Key Takeaways

- Beauty salons with annual taxable supplies exceeding AED 375,000 are mandatory VAT registrants under Federal Decree-Law No. 8 of 2017

- UAE Corporate Tax at 9% applies to net profits above AED 375,000 for financial years beginning on or after June 1, 2023

- Gift vouchers, prepaid packages, and loyalty points must be deferred as contract liabilities under IFRS 15 — not recognized as immediate revenue

- Visa and onboarding costs per employee (AED 5,000–10,000) must be amortized over the two-year visa life, not expensed in full upfront

- Mainland salons are subject to mandatory annual audits under Federal Decree-Law No. 32 of 2021

- Financial records must be retained for a minimum of five years under VAT Law and seven years under Corporate Tax Law

- Salons importing professional products must apply landed cost valuation, including customs duty, shipping, and insurance

- Small Business Relief exempts salons with revenue below AED 3 million from Corporate Tax obligations, subject to proper record-keeping

Overview of Accounting Requirements in the UAE for Beauty Salons

Beauty salon owners and wellness center operators in the UAE are legally required to maintain complete and accurate books of accounts under Federal Decree-Law No. 32 of 2021 (the Commercial Companies Law). This obligation applies regardless of business size and encompasses all financial transactions, supporting documents, and statutory reports. Failure to maintain proper records exposes a business to penalties from both the Federal Tax Authority and the relevant emirate’s Department of Economy.

The accounting and bookkeeping services in UAE framework applicable to beauty salons aligns with International Financial Reporting Standards (IFRS) or IFRS for SMEs, depending on the entity’s size and registration type. The Federal Tax Authority mandates that VAT-registered businesses retain all tax invoices, credit notes, and financial records for a minimum of five years. Under the UAE Corporate Tax Law (Federal Decree-Law No. 47 of 2022), the retention requirement extends to seven years for documents used in determining taxable income.

UAE commercial law further requires that salons registered as mainland limited liability companies (LLCs) undergo an annual statutory audit conducted by a licensed auditor registered with the UAE Ministry of Economy. This requirement transforms the audit from a formality into an active compliance mechanism — particularly critical now that Corporate Tax has introduced a direct financial consequence for inaccurate reporting.

Key accounting obligations for UAE beauty salons include:

- Maintaining a general ledger aligned with a salon-specific chart of accounts

- Issuing tax-compliant invoices for all services and retail sales

- Preparing quarterly VAT returns through the EmaraTax portal

- Preparing annual financial statements in accordance with IFRS

- Retaining payroll records, visa documentation, and supplier invoices for the legally required periods

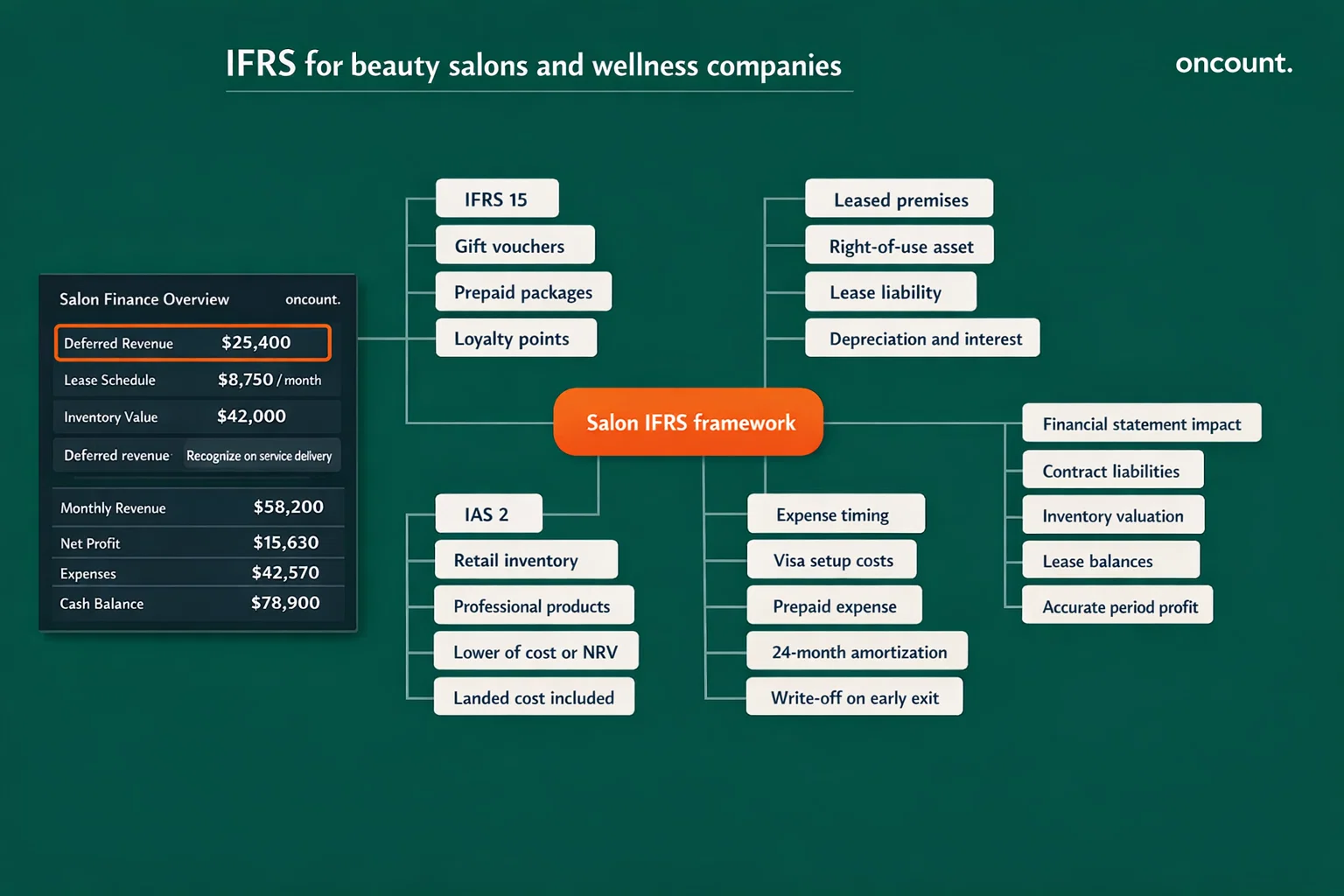

IFRS Application for Beauty Salons and Wellness Companies

International Financial Reporting Standards govern how beauty salons in the UAE recognize revenue, value assets, and classify liabilities. The three most operationally significant standards for this sector are IFRS 15, IFRS 16, and IAS 2.

IFRS 15 (Revenue from Contracts with Customers) directly affects how salons account for prepaid packages, gift vouchers, and loyalty programs. The standard requires that revenue be recognized only when a performance obligation is satisfied — meaning when the service is actually delivered, not when cash is received. A salon that collects AED 10,000 in December from clients purchasing New Year gift vouchers must record that amount as a contract liability (deferred revenue) on the balance sheet until each voucher is redeemed.

IFRS 16 (Leases) applies to any salon operating from leased premises. Under this standard, operating leases with terms exceeding 12 months must be brought onto the balance sheet as a right-of-use (ROU) asset and a corresponding lease liability. For Dubai salons operating under multi-year tenancy contracts — which are standard in the market — this significantly impacts both the balance sheet structure and the profit and loss statement, replacing a straight rental expense with depreciation and interest charges.

IAS 2 (Inventories) governs the valuation of retail products held for sale. Beauty salons that carry retail inventory must apply the lower of cost or net realizable value principle. For imported products, cost must include all landed costs — the invoice price, customs duty, freight, and insurance — not simply the supplier price.

Bookkeeping Framework and Financial Records Structure for Salons

A well-structured chart of accounts is the operational foundation of a salon’s accounting system. The chart must distinguish between service revenue, retail revenue, and deferred revenue — three categories that carry different tax and reporting treatments under UAE law.

Recommended chart of accounts categories for a UAE beauty salon:

- Revenue accounts: Service revenue, retail product revenue, deferred revenue (vouchers and packages)

- Cost of goods sold: Professional product usage, retail product cost, imported inventory with landed costs

- Labor costs: Base salaries, commissions, visa amortization, end-of-service gratuity accruals

- Operating expenses: Rent, municipality market fee, utilities, marketing, software subscriptions

- Fixed assets: Leasehold improvements, salon furniture, professional equipment, IT systems

- Tax liabilities: VAT payable, corporate tax payable, withholding tax (if applicable)

- Prepaid and accrual accounts: Prepaid visa costs, prepaid license fees, accrued leave

Supporting documentation requirements are equally critical. Every transaction must be backed by a valid tax invoice, a bank statement entry, or a signed delivery note. The Federal Tax Authority conducts periodic audits of VAT-registered businesses, and the inability to produce original source documents is treated as a compliance failure, regardless of whether the figures on the return are accurate.

Financial Statement Preparation Requirements

Beauty salons registered as companies in the UAE are required to prepare a complete set of financial statements at the end of each financial year. These statements form the basis for the statutory audit, Corporate Tax filing, and bank account maintenance.

The four required financial statements are:

- Balance Sheet (Statement of Financial Position): Reflects assets, liabilities, and equity. For salons, this includes leasehold improvements, deferred revenue balances, visa prepayments, and lease liabilities under IFRS 16.

- Profit and Loss Statement (Income Statement): Reports service and retail revenue against COGS, labor, and operating expenses. The prime cost ratio — labor plus COGS as a percentage of revenue — is the key performance indicator tracked here.

- Cash Flow Statement: Differentiates between cash from operations, investing (equipment purchases), and financing activities. Seasonal volatility in Dubai makes this statement particularly important for identifying cash shortfalls.

- Notes to Financial Statements: Discloses accounting policies, depreciation schedules, deferred revenue movements, and tax positions. Notes provide auditors and the FTA with the context needed to assess compliance.

According to the UAE Ministry of Finance Corporate Tax Guide (2023), businesses must maintain audited financial statements to support accurate tax determination. Salons claiming Small Business Relief must demonstrate through these statements that annual revenue does not exceed AED 3 million.

VAT Compliance for Beauty Salons in the UAE

Value Added Tax (VAT) at the standard rate of 5% applies to virtually all beauty and wellness services provided in the UAE under Federal Decree-Law No. 8 of 2017. Both hair services and aesthetic treatments are standard-rated supplies, as are retail product sales. The Federal Tax Authority administers VAT through the EmaraTax platform, which handles registration, return filing, and payment processing.

| VAT Registration Type | Annual Turnover Threshold | Filing Frequency |

| Mandatory Registration | AED 375,000+ | Quarterly (or monthly if directed) |

| Voluntary Registration | AED 187,500–375,000 | Quarterly |

| Exempt (below threshold) | Below AED 187,500 | No filing required |

Input VAT recovery is an important cash flow tool for salon operators. VAT paid on inventory purchases, equipment, utilities, and marketing services is generally recoverable. However, Article 53 of the UAE VAT Executive Regulations blocks recovery on certain expenses, including staff entertainment costs and motor vehicles not used exclusively for business purposes. Accountants must flag these non-recoverable amounts separately in the ledger to avoid overstating the VAT receivable balance.

A common VAT compliance issue in Dubai salons concerns mandatory service charges. FTA guidance clarifies that a voluntary tip paid directly by a client to a staff member falls outside the scope of VAT. However, if a salon includes a mandatory service charge on the customer invoice, that charge is considered part of the consideration for the service and is subject to the 5% VAT. This distinction must be clearly reflected in the POS system’s tax mapping configuration.

Corporate Tax Framework for Beauty Salons in the UAE

UAE Corporate Tax (CT) applies a 9% rate to taxable net profits exceeding AED 375,000 for financial years beginning on or after June 1, 2023, under Federal Decree-Law No. 47 of 2022. For most independently operated salons and wellness centers, this threshold represents a meaningful trigger point — particularly for established brands in premium districts such as Downtown Dubai or Dubai Marina.

Corporate Tax obligations by entity type:

- Mainland LLC (salon company): Subject to 9% CT on taxable profits above AED 375,000; Small Business Relief available for revenue below AED 3 million

- Free Zone entity (e.g., DDA-registered salon): May qualify for 0% on qualifying income if all conditions are met; income from mainland customers may not qualify

- Natural person (sole proprietor with commercial license): Must register for CT if annual turnover exceeds AED 1,000,000; the registration deadline for those active in 2024 was March 31, 2025

- Freelancer or individual therapist: Subject to CT registration if conducting business under a commercial license above the AED 1 million threshold

Deductible expenses for Corporate Tax purposes include staff salaries, professional product costs, rent, and depreciation of fixed assets calculated in accordance with IFRS. Non-deductible items include fines and penalties, personal expenses passed through the business, and entertainment costs that lack a documented business purpose. Salons must maintain expense documentation that clearly demonstrates the business purpose of each cost to support the deduction in the event of an FTA review.

Accounting for Revenue and Expenses in Beauty Salons

Revenue recognition is the most technically demanding area of salon accounting under UAE standards. The beauty sector’s reliance on prepayment business models — vouchers, packages, and membership subscriptions — creates a persistent gap between cash receipts and earned revenue that must be carefully managed.

When a client purchases a “Buy 5, Get 1 Free” blowout package priced at AED 450 total, the salon must allocate the transaction price across all six sessions on a pro-rata basis. Each session redeemed triggers partial revenue recognition. The unredeemed balance remains a contract liability on the balance sheet. If historical data demonstrates a statistically reliable breakage pattern — for example, 12% of packages expire unredeemed — the salon may recognize that estimated breakage amount as revenue over the expected redemption period under IFRS 15’s breakage guidance.

| Revenue Type | Recognition Trigger | Balance Sheet Classification |

| Direct hair and beauty services | At time of service delivery | Service Revenue |

| Retail product sales | At point of sale | Retail Revenue |

| Gift vouchers (redeemed) | Upon redemption | Transferred from Deferred Revenue |

| Gift vouchers (breakage) | Based on historical probability | Contract Revenue (partial) |

| Prepaid session packages | Pro-rata per session used | Deferred Revenue (Liability) |

| Loyalty points | Upon redemption by customer | Contract Liability |

On the expense side, the most significant accounting complexity involves human capital costs. The cost of securing a UAE employment visa — including government fees, Emirates ID, health card, and processing charges — ranges from AED 5,000 to AED 10,000 per employee. Under IFRS, these costs qualify as prepaid expenses and must be amortized monthly over the two-year visa life. If a stylist’s employment is terminated before the visa expires, the unamortized balance must be immediately written off as an expense in the period of termination.

Regulatory Compliance and Reporting Obligations

Beyond VAT and Corporate Tax, beauty salons operating in the UAE must address several additional compliance frameworks that carry financial reporting implications.

Economic Substance Regulations (ESR): ESR, introduced under Cabinet Resolution No. 57 of 2020, requires UAE businesses in certain sectors to demonstrate genuine economic activity in the country. Most standard beauty salons do not fall into a “Relevant Activity” category under ESR. However, salons structured within holding groups or those earning royalties from brand licensing may need to assess ESR applicability and file the appropriate notification or report.

Anti-Money Laundering (AML): The UAE’s AML framework under Federal Decree-Law No. 20 of 2018 applies to businesses dealing in high-value cash transactions. A salon regularly receiving cash payments above AED 55,000 from a single customer in a single transaction may fall under the “Designated Non-Financial Business and Profession” (DNFBP) category, triggering enhanced due diligence and reporting obligations to the UAE Financial Intelligence Unit (FIU).

Ultimate Beneficial Owner (UBO) Reporting: Cabinet Resolution No. 58 of 2020 requires mainland companies to maintain and file a register of ultimate beneficial owners — individuals holding more than 25% ownership or effective control. For a family-owned salon business, this typically means registering the individual owners with the relevant authority. The register must be kept current and is subject to inspection by regulators.

Audit Requirements for Beauty Salons in the UAE

Annual statutory audits are mandatory for mainland LLCs under UAE Commercial Companies Law, and most free zone authorities impose equivalent requirements on their registered entities. For beauty salon businesses, the audit serves three practical functions beyond legal compliance: it validates financial statements used for bank account maintenance, supports Corporate Tax filings, and provides a defensible record in the event of an FTA investigation.

Auditors review the accuracy of revenue recognition (particularly deferred revenue balances), verify that fixed assets are correctly capitalized and depreciated, confirm VAT return reconciliation against the general ledger, and assess whether payroll costs — including visa amortization and end-of-service gratuity accruals — are correctly stated.

UAE banks increasingly require audited financial statements to maintain corporate accounts or approve financing. A salon seeking to negotiate a payment plan with a landlord or access a working capital facility will almost certainly need audited financials dated within the last 12 months. Engaging a licensed auditor early in the financial year — rather than scrambling post-year-end — significantly reduces the risk of material restatements.

Industry-Specific Accounting Considerations for Beauty and Wellness Businesses

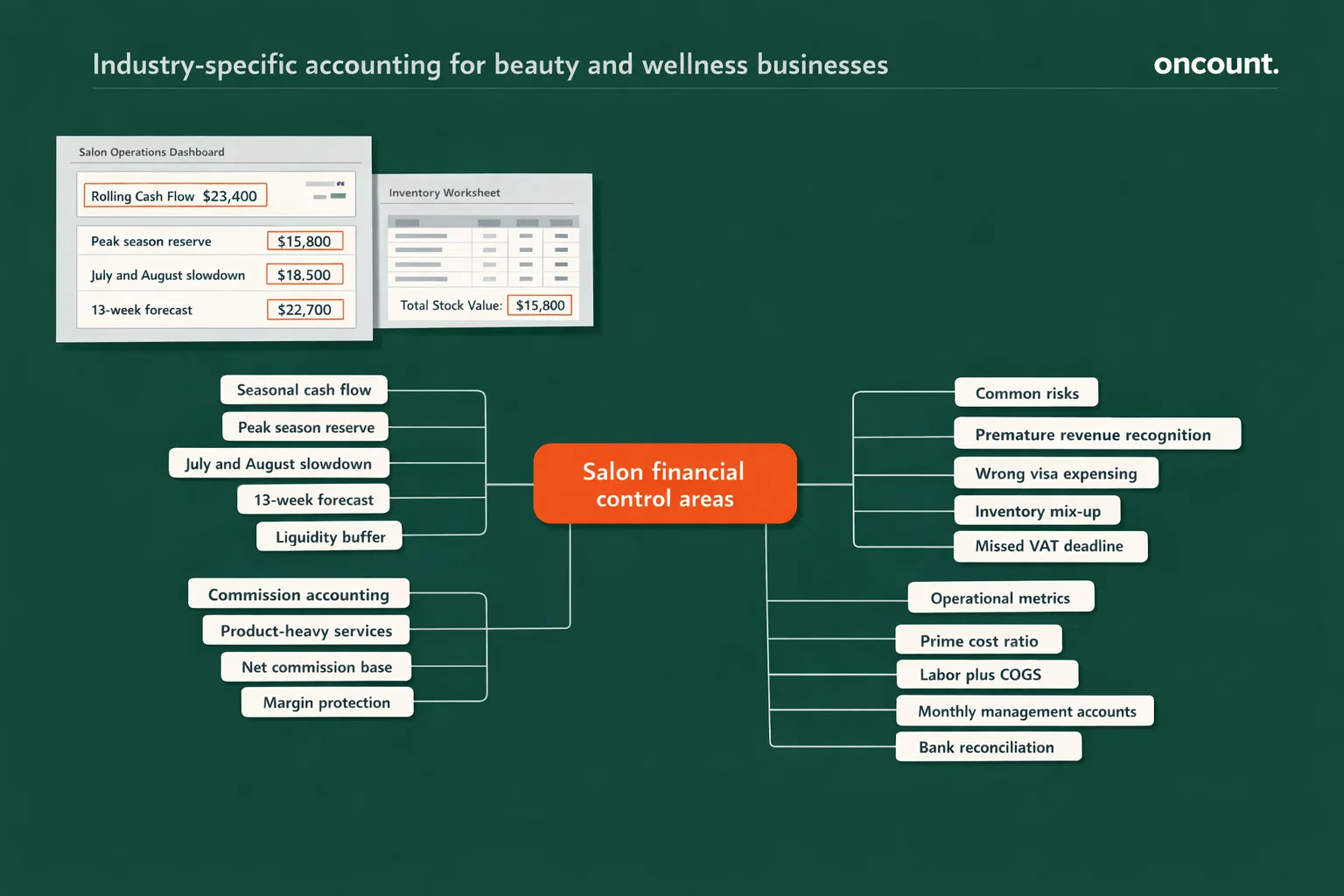

Seasonal Cash Flow and the Summer Slump

Dubai’s retail calendar creates extreme revenue seasonality. The high season runs from October through May, with the summer months of July and August representing the lowest booking volumes of the year. Industry data from Dubai-based salon operators indicates revenue drops of 30% to 50% during July and August compared to peak months. Financial planning for a UAE beauty salon must incorporate a formal seasonal cash flow model — specifically, a 13-week rolling cash flow forecast updated weekly.

Best practice involves reserving 20% to 40% of peak-season profits into a designated liquidity buffer. This buffer funds fixed costs — rent, minimum staff salaries, and utility deposits — through the lean period without requiring emergency borrowing.

Inventory Valuation and Landed Cost Calculation

Professional-use products (color, treatments, oils) imported from Europe or the United States require landed cost valuation under IAS 2. A consignment invoiced at EUR 3,000 may carry an additional 5% UAE customs duty, 3% insurance and freight charge, and AED 150 in customs processing fees. All of these costs form part of the inventory’s carrying value on the balance sheet. Monthly stocktaking — a physical count of both retail and professional inventory — is necessary to record shrinkage and expiration write-offs accurately.

Commission Accounting and Margin Protection

Stylist commissions represent the primary variable cost in a salon’s P&L. A commission calculated as a flat percentage of service revenue can erode margins when product-heavy services — such as balayage or keratin treatments — are involved. A technically sound approach calculates the commission base after deducting the product cost and a fixed overhead allocation, protecting the salon’s net margin even at high sales volumes.

| Service | Retail Price (AED) | Product Cost (AED) | Net Commission Base (AED) | Commission at 35% (AED) | Salon Margin |

| Blowout | 200 | 15 | 185 | 65 | 60% |

| Balayage | 800 | 320 | 480 | 168 | 64% |

| Facial | 350 | 40 | 310 | 109 | 69% |

| Manicure | 120 | 20 | 100 | 35 | 71% |

Common Accounting Challenges for Beauty Salon Companies

Premature revenue recognition is the most frequently encountered error in salon bookkeeping. Cash received for vouchers and packages is recorded directly as income — rather than as a liability — producing artificially inflated profit figures. When the FTA reviews VAT returns, a mismatch between cash receipts and recognized service revenue is a red flag that can trigger a full tax audit.

Incorrect visa cost expensing is similarly common. Many salon owners instruct their bookkeeper to expense visa costs in full in the month they are paid. Under IFRS, this misrepresents profitability by front-loading costs. The correct treatment — prepaid expense amortized monthly over 24 months — produces a more accurate picture of the business’s financial position.

Non-segregation of retail and professional inventory creates two problems: inaccurate COGS and unreliable VAT input recovery tracking. Professional-use products consumed in service delivery are expensed when used; retail products remain on the balance sheet until sold. Mixing these two categories results in balance sheet errors and can lead to incorrect VAT reclaim amounts on quarterly returns.

Additional common challenges include:

- Failing to accrue end-of-service gratuity (EOSB) monthly in accordance with UAE Labour Law

- Treating the 2.5% municipality market fee as a recoverable tax rather than a non-recoverable operating expense

- Applying incorrect depreciation lives to leasehold improvements that exceed the actual lease term

- Missing the quarterly VAT return deadline, which carries an automatic penalty under FTA regulations

Best Practices for Accounting and Financial Management in Wellness Businesses

Implementing a structured accounting framework from the point of business setup significantly reduces the risk of regulatory penalties and financial misstatement. The following practices reflect established standards among professionally managed salons in Dubai and Abu Dhabi.

- Deploy an integrated POS-accounting system. Platforms such as Zenoti or Fresha, connected to Xero or QuickBooks, automate journal entry creation for each transaction. Tax mapping within the POS — assigning the correct VAT code to each service or product category — ensures that output VAT is captured accurately without manual intervention.

- Prepare monthly management accounts. A monthly profit and loss review, including prime cost analysis (labor plus COGS as a percentage of revenue), allows management to identify margin erosion before it becomes critical. A prime cost consistently above 60% signals that either labor costs or product costs require immediate review.

- Conduct monthly bank reconciliations. Every transaction on the bank statement must be matched to a corresponding entry in the accounting software. Unreconciled items are a leading indicator of either bookkeeping errors or unauthorized transactions.

- Accrue all statutory liabilities monthly. End-of-service gratuity, accrued annual leave, and visa amortization should be calculated and posted monthly — not annually. This prevents large, unexpected charges appearing at year-end and ensures the P&L reflects the true cost of employing staff throughout the year.

- Engage a licensed UAE auditor before year-end. Pre-audit preparation — including reconciling deferred revenue balances, reviewing fixed asset schedules, and confirming VAT return alignment with the general ledger — reduces audit time and the risk of material adjustments to submitted tax returns.

Comparison: Free Zone vs. Mainland Accounting Requirements for Beauty Salons

| Factor | Mainland (DET-Registered) | Free Zone (e.g., DDA, DMCC) |

| Annual audit | Mandatory (UAE Companies Law) | Mandatory (zone-specific authority) |

| Corporate Tax rate | 9% on profits above AED 375,000 | 0% on qualifying income; 9% otherwise |

| VAT registration | Mandatory above AED 375,000 | Mandatory above AED 375,000 |

| Market/municipality fee | 2.5%–5% of annual rent | Zone-specific flat fee structure |

| Accounting standard | IFRS or IFRS for SMEs | IFRS or IFRS for SMEs |

| Trade scope | Unrestricted within UAE | Zone and international only (mainland restricted) |

| UBO registration | Required (Cabinet Resolution 58/2020) | Required per zone authority rules |

| ESR applicability | Sector-dependent | More commonly triggered for certain activities |

Free zone beauty salons must be especially careful to maintain clear revenue segregation between qualifying zone-based income and any services rendered to mainland clients. The Federal Tax Authority’s qualification criteria under Cabinet Decision No. 55 of 2023 specify that income derived from mainland UAE transactions may not qualify for the 0% Corporate Tax rate, even for otherwise compliant free zone entities. An accountant managing a free zone salon must establish a tracking system within the chart of accounts that separates these revenue streams at the transaction level.