What Is the UAE e-Invoicing System and Why It Matters

The UAE Federal Tax Authority (FTA) and the UAE Ministry of Finance have jointly introduced a Decentralized Continuous Transaction Control and Exchange (DCTCE) model for e-invoicing. Under this model, every B2B and B2G invoice must be generated in a machine-readable XML format, validated by an Accredited Service Provider (ASP), and simultaneously reported to the FTA through a structured Tax Data Document (TDD).

The legal foundation of the UAE e-invoicing regime rests on several interconnected instruments:

- Federal Decree-Law No. 8/2017 (UAE VAT Law), as amended by Decree-Law 16/2024

- Ministerial Decision No. 243/2025, which defines scope, obligations, and technical standards

- Cabinet Decision No. 106/2025, which specifies the penalty framework for violations

- UAE Ministry of Finance e-Invoicing Guidelines v1.0, published February 23, 2026

The FTA’s primary objectives include reducing VAT leakage, improving real-time audit capability, and accelerating digital transformation across the UAE tax administration system. According to the UAE Ministry of Finance, the e-invoicing mandate is expected to significantly improve transparency in supply-chain transactions and reduce the administrative burden of manual VAT reconciliation.

For CFOs and financial managers, this means the e-invoicing rollout is not simply an IT project — it requires coordinated action across finance, tax, legal, procurement, and technology departments.

UAE e-Invoicing Timeline: Deadlines by Business Category

The UAE Ministry of Finance has structured the rollout in three mandatory phases following an initial voluntary pilot. Missing any deadline exposes businesses to fines under Cabinet Decision No. 106/2025.

| Phase | Business Category | ASP Appointment Deadline | Mandatory Go-Live Date |

| Pilot | Invited volunteers | N/A | July 1, 2026 |

| Phase 1 | Large taxpayers (turnover ≥ AED 50M) | July 31, 2026 | January 1, 2027 |

| Phase 2 | SMEs (turnover < AED 50M) | March 31, 2027 | July 1, 2027 |

| Phase 3 | Federal government entities | March 31, 2027 | October 1, 2027 |

Phase 1 — Large Businesses (from January 1, 2027)

Companies with an annual turnover of AED 50 million or more face the earliest mandatory compliance date. These businesses must appoint an ASP by July 31, 2026 — a deadline that is only months away. Given that ASP onboarding, ERP integration, and end-to-end testing typically require a minimum of three to six months, large enterprises should treat the ASP appointment deadline as an activation trigger for their full compliance project, not just an administrative formality.

Phase 2 — SMEs and Smaller Businesses (from July 1, 2027)

Businesses below the AED 50 million annual turnover threshold must appoint their ASP by March 31, 2027 and be fully operational by July 1, 2027. While this timeline may appear more relaxed, smaller businesses often lack dedicated IT resources, making early engagement with an ASP essential. Many ASPs offer plug-and-play integration modules compatible with popular accounting software, which can reduce implementation time considerably.

Phase 3 — Federal Entities (from October 1, 2027)

Federal government entities share the same ASP appointment deadline as SMEs (March 31, 2027) but receive an additional quarter to complete full implementation, with a go-live date of October 1, 2027.

Businesses that voluntarily join the pilot phase beginning July 1, 2026, are exempt from penalties during the pilot period. FTA guidance confirms that early adopters will not face enforcement action until their respective mandatory compliance dates.

UAE e-Invoicing Requirements: What Every Business Must Do

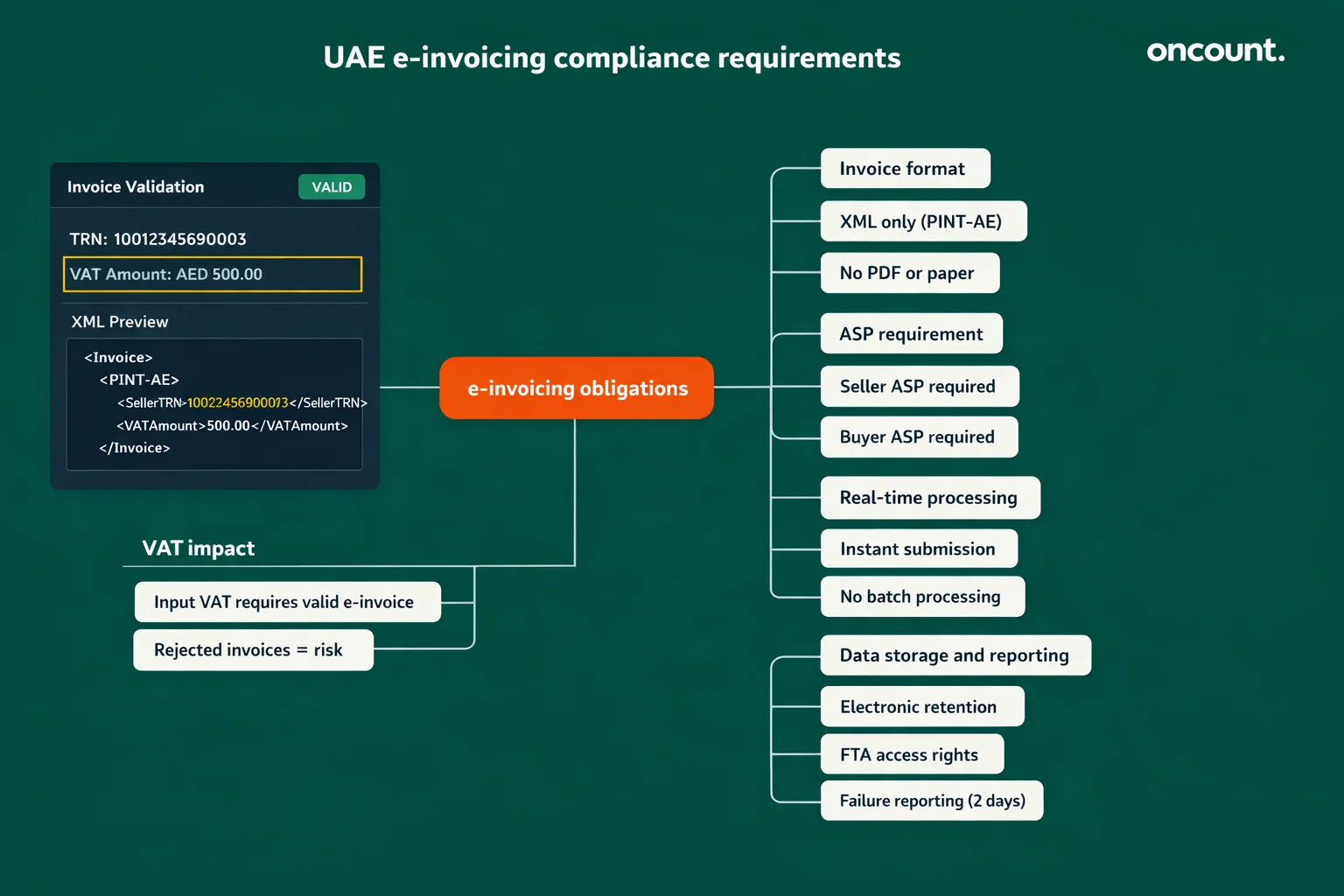

Under Ministerial Decision No. 243/2025, the UAE e-invoicing obligations apply to any person conducting business in the UAE for all B2B and B2G transactions. Business-to-consumer (B2C) invoicing is currently excluded from the mandate. The following obligations apply universally within scope:

- Issue invoices in XML format only All tax invoices and credit notes must be generated in the Peppol PINT-AE XML schema. PDF invoices, paper documents, and unstructured digital files do not satisfy the legal requirement, regardless of how they were previously accepted.

- Appoint an Accredited Service Provider Both the issuing party (seller) and the receiving party (buyer) must independently appoint an ASP accredited by the UAE Ministry of Finance. Businesses cannot transmit invoices directly to the FTA or to trading partners without routing through a certified ASP.

- Transmit invoices in real time The UAE e-invoicing system operates on a continuous transaction control model. Invoices must be submitted to the ASP at the point of issuance, not batched or delayed. The ASP validates the invoice, forwards it to the buyer’s ASP, and simultaneously reports a Tax Data Document (TDD) to the FTA.

- Store invoices electronically Businesses must retain all e-invoices and e-credit notes in electronic form for the full legally required retention period under UAE tax law. The FTA retains the right to access all e-invoicing data at any time.

- Report system failures within 2 business days In the event of a system failure affecting the ability to issue or transmit e-invoices, the business must notify the FTA within two business days. Failure to report constitutes a separate compliance violation.

Additional obligations include:

- Self-billing is permitted where both parties are VAT-registered, subject to ministerial guidelines

- Agents may issue e-invoices on behalf of principals in accordance with VAT Executive Regulation provisions

- Input VAT deductions are only valid where a compliant e-invoice exists in the system

UAE e-Invoicing Guidelines: Technical Standards and Data Format

The UAE e-invoicing system uses the Peppol PINT-AE specification — the UAE-adapted version of Peppol BIS Billing 3.0. All invoices must conform to this XML schema to pass ASP validation. Notably, the UAE specification does not require a QR code or barcode on the invoice document. Invoice authenticity is instead ensured through the ASP’s digital certificates and the secure Peppol network.

Mandatory Fields for a UAE e-Invoice

The UAE Ministry of Finance e-Invoicing Guidelines v1.0 (published February 23, 2026) specifies the following mandatory data categories:

| Category | Key Fields | Notes |

| Invoice Details | Invoice number, issue date, type code, currency code | Type code “380” for commercial invoices |

| Seller Information | Legal name, Tax Registration Number (TRN), address, city | Seller Peppol ID uses prefix “0235” |

| Buyer Information | Legal name, TRN (if VAT-registered), address, city | TRN mandatory for registered buyers |

| Line Items | Description, quantity, unit code, unit price, net amount | Each line must carry individual tax rate and amount |

| Tax Breakdown | Tax category code, tax rate (%), tax amount per category | 5% standard VAT or applicable exempt/zero rate |

| Document Totals | Net amount, total tax amount, gross payable amount | All figures in AED or invoice currency |

Structural and technical requirements under the PINT-AE specification include:

- BusinessProcessType and SpecificationID fields with fixed UAE-mandated values

- Seller’s Peppol electronic identifier based on the first ten digits of the UAE Tax Identification Number

- All monetary amounts expressed to two decimal places in the invoicing currency

- Credit notes must reference the original invoice number and date

ASPs validate every submitted invoice against both the XML schema and a set of business rules defined by the FTA. An invoice that fails validation returns a Message Level Status (MLS) response indicating rejection with error codes. Accepted invoices trigger an automatic TDD report to the FTA. Businesses whose ERP systems generate incomplete or incorrectly mapped data will face systematic rejections — making a thorough data audit a critical pre-implementation step.

How the Peppol 5-Corner Model Works in the UAE

The UAE e-invoicing architecture is built on a decentralized five-corner model, where no invoice travels directly between buyer and seller without passing through accredited intermediaries and the FTA’s tax data repository.

The five corners operate as follows:

- Corner 1 — Supplier (Seller): Generates the XML invoice and submits it to their appointed ASP via API

- Corner 2 — Supplier’s ASP: Validates the invoice against PINT-AE standards, transmits to the buyer’s ASP, and sends a TDD to the FTA

- Corner 3 — Buyer’s ASP: Receives the validated invoice, transmits to the buyer, and sends a confirming TDD to the FTA

- Corner 4 — Buyer: Receives the invoice from their ASP and processes it in their accounting system

- Corner 5 — FTA Tax Data Repository: Receives TDD reports from both ASPs, creating a complete real-time audit trail without direct access to the seller-buyer relationship

This architecture ensures the FTA receives structured tax data on every transaction without becoming a bottleneck in the invoicing flow. Businesses that previously operated closed bilateral invoicing systems — sending PDFs directly by email — must reconfigure their processes entirely around this API-based submission model.

All communication between businesses and ASPs uses HTTPS with TLS encryption. ASPs operate as certified Peppol Access Points and must comply with security requirements specified in Ministerial Decision No. 64/2025.

List of Accredited Service Providers (ASPs) for UAE e-Invoicing

The UAE Ministry of Finance maintains an official registry of Accredited Service Providers authorized to operate on the Peppol network for UAE e-invoicing. All businesses must select from this accredited list — engaging a non-accredited provider does not satisfy the legal requirement under Ministerial Decision No. 243/2025.

As of the first quarter of 2026, the Ministry of Finance has begun publishing its ASP accreditation list through the official UAE e-Invoicing portal. The list is subject to ongoing updates as new providers complete the accreditation process, which includes conformance testing, security certification, and compliance with Peppol network rules.

Key criteria for evaluating an ASP include:

- Accreditation status confirmed on the Ministry of Finance official portal

- ERP and accounting software compatibility (SAP, Oracle, Microsoft Dynamics, Zoho, QuickBooks, etc.)

- Sandbox/testing environment availability for pre-go-live validation

- API documentation quality and developer support

- Pricing model (per-invoice, subscription, or volume-tiered)

- Customer support in English and Arabic

- Data residency and security certifications

| Evaluation Factor | Large Enterprise Priority | SME Priority |

| ERP Integration Depth | High — custom API and middleware support | Medium — plug-and-play connectors preferred |

| Volume Capacity | High — thousands of invoices daily | Low to Medium |

| Sandbox Environment | Essential for pre-go-live testing | Recommended |

| Multi-entity Support | Required for group structures | Optional |

| Pricing Model | Volume-tiered or enterprise contract | Subscription or per-invoice |

| Arabic-language Support | Recommended | Often essential |

The Ministry of Finance has stressed that businesses should begin ASP evaluation well in advance of their appointment deadlines. Early engagement allows time for contract negotiation, technical onboarding, API integration, and at least one full round of end-to-end testing before the mandatory go-live date.

For businesses operating across multiple free zones or mainland entities, it is worth confirming whether a single ASP can manage invoicing for all legal entities within a group structure, or whether separate ASP arrangements are required per entity

E-Invoicing UAE FTA: Enforcement and Penalty Framework

The Federal Tax Authority (FTA) enforces the UAE e-invoicing regime under the penalty framework established by Cabinet Decision No. 106/2025. Understanding these penalties is essential for any CFO or compliance officer building a business case for timely implementation.

Penalties for UAE e-invoicing violations include:

- AED 5,000 per month for failing to appoint an accredited ASP by the applicable deadline

- AED 100 per invoice for each invoice issued outside the e-invoicing system after the mandatory go-live date

- Additional penalties for failure to report system failures within the two-business-day window

- Potential disallowance of input VAT claims where invoices cannot be verified in the FTA’s tax data repository

Voluntary early adopters who join the pilot phase before their mandatory deadline are explicitly exempt from penalties until their respective compliance dates. This creates a meaningful incentive for businesses — particularly large taxpayers — to commence voluntary participation in mid-2026 rather than waiting for the January 2027 deadline.

FTA officials have publicly stated that e-invoicing compliance will be integrated into the broader VAT audit process. Going forward, FTA auditors will be able to cross-reference declared VAT figures against the real-time TDD data received from ASPs, significantly narrowing the margin for reporting discrepancies. Businesses with unresolved data quality issues — missing TRNs, incorrect tax codes, incomplete line-item data — face heightened audit risk once the system is fully operational.

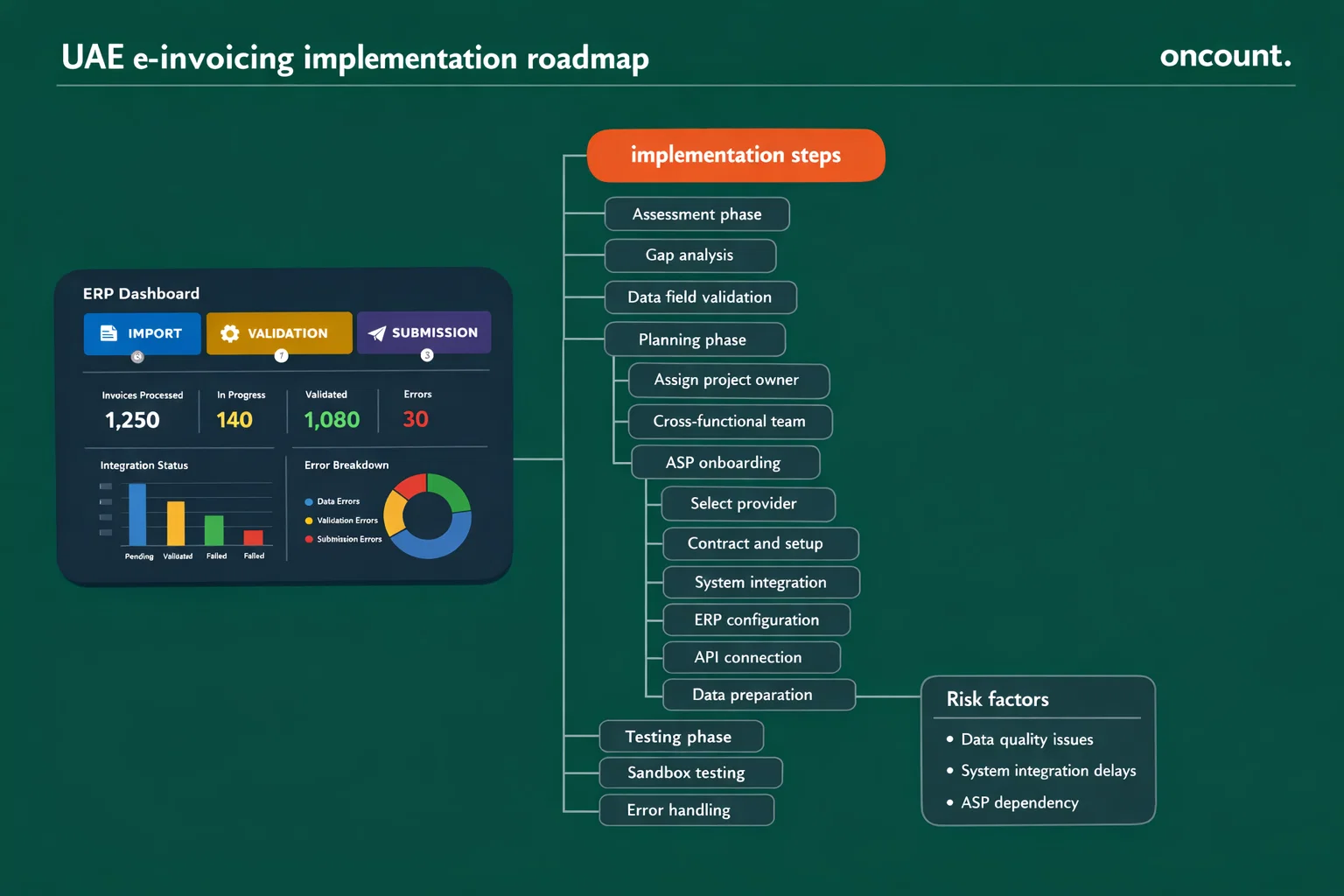

Step-by-Step Implementation Guide for UAE Businesses

Businesses approaching the UAE e-invoicing mandate for the first time should follow a structured implementation methodology. The following framework applies to both large enterprises and SMEs, with appropriate scaling by resource capacity.

Step 1: Conduct a Compliance Readiness Assessment

Map all current invoicing workflows, identify every system that generates invoices (ERP, billing platforms, manual processes), and compare existing invoice data fields against the PINT-AE mandatory field list. Document gaps — particularly missing TRNs, incorrect tax codes, and incomplete buyer master data.

Step 2: Assign a Project Owner and Cross-Functional Team

Appoint a senior project lead — typically within the finance or tax function — with authority to coordinate IT, operations, procurement, and external advisors. Large enterprises should form a formal steering committee; SMEs may rely on a single finance manager supported by the ASP’s implementation team.

Step 3: Select and Onboard an Accredited Service Provider

Research ASPs accredited by the UAE Ministry of Finance. Issue a request for proposal covering technical capabilities, pricing, and integration support. Sign an ASP agreement and initiate the onboarding process, including API access credentials and sandbox environment setup.

Step 4: Integrate Invoicing Systems with the ASP API

Modify or configure the existing ERP or accounting system to generate Peppol PINT-AE-compliant XML invoices. Develop or deploy the API connection to the ASP for invoice submission and MLS status retrieval. Test all invoice types: standard tax invoices, credit notes, zero-rated supplies, exempt supplies, and any special transaction types relevant to the business.

Step 5: Cleanse and Validate Master Data

Verify all supplier and customer TRNs through the FTA’s EmaraTax platform. Standardize address formats, product/service codes, and unit-of-measure codes across all invoice templates. Errors in master data are among the most common causes of invoice rejection in the early stages of e-invoicing deployment.

Step 6: Run End-to-End Testing

Submit test invoices through the ASP sandbox environment. Simulate both accepted and rejected scenarios. Confirm that MLS responses are correctly handled by the invoicing system. Validate TDD transmission to the FTA’s test environment if the ASP provides this capability.

Step 7: Train Finance and Operations Personnel

Deliver targeted training to accounts payable, accounts receivable, and procurement teams. Update standard operating procedures to reflect that no paper or PDF invoice constitutes a valid tax document after the mandatory go-live date. Establish an internal escalation process for rejected invoices.

Step 8: Go Live and Monitor Continuously

Activate e-invoicing for all applicable B2B and B2G transactions on or before the mandatory deadline. Monitor daily rejection rates, MLS status responses, and ASP system availability. Establish a protocol for system failure reporting to the FTA within the two-business-day window.

Free Zone Businesses and UAE e-Invoicing

Free zone entities conducting B2B transactions with mainland UAE businesses or other free zone companies are subject to the same e-invoicing obligations as mainland entities under Ministerial Decision No. 243/2025. The regulation applies to any person conducting business in the UAE — there is no blanket free zone exemption.

In practice, free zone entities that operate as qualifying free zone persons (QFZPs) for UAE Corporate Tax purposes and conduct inter-company or cross-border transactions must assess whether those transactions fall within the B2B and B2G scope of the e-invoicing mandate. Transactions that are currently treated as out-of-scope for UAE VAT purposes — such as certain supplies to overseas clients — may still require careful review against the e-invoicing scope rules.

Free zone businesses that have not yet registered for UAE VAT (because their revenues fall below the AED 375,000 mandatory registration threshold) should obtain legal clarity on whether their B2B supply activities nevertheless fall within scope of the e-invoicing requirement, as the mandate extends beyond VAT-registered entities in some contexts.

Practical Preparation: Checklist for CFOs and Finance Managers

The following checklist consolidates the core compliance tasks required before each phase deadline:

Before ASP Appointment Deadline:

- Complete internal gap analysis against PINT-AE mandatory fields

- Identify all invoice-generating systems across the business

- Evaluate and shortlist accredited ASPs from the Ministry of Finance registry

- Confirm ASP compatibility with existing ERP or accounting platform

- Execute ASP agreement and begin onboarding

Before Go-Live Deadline:

- Complete API integration between internal systems and ASP

- Cleanse all customer and supplier master data (TRNs, addresses, tax codes)

- Conduct full end-to-end testing in ASP sandbox environment

- Train all relevant finance and operations personnel

- Update internal invoice approval and archival procedures

- Establish system failure reporting protocol for FTA notification

- Confirm data retention infrastructure meets UAE legal requirements

Ongoing After Go-Live:

- Monitor daily MLS rejection rates and resolve errors promptly

- Review FTA and Ministry of Finance portals monthly for guidance updates

- Maintain ASP service agreements and renew accreditation confirmations

- Integrate e-invoice data into VAT return preparation process

- Prepare for FTA audits using TDD reconciliation reports

Conclusion: Acting Now Is Non-Negotiable

The UAE e-invoicing mandate represents one of the most significant structural changes to business compliance in the country since the introduction of VAT in 2018. With the first mandatory deadline — for large businesses — set for January 1, 2027, and ASP appointment required by July 31, 2026, the effective preparation window for large taxpayers is already narrowing.

The businesses that will navigate this transition most successfully are those that treat it as a finance and technology transformation initiative, not merely an IT upgrade. Engaging an accredited ASP early, conducting a thorough data readiness assessment, and running complete end-to-end tests before the deadline are the three most critical actions any UAE business can take today.

The Federal Tax Authority has made clear that enforcement under Cabinet Decision No. 106/2025 will be active and systematic. The combination of real-time TDD reporting and FTA audit integration means that non-compliant businesses will face both direct penalties and elevated VAT audit exposure. For CFOs and financial managers, the cost of delay far exceeds the cost of early preparation.