Key Takeaways

- UAE hotels must maintain IFRS-compliant financial statements under Federal Law No. 2 of 2015

- VAT at 5% applies to room revenue, F&B, events, and ancillary services

- UAE Corporate Tax applies a 9% rate to taxable profits exceeding AED 375,000

- Dubai imposes a Tourism Dirham of AED 7–20 per room per night, plus a 10% municipality fee

- Abu Dhabi applies a 4% tourism fee and 4% municipality fee on accommodation charges

- Revenue recognition for hotel operations is governed by IFRS 15’s five-step model

- Loyalty programs, OTA bookings, and bundled packages each require separate IFRS 15 treatment

- IFRS 16 mandates on-balance-sheet recognition of most property and equipment leases

- Audit by a UAE-licensed auditor is mandatory for most hotel entities

Overview of Accounting Requirements in the UAE for Hotels and Resorts

UAE commercial law establishes a clear obligation for hotel entities to maintain accurate, IFRS-compliant accounting records. Federal Law No. 2 of 2015 on Commercial Companies eliminated a separate UAE GAAP framework and made IFRS the mandatory standard for financial reporting across all UAE-registered entities, including hospitality businesses. Hotels operating in free zones such as DIFC or ADGM are subject to the same IFRS requirement, though their corporate tax treatment may differ.

The UAE Ministry of Finance requires businesses to retain accounting records for a minimum of five years. For hotels, this includes source documentation such as guest folios, purchase invoices, payroll records, bank statements, and contracts with OTAs and event clients. The Federal Tax Authority additionally requires VAT-registered businesses to retain tax-related records for five years, and ten years for real estate-related transactions.

A hotel operating in Dubai with annual revenues exceeding AED 375,000 must register for VAT through the EmaraTax portal administered by the Federal Tax Authority. Voluntary registration is available below this threshold, which is strategically advantageous for hotels seeking to recover input VAT on significant capital expenditures.

Key accounting obligations for UAE hotel operators include:

- Maintaining a general ledger and chart of accounts structured by department

- Preparing IFRS-compliant financial statements annually

- Filing VAT returns quarterly or monthly depending on revenue size

- Registering for and filing UAE Corporate Tax returns from financial year 2023 onward

- Remitting tourism and municipality fees to the relevant emirate authority

- Retaining all supporting documentation per FTA and Ministry of Finance requirements

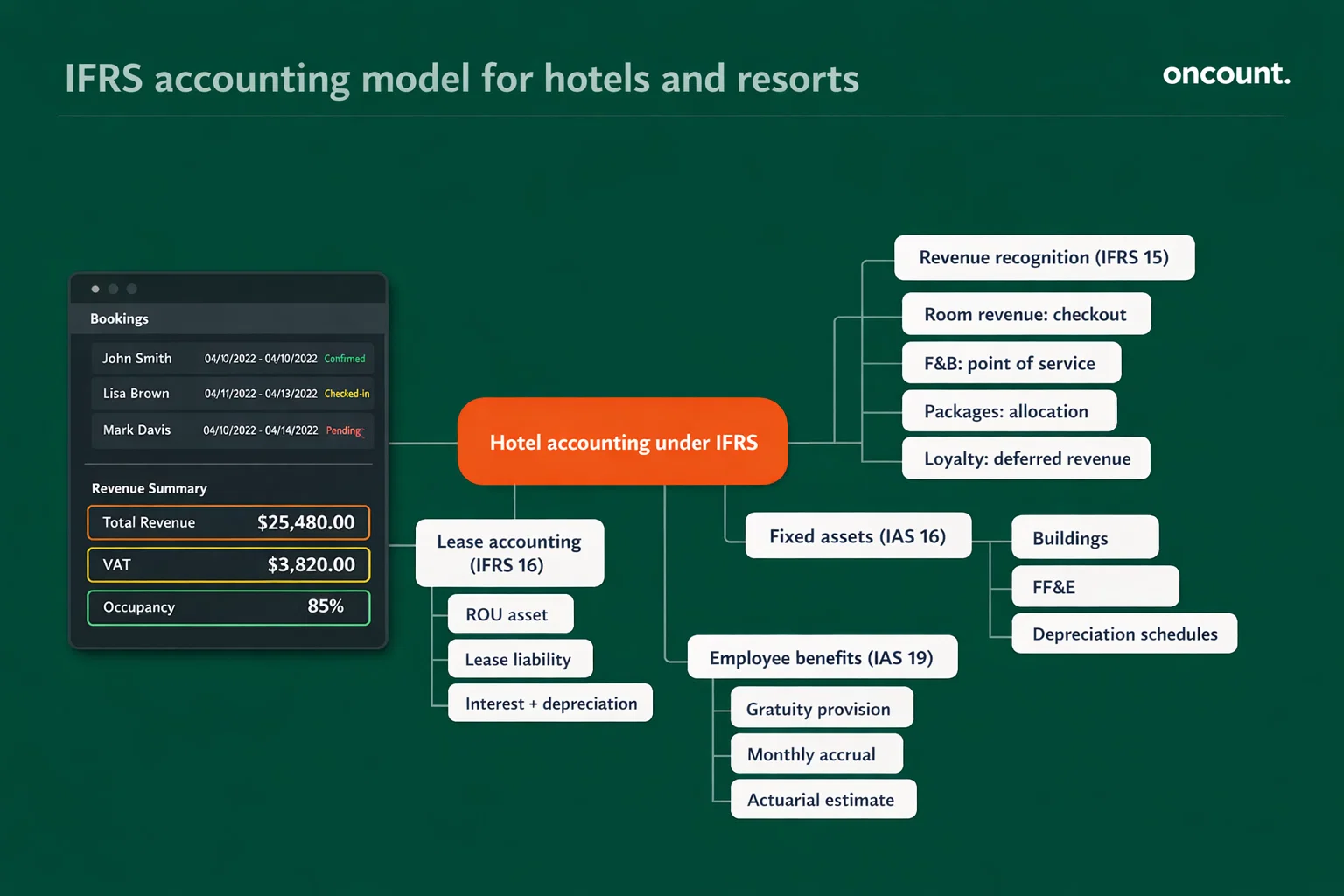

IFRS Application for Hotels and Resorts

International Financial Reporting Standards govern every material aspect of hotel financial reporting in the UAE. The three most operationally significant standards for hospitality entities are IFRS 15 (revenue), IFRS 16 (leases), and IAS 16 (property, plant, and equipment).

IFRS 15 — Revenue from Contracts with Customers defines a five-step recognition model: identify the contract, identify distinct performance obligations, determine the transaction price, allocate the price across obligations, and recognize revenue when each obligation is satisfied. For hotels, this means room revenue is recognized at checkout, F&B revenue at point of delivery, and bundled package revenue allocated across its components using standalone selling prices.

IFRS 16 — Leases requires hotel operators to recognize a right-of-use (ROU) asset and corresponding lease liability for all leases exceeding 12 months, including equipment leases, vehicle contracts, and long-term property leases. A hotel leasing kitchen equipment for five years at AED 20,000 annually must record a lease liability equal to the present value of those payments, with subsequent entries separating depreciation and interest expense.

IAS 16 — Property, Plant, and Equipment governs the capitalization and depreciation of hotel buildings, furniture, fixtures, and equipment (FF&E). Assets above the entity’s capitalization threshold — typically AED 5,000 per item — are depreciated over their useful lives: buildings over 20–40 years, furniture and equipment over 3–10 years.

Additional relevant standards include:

- IAS 2 — Inventory valuation for food, beverages, and operating supplies

- IAS 19 — Employee benefits, including end-of-service gratuity provisions

- IFRS 9 — Financial instruments, particularly for OTA receivables and hedging

- IAS 36 — Impairment of assets during periods of low occupancy

Bookkeeping Framework and Financial Records Structure for Hotel Operations

A well-structured chart of accounts is essential for hotel financial management. Hospitality entities typically organize their accounts by operational department, enabling department-level profit and loss reporting alongside consolidated financial statements.

| Code Range | Category | Examples |

| 1000–1999 | Assets | Cash, receivables, inventory, ROU assets, PP&E |

| 2000–2999 | Liabilities | Payables, contract liabilities, VAT payable, lease liabilities |

| 3000–3999 | Equity | Share capital, retained earnings |

| 4000–4999 | Revenue | Room revenue, F&B revenue, spa, service charges |

| 5000–5999 | Cost of Sales | F&B COGS, room amenities |

| 6000–6999 | Operating Expenses | Payroll, utilities, depreciation, marketing |

Guest advance deposits are recorded as contract liabilities (account 2110) until the stay is completed, at which point the liability is transferred to room revenue. This treatment aligns with IFRS 15’s requirement that revenue is recognized only when performance obligations are satisfied, not when cash is received.

Supporting documentation for each transaction must include: guest folios and PMS-generated invoices, supplier invoices with VAT breakdowns, payroll registers, bank reconciliation statements, and contracts for group bookings and events.

Financial Statements Preparation Requirements

UAE hotels are required to prepare a full set of IFRS-compliant financial statements annually. These include the statement of financial position (balance sheet), statement of profit or loss and other comprehensive income, statement of cash flows, statement of changes in equity, and notes to the financial statements.

The notes section is particularly significant for hotel operations, as it must disclose revenue recognition policies (including treatment of loyalty programs and OTA bookings), lease commitments under IFRS 16, end-of-service gratuity provisions under IAS 19, and related-party transactions such as management fees paid to parent companies or hotel chains.

According to the UAE Ministry of Finance Corporate Tax Guide (2023), businesses must maintain audited financial statements as the basis for determining taxable income. This creates a direct link between IFRS financial reporting quality and the accuracy of corporate tax filings.

VAT Compliance for Hotels and Resorts in the UAE

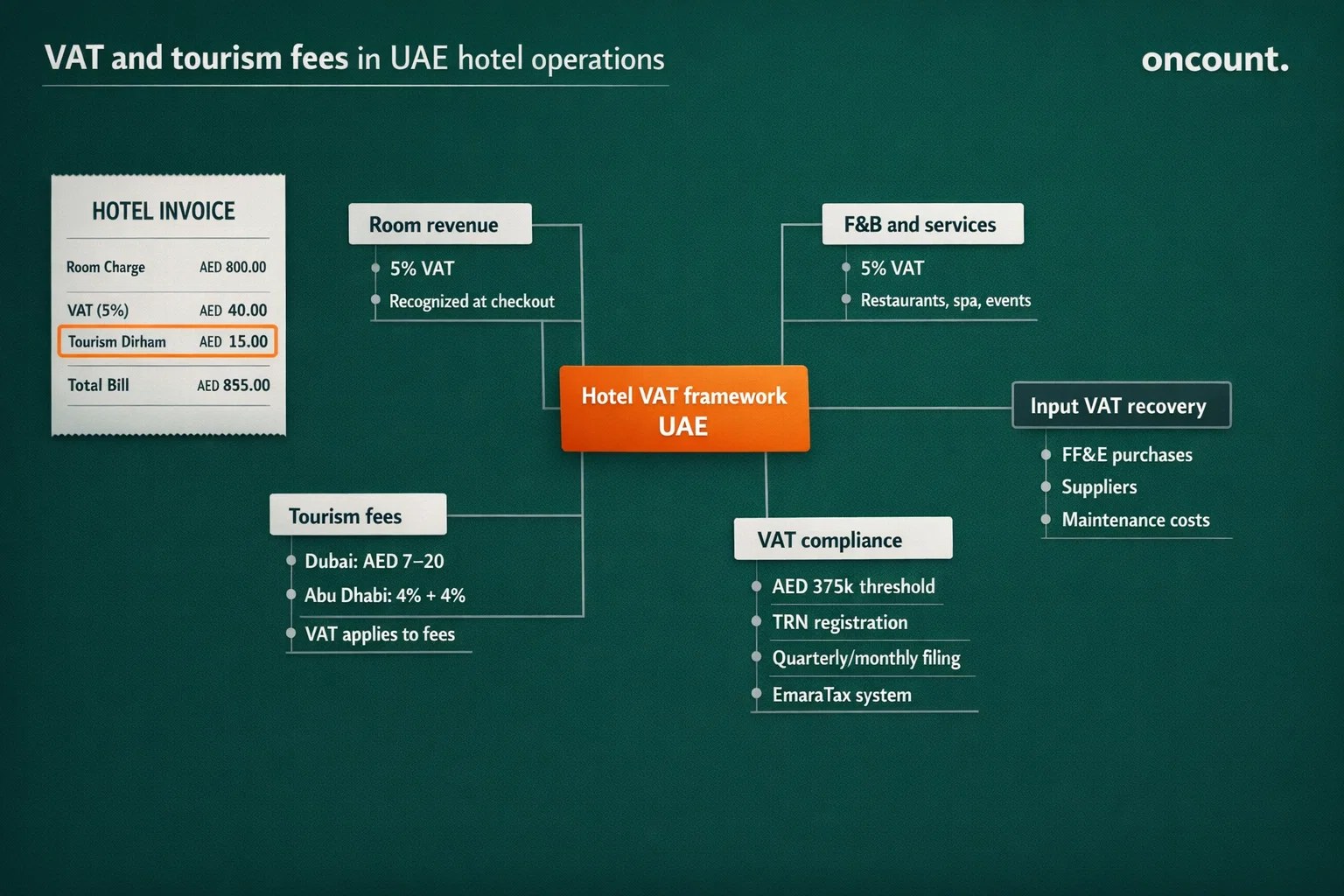

UAE VAT at 5% applies broadly to hotel operations under Federal Decree-Law No. 8 of 2017. The Federal Tax Authority (FTA) confirms that room accommodations, restaurant and bar sales, event catering, spa services, and ancillary hotel charges are all standard-rated supplies subject to the 5% VAT rate.

VAT on Tourism and Municipality Fees: VAT also applies to the tourism fees and municipality charges collected by hotels on behalf of local authorities. A Dubai hotel charging a Tourism Dirham of AED 20 per night must also apply 5% VAT to that charge on the final guest bill.

Input VAT Recovery: Hotels can recover input VAT on business-related purchases — food and beverage supplies, maintenance services, FF&E procurement, and professional fees. However, input VAT on entertainment expenses or costs directly linked to exempt supplies is not recoverable.

VAT return filing frequency is determined by the FTA:

- Quarterly filing — for businesses with annual taxable supplies below AED 150 million

- Monthly filing — for businesses exceeding AED 150 million in annual taxable supplies

A Dubai five-star hotel processing AED 50 million annually in room and F&B revenue would typically file VAT returns quarterly via the EmaraTax portal, with returns due within 28 days of the end of each tax period.

Corporate Tax Framework for Hotels and Resorts

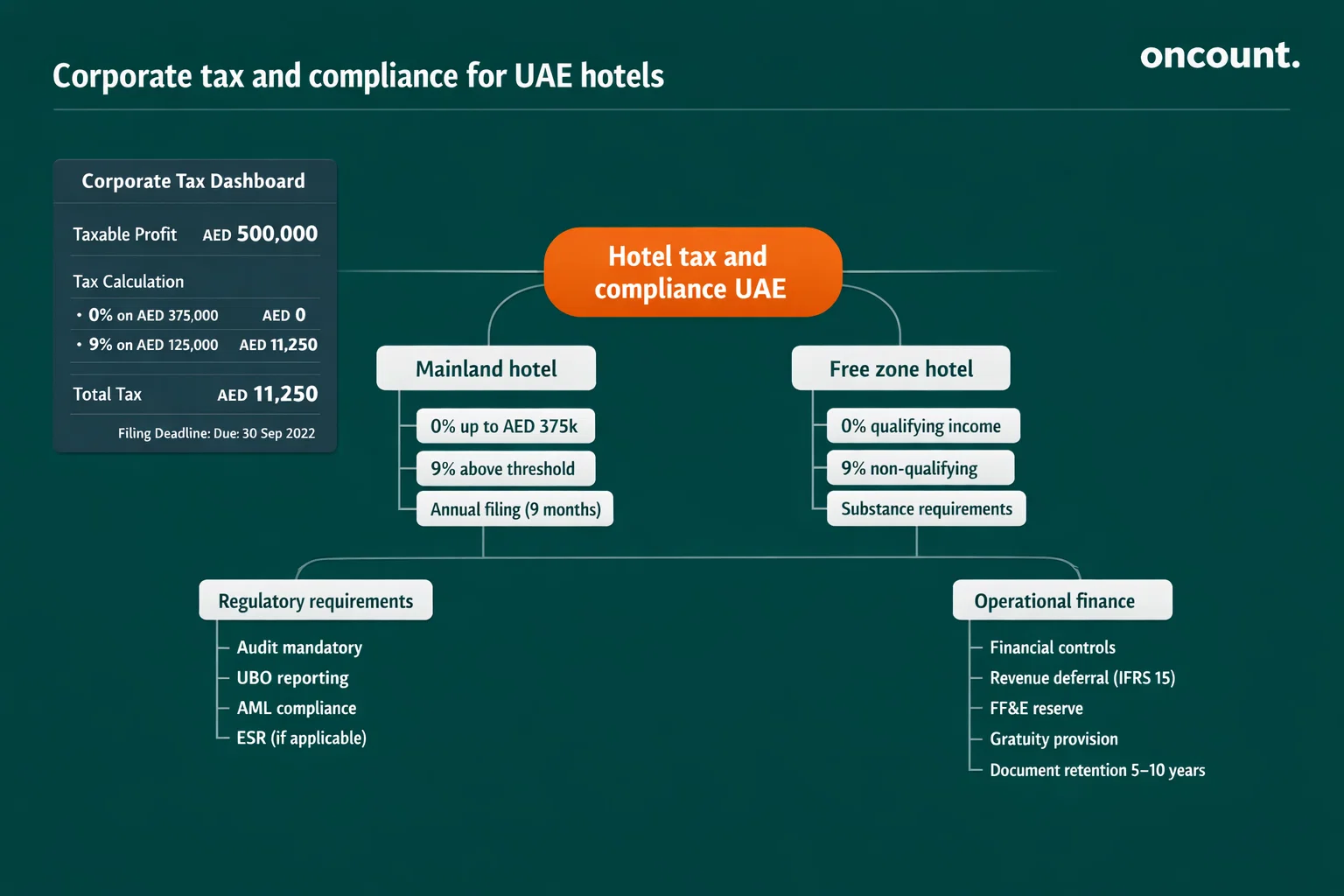

UAE Corporate Tax became effective for financial years beginning on or after June 1, 2023, under Federal Decree-Law No. 47 of 2022. Hotel and resort operators on the UAE mainland are subject to the standard rate structure: 0% on taxable profits up to AED 375,000 and 9% on profits exceeding that threshold.

| Taxable Profit (AED) | Corporate Tax Rate | Tax Payable (AED) |

| 0 – 375,000 | 0% | 0 |

| 375,001 – 1,000,000 | 9% on excess | 56,250 |

| 1,000,000+ | 9% on full amount above threshold | 56,250 + 9% of remainder |

Deductible Expenses for Hotels: Staff salaries and end-of-service gratuity, depreciation on PP&E, IFRS 16 lease interest and depreciation, marketing and distribution costs, and management fees at arm’s length are generally deductible. Penalties, fines, and entertainment expenses above prescribed limits are non-deductible.

Free Zone Considerations: Hotels operating within qualifying UAE free zones may benefit from a 0% corporate tax rate on qualifying income, provided they meet the substance requirements under Cabinet Decision No. 55 of 2023. However, income derived from UAE mainland operations — including mainland-directed room bookings or catering services — is taxed at 9%. Free zone hotel entities must carefully segregate qualifying and non-qualifying income in their accounting records.

A mainland Dubai hotel generating AED 2,000,000 in net taxable profit would owe AED 146,250 in corporate tax: 0% on the first AED 375,000 and 9% on the remaining AED 1,625,000.

Accounting for Revenue and Expenses in Hotel Operations

Revenue recognition for hotel operations is among the most technically complex areas of IFRS application. The document below outlines the primary treatment across key revenue streams.

Room Revenue: Each occupied room-night is a distinct performance obligation under IFRS 15. Revenue is recognized at checkout. Advance deposits are recorded as contract liabilities and transferred to room revenue upon completion of the stay. If a guest cancels after the non-refundable deadline, the retained deposit is recognized as cancellation income — a separate revenue line — at the point of confirmed cancellation.

Food and Beverage Revenue: F&B sales are recognized at the point of delivery. Mandatory service charges (typically 10%) require a policy decision: if retained by the hotel, they are recorded as other income; if distributed entirely to staff, they are excluded from revenue and recognized as a payroll expense. The IFRS Foundation’s guidance on IFRS 15 confirms that each distinct obligation within a contract must be assessed independently.

Loyalty Programs: When a guest earns loyalty points, IFRS 15 requires allocating a portion of the transaction price to those points as a separate performance obligation. The deferred amount — a contract liability — is released to revenue only when points are redeemed or expire.

OTA and Third-Party Bookings: In the vast majority of UAE hotel arrangements, the hotel acts as the principal. The hotel controls the room, sets pricing, and bears inventory risk. OTA commissions (typically 15–25%) are therefore recorded as selling expenses, not netted against revenue. Full room revenue is reported.

| Revenue Stream | Recognition Point | IFRS Standard | Common Treatment |

| Room revenue | Guest checkout | IFRS 15 | Per night, from contract liability |

| F&B sales | Point of delivery | IFRS 15 | At the time of service |

| Event/banquet | Completion of event | IFRS 15 | Over the event period if multi-day |

| Loyalty points earned | Allocated at the sale | IFRS 15 | Deferred as contract liability |

| OTA bookings (principal) | Checkout | IFRS 15 | Gross revenue, commission as expense |

| Cancellation fees | Confirmed cancellation | IFRS 15 | Variable consideration, constrained |

Regulatory Compliance and Reporting Obligations

Beyond tax and IFRS reporting, UAE hotel entities are subject to several additional compliance frameworks that directly affect accounting processes and documentation requirements.

Economic Substance Regulations (ESR): Hotels that earn income from activities defined under ESR — such as holding, leasing, or distribution functions within a group structure — must demonstrate adequate economic substance in the UAE. This includes having qualified staff, incurring operating expenditures locally, and conducting core income-generating activities from within the UAE. ESR reporting is filed annually with the relevant regulatory authority.

Anti-Money Laundering (AML): UAE hotels are subject to AML obligations under Federal Decree-Law No. 20 of 2018. High-value cash transactions above AED 55,000 must be reported to the Financial Intelligence Unit (FIU). Hotels must implement customer due diligence (CDD) procedures for large cash-paying guests and maintain transaction records for a minimum of five years.

Ultimate Beneficial Owner (UBO) Reporting: Hotel entities registered in the UAE mainland must file UBO declarations with the relevant emirate authority, disclosing individuals with 25% or greater ownership. This information feeds into accounting and corporate governance documentation maintained by the company secretary or CFO.

Audit Requirements for Hotels and Resorts in the UAE

Annual statutory audits are mandatory for most UAE hotel entities. Federal Law No. 2 of 2015 requires all limited liability companies and public joint-stock companies to appoint a UAE-licensed auditor and present audited financial statements to shareholders annually.

For hotels operating in free zones, the audit requirement is enforced by the relevant free zone authority. DIFC, ADGM, DMCC, and JAFZA each mandate annual audits as a condition of license renewal, with specific filing deadlines that vary by authority — typically 90 to 180 days after financial year-end.

Auditors reviewing hotel accounts focus on:

- Revenue cycle controls — verifying that all room nights are billed, receipts reconciled to PMS records, and advance deposits properly classified

- Inventory valuation — confirming physical counts align with F&B inventory records and COGS calculations

- Payroll completeness — testing gratuity provisions, service charge distributions, and headcount reconciliations

- Lease liabilities — confirming IFRS 16 ROU assets and liabilities are correctly calculated and disclosed

- Related-party transactions — validating that management fees and intercompany charges reflect arm’s length pricing

Industry-Specific Accounting Considerations for Hotel and Resort Operations

Emirate-Level Tourism Fee Accounting

Each UAE emirate imposes distinct levies that hotels collect from guests and remit to local authorities. These fees are not hotel revenue — they are collected on behalf of government bodies and recorded as pass-through liabilities. A Dubai hotel collecting AED 20 per room night as a Tourism Dirham records: Dr Cash, Cr Tourism Fee Payable. Upon remittance to the Dubai Department of Economy and Tourism: Dr Tourism Fee Payable, Cr Cash.

End-of-Service Gratuity Under IAS 19

UAE Labour Law entitles employees to end-of-service gratuity calculated on final basic salary and years of service. Under IAS 19, this is a defined benefit obligation requiring actuarial estimation. Hotels must accrue monthly: Dr Gratuity Expense, Cr Gratuity Provision. For a hotel with 200 staff members averaging 3 years of service, the annual gratuity provision movement can represent a material liability that requires disclosure in the financial statements.

FF&E Reserve Management

Many UAE hotel management agreements require operators to set aside 2–4% of gross room revenue annually into a Furniture, Fixtures, and Equipment (FF&E) reserve fund. While not an IFRS liability per se, this reserve must be tracked separately and disclosed in management reporting. Actual refurbishment expenditure funded from the reserve is capitalized and depreciated per IAS 16, not expensed as incurred.

Common Accounting Challenges for Hotel and Resort Companies

The hospitality sector in the UAE presents several recurring compliance and reporting challenges that financial managers must proactively address.

Improper Revenue Deferral: Many hotel operators incorrectly recognize advance deposits as revenue upon receipt. This overstates income in the booking period and understates it in the stay period, distorting both financial statements and VAT returns. The correct IFRS 15 treatment requires maintaining a contract liability until the guest completes the stay.

Incorrect VAT on Tourism Fees: Hotels sometimes fail to apply 5% VAT on the Tourism Dirham or municipality fee components of guest bills. The FTA has confirmed that VAT applies to these charges. Failure to account correctly creates both VAT underpayments and potential penalties.

Misclassification of Capital Expenditure: Routine maintenance such as repainting or replacing individual items below the capitalization threshold is frequently capitalized incorrectly, inflating asset values and understating operating expenses. IAS 16 is clear: only expenditure that extends the useful life or improves the asset beyond its original specification qualifies for capitalization.

Weak Inventory Controls: High-volume F&B operations are particularly vulnerable to inventory shrinkage and unrecorded consumption. Without regular cycle counts and reconciliation to POS records, COGS is understated and net income is overstated — a material misstatement risk in audited financials.

Best Practices for Accounting and Financial Management in UAE Hotels

Implementing structured financial management practices protects hotel operators from compliance failures and supports operational performance visibility.

- Adopt a hospitality-specific ERP or PMS with integrated accounting modules (e.g., Oracle OPERA, Infor HMS) to automate the guest folio-to-revenue recognition cycle and reduce manual entry errors

- Establish monthly departmental P&L reviews — comparing rooms, F&B, spa, and event departments independently against budget enables early identification of margin deterioration

- Conduct quarterly VAT reconciliations — matching VAT output in the PMS to VAT returns filed on EmaraTax, and verifying tourism fee remittances to DTCM or DCT

- Maintain a rolling gratuity provision model — updated monthly using headcount, tenure, and salary data to ensure IAS 19 compliance

- Engage specialized hotel accountants for annual audit preparation and corporate tax filing to ensure IFRS standards are applied consistently across all revenue streams

Comparison: Free Zone vs. Mainland Accounting Requirements for Hotels

| Requirement | Mainland Hotel | Free Zone Hotel |

| Corporate Tax Rate | 9% above AED 375,000 | 0% on qualifying income; 9% on non-qualifying |

| VAT Obligations | Full FTA compliance | Full FTA compliance (same as mainland) |

| Tourism Fees | Emirate-specific rates apply | Same emirate rates apply |

| Annual Audit | Mandatory (Federal Law) | Mandatory (free zone authority) |

| IFRS Reporting | Mandatory | Mandatory |

| ESR Obligations | Applicable where relevant | Applicable where relevant |

| UBO Filing | Mandatory with the emirate authority | Mandatory with the free zone authority |

| Management Fee Deductibility | Arm’s length required | Arm’s length required; transfer pricing rules apply |

Free zone hotels must be particularly careful about the distinction between qualifying and non-qualifying income under the UAE Corporate Tax law. A hotel within a free zone that accepts bookings from UAE mainland residents or operates a restaurant open to the public may generate income that does not qualify for the 0% rate.