Key Takeaways

- UAE Corporate Tax applies a 9% rate to taxable profits exceeding AED 375,000; agencies with revenue below AED 3 million may qualify for Small Business Relief until December 31, 2026

- VAT registration is mandatory when taxable supplies exceed AED 375,000; voluntary registration is available from AED 187,500

- The Reverse Charge Mechanism (RCM) applies to all international advertising platform spend, including Google Ads, Meta, and TikTok

- Every marketing agency — mainland or free zone — must maintain IFRS-compliant financial records for a minimum of seven years for corporate tax purposes

- Annual external audits are mandatory for mainland DED-licensed agencies and all major free zone entities, including DMCC, DDA, and DIFC

- E-invoicing becomes mandatory for large UAE businesses from January 1, 2027; broader rollout covers all VAT-registered entities from July 2027

Overview of Accounting Requirements in the UAE for Marketing Agencies

Marketing agencies operating in Dubai are subject to the UAE Commercial Companies Law (Federal Law No. 2 of 2015) and Federal Tax Authority regulations, both of which mandate the maintenance of accurate, auditable financial records. The FTA requires VAT records to be retained for a minimum of five years, while the UAE Corporate Tax Law (Federal Decree-Law No. 47 of 2022) extends the record retention obligation to seven years for corporate tax documentation.

All agency financial records must align with International Financial Reporting Standards (IFRS) as adopted in the UAE. This requirement applies regardless of whether the agency is incorporated on the mainland under the Department of Economic Development (DED) or within a free zone such as Dubai Media City (DDA), the Dubai Multi Commodities Centre (DMCC), or the Dubai International Financial Centre (DIFC). The UAE Ministry of Finance has consistently confirmed that IFRS compliance is non-negotiable for all entities preparing financial statements for regulatory or audit purposes.

For agencies still using cash-basis bookkeeping — a common legacy practice in boutique Dubai studios — the 2026 transition window represents the final opportunity to migrate to accrual-based accounting. The FTA’s use of data analytics to cross-verify filings means informal recordkeeping will increasingly be identified during compliance reviews.

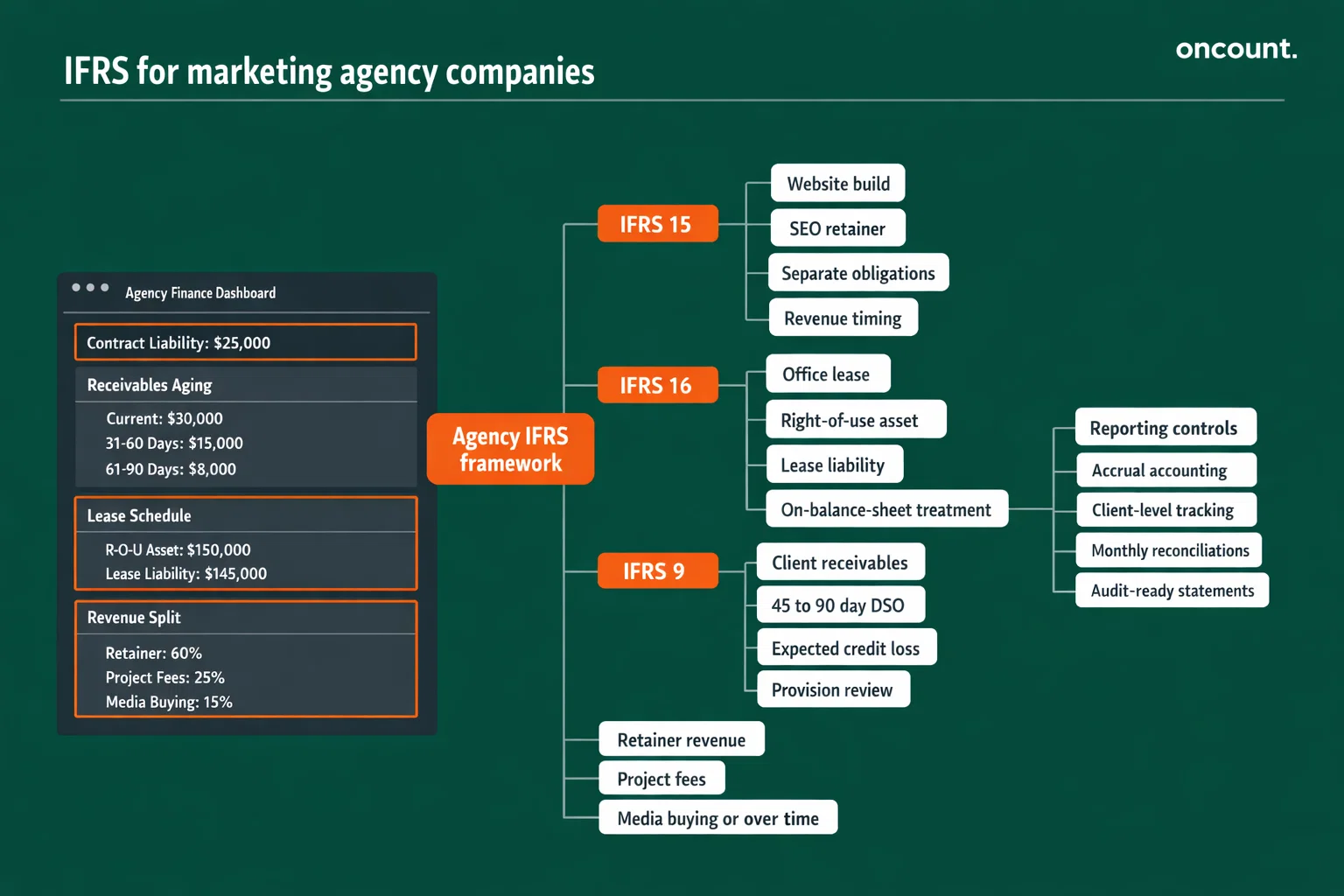

IFRS Application for Marketing Agency Companies

The most operationally significant IFRS standard for Dubai marketing agencies is IFRS 15 (Revenue from Contracts with Customers), which governs how and when revenue is recognized. IFRS 15 requires agencies to apply a structured five-step model: identify the contract, identify distinct performance obligations, determine the transaction price, allocate that price across obligations, and recognize revenue as each obligation is satisfied.

In practice, a client contract combining a website build with a six-month SEO retainer contains two separate performance obligations. The website build is recognized at a point in time upon delivery; the SEO retainer is recognized evenly across the service period. Advance payments must be recorded as “Contract Liabilities” on the balance sheet until the corresponding service is delivered.

IFRS 16 (Leases) affects agencies with long-term office leases in Dubai, requiring the recognition of right-of-use assets and corresponding lease liabilities. Agencies with significant premises in locations such as Business Bay or DIFC must reflect these on-balance-sheet rather than treating them as simple operating expenses.

IFRS 9 (Financial Instruments) applies to agencies extending payment terms to clients, requiring an Expected Credit Loss (ECL) model for receivables. This is particularly relevant in Dubai, where Days Sales Outstanding (DSO) for agency services commonly runs between 45 and 90 days.

Bookkeeping Framework and Financial Records Structure for Marketing Agencies

A compliant bookkeeping framework for a Dubai marketing agency requires more than tracking invoices and expenses. The general ledger must be structured to support VAT return preparation, corporate tax filings, and annual audit requirements simultaneously.

Core components of an agency-specific bookkeeping system:

- Chart of accounts segmented by revenue type (retainer, project, media buying), cost center (creative, digital, strategy), and overhead category (rent, payroll, software subscriptions)

- Client-level revenue tracking to support IFRS 15 obligation-by-obligation recognition and percentage-of-completion calculations

- Media spend ledger separating agency-owned spend from client pass-through costs for accurate principal vs. agent classification

- VAT sub-ledger recording output tax, input tax, and RCM entries separately for each VAT period

Supporting documentation must include signed client contracts, purchase orders, original supplier invoices (including foreign platform invoices from Google and Meta), proof of payment, and monthly bank reconciliation statements. As of January 1, 2026, the FTA tightened self-invoicing rules: agencies can no longer rely solely on internally generated RCM documents and must retain the original supplier commercial invoice alongside proof of payment.

Cloud-based platforms such as Zoho Books (UAE edition), Wafeq, and QuickBooks UAE are widely used by Dubai agencies. Software selection in 2026 should prioritize FTA e-invoicing readiness, given the mandatory rollout commencing January 2027.

Financial Statements Preparation Requirements

Dubai marketing agencies must prepare a complete set of IFRS-compliant financial statements annually. These form the basis for corporate tax filings, external audits, and free zone license renewals.

Required financial statements:

- Statement of Financial Position (Balance Sheet) — reflecting assets, liabilities, and equity at the financial year-end

- Statement of Profit or Loss and Other Comprehensive Income — reporting revenue, cost of sales, gross profit, and net profit

- Statement of Cash Flows — prepared using the indirect method, distinguishing operating, investing, and financing activities

- Statement of Changes in Equity — relevant for agencies with multiple shareholders or those distributing dividends

- Notes to the Financial Statements — including accounting policies, tax disclosures, related party transactions, and revenue recognition policies

UAE banks typically require two to three years of audited financial statements before extending credit facilities to SME agencies. Consistent IFRS-compliant reporting builds the financial credibility required to access growth financing in Dubai’s competitive agency landscape.

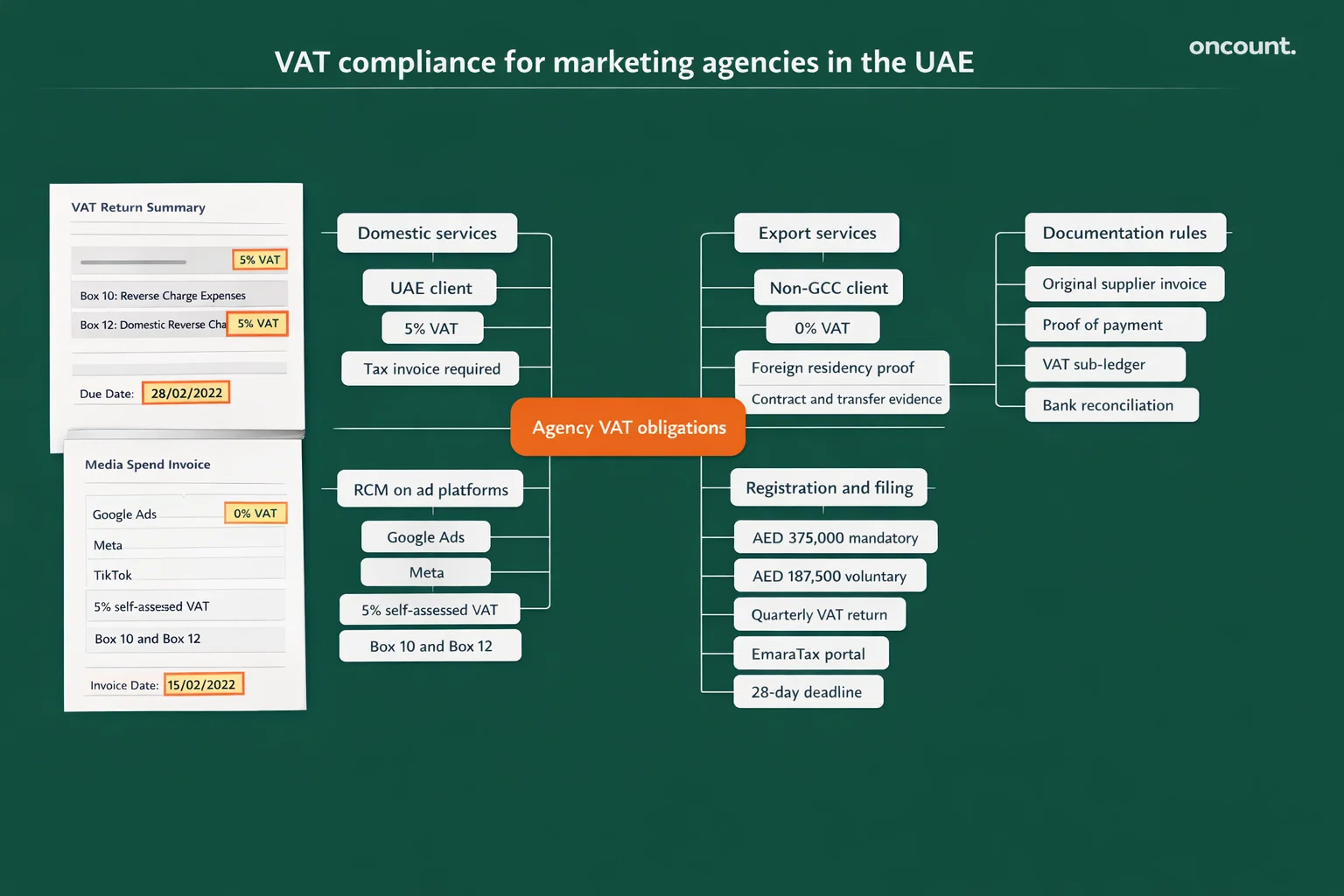

VAT Compliance for Marketing Agencies in the UAE

UAE VAT compliance for marketing agencies is governed by Federal Decree-Law No. 8 of 2017 and FTA Executive Regulations. The standard VAT rate of 5% applies to most domestic services, but agency operations frequently span multiple VAT treatments simultaneously.

| VAT Scenario | Rate | Key Condition |

| Local client services | 5% | Client is UAE-based |

| Export services to non-GCC client | 0% | No UAE presence; supported by contract and foreign transfer |

| International ad platform spend (RCM) | 5% self-assessed | Non-resident supplier; declared in Box 10 and Box 12 of VAT 201 |

| Intra-GCC services | Subject to bilateral rules | Dependent on implementing state status |

VAT registration thresholds:

- Mandatory registration: taxable supplies exceeding AED 375,000 in the prior 12 months

- Voluntary registration: available from AED 187,500

- Agencies below AED 187,500 are ineligible to register and cannot reclaim input VAT on business costs

The Reverse Charge Mechanism is the most audit-sensitive VAT area for Dubai agencies. Spend on Google Ads, Meta Business Manager, TikTok for Business, and LinkedIn Campaign Manager is invoiced without UAE VAT because these platforms are non-resident suppliers. Under FTA guidance, the registered UAE recipient must self-assess 5% VAT on the full invoice amount, declare it as output tax, and simultaneously claim it as input tax — provided the spend directly supports taxable supplies. Incomplete RCM documentation is among the leading causes of adverse FTA audit findings in the agency sector.

VAT returns are submitted quarterly through the EmaraTax portal. Late filing incurs a fixed AED 1,000 penalty for a first offense, rising to AED 2,000 for repeat non-compliance within 24 months.

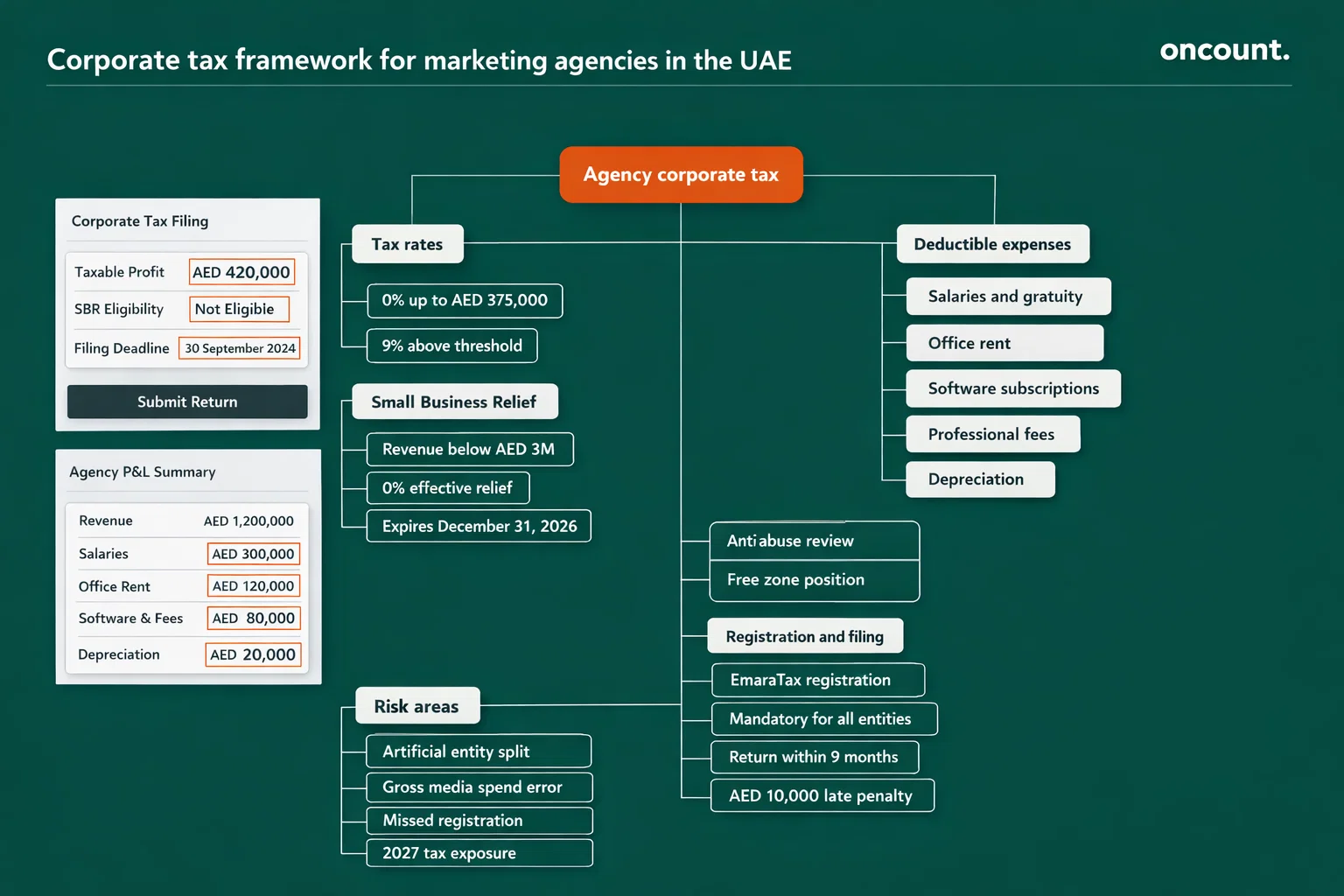

Corporate Tax Framework for Marketing Agencies in the UAE

UAE Corporate Tax is governed by Federal Decree-Law No. 47 of 2022 and applies to financial years commencing on or after June 1, 2023. Marketing agencies incorporated as LLCs or free zone entities are classified as taxable persons and are subject to CT registration and filing obligations.

| Corporate Tax Tier | Rate | Applicability |

| Exempt threshold | 0% | Taxable profits up to AED 375,000 |

| Standard rate | 9% | Taxable profits exceeding AED 375,000 |

| Small Business Relief (SBR) | 0% effective | Revenue below AED 3 million; expires December 31, 2026 |

| Qualifying Free Zone Income | 0% | Meets substance and qualifying activity conditions |

The Small Business Relief program has allowed micro-agencies to defer full CT compliance during the regime’s introductory phase. The FTA has indicated it will use Emirates ID cross-referencing and trade license data to identify artificial entity separation — where a single agency splits operations across multiple licenses to keep each below the AED 3 million threshold — which is treated as an anti-abuse arrangement.

Corporate tax registration is completed through the EmaraTax portal. The annual CT return must be filed within nine months of the financial year-end. For a calendar-year agency, the return covering the 2025 tax period is due by September 30, 2026. Late registration triggers an immediate administrative penalty of AED 10,000.

Accounting for Revenue and Expenses in Marketing Agencies

Revenue recognition is the most consequential accounting judgment for a Dubai marketing agency. Three primary revenue models require distinct IFRS 15 treatment.

Retainer agreements: Monthly fees for social media management, SEO, or paid media oversight are recognized evenly across the service period regardless of invoicing or payment timing. A retainer invoiced quarterly in advance must be deferred, with one-third recognized each month.

Project-based fees: Fees for defined deliverables — brand identity packages, campaign launches, website builds — are recognized at the point of delivery or, for multi-month projects, using the percentage-of-completion method based on costs incurred or contractual milestones achieved.

Media buying — principal vs. agent: An agency acting as an agent — one that does not bear inventory risk or set the final price of media placements — reports only its commission or markup as revenue, not the gross media spend. Reporting gross media spend as revenue when operating as an agent constitutes a material misstatement, inflates reported turnover, and can directly disqualify an agency from Small Business Relief.

Deductible expenses under UAE Corporate Tax Law include:

- Staff salaries, end-of-service gratuity provisions, and health insurance contributions

- Office rent and utilities

- Software subscriptions, including creative tools and project management platforms

- Professional fees for auditors, legal counsel, and tax advisors

- Depreciation of qualifying fixed assets under IFRS-compliant useful life schedules

Entertainment expenses and administrative penalties imposed by regulatory authorities are explicitly non-deductible under Federal Decree-Law No. 47 of 2022.

Regulatory Compliance and Reporting Obligations

Beyond direct tax obligations, Dubai marketing agencies must comply with three additional regulatory frameworks that directly affect accounting processes and documentation requirements.

- Economic Substance Regulations (ESR): Agencies providing intellectual property licensing, royalty arrangements, or holding company services must demonstrate adequate substance in the UAE. This requires being directed and managed from within the UAE, employing qualified local staff, and incurring sufficient operating expenditure domestically. Annual ESR notifications and reports must be filed with the relevant licensing authority. Non-filing incurs a minimum penalty of AED 50,000.

- Ultimate Beneficial Owner (UBO) Reporting: Under Cabinet Decision No. 58 of 2020, every UAE-registered agency must identify, verify, and maintain a register of individuals who directly or indirectly own 25% or more of the entity. This register must be submitted to the relevant authority — DED or the applicable free zone regulator — and updated within 15 days of any ownership change.

- Anti-Money Laundering (AML): Marketing agencies that receive cash payments exceeding AED 55,000 are classified as Designated Non-Financial Businesses and Professions (DNFBPs) under Federal Decree-Law No. 20 of 2018, triggering customer due diligence obligations and suspicious transaction reporting requirements to the UAE Financial Intelligence Unit (FIU).

Audit Requirements for Marketing Agencies in the UAE

External audit requirements for Dubai marketing agencies vary by jurisdiction but are universally enforced as a condition of license renewal or regulatory standing.

| Jurisdiction | Audit Requirement | Deadline | Auditor Qualification |

| Mainland (DED) | Mandatory annual | License renewal date | MoE-registered auditor |

| Dubai Media City (DDA) | Mandatory for renewal | License renewal date | DDA-approved auditor |

| DMCC | Mandatory annual | 90–180 days post FY-end | DMCC-approved list |

| DIFC | Mandatory annual | 4 months post FY-end | DFSA-registered auditor |

The FTA increasingly cross-references audit reports against VAT returns and corporate tax filings. Agencies whose audited financials reflect revenue or margin data materially inconsistent with their tax submissions are at elevated risk of a compliance review. Audit preparation is a year-round discipline, not a year-end exercise. Engaging qualified accounting and bookkeeping outsourcing professionals reduces the risk of audit qualifications and ensures documentation standards consistently meet FTA expectations.

Industry-Specific Accounting Considerations for Marketing Agencies

Revenue from Influencer and Content Creator Engagements

Agencies managing influencer marketing campaigns face a specific accounting determination: whether payments to influencers represent a cost of sale (agency bears and controls the fee) or a client disbursement (passed through at actual cost). Under IFRS 15, if the agency controls the influencer’s output and assumes the risk of non-delivery, the full fee is recognized as both revenue and cost of sales. If the agency merely facilitates the arrangement, net commission reporting applies. Misclassification is common and creates inconsistencies in gross margin reporting.

Treatment of Proprietary Digital Assets

Creative assets developed by the agency — brand identities, motion graphic templates, or proprietary workflow tools — may qualify as intangible assets under IAS 38 if they are expected to generate future economic benefits for the agency itself. Assets developed exclusively for client delivery are expensed as cost of sales upon delivery and do not appear on the agency’s balance sheet.

E-Invoicing System Integration

As of July 1, 2026, the UAE launched the voluntary pilot phase of its mandatory e-invoicing system. Marketing agencies must ensure their accounting software can generate and transmit invoices in structured XML or JSON format through an FTA-accredited portal. Failure to comply from January 2027 invalidates invoices for client VAT reclaim purposes, making the agency’s services effectively 5% more expensive to VAT-registered clients. According to UAE Ministry of Finance communications, the e-invoicing framework is designed to align the UAE with global digital taxation infrastructure under OECD standards.

Common Accounting Challenges for Marketing Agency Companies

Scope creep and revenue underreporting: Agencies that deliver services beyond contracted scope without issuing change orders or supplementary invoices systematically underreport revenue. Agencies without automated time-tracking systems capture only approximately 77% of billable hours on average, compared to around 95% for those with integrated systems — a gap that can represent AED 30,000 to AED 75,000 in unrecovered annual revenue per mid-sized account.

Incorrect principal vs. agent classification: Reporting gross media spend as revenue when acting as an agent inflates turnover materially. This can disqualify an agency from Small Business Relief eligibility and constitutes a misstatement in audited financial statements, creating direct FTA audit exposure.

RCM non-compliance on platform spend: Many smaller Dubai agencies fail to declare the Reverse Charge Mechanism on Google, Meta, and TikTok invoices. The FTA’s cross-referencing of bank statements against VAT 201 returns is increasingly capable of identifying this discrepancy. The penalty is 50% of the underpaid tax amount, reducible to 15% under a voluntary disclosure filed before an audit notice is received.

Late corporate tax registration: Registration deadlines are tied to trade license issuance dates on a rolling basis. New agencies frequently miss the window without professional guidance, incurring an immediate AED 10,000 penalty that is entirely avoidable.

Best Practices for Accounting and Financial Management in Marketing Agencies

- Implement an IFRS-aligned chart of accounts from day one — Structure the general ledger to separately track retainer revenue, project revenue, and media pass-through costs. Reclassification at year-end is costly and introduces audit risk.

- Select FTA e-invoicing-ready accounting software in 2026 — Platforms currently in certification for the UAE e-invoicing mandate include Zoho Books (UAE edition) and Wafeq. Software selection should be confirmed before the July 2026 pilot phase.

- Integrate time-tracking with billing systems — Automated time-tracking linked directly to the billing module ensures near-complete billable hour capture and supports IFRS 15 percentage-of-completion calculations on long-duration project work.

- Conduct quarterly VAT reconciliations before submission — Reconcile the VAT 201 return to the general ledger each quarter. Verify RCM entries, confirm zero-rating documentation for international clients, and flag any partially exempt supplies before filing.

- Register for Corporate Tax immediately upon license issuance — CT registration is mandatory regardless of profitability. The AED 10,000 late registration penalty is entirely avoidable with timely action through the EmaraTax portal.

- Model 2027 tax exposure during 2026 — Use the SBR transition year to calculate projected 9% corporate tax liability for 2027 and adjust client pricing structures and cost models accordingly.

- Engage a qualified auditor for year-round review — Annual audit preparation is most efficient when financial records are maintained in audit-ready condition throughout the year, rather than reconstructed after year-end.

Comparison: Free Zone vs. Mainland Accounting Requirements for Marketing Agencies

| Factor | Mainland (DED) | Dubai Media City (DDA) | DMCC | DIFC |

| Corporate Tax Rate | 9% on profits > AED 375K | 9% or 0% (qualifying) | 9% or 0% (qualifying) | 9% or 0% (qualifying) |

| Audit Requirement | Mandatory annual | Mandatory for renewal | Mandatory annual | Mandatory annual |

| Reporting Standard | IFRS | IFRS | IFRS | Full IFRS |

| Submission Deadline | License renewal date | License renewal date | 90–180 days post FY | 4 months post FY |

| UAE Market Access | Unrestricted | Sector-restricted | Sector-restricted | Sector-restricted |

| Regulatory Body | DED / MoE | DDA | DMCC Authority | DFSA / DIFC Registrar |

| Auditor Requirement | MoE-registered | DDA-approved | DMCC-approved list | DFSA-registered |

Mainland agencies operate under the most direct regulatory oversight but benefit from unrestricted access to the UAE domestic market. DIFC entities operate under a common law framework with the strictest full-IFRS application, making DIFC registration particularly suited to agencies seeking international investor credibility or cross-border financing.