Key Takeaways

- UAE SaaS companies must recognize revenue using the five-step model under IFRS 15, with deferred revenue treatment for upfront annual payments.

- UAE Corporate Tax applies at 9% on taxable profits exceeding AED 375,000, effective June 1, 2023, under Federal Decree-Law No. 47 of 2022.

- Free Zone SaaS entities can qualify for a 0% Qualifying Free Zone Person (QFZP) rate, but only if UAE-based R&D generates the software IP under the Modified Nexus Approach.

- VAT registration is mandatory once taxable supplies exceed AED 375,000 annually; non-resident SaaS providers selling to UAE individuals must register from their first transaction.

- From January 1, 2026, mandatory XML e-invoicing, a 5-year VAT credit expiry cap, and a flat 14% annualized penalty interest on unpaid tax take effect.

- DIFC and ADGM-registered SaaS companies are required to produce annual IFRS-audited financial statements regardless of revenue volume.

- Software development costs are capitalized under IAS 38 only after the project meets six specific development-phase criteria.

Overview of Accounting Requirements in the UAE for SaaS Companies

SaaS companies registered in the UAE are legally required to maintain accurate accounting records under the UAE Commercial Companies Law and Federal Tax Authority (FTA) regulations. The FTA mandates a minimum five-year record retention period for all financial documents, including contracts, invoices, bank statements, and tax filings. Failure to maintain these records exposes businesses to penalties during FTA audits, which have expanded significantly in scope following the introduction of Corporate Tax.

The UAE Ministry of Finance has confirmed that all UAE businesses, including technology and SaaS entities, must align their financial statements with International Financial Reporting Standards (IFRS). This alignment ensures that financial reporting is consistent with global investor expectations and facilitates access to international venture capital. For SaaS companies specifically, correct application of IFRS is not optional — it is a prerequisite for investment readiness and regulatory good standing. Engaging qualified accounting and bookkeeping services in UAE from the outset prevents costly restatements and audit complications later.

IFRS Application for SaaS Companies in the UAE

Revenue Recognition Under IFRS 15

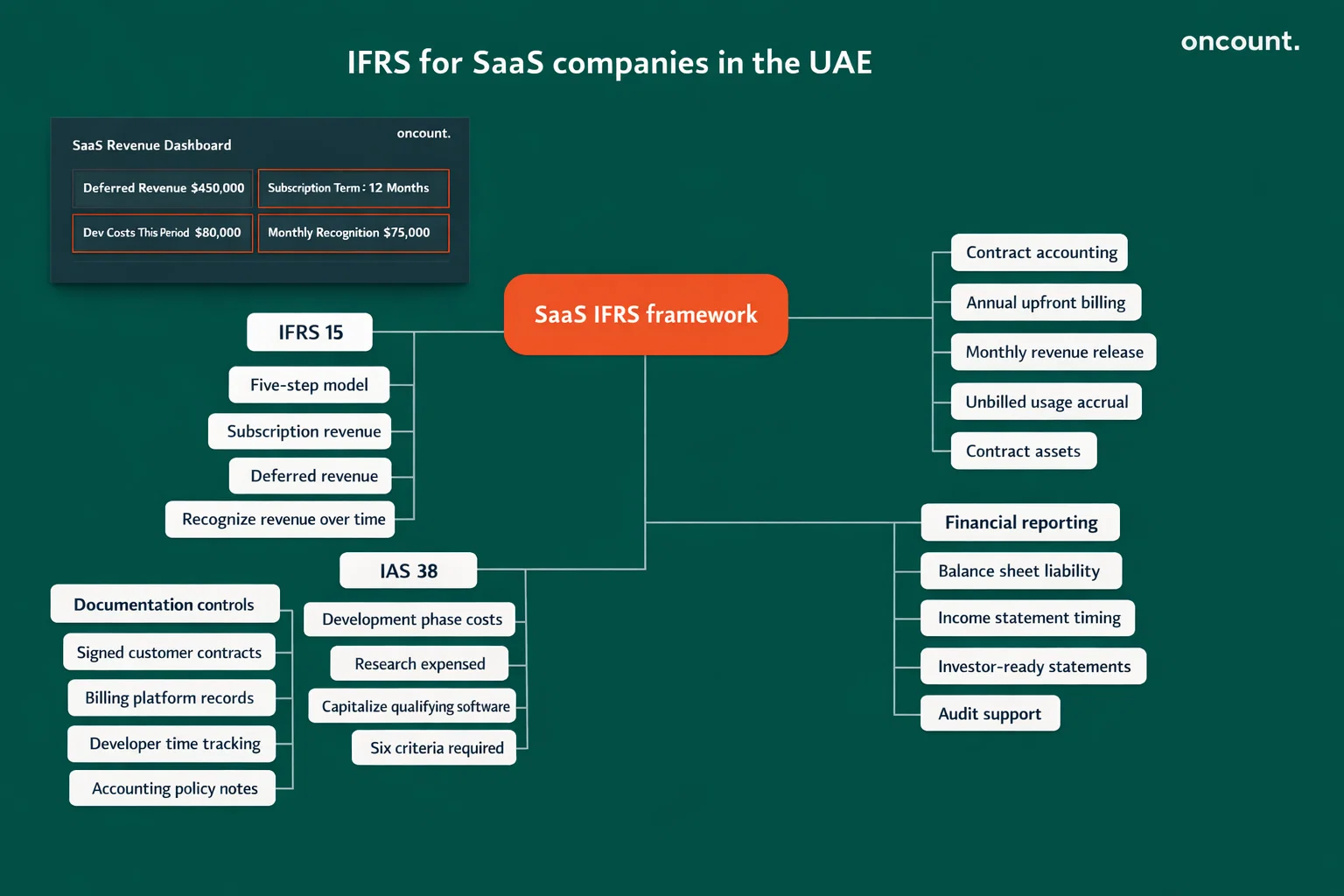

The most consequential accounting standard for any SaaS business is IFRS 15: Revenue from Contracts with Customers. This standard mandates a uniform five-step model for recognizing revenue that replaces all prior industry-specific guidance. The IFRS Foundation issued IFRS 15 to standardize how companies across all sectors — including subscription-based software providers — report when and how much revenue they earn.

The five steps are:

- Identify the contract with the customer, including its enforceability and termination rights.

- Identify distinct performance obligations, such as software access, onboarding, and support.

- Determine the transaction price, including variable components like usage fees or volume discounts.

- Allocate the transaction price across performance obligations based on standalone selling prices (SSP).

- Recognize revenue as each obligation is satisfied — for SaaS, this is almost always over time.

In practice, a UAE SaaS company that receives an AED 120,000 upfront payment for a 12-month subscription must recognize AED 10,000 per month, while the remaining balance sits on the balance sheet as Deferred Revenue — a liability, not income.

Intangible Asset Accounting Under IAS 38

IAS 38: Intangible Assets governs how SaaS companies capitalize software development costs. Expenses incurred during the research phase — such as evaluating technical alternatives or conducting market feasibility studies — must be expensed immediately. Capitalization is only permissible once the project enters the development phase and satisfies all six IAS 38 criteria, including technical feasibility, management intent to complete the asset, and the ability to demonstrate how the software will generate future economic benefits.

| Expenditure Type | Accounting Treatment | Standard |

| Initial product brainstorming | Expense as incurred | IAS 38 |

| Coding the core platform | Capitalize as intangible asset | IAS 38 |

| Security patches and bug fixes | Operational expense | IAS 38 |

| Data migration costs | Generally expensed | IAS 38 / IFRIC |

| Customer implementation (SaaS buyer) | Prepayment or expense | IFRIC guidance |

UAE auditors increasingly require SaaS companies to produce time-tracking records and sprint-level project logs to substantiate which development hours are capitalizable. Without this documentation, capitalized assets may be disallowed during FTA or external audits.

Bookkeeping Framework and Financial Records for SaaS Entities

A well-structured bookkeeping framework for a UAE SaaS company must reflect the recurring revenue model, subscription cycles, and IP-driven cost structure of the business. The general ledger should be organized with a chart of accounts that separates subscription revenue, professional services revenue, deferred revenue liabilities, capitalized software development costs, and customer acquisition expenses.

Core documentation requirements include:

- Signed subscription agreements and order forms

- Customer invoices issued via the billing platform

- Bank statements and payment reconciliation records

- Developer time-tracking reports for IAS 38 capitalization support

- Intercompany agreements if the SaaS entity is part of a group structure

Accurate bookkeeping also supports the reconciliation of SaaS-specific metrics — Monthly Recurring Revenue (MRR), Annual Recurring Revenue (ARR), and churn rates — with IFRS-audited financial statements. A material discrepancy between investor-facing metrics and audited revenue is a common cause of investor concern during due diligence processes and can directly reduce company valuation.

Financial Statements Preparation Requirements for SaaS Companies

UAE SaaS companies are required to prepare a complete set of financial statements that includes:

- Balance Sheet (Statement of Financial Position): Reflects deferred revenue liabilities, capitalized software as intangible assets, accrued income from unbilled usage fees, and contract assets.

- Profit and Loss Statement (Income Statement): Shows recognized SaaS subscription revenue separately from professional services or one-time fees.

- Cash Flow Statement: Distinguishes between cash received from customers (often front-loaded) and revenue earned (recognized over the period).

- Notes to Financial Statements: Discloses revenue recognition policies, performance obligations, and valuation methods for capitalized assets.

For DIFC and ADGM-registered SaaS companies, annual audited financial statements prepared under full IFRS are mandatory regardless of revenue size, per the respective financial center regulators. For Mainland UAE entities, the audit requirement is triggered by revenue thresholds and legal structure. A SaaS company approaching a funding round should produce IFRS-compliant audited statements proactively, as international investors view this as a baseline credibility requirement.

VAT Compliance for SaaS Companies in the UAE

Registration and Place of Supply Rules

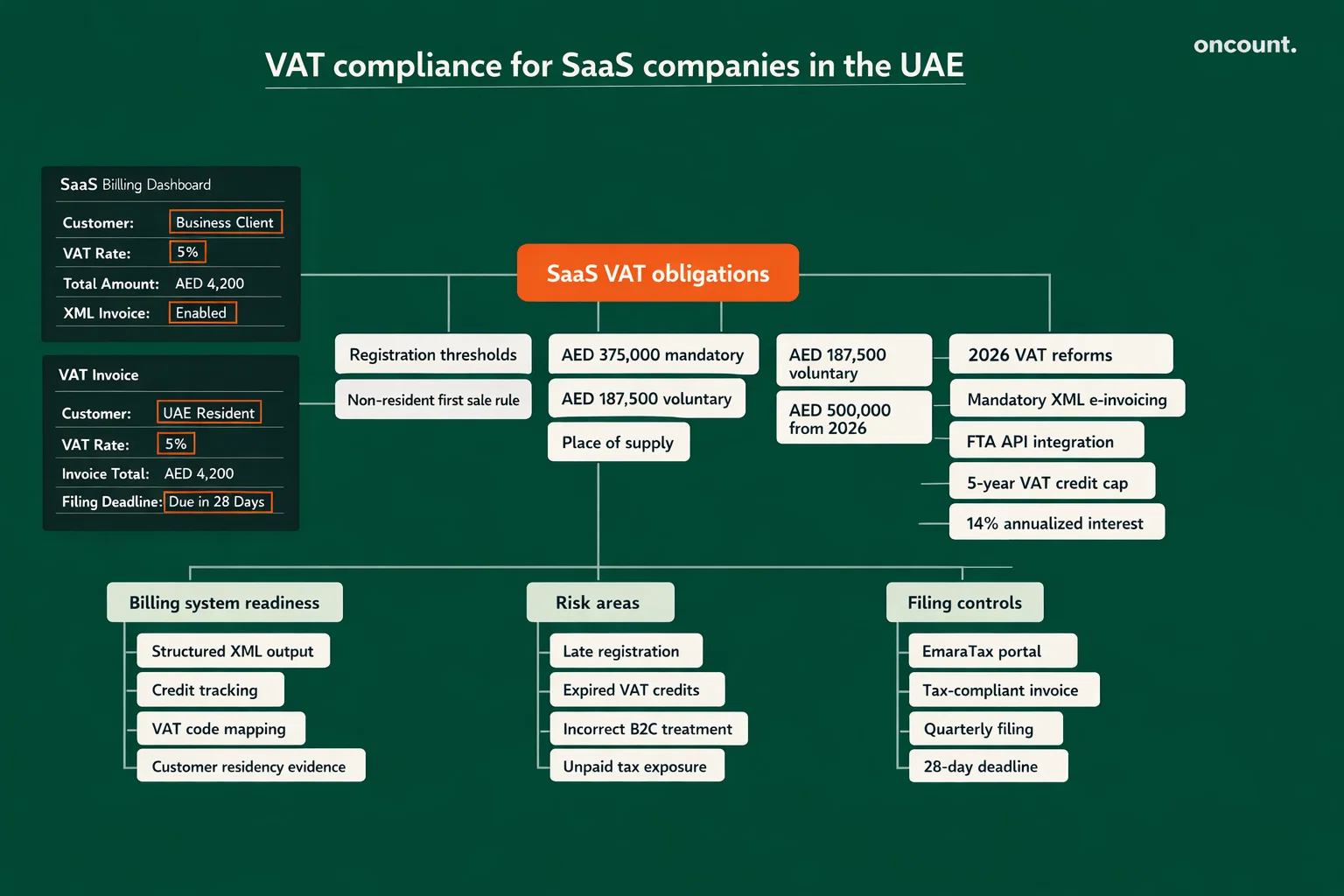

UAE VAT is governed by Federal Decree-Law No. 8 of 2017, administered by the Federal Tax Authority through the EmaraTax portal. SaaS companies must register for VAT once taxable supplies exceed AED 375,000 annually (mandatory threshold) or AED 187,500 (voluntary threshold). For digital services like SaaS, the place of supply is determined by where the service is “used and enjoyed.”

Business-to-Business (B2B) supplies: When a UAE-registered SaaS company sells to a foreign business, the supply is treated as outside the scope of UAE VAT or zero-rated, subject to documentation confirming the client’s foreign residency and business status.

Business-to-Consumer (B2C) supplies: SaaS subscriptions sold to individual UAE residents are subject to 5% VAT. Critically, non-resident SaaS providers selling to UAE individuals must register with the FTA from their very first transaction — there is no minimum threshold for non-residents under current rules.

2026 VAT Reforms Affecting SaaS Businesses

Federal Decree-Laws No. 16 and 17 of 2025 introduce three major VAT changes effective January 1, 2026 that directly affect SaaS billing operations:

| VAT Factor | Current Rule (2025) | New Rule (2026+) |

| Mandatory registration threshold | AED 375,000 | AED 500,000 |

| RCM self-invoice requirement | Mandatory | Eliminated |

| VAT credit carry-forward | Indefinite | 5-year expiry cap |

| E-invoicing format | Optional / paper | Mandatory XML via FTA API |

| Penalty interest on unpaid VAT | Tiered penalties | 14% annualized flat rate |

SaaS companies that have accumulated input VAT credits from 2021 onward face an urgent deadline. Credits older than five years will expire permanently on December 31, 2026, unless reclaimed during the transitional relief window. SaaS billing platforms must also integrate with the FTA’s e-invoicing API infrastructure to comply with mandatory structured XML invoicing requirements — large taxpayers (over AED 100 million revenue) must comply by July 1, 2026. According to FTA official guidance, all other registrants must follow by early 2027.

Corporate Tax Framework for SaaS Companies in the UAE

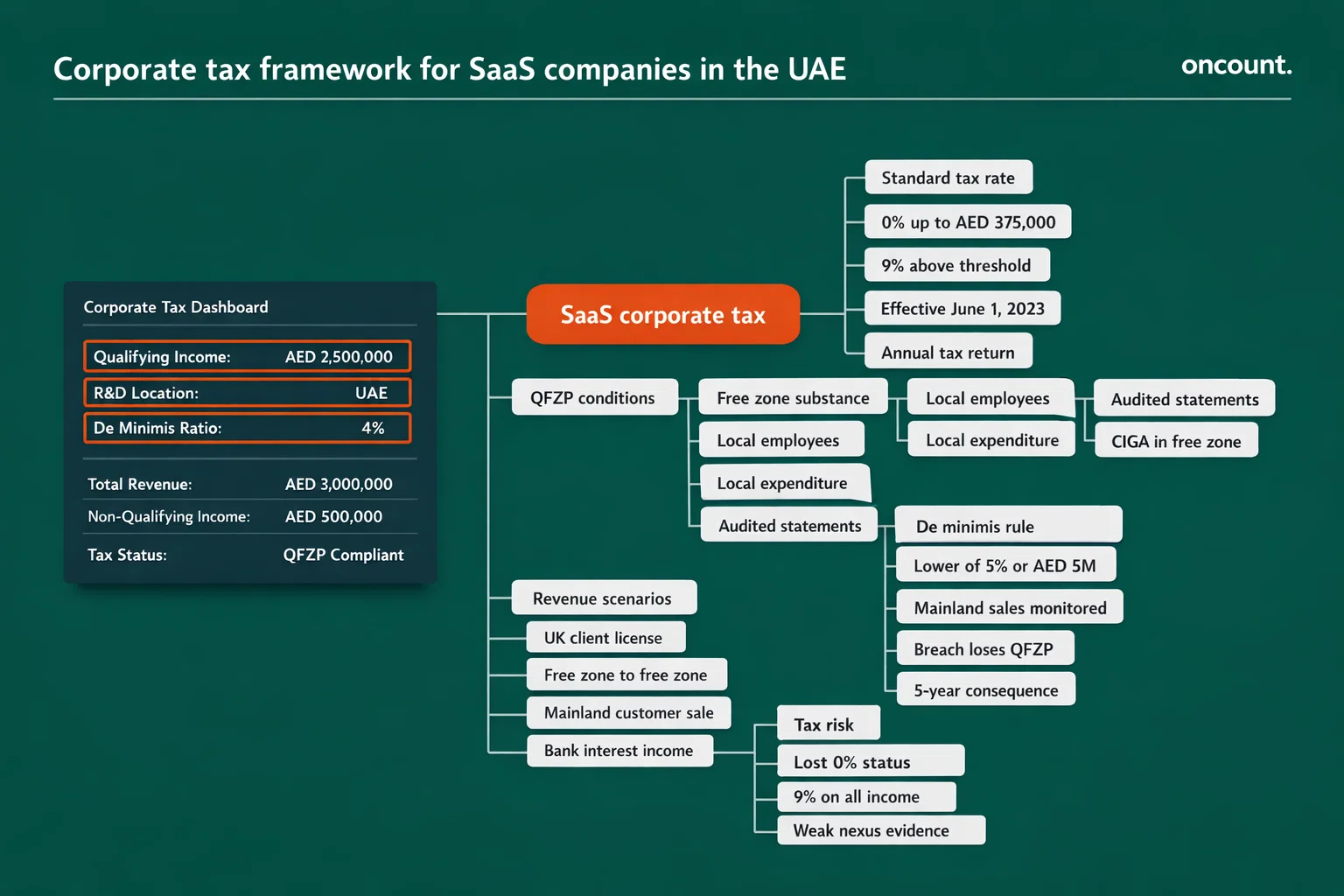

The introduction of UAE Corporate Tax under Federal Decree-Law No. 47 of 2022 fundamentally changed the financial calculus for SaaS companies in Dubai. Where the region once offered blanket tax neutrality, SaaS entities must now navigate a dual-rate structure — a standard 9% rate on profits exceeding AED 375,000 and a conditional 0% rate available exclusively to Free

Zone entities that satisfy the Qualifying Free Zone Person (QFZP) criteria. For software businesses built on IP-driven revenue and recurring subscription income, the difference between these two outcomes depends entirely on how the company is structured, where its R&D activity occurs, and how rigorously it monitors its qualifying income thresholds.

Standard Rate and Qualifying Free Zone Person Status

UAE Corporate Tax was introduced under Federal Decree-Law No. 47 of 2022, effective June 1, 2023. The standard rate is 9% on taxable profits exceeding AED 375,000, with a 0% rate applied to profits below this threshold. For SaaS companies operating in UAE Free Zones, a 0% rate on Qualifying Income is available through QFZP status — but the compliance requirements are stringent.

To qualify as a QFZP, a SaaS entity must:

- Maintain adequate substance in the Free Zone — physical office, local employees, and local operational expenditure.

- Ensure that its Core Income-Generating Activities (CIGA) are performed within the Free Zone.

- Prepare and maintain audited financial statements annually.

- Limit non-qualifying income to the De Minimis threshold: the lower of 5% of total revenue or AED 5 million.

Qualifying Income and the Modified Nexus Approach for Software IP

Cabinet Decision No. 100 of 2023 defines Qualifying Income to include revenue from “ownership or exploitation of Qualifying Intellectual Property,” specifically encompassing copyrighted software. However, the 0% benefit applies only under the Modified Nexus Approach, which links tax relief directly to R&D expenditure incurred within the UAE. A SaaS company that licenses software developed by a foreign parent company through a Dubai Free Zone entity does not automatically qualify — the IP income must be traceable to UAE-based development activity.

| Revenue Scenario | QFZP Impact | Effective Tax Rate |

| SaaS license sold to a UK company | Qualifying (global export) | 0% |

| SaaS sold to another DIFC-registered entity | Qualifying (FZ-to-FZ) | 0% |

| SaaS sold to a Dubai Mainland retailer | Non-qualifying (subject to 5% cap) | 9% |

| Interest income from UAE bank | Excluded activity | 9% |

| Breach of 5% De Minimis threshold | QFZP status lost for 5 years | 9% on ALL income |

The De Minimis threshold carries significant risk. Breaching it — even marginally — results in loss of QFZP status for the entire current tax period and the following four years, during which the company is taxed at 9% on all income and loses access to the AED 375,000 zero-rate band.

Accounting for Revenue and Expenses in SaaS Operations

Deferred Revenue and Contract Asset Management

The SaaS billing cycle creates a specific accounting pattern that must be managed carefully under IFRS. When a customer pays AED 60,000 upfront for a 12-month subscription, the full amount is initially recorded as a Deferred Revenue liability. Over the contract term, AED 5,000 per month is released to the income statement as earned revenue. This matching principle ensures that the income statement reflects economic performance, not cash flow timing.

Accrued income arises when services have been delivered but not yet invoiced — common in usage-based SaaS billing models. This amount is recorded as a current asset on the balance sheet and recognized as revenue in the corresponding period. Failure to accrue unbilled revenue leads to understated income, which affects tax calculations, investor reporting, and loan covenant compliance.

Development Cost Classification

SaaS companies typically carry significant software development expenditure. Proper classification between capitalized development costs (intangible assets under IAS 38) and operational expenses (such as maintenance and bug fixes) has direct implications for both financial reporting and corporate tax. Capitalized costs are amortized over the useful life of the asset, reducing taxable income over multiple periods rather than in a single year.

Regulatory Compliance and Reporting Obligations for SaaS Entities

Beyond tax filings, UAE SaaS companies are subject to several parallel compliance frameworks.

Economic Substance Regulations (ESR): Following the introduction of Corporate Tax, separate ESR notifications for financial years from January 1, 2023 onward are no longer required. Substance requirements — adequate staff, premises, and expenditure in the UAE — are now embedded within Corporate Tax returns and audited financials. Free Zone SaaS companies claiming 0% QFZP status must satisfy these substance tests directly within their annual tax submission.

Anti-Money Laundering (AML): SaaS companies processing recurring subscription payments, particularly those serving financial services clients, may fall within the scope of AML obligations under UAE Cabinet Decision No. 10 of 2019. Businesses in designated non-financial businesses and professions (DNFBPs) must implement customer due diligence (CDD) procedures and report suspicious transactions to the UAE Financial Intelligence Unit.

Ultimate Beneficial Owner (UBO) Reporting: Under Cabinet Decision No. 58 of 2020, all UAE-registered companies must maintain a UBO register identifying any individual who owns or controls more than 25% of the entity. This register must be filed with the relevant licensing authority and updated promptly upon any ownership change. Failure to maintain an accurate UBO register results in fines and potential license suspension.

According to UAE Ministry of Finance guidelines, all these compliance obligations intersect with financial record-keeping, meaning that accounting systems must be structured to support multi-framework reporting simultaneously.

Audit Requirements for SaaS Companies in the UAE

When Audits Are Mandatory

Audit requirements in the UAE depend on legal structure and jurisdiction:

- DIFC-registered SaaS companies: Annual IFRS audit by a DIFC-registered auditor is mandatory regardless of revenue.

- ADGM-registered companies: Same requirement as DIFC — annual audit is non-negotiable.

- Free Zone companies (e.g., DMCC, DIC): Annual audited financial statements are required for license renewal and are a prerequisite for QFZP status under Corporate Tax.

- Mainland UAE companies: Audit obligations are tied to legal form; LLCs with certain revenue thresholds or investor reporting requirements are typically subject to audit.

The FTA’s expanded audit powers effective in 2026 mean that SaaS companies should treat their financial statements as audit-ready at all times. The FTA can now issue binding directions on specific tax treatments, including the classification of software IP income under the Modified Nexus Approach. Companies that have relied on informal interpretations without documented positions face heightened risk.

Industry-Specific Accounting Considerations for SaaS Businesses

Bundled Contracts and Performance Obligation Separation

Enterprise SaaS contracts frequently bundle software access, implementation services, custom development, and ongoing support into a single price. Under IFRS 15, each component must be assessed for “distinctness.” If the implementation service is so specialized that it cannot function independently of the software platform, it is not a separate performance obligation and must be combined with the subscription for revenue recognition purposes. This results in a longer recognition period and a larger deferred revenue balance.

Variable Consideration and Usage-Based Pricing

SaaS pricing models increasingly include usage-based or consumption-based components alongside fixed subscriptions. The FTA and IFRS require that variable consideration be estimated using either the expected value method or the most likely amount method, but only recognized to the extent that a significant revenue reversal is not probable. For SaaS companies with high usage volatility, this creates a judgment-intensive accounting process that must be documented and consistently applied.

Software IP and Transfer Pricing

SaaS groups with entities across multiple jurisdictions — a common structure for UAE Free Zone companies with offshore parents — must maintain transfer pricing documentation compliant with OECD guidelines, as adopted within UAE Corporate Tax regulations. Royalty payments for software licenses between related parties must reflect arm’s-length pricing. Under-priced royalties flowing to a UAE entity reduce its taxable base; over-priced royalties increase costs without economic substance, potentially triggering FTA scrutiny.

Common Accounting Challenges for SaaS Companies in Dubai

SaaS companies in Dubai frequently encounter the following accounting issues:

- Incorrect deferred revenue treatment: Recording upfront subscription payments as immediate revenue inflates reported income and creates a VAT and Corporate Tax exposure.

- Failure to separate performance obligations: Bundling implementation fees with subscription revenue without proper IFRS 15 analysis leads to misaligned recognition timing.

- IAS 38 capitalization errors: Capitalizing maintenance and bug-fix costs that should be expensed, or failing to capitalize development costs that qualify, distorts both the balance sheet and tax position.

- De Minimis threshold breach: Selling to UAE Mainland customers without monitoring the 5% revenue cap results in unintended loss of QFZP status and a five-year tax cost.

- VAT credit expiry (from 2026): SaaS startups that carried forward input VAT credits without claiming refunds face permanent loss of credits older than five years starting December 31, 2026.

- Pitch deck vs. audited ARR discrepancy: Presenting ARR metrics to investors that cannot be reconciled with IFRS-audited revenue causes due diligence failures and valuation reductions.

Best Practices for Accounting and Financial Management in SaaS

- Implement a SaaS-specific chart of accounts that separates deferred revenue, contract assets, capitalized software development costs, and MRR-derived income at the account level.

- Deploy cloud accounting software — such as Xero, QuickBooks, or NetSuite — integrated with your subscription billing platform to automate deferred revenue schedules and invoice generation.

- Maintain sprint-level time-tracking records for all developers to substantiate IAS 38 capitalization decisions with granular evidence acceptable to FTA auditors.

- Monitor De Minimis revenue monthly if operating as a QFZP. Establish internal alerts when non-qualifying income approaches 3% of total revenue to allow proactive restructuring.

- Prepare for e-invoicing compliance by auditing your billing platform’s API capabilities before the 2026 FTA mandatory XML e-invoicing deadline.

- Engage registered auditors early in the financial year, particularly for DIFC or Free Zone entities where audit reports are required for both license renewal and QFZP tax status confirmation.

Comparison: Free Zone vs. Mainland Accounting Requirements for SaaS

| Feature | Dubai Mainland | Dubai Internet City (DIC) | DIFC / ADGM |

| Legal framework | UAE Civil Law | UAE Civil Law | English Common Law |

| Corporate tax rate | 9% (>AED 375,000) | 0% if QFZP | 0% if QFZP |

| Audit requirement | Revenue-dependent | Mandatory (license renewal) | Mandatory (annual) |

| IFRS reporting | Required | Required | Full IFRS required |

| Investor preference | Moderate | High (operational) | Very High (legal certainty) |

| UBO registration | Mandatory | Mandatory | Mandatory |

| E-invoicing (2026) | Mandatory | Mandatory | Mandatory |

| Bank account access | High (local banks) | Moderate | High (global banks) |

For SaaS companies planning a future exit or Series A raise, DIFC-registered entities consistently achieve higher valuations — estimated 2–3x premium over Mainland structures — due to the English common law judicial framework and established shareholder protections valued by international institutional investors. The operational trade-off is a higher setup cost and non-negotiable annual IFRS audit obligation, which is best managed through dedicated accounting and bookkeeping outsourcing from a firm with Free Zone regulatory experience.