Key Takeaways

- All UAE law firms must prepare financial statements in accordance with IFRS, regardless of jurisdiction.

- Client trust accounts must be legally segregated from operating funds and reconciled on a monthly three-way basis.

- Law firms are subject to 5% VAT on legal services and 9% corporate tax on taxable profits exceeding AED 375,000.

- Law firms are classified as Designated Non-Financial Businesses and Professions (DNFBPs) under UAE AML law, requiring goAML registration and appointment of a Money Laundering Reporting Officer (MLRO).

- Free zone firms in the DIFC and ADGM are governed by separate regulators (DFSA and FSRA, respectively) with distinct audit and client money obligations.

- As of October 2025, the UAE AML law applies an objective liability test — firms can be held accountable if they reasonably should have identified illicit funds.

- Annual statutory audits are mandatory for most UAE legal entities, with heightened requirements in financial free zones.

Overview of Accounting Requirements for Law Firms in the UAE

Law firms in the UAE operate under a legal obligation to maintain accurate, IFRS-compliant financial records. Federal Law No. 32 of 2021 (the Commercial Companies Law) requires all mainland LLCs and joint-stock companies to retain financial records for a minimum of five years. This requirement applies equally to law firms structured as limited liability companies, professional civil companies, or branch offices of foreign firms.

Federal Decree-Law No. 34 of 2022 on Regulating the Profession of Law and Legal Consultancies governs the operational structure of mainland legal practices. This legislation explicitly prohibits lawyers from engaging in traditional commercial trade while permitting ownership of financial and real estate assets — a distinction that directly affects how a firm’s chart of accounts and capital structure must be configured.

Foreign law firms seeking to establish a branch in Abu Dhabi must meet stringent financial prerequisites: a minimum of 15 years of international practice, at least 50 global partners, and a bank-certified undertaking from the headquarters to financially underwrite UAE operations. These financial thresholds must be documented and maintained in the firm’s compliance records.

IFRS Application for Law Firms in the UAE

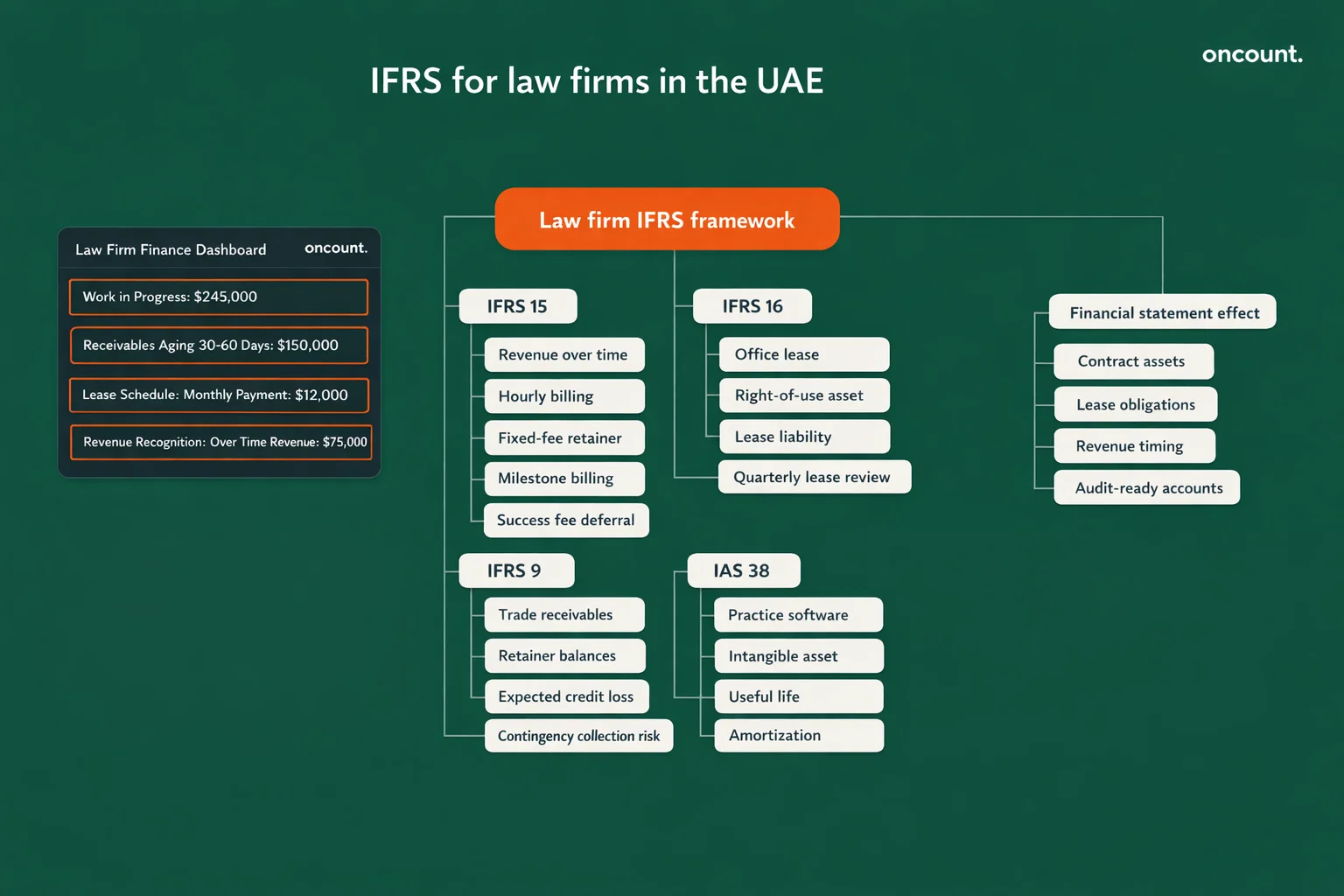

The UAE mandates IFRS as the national accounting standard for all commercial entities, including law firms. Article 237 of Federal Law No. 2 of 2015 requires firms to apply international standards when preparing interim or annual accounts. For legal practices, three IFRS standards carry the greatest operational weight.

IFRS 15 — Revenue from Contracts with Customers governs how and when a law firm recognizes income. Legal billing arrangements are inherently complex, involving hourly rates, fixed-fee retainers, milestone-based invoicing, and contingency success fees. Under IFRS 15, revenue is recognized over time — not upon billing — because clients simultaneously receive and consume legal services as they are delivered.

IFRS 16 — Leases requires law firms to record almost all commercial lease agreements on the balance sheet as right-of-use assets, with corresponding lease liabilities. Given the cost of office space in Dubai and Abu Dhabi, this standard materially affects balance sheet ratios and must be tracked with precision, including lease term schedules, applicable discount rates, and any lease modifications.

IFRS 9 — Financial Instruments applies to the measurement of trade receivables, retainer balances, and any financial assets held by the firm. Receivables must be assessed for expected credit losses, particularly for contingency-fee matters where collection is uncertain.

| IFRS Standard | Applicability to Law Firms | Key Requirement |

| IFRS 15 | Revenue recognition | Recognize income over the performance period |

| IFRS 16 | Office and equipment leases | Capitalize right-of-use assets |

| IFRS 9 | Receivables and financial assets | Apply the expected credit loss model |

| IAS 38 | Intangible assets (e.g., software) | Amortize over useful life |

Firms with annual revenue exceeding AED 50 million must apply the full IFRS framework. Smaller practices may qualify for IFRS for SMEs, which carries significantly reduced disclosure requirements.

Bookkeeping Framework and Financial Records for Legal Practices

A law firm’s bookkeeping structure must reflect both its professional obligations and the regulatory expectations of its licensing jurisdiction. The chart of accounts should be designed to separately track operating income, client trust liabilities, work-in-progress (WIP), and disbursements.

Core components of a law firm’s bookkeeping framework include:

- General ledger — segregated into operating accounts and trust accounts

- WIP ledger — tracks billable hours recorded but not yet invoiced

- Client sub-ledgers — individual records for each client holding trust funds

- Disbursement tracking — distinguishes between VAT-applicable reimbursements and out-of-scope court fees

- Partner capital accounts — reflects each partner’s equity contribution and profit allocation

Supporting documentation — including engagement letters, time-entry logs, invoices, and bank statements — must be retained for a minimum of five years under both the Commercial Companies Law and the UAE AML Law of 2018.

Work-in-progress management is a legally and financially critical function. WIP represents billable time recorded by lawyers and paralegals that has not yet been invoiced. Under IFRS 15, WIP must appear on the balance sheet as a contract asset, reflecting effort expended during the reporting period even in the absence of cash receipt.

Financial Statements Preparation for Law Firms

UAE law firms are required to prepare a complete set of IFRS-compliant financial statements annually. These statements serve multiple functions: satisfying regulatory requirements, supporting tax filings, and providing transparency to partners and external stakeholders.

Mandatory financial statements include:

- Statement of Financial Position (Balance Sheet) — reflects assets, including WIP, right-of-use assets, and cash; liabilities, including trust account balances and lease obligations; and partner equity.

- Statement of Profit or Loss — presents net revenue after deducting admissible expenses such as salaries, rent, marketing, and professional indemnity insurance.

- Statement of Cash Flows — distinguishes between operating, investing, and financing activities.

- Notes to Financial Statements — discloses accounting policies, lease terms, revenue recognition methods, and related-party transactions.

Accurate financial statement preparation is directly tied to corporate tax compliance. According to the UAE Ministry of Finance Corporate Tax Guide (2023), businesses must maintain audited financial statements for accurate tax determination. Firms generating revenue above AED 50 million must submit audited financials alongside their corporate tax return.

VAT Compliance for Law Firms in the UAE

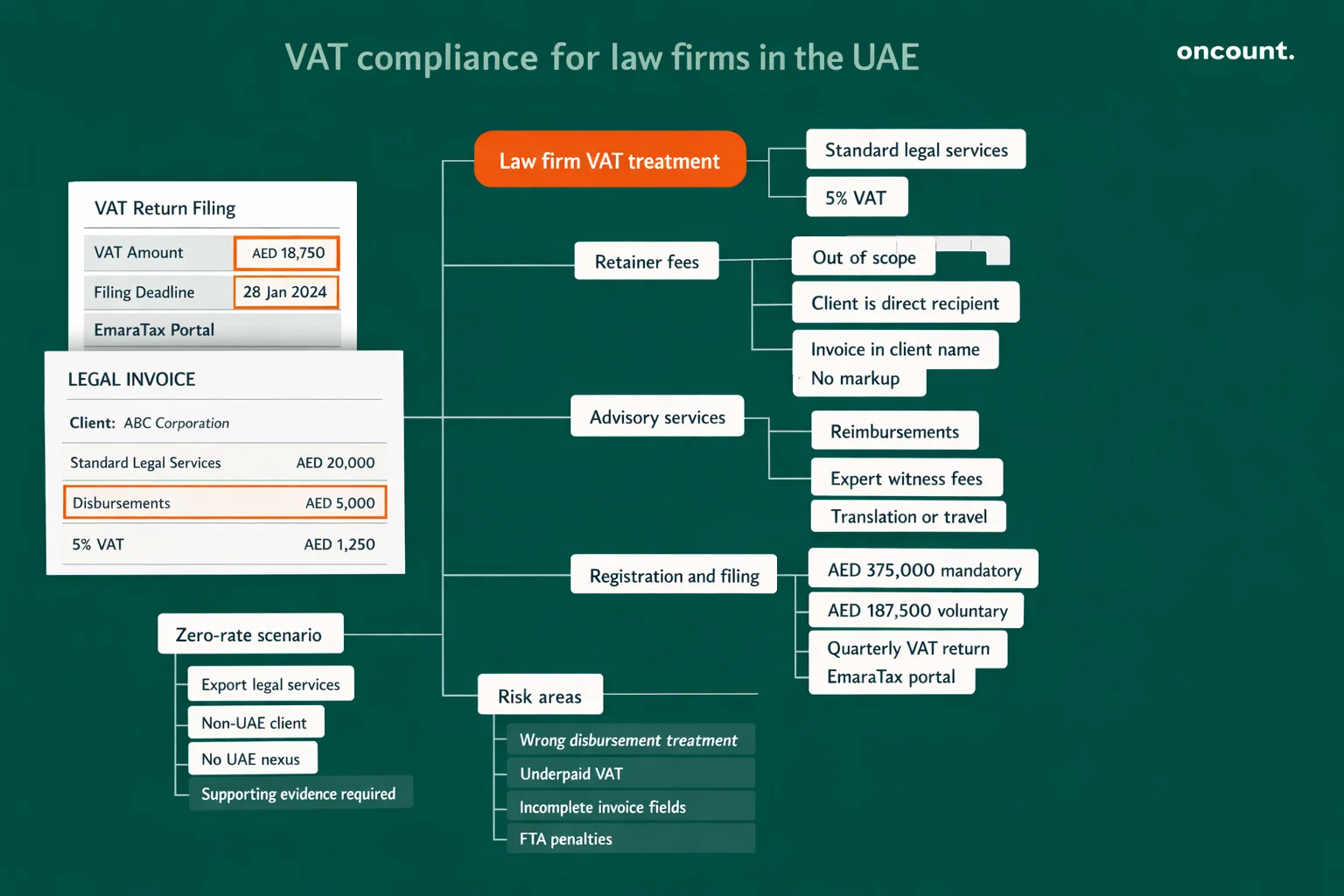

Legal services in the UAE are subject to a standard VAT rate of 5% under Federal Decree-Law No. 8 of 2017. Mandatory VAT registration applies once taxable supplies exceed AED 375,000 annually, with voluntary registration permitted from AED 187,500.

The most operationally significant VAT issue for law firms is the correct treatment of costs incurred on behalf of clients. The Federal Tax Authority’s Public Clarification VATP013 draws a critical distinction between disbursements and reimbursements.

- Disbursements are out-of-scope for VAT when all three conditions are met: the client is the direct recipient of the third-party service, the original invoice is in the client’s name, and the firm recovers exactly the amount paid with no markup. Court filing fees and government registration charges typically qualify.

- Reimbursements are treated as part of the consideration for legal services and must be charged at 5% VAT. This applies when the firm is the contracting party — for example, when engaging expert witnesses, arranging travel, or commissioning translations.

| VAT Treatment | Condition | Example |

| Out-of-scope (disbursement) | Client is the direct recipient; no markup | Court filing fees |

| Taxable at 5% (reimbursement) | The firm is the contracting party | Expert witness fees |

| Taxable at 5% (legal service) | Standard service delivery | Retainer fees, advisory |

| Zero-rated | Export of legal services | Advice to a non-UAE client with no UAE nexus |

VAT returns must be filed 28 days after the end of each tax period, which is typically quarterly. Firms using the EmaraTax portal administered by the Federal Tax Authority must ensure that all tax invoices meet the mandatory fields specified under UAE VAT law.

Corporate Tax Framework for Law Firms in the UAE

UAE Corporate Tax, introduced under Federal Decree-Law No. 47 of 2022, applies to financial years beginning on or after June 1, 2023. Law firms structured as legal entities — including LLCs, civil companies, and branch offices — are subject to a 9% tax rate on taxable profits exceeding AED 375,000.

All law firms must register for corporate tax regardless of profitability. Registration is completed through the EmaraTax platform. Corporate tax returns must be filed within nine months of the financial year-end.

For multi-partner law firms, the calculation of taxable profit requires careful deduction of admissible operating expenses. Allowable deductions include staff salaries, office rent, professional indemnity insurance, IT infrastructure costs, and marketing expenses. Partner profit distributions and entertainment expenses above prescribed limits may be subject to deduction restrictions.

Firms with annual revenue below AED 3 million may elect for Small Business Relief, reducing their effective tax rate to 0% for eligible periods. This election must be made annually and is subject to FTA approval.

Free zone firms operating in the DIFC or ADGM may qualify as Qualifying Free Zone Persons (QFZPs) for a 0% rate on qualifying income, provided they maintain adequate substance in the zone and derive income exclusively from qualifying activities. Income from services provided to mainland UAE clients is generally treated as non-qualifying and taxed at 9%. This necessitates cost-center accounting to segregate income streams.

Accounting for Revenue and Expenses in Legal Practices

Law firm revenue recognition follows the IFRS 15 five-step model: identify the contract, identify performance obligations, determine the transaction price, allocate the price to obligations, and recognize revenue as obligations are satisfied.

A single client engagement may contain multiple distinct performance obligations. For example, an engagement covering an initial legal opinion followed by courtroom representation involves two separable services, each recognized independently as the firm performs.

Contingency or success fees introduce variable consideration. Under IFRS 15, the Federal Tax Authority guidance recommends that firms recognize variable fees only when it is highly probable that no significant reversal of cumulative revenue will occur. In practice, this means success fees for ongoing litigation are often deferred until the matter concludes.

Typical expense categories for UAE law firm financial statements:

- Personnel costs (salaries, visa fees, end-of-service gratuity provisions)

- Office rent (capitalized under IFRS 16 for multi-year leases)

- Professional indemnity insurance

- Bar association fees and licensing costs

- Technology and practice management software subscriptions

- Client development and marketing expenses

Regulatory Compliance and Reporting Obligations

Law firms in the UAE carry compliance obligations that extend well beyond tax and accounting. Three regulatory frameworks directly affect how financial records must be structured and maintained.

Economic Substance Regulations (ESR), introduced by Cabinet Resolution No. 57 of 2020, require UAE entities conducting relevant activities to demonstrate genuine economic presence. For law firms, legal advisory services may constitute a relevant activity. Firms must file annual ESR notifications and, where required, substance reports demonstrating adequate staffing, premises, and expenditure in the UAE.

Anti-Money Laundering (AML) obligations classify UAE law firms as DNFBPs under the UAE AML Law of 2018 and its October 2025 amendments. Firms must register on the goAML platform, appoint a qualified MLRO, and apply a risk-based approach to client onboarding. The 2025 amendment introduces an objective liability test: a legal professional can face prosecution if it would have been reasonable to identify illicit funds, even without actual knowledge. The accounting department plays a direct role in monitoring red flags such as unexplained third-party payments, sudden changes in beneficial ownership, and transactions with no apparent legal rationale.

Ultimate Beneficial Owner (UBO) reporting requires firms to maintain and update records of individuals who ultimately own or control the firm. These records must be submitted to the relevant licensing authority and kept current in the firm’s internal compliance files.

All CDD records, transaction logs, and internal risk assessments must be retained for a minimum of five years.

Audit Requirements for Law Firms in the UAE

Annual statutory audits are mandatory for the majority of UAE law firms. Under Commercial Companies Law No. 32 of 2021, all mainland LLCs and joint-stock companies must appoint an independent auditor licensed by the UAE Ministry of Economy. Auditors must hold recognized professional qualifications such as CPA or ACCA.

For firms in the DIFC, auditors must be approved by the Dubai Financial Services Authority (DFSA). ADGM firms require auditors recognized by the Financial Services Regulatory Authority (FSRA). In both free zones, the scope of the audit extends beyond financial statements to include compliance with client money rules and AML procedures.

| Audit Category | Mainland | DIFC | ADGM |

| Statutory Audit | Mandatory (LLC/PJSC) | Mandatory | Mandatory |

| Approved Auditor | UAE MOE Licensed | DFSA-Approved | FSRA-Approved |

| Client Money Review | Regulatory expectation | Mandatory | Mandatory |

| AML Audit | Risk-based | Required | Required |

| Financials Language | Arabic available | English | English |

For firms with revenue exceeding AED 50 million, audited financial statements are mandatory for corporate tax filing. The audit must verify the accuracy of the tax return and confirm the integrity of the income recognition methodology.

Industry-Specific Accounting for Legal Practices

Client Trust Account Governance

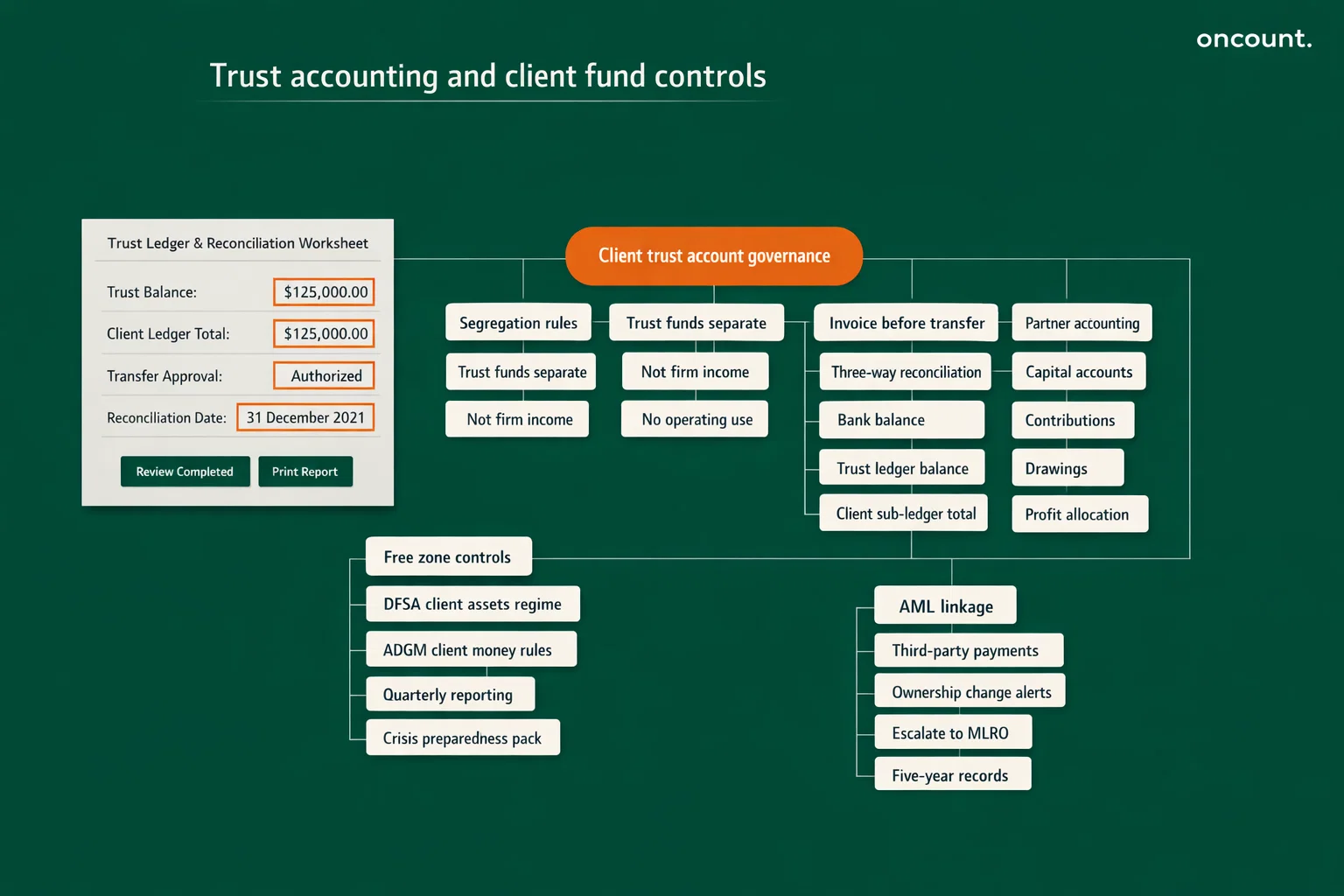

The segregation of client funds is the most legally sensitive area of law firm accounting. A client trust account represents a liability on the firm’s balance sheet — it reflects money held on behalf of third parties, not income of the firm. Funds may only be transferred to the operating account once legal work has been completed and a formal invoice issued.

The mandatory three-way reconciliation must be performed monthly and satisfies the following mathematical relationship:

Bank Balance = Trust Ledger Balance = Sum of All Individual Client Sub-Ledger Balances

Any discrepancy, regardless of size, must be investigated and resolved immediately. The DFSA’s revised Client Assets Regime, effective January 1, 2026, introduces a “Client Assets Crisis Preparedness Pack” — a structured data set designed to allow regulators and liquidators to retrieve client fund information immediately in the event of firm insolvency.

Work-in-Progress (WIP) Valuation

WIP valuation requires firms to estimate the realizable value of unbilled time. Not all recorded hours translate to invoiceable amounts — write-downs occur when the billed amount is adjusted for client negotiations, write-offs, or fixed-fee caps. Monthly WIP reconciliations ensure the income statement accurately reflects effort expended during the period.

Partner Capital and Profit Allocation

In multi-partner firms, the partnership deed or shareholder agreement governs how taxable profit is allocated among partners. Each partner’s capital account must be maintained separately, tracking contributions, drawings, and profit distributions. These accounts are subject to corporate tax treatment and must be clearly documented for FTA review.

Common Accounting Challenges for Law Firms in the UAE

Misclassification of disbursements as reimbursements is one of the most frequent VAT errors in legal practices. Charging 5% VAT on a court fee that should be treated as an out-of-scope disbursement — or failing to charge VAT on an expert witness fee that qualifies as a reimbursement — can result in underpayment or overpayment of VAT, both of which attract FTA penalties.

Commingling of client and firm funds remains a serious compliance risk. In practice, this occurs when small amounts from client trust accounts are inadvertently used to cover operating shortfalls, or when interest earned on pooled trust funds is not properly attributed. Both the DIFC and ADGM require written client consent before pooling funds and mandate quarterly reporting of trust account activity.

WIP write-down timing creates income statement distortions when firms defer write-downs to avoid reporting a loss in a particular period. IFRS 15 requires that the carrying value of a contract asset reflect only the amount that is highly probable of collection — delayed recognition of write-downs constitutes a misstatement.

Inadequate AML documentation is a growing enforcement priority. Following the October 2025 amendments, the objective test for AML liability means that firms cannot rely solely on client self-declarations. Accounting teams must flag transactions that deviate from established client profiles and escalate promptly to the MLRO.

Best Practices for Accounting and Financial Management

Effective financial governance in a UAE law firm requires proactive systems, qualified personnel, and ongoing regulatory monitoring. The following practices reduce compliance risk and improve financial visibility.

- Implement specialist legal accounting software — platforms such as Clio Manage, App4Legal, or Zoho Books with legal modules provide integrated time-tracking, trust reconciliation, and FTA-compliant VAT invoicing within a single system.

- Conduct monthly three-way reconciliations — do not treat this as an annual audit preparation task. Monthly reconciliation catches discrepancies before they compound.

- Engage a qualified MLRO — the MLRO should have direct access to accounting records and participate in client onboarding reviews for high-risk matters.

- Separate free zone and mainland income streams — firms eligible for QFZP status must maintain cost-center accounting to protect the 0% rate on qualifying income from contamination by non-qualifying revenues.

- Review IFRS 16 lease schedules quarterly — lease modifications, rent-free periods, and lease extensions must be captured immediately to maintain accurate right-of-use asset balances.

- Train finance staff on AML red flags — the accounting team is often the first line of defense. Unusual payment sources, third-party funding, and inconsistent transaction patterns should trigger an internal escalation process.

Comparison: Free Zone vs. Mainland Accounting for Law Firms

| Requirement | Mainland | DIFC | ADGM |

| Governing Law | UAE Federal / Civil Law | Codified Common Law | English Common Law |

| Regulatory Authority | Ministry of Justice / DED | DFSA / DIFC Authority | FSRA / ADGM Authority |

| Accounting Standard | IFRS (Mandatory) | IFRS | IFRS |

| Audit Requirement | Mandatory (LLC/PJSC) | Mandatory (all firms) | Mandatory (all firms) |

| Primary Language | Arabic (regulatory filings) | English | English |

| Corporate Tax Rate | 9% (>AED 375,000) | 9% / 0% (QFZP) | 9% / 0% (QFZP) |

| Client Money Rules | General fiduciary obligation | DFSA Client Assets Regime | ADGM Client Money Rules 2021 |

| AML Registration | goAML (Ministry of Justice) | goAML (DFSA oversight) | goAML (FSRA oversight) |

| ESR Applicability | Yes | Yes (if relevant activity) | Yes (if relevant activity) |

Free zone firms benefit from English-language documentation requirements, which simplify financial consolidation for international legal networks. However, the DIFC and ADGM impose stricter and more formal client money obligations, including quarterly client trust reporting and mandatory crisis preparedness documentation under the 2026 DFSA regime.