Key Takeaways

- Healthcare services delivered by licensed providers to patients are zero-rated for VAT under Federal Decree-Law No. 8 of 2017

- UAE Corporate Tax applies at 9% on taxable profits exceeding AED 375,000, with a 0% rate below that threshold

- Medical clinics must maintain financial records in accordance with IFRS and retain documentation for a minimum of five years

- Emirati employees are subject to GPSSA pension contributions (15% employer, 11% employee); expatriate staff require mandatory employer-funded health insurance

- Free zone clinics may qualify for 0% corporate tax under the Qualifying Free Zone Person framework

- VAT returns are due 28 days after the close of each tax period, typically quarterly

- Corporate tax returns must be filed within nine months of the fiscal year-end

Overview of Accounting Requirements for Medical Clinics in the UAE

Medical clinics operating in the UAE — whether mainland LLCs, sole establishments, or free zone entities — are legally required to maintain accurate financial records under UAE Federal Law No. 2 of 2015 (Commercial Companies Law) and FTA regulations. These records must reflect all revenues, expenses, assets, and liabilities using accrual-basis accounting consistent with International Financial Reporting Standards.

The UAE Federal Tax Authority mandates that all VAT-registered businesses, including healthcare providers, retain supporting documentation — invoices, contracts, receipts, and account statements — for a minimum of five years. For medical clinics, this includes patient billing records, insurance claim submissions, supplier invoices, and payroll documentation.

Clinics licensed by the Dubai Health Authority (DHA), Abu Dhabi Department of Health (DOH), or the Ministry of Health and Prevention (MOHAP) must also maintain financial records that may be reviewed during licensing renewals or regulatory audits. Health authorities in the UAE increasingly require evidence of financial viability as part of facility accreditation.

A practical point: a multi-specialty clinic in Dubai operating as a mainland LLC must prepare annual audited financial statements, register for corporate tax via the EmaraTax portal, and file quarterly VAT returns — all simultaneously. This layered obligation makes structured accounting essential, not optional.

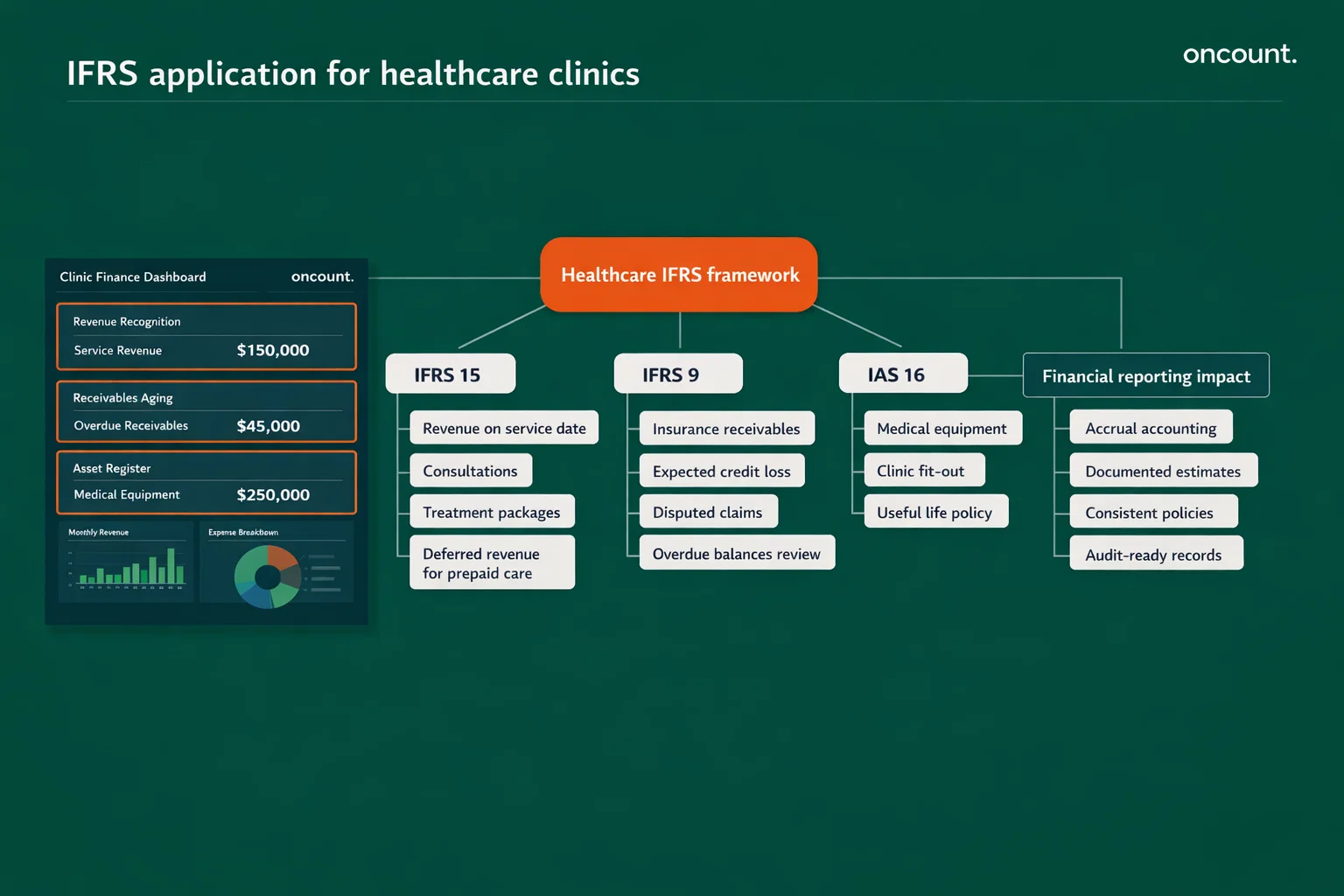

IFRS Application for Healthcare Clinics

International Financial Reporting Standards govern how UAE medical clinics recognize revenue, account for assets, and report financial performance. The three standards most directly relevant to healthcare operations are IFRS 15, IFRS 9, and IAS 16.

IFRS 15 — Revenue from Contracts with Customers requires clinics to recognize revenue when a performance obligation is satisfied — that is, when medical services are actually delivered to the patient. For a standard outpatient consultation, revenue is recognized on the day of treatment. For multi-session treatment programs or surgical packages, revenue may be allocated across individual components of the service.

IFRS 9 — Financial Instruments governs how clinics account for receivables. Because insurance claim settlements often lag by 30 to 90 days, clinics must apply the expected credit loss (ECL) model to assess collectability. Disputed or overdue claims from insurers require specific provisioning under IFRS 9.

IAS 16 — Property, Plant and Equipment applies to significant capital assets such as diagnostic imaging equipment, surgical tools, and clinic fit-outs. Useful life estimates — typically 7 to 10 years for advanced diagnostics equipment and 3 to 5 years for smaller devices — must be documented and applied consistently. Depreciation expense computed under IAS 16 is fully deductible under the UAE Corporate Tax Law, per Ministry of Finance guidance.

Bookkeeping Framework and Financial Records for Medical Practices

A well-structured chart of accounts is the foundation of accurate bookkeeping for any medical clinic. The chart of accounts should segment income and expenses by clinical function to support both regulatory reporting and internal management decisions.

Recommended account structure for UAE medical clinics:

| Account Range | Category | Examples |

| 1000–1999 | Current Assets | Cash, bank, insurance receivables, patient receivables |

| 2000–2999 | Non-Current Assets | Medical equipment, leasehold improvements, intangibles |

| 3000–3999 | Liabilities | Trade payables, accrued salaries, VAT payable, deferred revenue |

| 4000–4999 | Equity | Share capital, retained earnings |

| 5000–5999 | Clinical Revenue | Consultation fees, procedure fees, lab revenue, pharmacy sales |

| 6000–6999 | Cost of Services | Drug costs, lab consumables, and clinical staff salaries |

| 7000–7999 | Operating Expenses | Rent, admin salaries, depreciation, professional fees |

Supporting documentation requirements include:

- Numbered patient invoices or insurance claim submissions for every service rendered

- Supplier invoices matched to purchase orders and delivery receipts

- Monthly payroll registers with WPS payment confirmation

- Bank reconciliations are prepared no less than monthly

- Fixed asset register updated on acquisition or disposal

Financial Statements Preparation for Healthcare Providers

UAE medical clinics are required to prepare annual financial statements in accordance with IFRS. For mainland companies, these statements must be audited by a UAE-licensed external auditor. Free zone entities are subject to the audit requirements of their respective free zone authority, which in most cases also mandates annual audited accounts.

The standard set of financial statements for a UAE medical clinic includes:

- Statement of Financial Position (Balance Sheet) — detailing current assets (cash, receivables, inventory), non-current assets (medical equipment, leasehold), current liabilities (trade payables, accruals, VAT payable), and equity

- Statement of Profit or Loss — segregating clinical revenue by service line, cost of services, gross profit, operating expenses, and net profit

- Statement of Cash Flows — distinguishing operating, investing, and financing activities

- Notes to the Financial Statements — covering accounting policies, PPE schedules, related-party disclosures, and contingent liabilities

A multi-step profit and loss format is strongly recommended for clinics. Separating consultation revenue from laboratory, pharmacy, and ancillary income provides management with the data needed to assess profitability by service line — a critical input for pricing decisions and cost control.

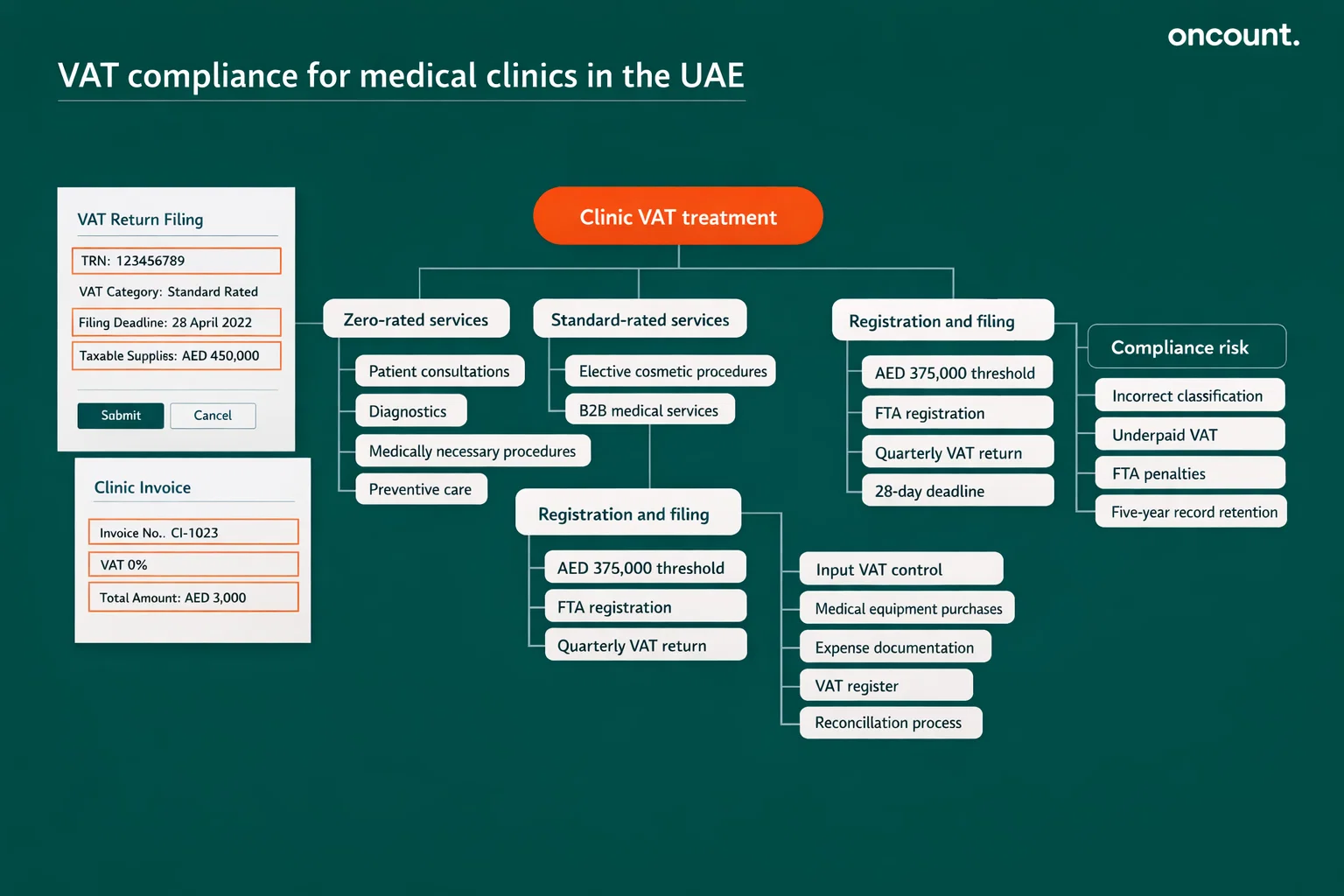

VAT Compliance for Medical Clinics in the UAE

VAT treatment is one of the most operationally significant compliance areas for healthcare providers. Federal Decree-Law No. 8 of 2017 and its Executive Regulation (Article 41) establish that healthcare services provided by licensed practitioners directly to patients for preventive or curative purposes are zero-rated at 0%.

This zero-rating applies specifically when:

- The provider holds a valid license from MOHAP, DHA, DOH, or an equivalent competent authority

- The service directly relates to human health

- The patient is the contractual recipient of the service

VAT treatment summary for common clinic scenarios:

| Supply Type | VAT Rate | Basis |

| Patient consultation and treatment | 0% | Licensed provider, direct patient care |

| Diagnostic lab tests and imaging | 0% | Part of the patient treatment pathway |

| Medically necessary surgery | 0% | As above |

| Vaccinations and preventive care | 0% | Included in the “preventive healthcare” definition |

| Elective cosmetic procedures | 5% | Not medically necessary |

| Medications on the Cabinet-approved list | 0% | Cabinet Decision on Pharmaceutical Zero-Rating |

| B2B medical services (clinic to clinic) | 5% | Patient is not the contractual recipient |

| Medical equipment purchased by the clinic | 5% | Unless Cabinet-specified for zero-rating |

VAT registration is mandatory when taxable supplies exceed AED 375,000 annually. Clinics whose supplies are entirely zero-rated may apply to the Federal Tax Authority for an exception from mandatory registration. VAT returns are filed quarterly in most cases, with payment due 28 days after the close of each tax period — for example, a Q4 return covering October through December must be submitted and paid by January 28.

Clinics should maintain a dedicated VAT register reconciling output tax on taxable supplies against input tax on business expenses. Bad debt relief provisions allow recovery of VAT on zero-rated supplies where associated receivables have been written off after six months of default.

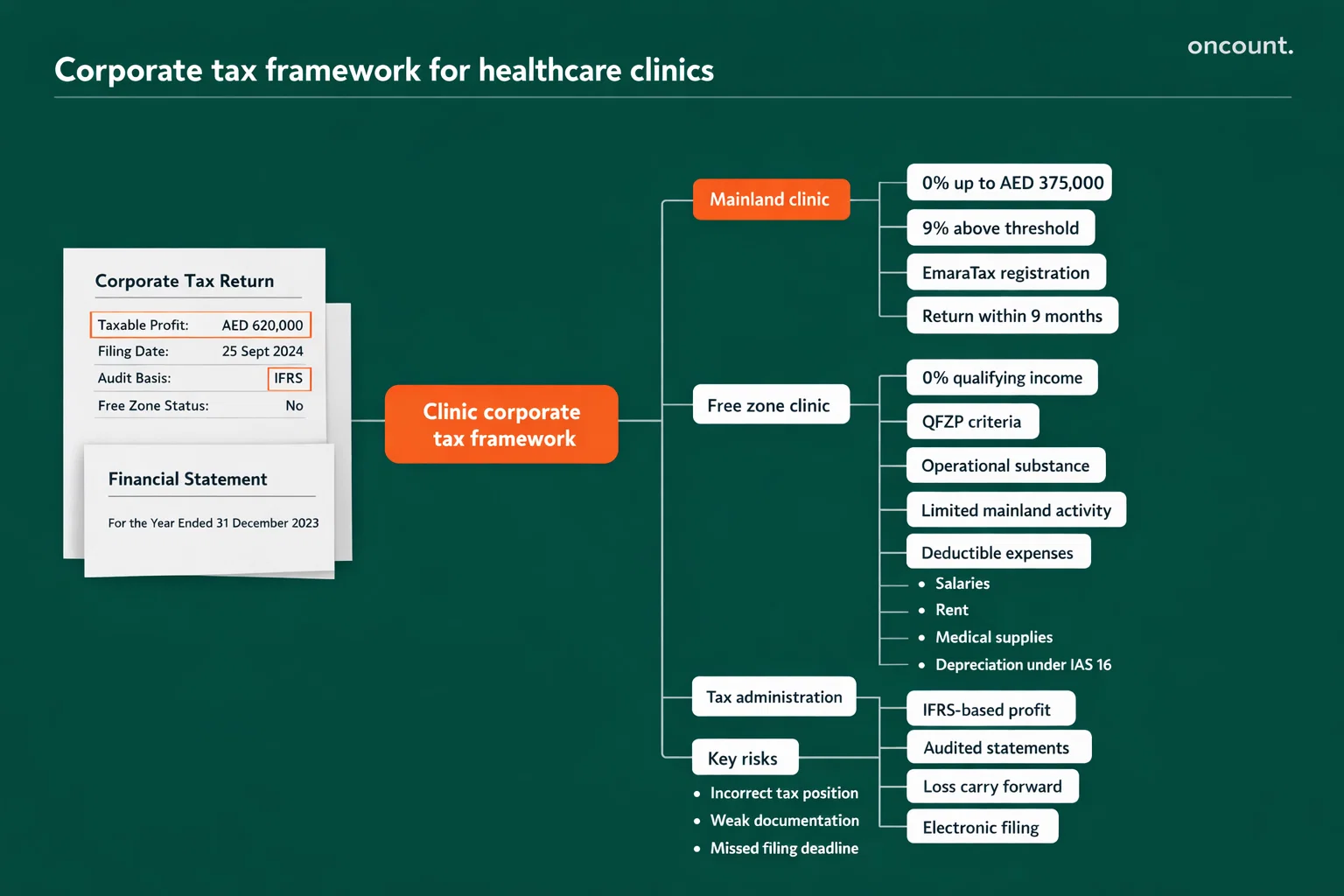

Corporate Tax Framework for Healthcare Clinics in the UAE

UAE Corporate Tax (CT), introduced under Federal Decree-Law No. 47 of 2022, applies to financial years beginning on or after June 1, 2023. All medical clinics registered as corporate entities — including mainland LLCs and free zone companies engaging in patient care — are classified as Taxable Persons under this legislation.

Corporate tax rate structure:

| Taxable Profit (AED) | CT Rate | Notes |

| 0 to 375,000 | 0% | Small business relief threshold |

| Above 375,000 | 9% | Standard rate on excess profit |

| Qualifying free zone income | 0% | Subject to Qualifying Free Zone Person criteria |

Taxable income is calculated from IFRS-based accounting profits, with adjustments for non-deductible items. Medical equipment depreciation computed under IAS 16 is fully deductible. Salary expenses, rent, medical supplies, and professional fees are deductible when incurred wholly and exclusively for business purposes.

According to the UAE Ministry of Finance Corporate Tax Guide (2023), businesses must maintain audited financial statements as the basis for tax computation. Tax losses may be carried forward for up to five years and applied against up to 70% of taxable income in any single year.

Corporate tax returns must be filed electronically through the EmaraTax platform within nine months of the fiscal year-end. A clinic with a December 31 fiscal year-end must file its FY2024 return by September 30, 2025.

Free zone clinics should assess their eligibility for 0% corporate tax under the Qualifying Free Zone Person rules — this requires genuine free zone operational substance, appropriate licensing, and compliance with the relevant ministerial decisions issued by the Ministry of Finance.

Accounting for Clinical Revenue and Operating Expenses

Revenue in a UAE medical clinic flows from multiple streams: direct patient fees, insurance reimbursements, government health scheme settlements (Thiqa, Saada), and ancillary services such as pharmacy dispensing and diagnostics. Each stream has different collection cycles, contractual terms, and recognition implications under IFRS 15.

Revenue recognition approach by stream:

- Self-pay consultations: Revenue and receivable recognized on the date of service delivery

- Insurance claims: Revenue recognized at the time of service; receivable tracked separately under “Accounts Receivable — Insurers” with ECL provisioning applied under IFRS 9

- Government health schemes: Revenue recognized on service date; subject to periodic reconciliation with scheme administrators

- Prepaid health packages: Revenue deferred and recognized as individual services are delivered

Operating expenses in healthcare tend to concentrate in three areas: clinical staffing (typically 40–55% of revenue), medical consumables and pharmaceuticals (10–20%), and occupancy costs (10–15%). Clinics should implement department-level cost centers — at a minimum, separating outpatient, diagnostics, pharmacy, and administration — to enable meaningful profitability analysis by service line.

Regulatory Compliance and Reporting Obligations for Healthcare Businesses

Beyond taxation, UAE medical clinics are subject to several compliance frameworks that directly affect financial operations and documentation requirements.

Economic Substance Regulations (ESR): Clinics providing services to related parties in other jurisdictions may fall within ESR scope. ESR requires demonstrating genuine operational activity in the UAE — relevant for clinic groups with cross-border structures.

Anti-Money Laundering (AML): Clinics handling high-value cash transactions or operating in contexts where large payments are made must maintain AML policies in accordance with UAE Federal Decree-Law No. 20 of 2018. This includes customer due diligence procedures and suspicious transaction reporting to the UAE Financial Intelligence Unit.

Ultimate Beneficial Owner (UBO) Register: All UAE companies, including medical clinics, must maintain a UBO register identifying individuals who ultimately own or control 25% or more of the entity. This register must be filed with the relevant authority (DED for mainland, free zone authority for free zone entities) and updated within 15 days of any change in ownership.

Wage Protection System (WPS): The UAE Ministry of Human Resources and Emiratisation mandates that all private-sector employers pay salaries electronically through WPS-compliant channels on a monthly basis. Non-compliance can result in suspension of new work permits and financial penalties.

Audit Requirements for Medical Clinics in the UAE

Annual audits are mandatory for most UAE medical clinics. Mainland companies incorporated under the Commercial Companies Law must appoint a UAE-licensed external auditor to audit annual financial statements. Most free zone authorities — including DHCC (Dubai Healthcare City), Dubai Silicon Oasis, and Abu Dhabi’s KIZAD — similarly require audited accounts as a condition of license renewal.

Auditors examining healthcare providers focus on the following high-risk areas:

- Revenue completeness: Testing that all treatments delivered are billed and recorded, with particular attention to insurance claim populations

- Receivables valuation: Assessing adequacy of IFRS 9 ECL provisions on outstanding insurer and patient balances

- VAT compliance: Verifying that zero-rating has been applied correctly and that compliant tax invoices have been issued for all supplies

- Payroll and contributions: Confirming WPS compliance, GPSSA enrollment for Emirati staff, and health insurance coverage for expatriate employees

- PPE and depreciation: Verifying asset existence, cost, and consistent application of useful life estimates

Clinics in Dubai Healthcare City (DHCC) are subject to the DHCC Authority’s specific licensing and compliance framework, which may require additional financial disclosures alongside the standard audit.

Industry-Specific Accounting Considerations for Healthcare Providers

Insurance Billing and Claim Reconciliation

Clinic accounting must accommodate the structural lag between service delivery and insurer payment. A claims aging schedule — segregating outstanding balances by insurer, claim date, and days outstanding — is essential. Claims unpaid beyond 90 days require individual assessment; those beyond 180 days should typically be provisioned or written off in accordance with IFRS 9.

Pharmaceutical and Supply Inventory

Clinics operating in-house pharmacies must apply IAS 2 (Inventories) to value pharmaceutical stock on a weighted average or FIFO basis. Regular physical stock counts — at minimum quarterly — are necessary to identify shrinkage, expiry write-offs, and discrepancies between dispensing records and inventory balances.

Medical Equipment Capitalization and Depreciation

A formal capitalization policy should define the threshold above which expenditure is treated as a non-current asset (commonly AED 5,000). Diagnostic imaging equipment (MRI, CT scanners) typically carries a useful life of 7 to 10 years; smaller clinical devices are depreciated over 3 to 5 years. All depreciation entries must be supported by an updated fixed asset register.

Emirati Staffing Costs

Clinics employing UAE nationals must register those employees with the General Pension and Social Security Authority (GPSSA). The employer contribution rate is 15% of pensionable salary; the employee contribution is 11%. A government subsidy of 2.5% applies for Emirati private-sector employees earning below AED 20,000 per month. These contributions must be remitted monthly through the GPSSA portal and recorded as a separate payroll liability in the general ledger.

Common Accounting Challenges for Medical Clinics

Insurance claim disputes and delayed settlements represent the most common revenue management challenge. Clinics that fail to track denied claims systematically often overstate receivables and understate bad debt provisions, leading to distorted profit figures.

Incorrect VAT classification of cosmetic versus medically necessary procedures creates significant compliance risk. A UAE clinic that zero-rates elective aesthetic treatments — which are standard-rated at 5% — may face FTA assessments, penalties, and interest on underpaid VAT. Clear written policies for VAT classification, reviewed against FTA guidance, are essential.

Payroll complexity increases proportionally with clinic size. Multi-nationality workforces, variable commission structures for consultants, and end-of-service gratuity accruals all require careful accounting treatment. Gratuity obligations under UAE Labor Law accumulate at 21 days’ pay per year for the first five years and 30 days per year thereafter — accruals must be maintained monthly and disclosed in financial statements.

Weak internal controls over pharmaceutical inventory expose clinics to stock losses, expired medication write-offs, and potential regulatory non-compliance. Clinics should implement segregation of duties between procurement, dispensing, and financial recording functions.

Best Practices for Accounting and Financial Management in Clinics

Implementing structured financial management practices reduces compliance risk and improves operational visibility. The following are recommended for UAE healthcare providers:

- Deploy a healthcare-compatible accounting system (e.g., Xero, QuickBooks, or an ERP with medical billing integration) that supports VAT reporting, cost center tracking, and insurance claim management

- Prepare a month-end closing checklist covering: bank reconciliations, depreciation postings, payroll accruals, GPSSA remittance verification, VAT calculation, insurance receivables aging, and inventory reconciliation

- Engage a UAE-licensed external auditor early in the financial year to identify compliance gaps before the audit cycle

- Establish written accounting policies covering revenue recognition thresholds, capitalization limits, provisioning methodology, and VAT classification criteria

- Train billing staff on correct ICD coding and insurer-specific claim submission requirements to minimize rejection rates

Comparison: Free Zone vs. Mainland Accounting for Medical Clinics

| Criteria | Mainland Clinic | Free Zone Clinic |

| Corporate Tax Rate | 9% above AED 375,000 | 0% if Qualifying Free Zone Person |

| Audit Requirement | Mandatory (UAE-licensed auditor) | Mandatory (free zone authority auditor) |

| VAT Registration | FTA, EmaraTax portal | FTA, EmaraTax portal (same rules) |

| GPSSA (Emirati Staff) | Applicable | Applicable |

| Health Insurance (Expats) | Mandatory from 2025 | Mandatory from 2025 |

| UBO Register | DED filing | Free zone authority filing |

| ESR Applicability | Depends on activity | More commonly applicable |

| Mainland Patient Access | Unrestricted | May require dual licensing |

In practice, free zone entities often benefit from the 0% corporate tax rate but must demonstrate genuine operational substance within the free zone. The UAE Ministry of Finance has issued detailed guidance on qualifying income and substance requirements under the free zone regime.