Key Takeaways

- VAT registration is mandatory for fitness centers exceeding AED 375,000 in annual taxable supplies

- Annual membership revenue must be deferred under IFRS 15 and recognized monthly as facility access is provided

- IFRS 16 requires gym lease obligations to be recorded as right-of-use assets and lease liabilities on the balance sheet

- UAE Corporate Tax at 9% applies to taxable profits above AED 375,000; Small Business Relief applies to entities below AED 3 million in revenue

- End-of-service gratuity must be accrued monthly under IAS 19 to prevent balance sheet liquidity risk

- Statutory audits are mandatory for free zone entities and mainland businesses with revenue exceeding AED 50 million

- WPS compliance is enforced monthly by MOHRE; salary discrepancies can trigger trade license blockages

Overview of Accounting Requirements in the UAE for Fitness Centers

UAE Commercial Companies Law requires all businesses — including gyms and fitness studios — to maintain accurate financial records aligned with International Financial Reporting Standards. The Federal Tax Authority mandates that all tax-related documentation, including VAT invoices, membership contracts, and payroll records, be retained for a minimum of seven years.

Mainland fitness centers are subject to the full scope of federal commercial law, while free zone entities face additional obligations tied to their respective authority’s licensing framework. Both jurisdictions require IFRS-compliant financial statements and timely registration with the FTA’s EmaraTax portal.

The UAE Ministry of Finance requires that financial records reflect the economic substance of transactions rather than their legal form. This principle applies directly to deferred membership revenue, lease obligations, and employee gratuity accruals — areas where fitness centers frequently receive adverse audit findings due to cash-basis bookkeeping practices that fail to meet IFRS requirements.

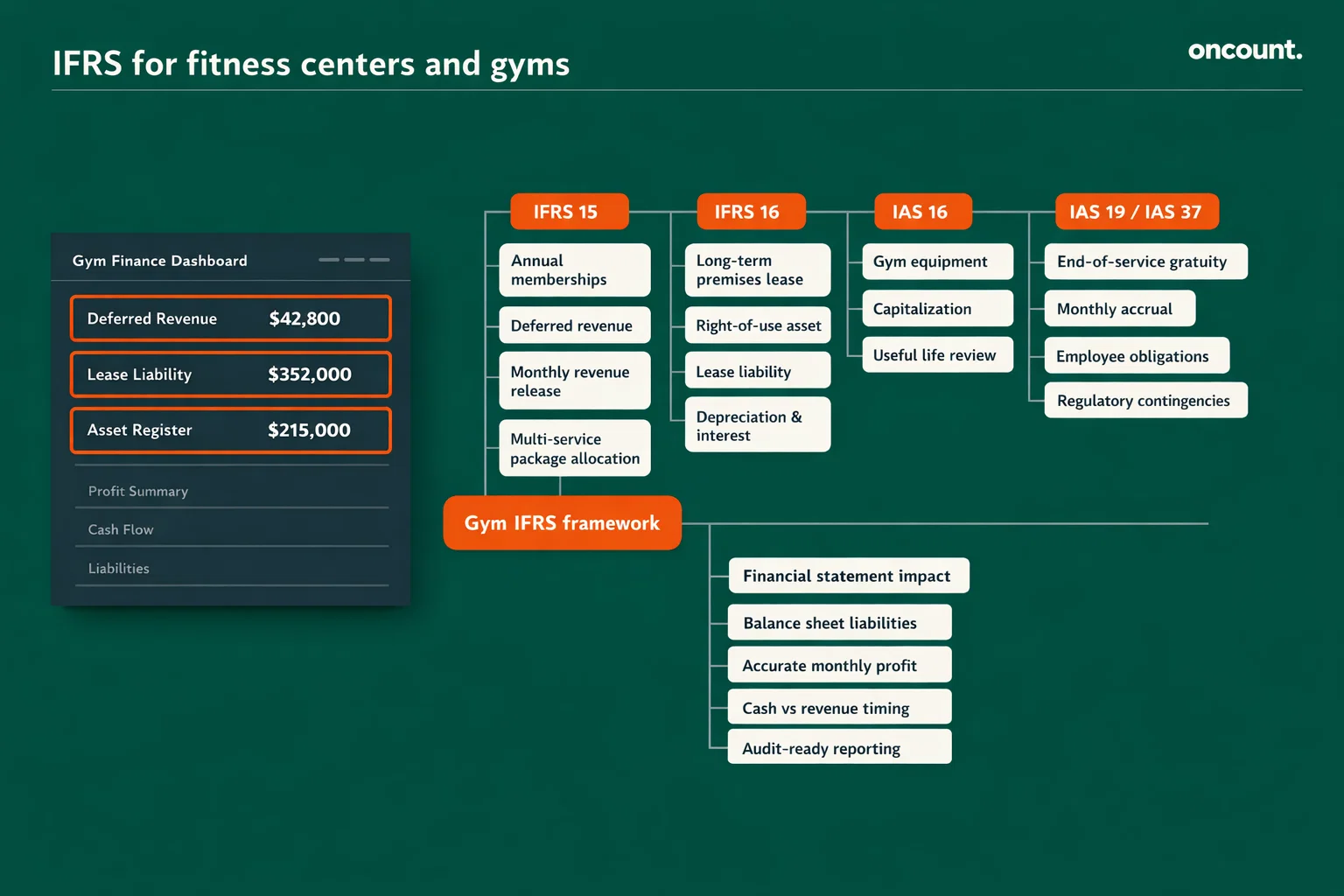

IFRS Application for Fitness Center and Gym Companies

IFRS 15 — Revenue from Contracts with Customers governs membership revenue recognition. When a member pays AED 4,800 for a 12-month membership, the gym records the full amount as deferred revenue — a balance sheet liability — and recognizes AED 400 per month as each month of facility access is delivered. Recognizing the full payment on the date of receipt is a material accounting error under IFRS 15.

IFRS 16 — Leases transforms how gym premises costs are reported. A five-year lease with annual payments of AED 600,000 generates a right-of-use (ROU) asset and a lease liability measured at the present value of future payments, discounted at the gym’s incremental borrowing rate. The gym subsequently records depreciation on the ROU asset and interest expense on the declining lease liability — replacing the single rent line item that existed under the previous lease standard.

IAS 16 — Property, Plant and Equipment governs gym equipment capitalization. The UAE’s sustained ambient temperatures and humidity levels accelerate motor degradation in cardio equipment, often shortening standard useful life estimates by 20–30% compared to international benchmarks. Finance teams must integrate usage-hour data from gym management platforms to assess whether depreciation rates remain appropriate on an annual basis.

Key IFRS standards applicable to UAE gym operations:

- IFRS 15: Membership revenue deferral and multi-element package revenue allocation

- IFRS 16: Balance sheet recognition of gym premises leases and equipment financing

- IAS 16: Fixed asset capitalization, depreciation, and useful life assessment

- IAS 19: Employee benefit obligations, including end-of-service gratuity provisioning

- IAS 37: Contingent liabilities arising from regulatory fines or license penalties

Bookkeeping Framework and Financial Records Structure for Gyms

A gym’s chart of accounts must reflect its operational complexity. Revenue streams, cost categories, and liability accounts require precise structuring to support both management reporting and FTA compliance reviews. Engaging experienced accounting and bookkeeping firms in UAE with sector-specific knowledge ensures that account classifications align with IFRS disclosure standards and FTA audit expectations.

Core components of a fitness center’s bookkeeping framework:

- Revenue accounts: Deferred membership fees, recognized membership income, personal training revenue, group class income, retail product sales, joining and initiation fees

- Cost of sales: Trainer commissions, group instructor fees, equipment servicing, fitness consumables

- Operating expenses: Lease depreciation and interest (post-IFRS 16), utilities, marketing, cleaning services, insurance

- Balance sheet items: Right-of-use assets, lease liabilities, deferred revenue, employee benefit provisions, prepaid expenses

- Tax accounts: VAT output, VAT input, VAT payable, corporate tax provision

Supporting documentation required by the FTA includes signed membership agreements, personal training session completion records, POS transaction receipts, supplier tax invoices, bank statements, and monthly payroll reports. All documents must remain available for inspection for seven years from the transaction date.

Financial Statements Preparation Requirements

UAE fitness centers must prepare annual financial statements comprising the statement of financial position, income statement, statement of cash flows, statement of changes in equity, and accompanying notes. Financial statements must be prepared under IFRS and, in the case of free zone entities, submitted to the relevant authority as part of the annual license renewal process.

| Statement | Regulatory Purpose | Key Gym-Specific Items |

| Balance Sheet | FTA audit, banking, investor reporting | Deferred revenue, ROU assets, lease liabilities |

| Income Statement | Corporate Tax calculation, performance review | Membership revenue by stream, depreciation, interest |

| Cash Flow Statement | Liquidity assessment, loan covenants | Operating vs. financing classification post-IFRS 16 |

| Notes to Financials | IFRS disclosure requirements | Lease terms, gratuity assumptions, VAT reconciliation |

The cash flow statement requires particular attention under IFRS 16. Lease repayments are classified as financing outflows rather than operating expenses, which makes operating cash flow appear stronger than the underlying business may warrant. UAE lenders and investors routinely request pre-IFRS 16 adjusted figures to assess a gym’s true cash-generation capacity.

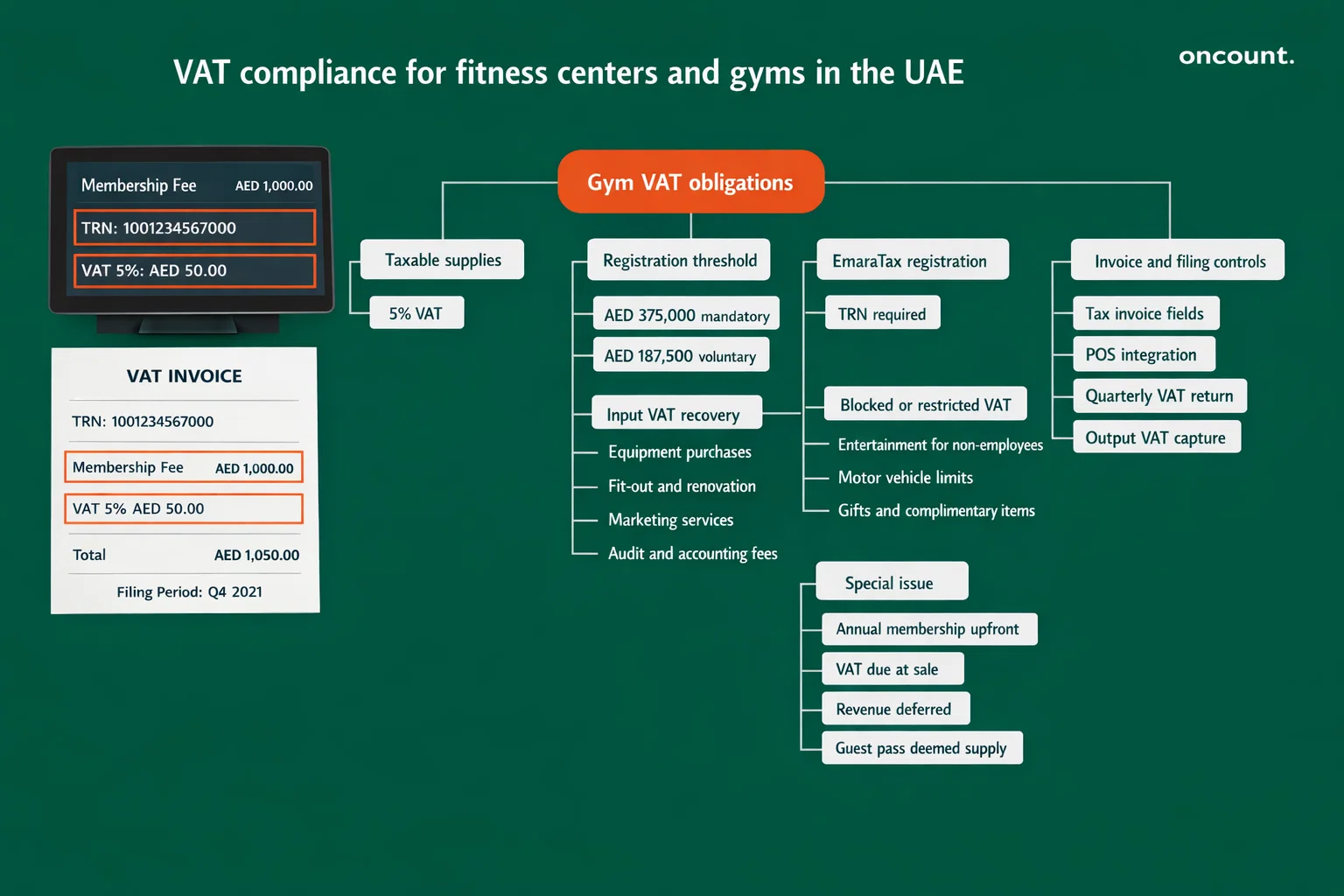

VAT Compliance for Fitness Centers and Gyms in the UAE

Under Federal Decree-Law No. 8 of 2017, UAE gyms must register for VAT with the Federal Tax Authority when taxable supplies exceed AED 375,000 within any trailing 12-month period. Voluntary registration is available at the AED 187,500 threshold and is advisable for new operators seeking to recover input VAT on substantial startup costs, including equipment and fit-out. The FTA’s EmaraTax portal processes TRN applications with a standard turnaround of approximately 20 business days.

VAT at 5% applies to membership fees, personal training packages, group fitness classes, and retail sales. Tax invoices must include the gym’s Tax Registration Number, the date of supply, a service description, and the VAT amount stated separately — as required under FTA guidance on tax invoice compliance.

Input VAT is recoverable on:

- Equipment purchases and leasing arrangements

- Facility renovation and fit-out expenditure

- Marketing and advertising services

- Cleaning and sanitation supplies

- Professional services, including accounting and audit fees

Input VAT is not recoverable on:

- Entertainment expenses provided to non-employees

- Motor vehicle expenses (with limited exceptions)

- Gifts or complimentary supplies to members not forming part of a taxable supply

| VAT Scenario | Treatment | Example |

| Monthly Membership Fee | Taxable at 5% | AED 500 + AED 25 VAT |

| Annual Membership (Upfront) | Taxable at 5%; revenue deferred | AED 5,250 total; AED 250 output VAT |

| Joining Fee (Administrative) | Taxable at 5%; amortized over membership life | AED 210 total; AED 10 VAT |

| Retail Supplement Sale | Taxable at 5% | AED 52.50; AED 2.50 VAT |

| Complimentary Guest Pass | Potential deemed supply; output VAT may apply | Self-assessment required |

Given the volume of daily transactions across POS terminals, membership renewals, and PT bookings, direct integration between gym management software and the accounting ledger is essential to ensure every dirham of output VAT is captured without reliance on manual reconciliation.

Corporate Tax Framework for Fitness Centers in the UAE

UAE Corporate Tax, established under Federal Decree-Law No. 47 of 2022, applies a 9% rate to taxable profits exceeding AED 375,000 per financial year for UAE-resident businesses. A Dubai fitness center generating AED 2.5 million in revenue with AED 1.8 million in allowable deductions reports taxable income of AED 700,000, resulting in a Corporate Tax liability of AED 29,250 — calculated as 9% of AED 325,000, the amount above the AED 375,000 threshold.

Small Business Relief (SBR), available under Ministerial Decision No. 73 of 2023, allows fitness centers with revenue at or below AED 3 million to elect for zero taxable income. According to UAE Ministry of Finance guidance, SBR remains available for tax periods ending on or before December 31, 2026. Electing SBR, however, prevents the carry-forward of tax losses generated during the relief period — a material consideration for gyms investing heavily in start-up infrastructure.

| Feature | Small Business Relief | Standard Corporate Tax |

| Revenue Threshold | ≤ AED 3 Million | > AED 3 Million |

| Tax Rate | 0% (deemed zero taxable income) | 9% on profits > AED 375,000 |

| Loss Carry-Forward | Not permitted | Permitted indefinitely |

| Transfer Pricing Documentation | Simplified arm’s length | Full master/local file if applicable |

| CT Return Filing | Mandatory | Mandatory |

The 2026 Sports Entity Exemption under Cabinet Decision No. 1 of 2026 grants Corporate Tax exemption to recognized non-profit sports bodies and internationally affiliated sports governance entities. Commercial gym operators distributing profits to shareholders will not qualify under the current criteria. Community sports clubs and academies affiliated with international federations should obtain a formal FTA ruling before applying the exemption.

Accounting for Revenue and Expenses in UAE Fitness Centers

Revenue recognition requires precise unbundling when membership packages include multiple services. The revenue from a Premium Membership priced at AED 2,000 per month that bundles unlimited gym access and four personal training sessions must be allocated between the two performance obligations based on their standalone selling prices. Revenue for facility access is recognized ratably over each month; PT session revenue is recognized at the point each session is completed and documented by the trainer.

Expense classification directly affects the Corporate Tax computation:

- Immediately deductible: Routine maintenance, trainer salaries, utilities, consumables, marketing costs

- Capitalized and depreciated: Major equipment purchases, leasehold fit-out, technology systems

- Non-deductible: Fines and penalties, undocumented expenditure, and entertainment for non-employees

Fitness centers using accounting and bookkeeping outsourcing benefit from consistent capital versus revenue expenditure classification, reducing the risk of FTA adjustments during a Corporate Tax examination.

Regulatory Compliance and Reporting Obligations

Economic Substance Regulations (ESR), under Cabinet Resolution No. 57 of 2020, require UAE entities conducting defined relevant activities to demonstrate adequate physical and economic presence in the UAE. Standard gym operations are generally not classified within the ESR’s relevant activity categories. However, gyms operating under international franchise structures with offshore management fee arrangements should confirm their ESR status with a qualified advisor.

Anti-Money Laundering (AML) compliance under Federal Decree-Law No. 20 of 2018 applies to all UAE businesses. Although fitness centers are not classified as Designated Non-Financial Businesses and Professions (DNFBPs), large cash payments for annual memberships should be processed through verified banking channels to maintain audit trails consistent with FTA and Central Bank expectations.

Ultimate Beneficial Owner (UBO) disclosure under Cabinet Decision No. 58 of 2020 requires all UAE-registered entities — including fitness centers — to maintain an updated register identifying individuals who own or control 25% or more of the entity. This register must be filed with the licensing authority and updated within 15 days of any ownership change.

Audit Requirements for Gyms and Fitness Centers in the UAE

A UAE mainland fitness center with annual revenue below AED 50 million is not subject to a mandatory federal statutory audit solely on revenue grounds. All Qualifying Free Zone Persons (QFZPs) seeking to benefit from the 0% Corporate Tax rate must submit audited financials regardless of revenue level. Most major free zones — including DMCC, JAFZA, and IFZA — mandate annual audit submissions as a condition of license renewal.

Even where a statutory audit is not legally required, audited financial statements are frequently necessary for:

- Annual free zone license renewal

- Maintaining corporate banking facilities with UAE financial institutions

- Facilitating dividend distributions or new investor entry

- Securing financing from UAE-based lenders

The audit scope for a gym typically covers deferred revenue accuracy, lease liability calculations, equipment depreciation schedules, payroll compliance (WPS and gratuity), and VAT return reconciliations. Discrepancies between gym management software data and the accounting ledger represent the most common audit finding across the sector.

Industry-Specific Accounting Considerations for Fitness Centers

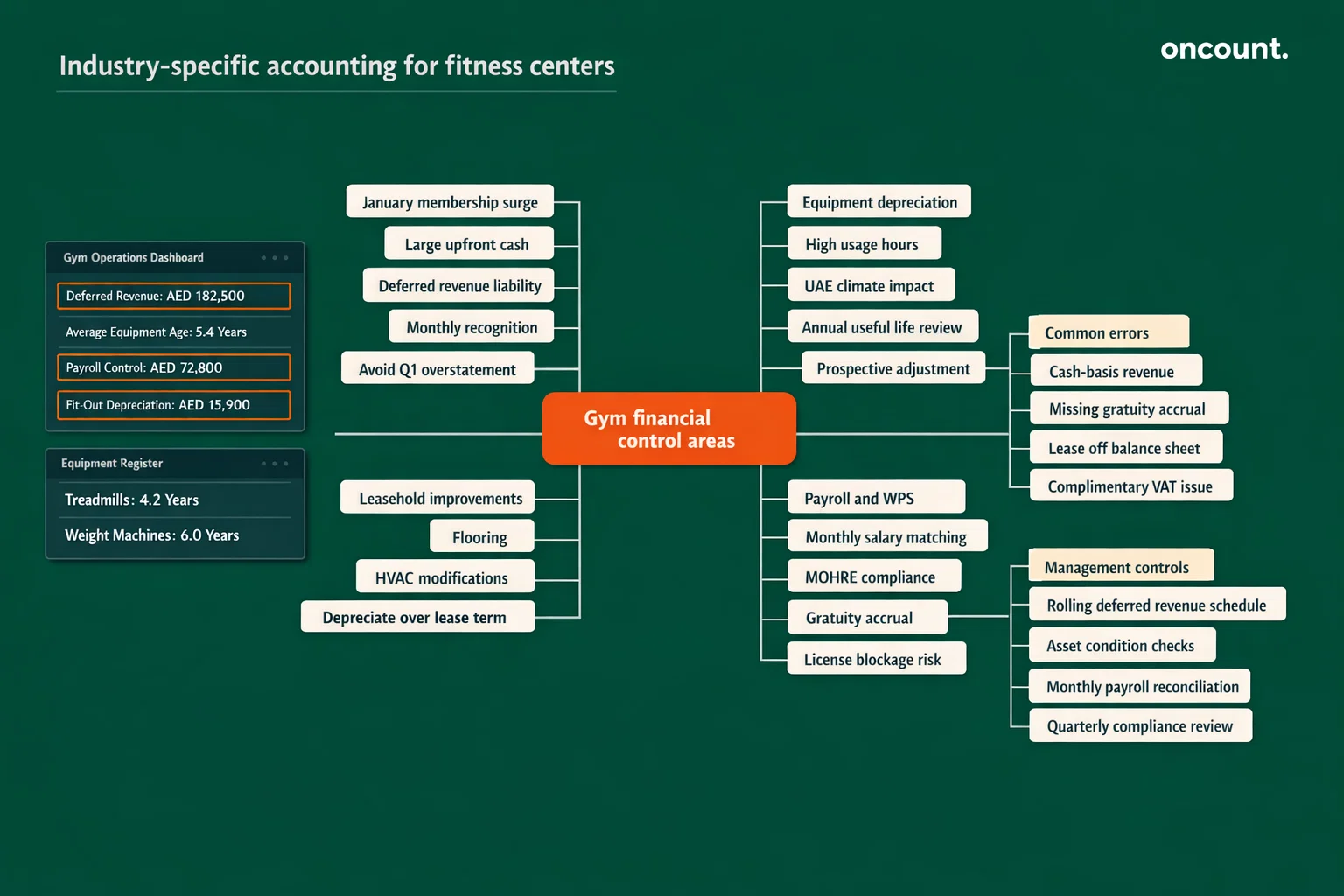

The January Surge and Deferred Revenue Management

The annual influx of January membership sign-ups creates a material risk of income overstatement if deferred revenue is not applied correctly. A gym collecting AED 600,000 in January from annual memberships must record the full amount as a liability and recognize only AED 50,000 per month over the following 12 months. Failure to apply this treatment inflates Q1 profits while understating Q2–Q4 performance, distorting both management decision-making and the Corporate Tax computation.

UAE Climate Factor and Equipment Depreciation Adjustments

Sustained ambient temperatures exceeding 40°C during UAE summer months accelerate the degradation of treadmill motors and electronic consoles. An asset register that assigns a standard seven-year useful life to cardio equipment without reference to actual usage hours and environmental conditions may materially understate depreciation charges. Under IAS 16, useful life estimates must be reviewed at least annually, and any revision applied prospectively from the date of reassessment.

Leasehold Improvements and Short Lease Terms

Fitness center fit-out costs — including rubber performance flooring, plumbing installations, HVAC modifications, and soundproofing — must be capitalized and depreciated over the shorter of their useful life or the remaining lease term. A Dubai gym incurring AED 1,200,000 in fit-out costs under a five-year lease records annual depreciation of AED 240,000 — a fixed charge that significantly affects operating profitability from the first year of operation and must be factored into pre-opening financial models.

Common Accounting Challenges for Fitness Centers in the UAE

| Challenge | Root Cause | Financial Consequence |

| Deferred revenue has not been applied | Cash-basis bookkeeping | Overstated income; incorrect Corporate Tax filing |

| Gratuity is not accrued monthly | Absence of payroll controls | Liquidity risk; MOHRE labor case exposure |

| VAT on complementary services not declared | Misunderstanding of deemed supply rules | FTA back-assessment; administrative penalties |

| Lease not recognized on the balance sheet | IFRS 16 non-compliance | Understated liabilities; audit qualification |

| Equipment depreciation is not adjusted for climate | No annual useful life review | Inflated asset values; understated depreciation |

Misclassifying deferred revenue is the most prevalent accounting error across UAE gyms. Inadequate gratuity provisioning creates immediate cash flow exposure when long-tenure staff depart. VAT misclassification of complimentary services — including free guest passes and staff fitness perks — is consistently identified during FTA field audits and can result in output VAT assessments plus administrative penalties under Cabinet Decision No. 74 of 2023.

Best Practices for Accounting and Financial Management in UAE Gyms

- Adopt FTA-ready cloud accounting software such as Zoho Books or Xero, integrated directly with gym management platforms like Mindbody or Glofox, to automate VAT capture and eliminate manual reconciliation gaps.

- Maintain a rolling deferred revenue schedule updated monthly to ensure IFRS 15 compliance and accurate profit recognition across membership contract terms.

- Review equipment useful life estimates annually against actual usage data and physical condition assessments, adjusting depreciation rates where UAE climate conditions have accelerated wear beyond original estimates.

- Accrue end-of-service gratuity monthly using the MOHRE-prescribed formula, and evaluate the UAE Voluntary Savings Scheme — available since 2023 — as a structured alternative to lump-sum settlement payments.

- Reconcile WPS payroll files monthly against MOHRE labor contract records to prevent the automatic trade license blockages triggered by salary discrepancies in the Wage Protection System.

- Engage qualified accounting and bookkeeping firms in the UAE with fitness sector experience for quarterly compliance reviews, particularly ahead of VAT return deadlines and the annual Corporate Tax filing cyclе

Comparison: Free Zone vs. Mainland Accounting Requirements for Gyms

| Requirement | Mainland | Free Zone |

| Corporate Tax Rate | 9% on profits > AED 375,000 | 0% on qualifying income (conditions apply) |

| Audit Obligation | Required if revenue > AED 50M | Mandatory annually (most free zones) |

| UAE Market Access | Unrestricted | Primarily intra-free zone or international |

| Foreign Ownership | 100% (post-2021 reforms) | 100% |

| VAT Registration Threshold | AED 375,000 | AED 375,000 |

| IFRS Compliance | Mandatory | Mandatory |

| UBO Register Filing | Required | Required |

| WPS Compliance | Enforced by MOHRE | Enforced by free zone authority equivalent |

Mainland fitness centers benefit from unrestricted access to UAE government institutions and walk-in clientele across all seven emirates. Free zone gyms embedded in lifestyle developments must verify that their revenue sources meet the qualifying income criteria under the Corporate Tax Law before assuming the 0% rate applies to their operations.