Key Takeaways

- VAT registration is mandatory for travel agencies with annual taxable supplies exceeding AED 375,000, per Federal Decree-Law No. 8 of 2017.

- Tour Operator Margin Scheme (TOMS) is mandatory for UAE-resident agencies acting as principals — VAT is calculated on the profit margin, not total package price.

- UAE Corporate Tax imposes a 9% rate on profits above AED 375,000; small business relief applies for revenue at or below AED 3,000,000.

- IFRS is the mandatory reporting framework for all UAE-registered companies under Commercial Companies Law No. 2 of 2015.

- Dubai DET licensing requires audited financial statements for annual license renewal, minimum office space of 40 sqm, and qualified management.

- Free zone agencies may qualify for 0% corporate tax as Qualifying Free Zone Persons (QFZP), subject to substance and audit requirements.

- Compliance deadlines include VAT returns within 28 days of the end of the period, corporate tax returns within 9 months of financial year-end, and Tourism Dirham remittance by the 16th of the following month.

Overview of Accounting Requirements in the UAE for Travel Agencies

Travel agencies registered in Dubai are subject to the UAE Commercial Companies Law (Federal Law No. 2 of 2015), which mandates that all companies maintain financial records in accordance with internationally accepted accounting standards. No local GAAP exists in the UAE; IFRS is the sole recognized framework.

The Federal Tax Authority (FTA) requires VAT-registered travel agencies to maintain detailed accounting records for a minimum of five years, supporting VAT return filings and potential FTA audits. These records must include sales invoices, supplier invoices, bank statements, and documentation of tour package costs and margins.

Dubai’s Department of Economy and Tourism (DET) imposes additional reporting obligations. Travel agencies must submit audited financial statements as part of the annual trade license renewal process. Failure to maintain compliant records can result in license non-renewal, operational restrictions, and financial penalties from both DET and the FTA.

Travel agencies are also required to register for corporate tax through the EmaraTax portal if annual turnover exceeds AED 1,000,000. Even agencies below the mandatory VAT threshold benefit from maintaining structured accounting records to support business planning, investor reporting, and regulatory audits.

IFRS Application for Travel Agency Companies

The IFRS Foundation framework applies universally to UAE-registered travel agencies. Full IFRS standards govern medium-to-large agencies, while IFRS for SMEs is available to qualifying smaller agencies as a simplified alternative, subject to local audit requirements and free zone authority approvals.

Key standards with direct application to travel agency operations include:

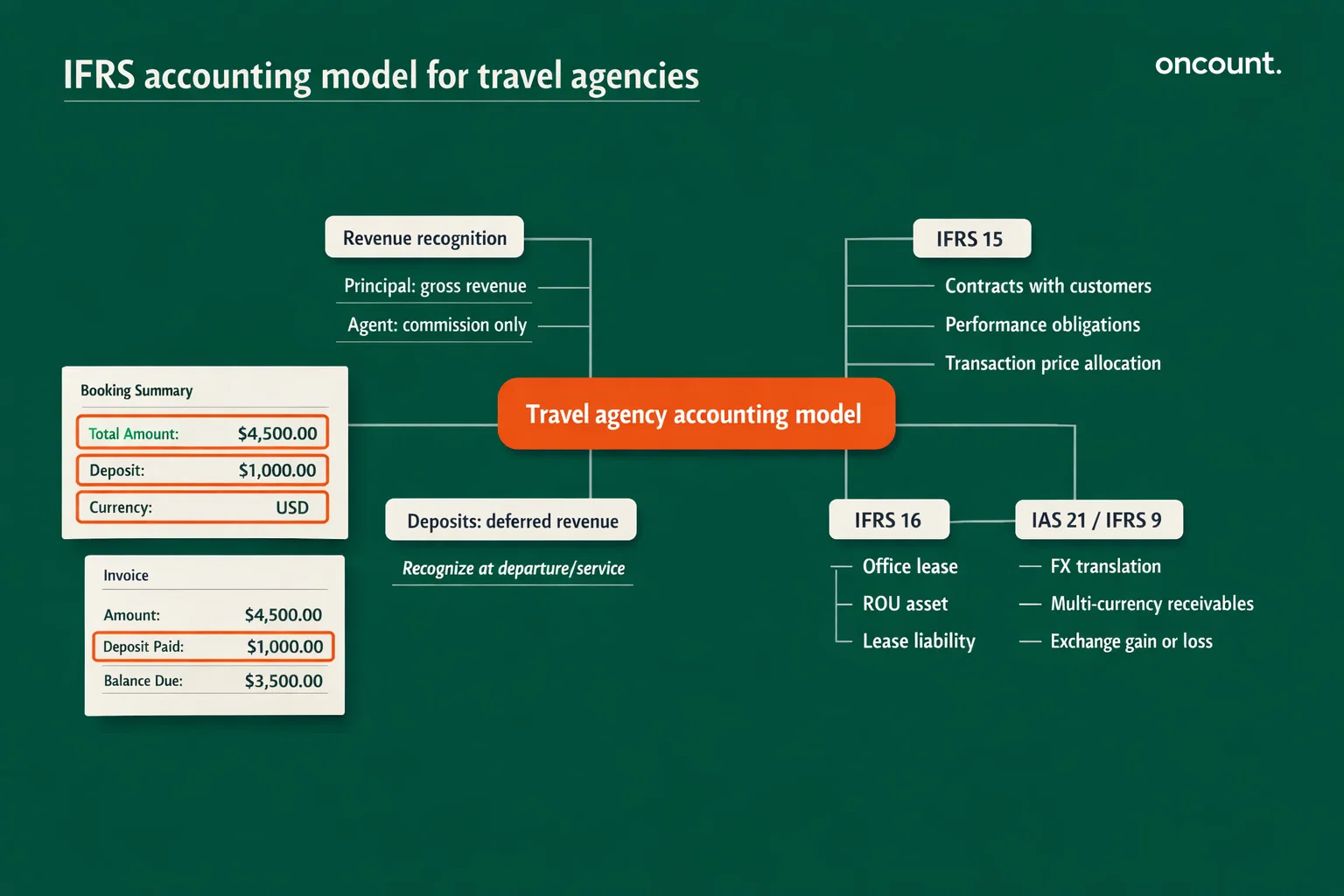

- IFRS 15 (Revenue from Contracts with Customers): Governs when and how tour package revenue, commission income, and service fees are recognized. Revenue is recognized when performance obligations are satisfied — typically upon departure or service delivery, not at the point of deposit receipt.

- IFRS 16 (Leases): Applies to office lease agreements. Dubai travel agencies operating from leased commercial premises must capitalize right-of-use assets and corresponding lease liabilities on the balance sheet.

- IFRS 9 (Financial Instruments): Relevant for managing foreign currency receivables and payables — a common issue given multi-currency airline and hotel supplier contracts denominated in USD or EUR.

- IAS 21 (Effects of Changes in Foreign Exchange Rates): Requires translation of foreign currency transactions at spot rates and recognition of exchange gains or losses in the income statement.

Free zone travel agencies seeking to maintain Qualifying Free Zone Person (QFZP) status under UAE Corporate Tax Law must prepare audited financial statements in accordance with IFRS Standards, as stipulated by the UAE Ministry of Finance Corporate Tax Guide.

Bookkeeping Framework and Financial Records for Travel Agencies

A well-structured bookkeeping system for a Dubai travel agency must reflect the dual nature of agency operations — acting as both agent (earning commissions) and principal (selling packaged tours). The chart of accounts should separate these revenue streams clearly to support accurate VAT calculation under TOMS and correct corporate tax determination.

Recommended chart of accounts structure:

| Code Range | Category | Examples |

| 1000–1500 | Assets | Cash, receivables, prepaid bookings, fixed assets |

| 2000–2500 | Liabilities & Equity | Payables, customer advances, VAT payable, share capital |

| 3000–3500 | Revenue | Tour package sales, commissions, service fees |

| 4000–4300 | Cost of Sales | Airfare cost, hotel cost, disbursements |

| 5000–5700 | Operating Expenses | Salaries, rent, marketing, depreciation, FX losses |

Critical bookkeeping practices for travel agencies include:

- Separate ledger accounts for customer advance deposits (recorded as deferred revenue until service delivery).

- Tracking blocked versus recoverable input VAT — under TOMS, input VAT on designated travel components (airfare, hotels) is not reclaimable, while input VAT on overhead expenses (rent, marketing) remains recoverable.

- Monthly bank reconciliations aligned with IATA BSP airline clearing cycles.

- Multi-currency transaction recording with exchange rate documentation per IAS 21.

Supporting documentation must include: supplier contracts, airline BSP statements, hotel confirmation invoices, client booking agreements, visa fee receipts (as disbursement evidence), and bank transaction records.

Financial Statements Preparation Requirements

Dubai travel agencies must prepare a complete set of IFRS-compliant financial statements annually. These serve multiple regulatory functions: corporate tax determination, FTA VAT audits, DET license renewal, and free zone authority compliance.

Required financial statements include:

- Statement of Profit or Loss: Reflects tour package revenues, commission income, service fees, cost of sales, and operating expenses. Net profit above AED 375,000 triggers UAE corporate tax at 9%.

- Statement of Financial Position (Balance Sheet): Discloses cash, trade receivables, prepaid booking costs, fixed assets, accounts payable to suppliers, customer advance liabilities, VAT payable, and equity.

- Statement of Cash Flows: Particularly important for travel agencies given timing gaps between customer deposit receipts and supplier payment obligations.

- Notes to Financial Statements: Must include accounting policies (especially TOMS-related VAT treatment), foreign currency policies, and lease disclosures under IFRS 16.

Audited financial statements are required for annual license renewal with the DET and, for free zone agencies, for submission to the relevant free zone authority. Dubai free zones such as IFZA now mandate audit report submission at the point of license renewal.

VAT Compliance for Travel Agency Companies in the UAE

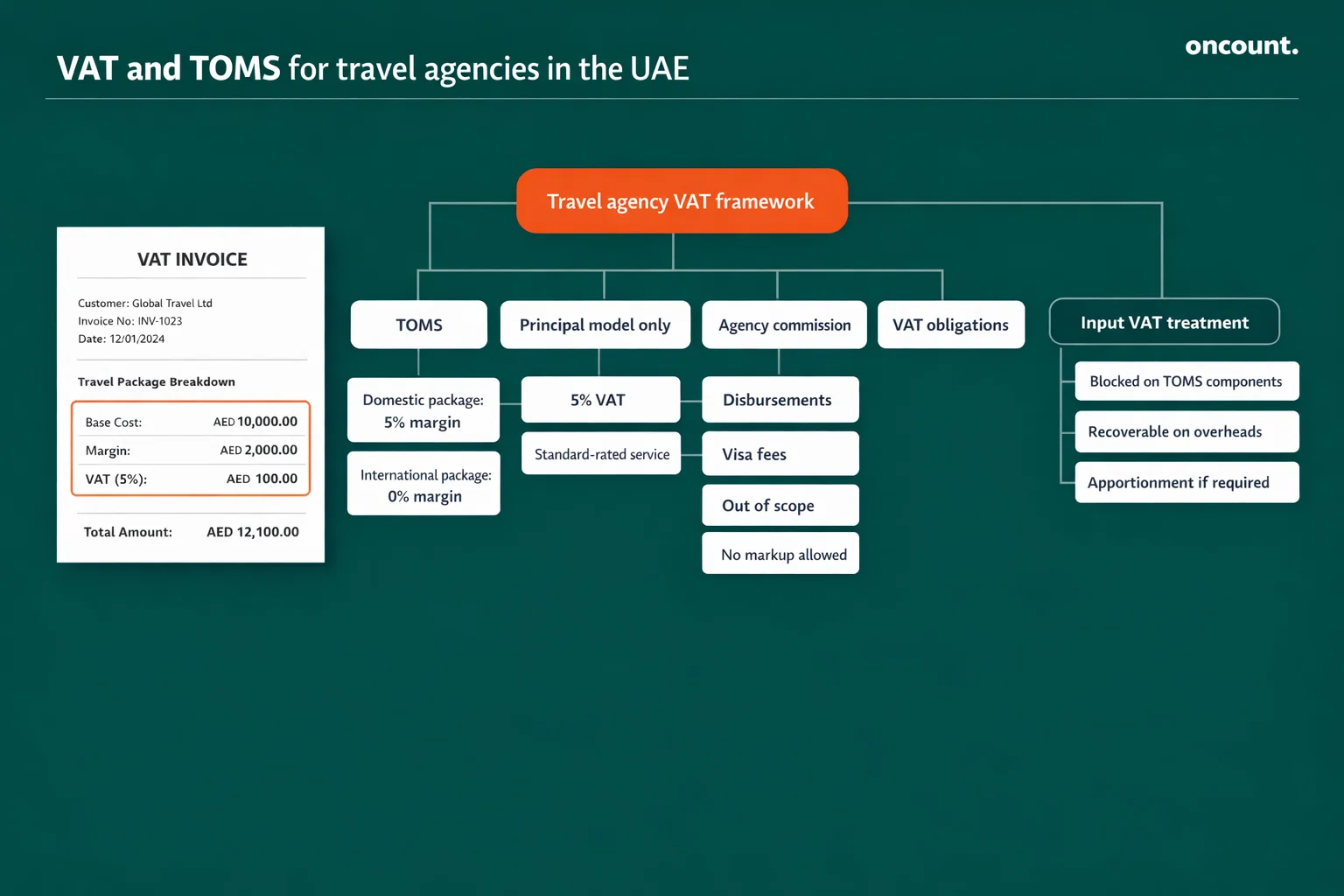

The Federal Tax Authority (FTA) administers VAT under Federal Decree-Law No. 8 of 2017. Travel agencies must register for VAT when annual taxable supplies exceed AED 375,000 (mandatory threshold) or AED 187,500 (voluntary threshold). Registration is completed through the EmaraTax portal.

Tour Operator Margin Scheme (TOMS) is the defining VAT mechanism for UAE travel agencies acting as principals. Under TOMS:

- Output VAT is applied to the margin (package sale price minus direct cost of designated travel components), not the full package price.

- Domestic packages (services consumed within the UAE) attract 5% VAT on the margin.

- International packages (services consumed outside the UAE/GCC) are zero-rated on the margin.

- A loss-making package yields zero VAT liability — the margin floor is zero.

- Input VAT on designated travel components (airfare, hotel costs) is not recoverable. Input VAT on agency overheads remains recoverable subject to apportionment.

| Service Type | Place of Supply | VAT Rate | Scheme |

| UAE-departure international flight | UAE | 5% | Standard |

| Foreign-departure flight | Outside UAE | 0% | Exempt |

| Hotel in Dubai | UAE | 5% | Standard |

| Hotel outside UAE | Outside UAE | 0% | Zero-rated |

| Domestic tour package margin | UAE | 5% on margin | TOMS |

| International tour package margin | Outside UAE | 0% on margin | TOMS |

| Agency commission (UAE agent) | UAE | 5% | Standard |

| Visa fees (disbursement) | Out of scope | 0% | Disbursement |

VAT returns must be filed and VAT payments submitted within 28 days of the end of each tax period (typically quarterly). Agencies earning commissions only — acting as agents rather than principals — invoice the commission fee at 5% VAT and are not subject to TOMS.

Corporate Tax Framework for Travel Agencies in Dubai

UAE Corporate Tax (CT), introduced under Federal Decree-Law No. 47 of 2022, applies to all UAE-resident companies with financial years beginning on or after June 1, 2023. Travel agencies are subject to the following tiered structure:

- 0% on taxable profits up to AED 375,000

- 9% on taxable profits above AED 375,000

Small Business Relief permits resident travel agencies with annual revenue at or below AED 3,000,000 (in both the current and prior tax period) to elect a 0% effective CT rate. Once revenue exceeds AED 3,000,000 in any period, relief ceases permanently. Free zone entities are explicitly excluded from Small Business Relief eligibility.

Free zone travel agencies may qualify as Qualifying Free Zone Persons (QFZP) and apply a 0% rate to qualifying income, provided they:

- Maintain adequate economic substance within the UAE

- Prepare audited IFRS-compliant financial statements

- Derive income from qualifying activities

- Do not opt out of the free zone tax regime

If QFZP conditions are not met, the entity is taxed at 9% on all income for that year and the subsequent four years. Corporate tax returns must be filed through the EmaraTax portal within 9 months of the financial year-end.

Accounting for Revenue and Expenses in Travel Agencies

Revenue recognition for Dubai travel agencies depends on whether the agency operates as principal or agent, a distinction with significant implications under both IFRS 15 and TOMS.

As principal: The agency controls the travel service before transferring it to the customer. Full package revenue is recorded gross, with costs of airfare, hotels, and tours shown separately. TOMS applies for VAT purposes.

As agent: The agency facilitates the transaction on behalf of a supplier. Only the commission or service fee is recorded as revenue. VAT at 5% applies to the commission amount.

Revenue recognition timing follows IFRS 15 performance obligations. Customer deposits are recorded as deferred revenue (Customer Advances — Account 2120) until the travel service is delivered. For package tours, revenue is typically recognized on the departure date or over the duration of the service.

Expense classification matters for corporate tax deductibility. Allowable deductions include staff salaries, office rent, marketing costs, audit and accounting fees, and depreciation of fixed assets. Non-deductible items include fines, penalties, and entertainment expenses exceeding statutory limits per UAE CT Law.

Regulatory Compliance and Reporting Obligations

Beyond VAT and corporate tax, Dubai travel agencies face several additional compliance obligations:

Economic Substance Regulations (ESR): UAE Cabinet Resolution No. 57 of 2020 requires entities conducting relevant activities to demonstrate genuine economic substance in the UAE. Travel agencies engaged in certain holding or distribution activities may be subject to ESR notification and reporting, filed annually within 12 months of the financial year-end with the UAE Ministry of Finance.

Anti-Money Laundering (AML): Travel agencies handling large cash transactions or high-value luxury travel bookings may fall under UAE AML obligations per Federal Decree-Law No. 20 of 2018. Designated Non-Financial Businesses and Professions (DNFBPs) must implement customer due diligence, transaction monitoring, and suspicious transaction reporting to the UAE Financial Intelligence Unit.

Ultimate Beneficial Owner (UBO) Reporting: UAE Cabinet Resolution No. 58 of 2020 requires all UAE companies to maintain a UBO register disclosing natural persons with direct or indirect ownership of 25% or more. This register must be submitted to and maintained with the relevant licensing authority (DET for mainland agencies; free zone authority for free zone entities).

Audit Requirements for Travel Agencies in Dubai

Mandatory audit requirements vary based on the agency’s jurisdiction and structure:

- Mainland Dubai agencies must submit audited financial statements to the DET as part of annual trade license renewal. The DET and Dubai Tourism enforcement framework (Executive Council Resolution No. 6 of 2006) treats financial transparency as a condition of continued tourism licensing.

- Free zone agencies face explicit audit mandates from their respective free zone authorities. For example, IFZA requires submission of audited accounts at license renewal, and QFZP status under corporate tax law requires IFRS-audited statements.

Auditors engaged by Dubai travel agencies must be registered with the UAE Ministry of Economy and hold a valid UAE audit license. Audit scope typically includes verification of TOMS margin calculations, input VAT recovery accuracy, customer advance balances, supplier payable reconciliations, and IFRS compliance of financial statements.

The audit process supports accurate corporate tax determination and protects agencies from FTA assessments. FTA guidance stipulates that businesses maintaining incomplete or inaccurate records face administrative penalties beginning at AED 10,000 per violation.

Industry-Specific Accounting Considerations for Travel Agencies

Tour Operator Margin Scheme Implementation

Implementing TOMS correctly requires the accounting system to separate designated travel components (airfare, accommodation, ground transport bought for resale) from overhead costs (salaries, rent, marketing). The margin is calculated per package: sales price minus direct component cost. Mixing overhead costs into the TOMS margin calculation is a common and costly error.

Multi-Currency Transaction Management

Dubai travel agencies routinely transact in USD, EUR, and GBP with international hotel chains, airlines, and ground operators. IAS 21 requires each transaction to be recorded at the spot exchange rate on the transaction date, with monetary assets and liabilities retranslated at the closing rate. Exchange differences are recognized in the income statement under Account 5710 (FX Losses) or Account 3510 (FX Gains).

Tourism Dirham Accounting

The Dubai Tourism Dirham fee (AED 7–20 per room-night depending on hotel category) is collected by hotels and remitted to DET by the 16th of the following month. Travel agencies packaging hotel accommodation must track and account for this fee through Account 2140 (Tourism Dirham Payable) to avoid pass-through disputes with hotel suppliers.

Common Accounting Challenges for Travel Agency Companies

Travel agencies in Dubai face distinct accounting difficulties that can result in regulatory penalties if left unaddressed:

- Incorrect TOMS application: Agencies misclassifying themselves as agents when acting as principals — or incorrectly applying standard VAT to package sales instead of TOMS — face FTA reassessment and penalties.

- Deferred revenue mismanagement: Failure to properly account for customer deposits as liabilities until service delivery inflates reported revenue and distorts tax calculations.

- Unreconciled BSP statements: Airline billing through IATA’s Billing and Settlement Plan generates complex monthly statements. Unreconciled BSP balances create phantom payables and distort cash flow reporting.

- Blocked input VAT errors: Agencies incorrectly reclaiming input VAT on designated TOMS travel components — which is specifically disallowed — expose themselves to FTA recovery demands and surcharges.

- Insufficient disbursement documentation: Visa fees and government charges treated as disbursements (out-of-scope for VAT) require evidence that the customer is the true recipient and no markup was applied. Missing documentation results in FTA reclassification as taxable supplies.

Best Practices for Accounting and Financial Management

Structured accounting management reduces compliance risk and strengthens financial visibility for Dubai travel agency owners and CFOs:

- Implement TOMS-compatible accounting software that separates margin calculations by package, tracks blocked input VAT, and generates FTA-compliant VAT return data automatically.

- Perform monthly bank and BSP reconciliations to maintain clean payable and receivable ledgers and detect discrepancies early.

- Engage UAE-licensed auditors annually, well in advance of license renewal dates, to ensure audited statements are available for DET and free zone authority submissions.

- Maintain a compliance calendar tracking VAT return deadlines (28 days post-period), corporate tax return deadlines (9 months post-year-end), Tourism Dirham remittance (16th of following month), and license renewal dates.

- Segregate financial duties — separate the booking, invoicing, and payment functions to prevent misappropriation of customer advance deposits, a high-risk area in travel businesses.

- Review UBO and ESR obligations annually, particularly if ownership structures or business activities change, to ensure filings remain current with DET and the Ministry of Finance.

Comparison: Free Zone vs Mainland Accounting Requirements

| Criteria | Mainland Dubai Agency | Free Zone Agency (QFZP) |

| Corporate Tax Rate | 0% ≤ AED 375k profit; 9% above | 0% on qualifying income (if conditions met) |

| Small Business Relief | Available (revenue ≤ AED 3m) | Not available (excluded by CT Law) |

| Audit Requirement | Mandatory for DET license renewal | Mandatory for free zone authority renewal + QFZP status |

| Accounting Standard | IFRS or IFRS for SMEs | Full IFRS (required for QFZP) |

| VAT Obligations | Full FTA registration and TOMS | Same; free zone status does not exempt from VAT |

| UBO/ESR Reporting | Filed with DET / Ministry of Finance | Filed with free zone authority |

| QFZP Failure Consequence | N/A | 9% tax on all income for 5-year period |

| Operational Flexibility | Full UAE market access | Restricted to free zone / international activity (varies) |

Mainland agencies benefit from unrestricted UAE market access and Small Business Relief eligibility, while free zone agencies can achieve effective 0% corporate tax on qualifying income — but must maintain stricter substance and audit standards to preserve that status.