within the zone’s boundaries.

For manufacturing companies, revenue derived from the “manufacturing and processing of goods or materials” is an explicitly designated Qualifying Activity. This covers sales to other free zone persons and, critically, sales to mainland or international customers where the transaction relates to the qualifying manufacturing activity.

The de minimis rule permits a QFZP to earn non-qualifying income not exceeding the lower of 5% of total revenue or AED 5 million in any tax year without losing its exempt status. Breaching this threshold results in the entity losing QFZP status for the current year and the subsequent four tax years — the “tainting” effect. A manufacturer selling finished goods directly to UAE consumers (B2C transactions, classified as excluded activities) must monitor this revenue stream in real time to prevent unintended tainting.

Mainland manufacturing companies do not face substance tests but pay 9% on taxable income above AED 375,000. In return, they enjoy unrestricted GCC market access and may qualify for industrial license-based customs exemptions not generally available to free zone entities.

Accounting for Revenue and Expenses in Manufacturing

Revenue recognition for manufacturing companies follows the IFRS 15 five-step model: identify the contract, identify performance obligations, determine the transaction price, allocate that price to obligations, and recognize revenue when each obligation is satisfied.

For manufacturers of standard goods delivered at a single point, revenue is recognized upon transfer of control to the customer — typically at delivery. For manufacturers of bespoke industrial equipment under long-term contracts, revenue may be recognized over time if the customer controls the asset as it is created and the manufacturer has an enforceable right to payment for work completed to date.

Expense recognition in a manufacturing context is governed by IAS 2 for product costs and IAS 16 (Property, Plant and Equipment) for capital expenditure. A common misclassification in UAE manufacturing companies is the expensing of production machinery modifications that meet the IAS 16 criteria for capitalization — particularly relevant when upgrading production lines under the UAE’s Operation 300bn industrial expansion program.

Fixed production overhead allocation represents one of the most audited areas in UAE manufacturing accounts. IAS 2 requires that fixed overheads — factory rent, depreciation of production equipment, supervisory salaries — be allocated to inventory based on normal production capacity. During periods of low output or planned shutdowns, unabsorbed fixed overheads must be expensed immediately and may not be deferred into inventory values. This prevents balance sheet inflation and ensures that reported profit reflects actual production efficiency.

Regulatory Compliance and Reporting Obligations

Beyond tax, UAE manufacturing companies are subject to several regulatory frameworks that directly affect accounting processes and documentation requirements.

Economic Substance Regulations (ESR): Cabinet Resolution No. 57 of 2020 requires entities conducting relevant activities — which may include certain manufacturing-adjacent functions such as holding company activities or intellectual property income — to demonstrate adequate economic substance in the UAE. Entities subject to ESR must file annual notifications and, where required, substance reports with the UAE Ministry of Finance. Manufacturing companies that operate in free zones and earn royalties or IP income should assess their ESR obligations carefully, as non-compliance carries penalties of AED 50,000 for first-year breaches, rising to AED 400,000 for repeat failures.

Anti-Money Laundering (AML): Designated Non-Financial Businesses and Professions (DNFBPs) in the UAE — including dealers in precious metals and stones — are subject to Federal Decree-Law No. 20 of 2019 on AML. Manufacturing companies that process gold, silver, or platinum as production inputs must implement customer due diligence procedures, maintain transaction records, and file Suspicious Transaction Reports with the UAE Financial Intelligence Unit where required.

Ultimate Beneficial Owner (UBO) Reporting: Cabinet Decision No. 58 of 2020 requires all UAE companies to maintain and submit accurate UBO registers to the relevant licensing authority. Manufacturing entities — mainland and free zone — must record all natural persons holding 25% or more of shares or exercising effective control, update registers within 15 days of any change, and submit annual confirmations. Failure to comply carries fines of up to AED 100,000.

Audit Requirements for Manufacturing Companies in the UAE

Statutory audits are mandatory for the majority of UAE manufacturing entities. All mainland limited liability companies and joint stock companies must have annual financial statements audited by a UAE Ministry of Economy-approved audit firm. Under UAE Corporate Tax Law, any entity generating annual revenue exceeding AED 50 million must maintain audited financials for tax filing purposes. Free zone entities claiming QFZP status — and the 0% corporate tax rate — must be audited regardless of revenue level.

Submission deadlines vary by jurisdiction:

| Jurisdiction | Audit Requirement | Submission Deadline |

| Mainland UAE | Mandatory for LLCs and corporations | Within 6 months of the financial year-end |

| JAFZA (Dubai) | Mandatory for all entities | Within 180 days of the year-end |

| DMCC (Dubai) | Mandatory for all entities | Within 90 days of the year-end |

| KIZAD (Abu Dhabi) | Mandatory for all entities | Within 6 months of the year-end |

| DIFC (Dubai) | Mandatory for all entities | Within 4 months of the year-end |

| ADGM (Abu Dhabi) | Mandatory (exempt if < $13.5M revenue and < 35 staff) | Within 9 months of the year-end |

Failure to file audited accounts on time results in penalties ranging from AED 50,000 for mainland entities to monthly fines and trade license non-renewal in most free zones. Audit firms must be licensed by the UAE Ministry of Economy or the relevant free zone authority. Auditor rotation is required every six years, with a mandatory three-year cooling-off period, and the lead audit partner must typically rotate every three years.

Industry-Specific Accounting Considerations for Manufacturing

Inventory Costing and IAS 2 Compliance

IAS 2 mandates that inventories be stated at the lower of cost and Net Realizable Value (NRV). For UAE manufacturers, the cost of inventory encompasses the purchase price of raw materials (including import duties and non-refundable taxes), direct conversion costs (labor and allocated production overheads), and any other costs incurred in bringing inventory to its present location and condition. LIFO (Last-In, First-Out) is strictly prohibited under IAS 2 — manufacturers must use either FIFO (First-In, First-Out) or the Weighted Average Cost method, applied consistently across reporting periods.

NRV write-downs are required where the estimated selling price of finished goods, less estimated costs of completion and selling expenses, falls below the accumulated cost. For manufacturers exposed to commodity price volatility — such as aluminum fabricators or chemical processors in the UAE’s industrial zones — NRV testing at each reporting date is a material compliance obligation, not a formality.

Cost Accounting Methodologies

Beyond statutory IFRS compliance, UAE manufacturers deploy specialized cost accounting systems to support pricing, margin management, and operational efficiency:

| Costing Method | Best Application | Primary Benefit |

| Standard Costing | Repetitive, high-volume production | Variance analysis identifies material and labor inefficiencies |

| Activity-Based Costing (ABC) | Diverse product lines with high overhead | Reveals true profitability by product and customer |

| Job Order Costing | Custom and made-to-order manufacturing | Precise cost tracking per project or production order |

| Process Costing | Continuous homogeneous production (chemicals, food) | Simplified average cost per unit across production runs |

Customs Duty Exemptions for Industrial Inputs

Mainland manufacturers holding a valid industrial license may apply for exemptions from the standard 5% GCC customs duty on imports of production machinery, equipment, spare parts, raw materials, semi-finished goods, and packaging materials directly related to their licensed manufacturing activity. These exemptions require regular reporting to the relevant emirate’s industrial authority on manufacturing processes and local value addition.

To export goods duty-free to GCC and GAFTA (Greater Arab Free Trade Area) member states, manufacturers must satisfy the rules of origin: at minimum 51% UAE or GCC national ownership of the manufacturing entity and at least 40% local value addition within the UAE. Free zone manufacturers are generally treated as foreign entities for GCC export purposes unless they hold a national industrial license under specific zone frameworks such as JAFZA.

Common Accounting Challenges for Manufacturing Companies

Overhead absorption errors represent one of the most frequent audit findings in UAE manufacturing accounts. Allocating fixed overheads at actual rather than normal capacity artificially inflates inventory values during high-production periods and understates them during downturns — both misrepresentations under IAS 2.

QFZP de minimis breaches are a growing compliance risk as free zone manufacturers expand their mainland customer base. Real-time monitoring of non-qualifying revenue against the 5% threshold is essential; a single unmonitored quarter of direct B2C sales can trigger five years of 9% taxation on the entire entity.

Export VAT documentation failures are a common FTA audit finding. Manufacturers often assume that customs system entries constitute sufficient evidence, while the FTA requires both official and commercial documentation to be retained within the 90-day window. Late discovery of missing airway bills or clearance certificates can convert a zero-rated transaction into a 5% standard-rated liability.

Misapplication of RCM on imported inputs — either failing to self-assess output VAT or failing to claim the corresponding input credit in the same return period — results in penalties and distorted VAT return positions.

Best Practices for Accounting and Financial Management

Manufacturing companies operating in the UAE can substantially reduce compliance risk and improve financial performance by adopting the following practices:

- Implement an integrated ERP system that connects production, procurement, inventory, and finance modules — enabling real-time IAS 2 cost tracking, automated VAT RCM entries, and 90-day export window monitoring.

- Conduct monthly inventory reviews against NRV benchmarks, particularly for manufacturers exposed to international commodity price movements or foreign exchange fluctuations affecting input costs.

- Establish a dedicated tax calendar covering corporate tax registration, VAT 201 return deadlines, ESR notification filing, UBO annual confirmations, and audit submission deadlines by jurisdiction.

- Maintain granular revenue segmentation between qualifying and non-qualifying income streams in real time, with automated alerts when non-qualifying revenue approaches the QFZP de minimis threshold.

- Engage UAE Ministry of Economy-licensed auditors well in advance of each jurisdiction’s submission deadline — particularly for DMCC entities subject to the 90-day deadline.

- Train accounts payable teams on VATP031 payment intention requirements to prevent inadvertent input tax deferrals.

Comparison: Free Zone vs Mainland Accounting Requirements for Manufacturers

| Criteria | Free Zone (QFZP) | Mainland |

| Corporate Tax Rate | 0% on qualifying manufacturing income | 9% above AED 375,000 |

| Substance Requirements | Mandatory (physical presence, staff, expenditure in zone) | Not required |

| GCC Export Duty-Free Access | Limited (requires national industrial license) | Available with rules of origin compliance |

| Customs Duty on Imports | Generally duty-free within zone | Exemptions available under industrial license |

| Audit Requirement | Mandatory regardless of revenue | Mandatory for LLCs; revenue > AED 50M for tax |

| Revenue Monitoring | De minimis rule (5% / AED 5M non-qualifying cap) | No equivalent restriction |

| VAT Registration | Mandatory above AED 375,000 turnover | Mandatory above AED 375,000 turnover |

| Mainland Market Access | Restricted (requires a separate mainland entity for some activities) | Unrestricted |