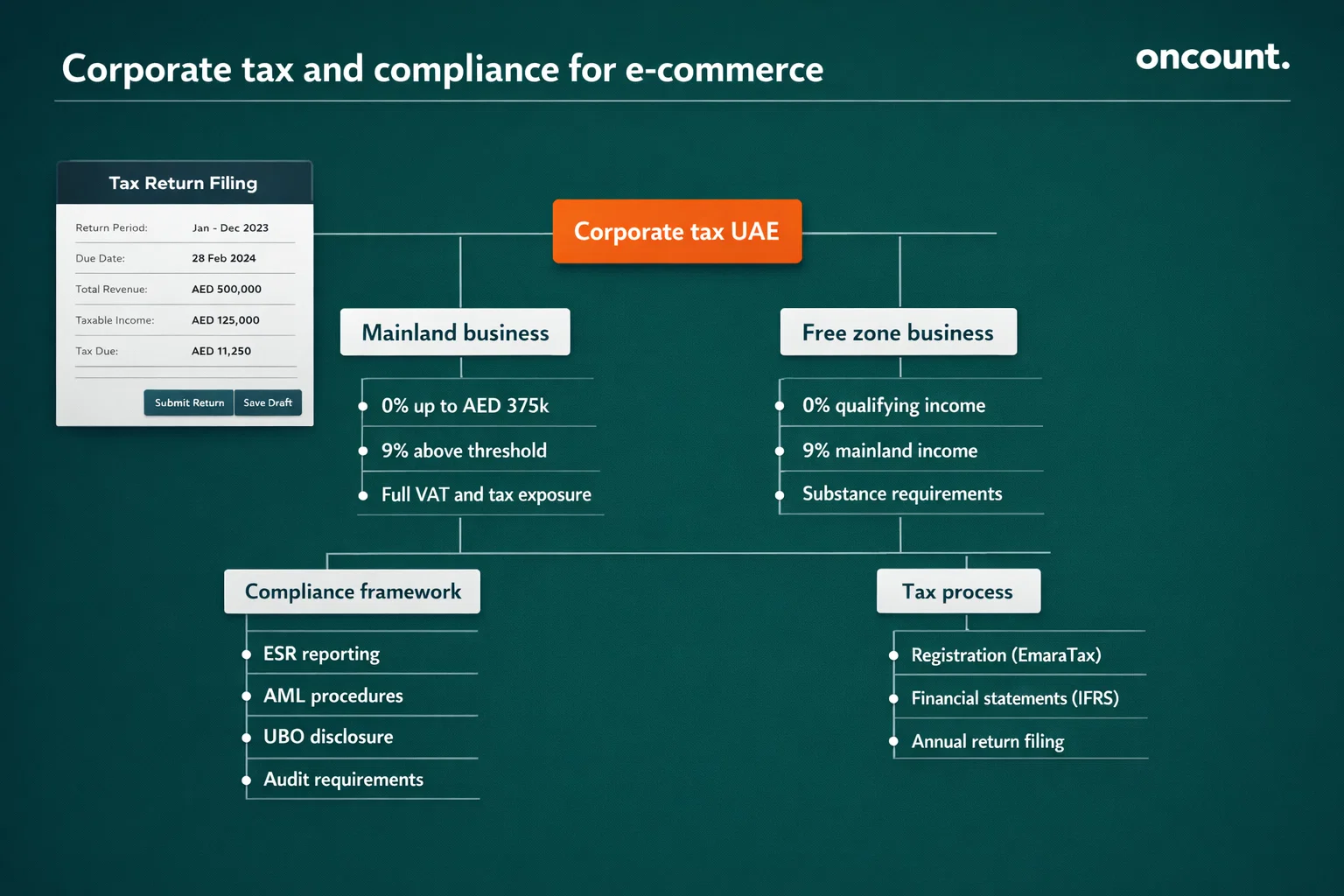

Key Takeaways

- E-commerce companies must maintain IFRS-compliant accounting records with a minimum five-year retention period for VAT documentation and seven years for corporate tax records

- UAE VAT registration becomes mandatory when annual taxable supplies exceed AED 375,000, with immediate registration required for non-resident digital service providers

- Corporate tax applies at 0% on income up to AED 375,000 and 9% on excess profits, with Free Zone entities potentially qualifying for 0% tax on qualifying income

- Multi-currency accounting must follow IAS 21 standards, translating all foreign transactions to AED at spot rates on transaction dates

- Payment gateway reconciliations require daily matching of net settlements to gross sales, accounting for merchant fees and VAT components separately

- Inventory valuation follows FIFO or weighted-average methods, with import costs including customs duties (5% standard rate) and import VAT capitalized into inventory

- E-invoicing compliance becomes mandatory starting July 2026 for businesses with annual turnover exceeding AED 50 million, with full rollout by mid-2027

Overview of Accounting Requirements in the UAE for E-commerce Companies

The UAE Commercial Companies Law (Federal Law No. 32 of 2021) requires all commercial entities to maintain systematic accounting records. E-commerce businesses in Dubai must comply with bookkeeping obligations regardless of structure, including sole proprietorships, LLCs, and free zone entities. The Federal Tax Authority enforces compliance under the Tax Procedures Law (Federal Decree-Law No. 7 of 2017), ensuring accurate records for VAT and corporate tax.

Online retailers must retain accounting documentation for at least five years from VAT filing, while corporate tax rules extend this period to seven years. According to UAE Ministry of Finance guidance (2023), records must be maintained in Arabic or English and remain accessible for FTA inspection. Digital records are legally valid if supported by proper data security and backup systems.

E-commerce companies face additional challenges due to high transaction volumes across multiple channels. Mainland businesses licensed by Dubai’s Department of Economic Development must track transactions across platforms such as Amazon, Noon, and proprietary websites. Free zone entities in locations like Dubai CommerCity, Dubai Internet City, and DMCC follow the same tax rules but benefit from simplified licensing and potential tax advantages.

Key additional obligations:

- inventory control and stock movement tracking

- compliance with UAE Data Protection Law

- documentation of payment processing

- adherence to Central Bank regulations for cross-border transactions

These requirements apply to dropshipping models, fulfillment-based retailers, and digital product providers.

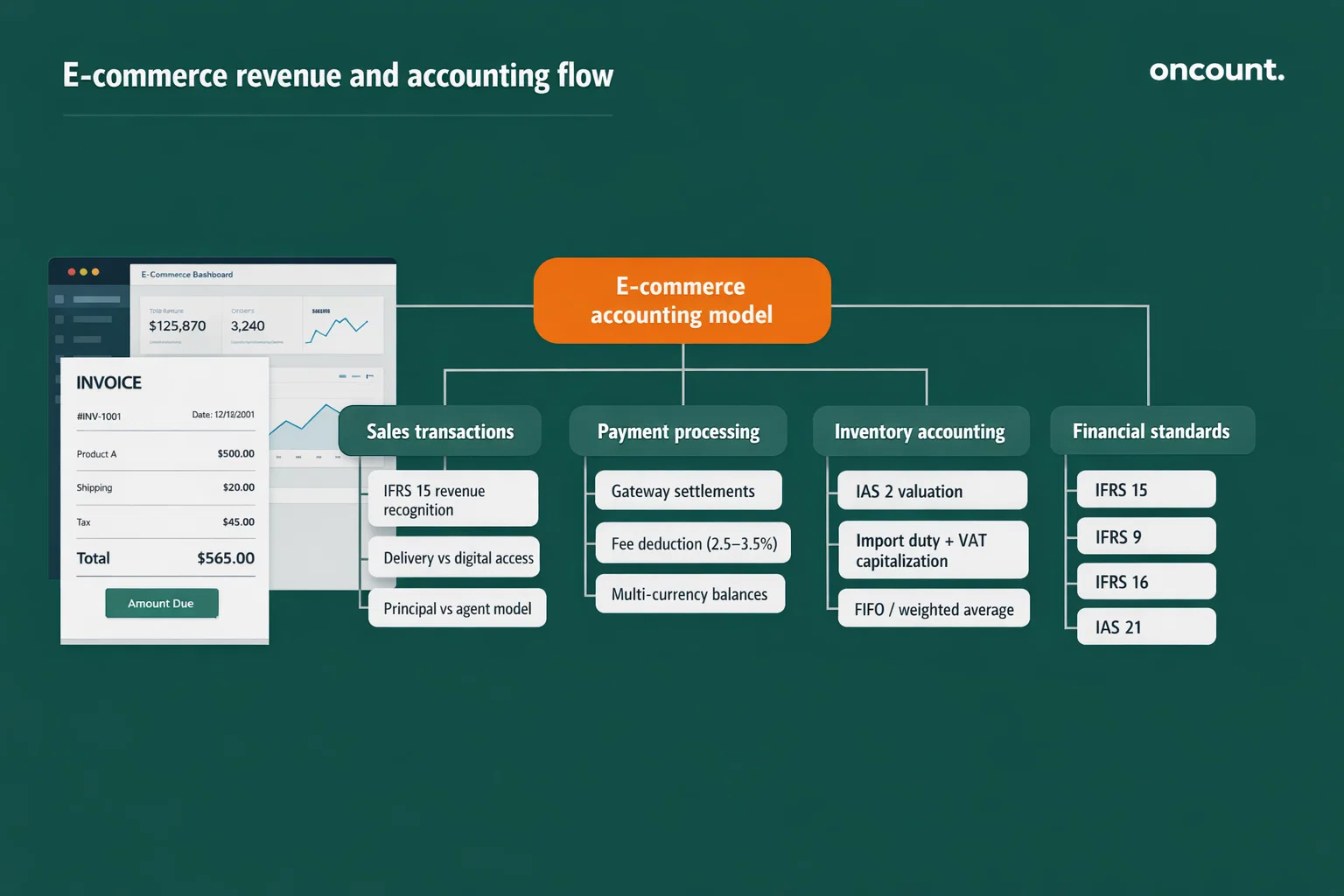

IFRS Application for E-commerce Companies

International Financial Reporting Standards form the mandatory accounting basis for all UAE e-commerce entities preparing financial statements. The UAE Cabinet Resolution No. 44 of 2023 confirms IFRS adoption for corporate tax calculations, requiring online retailers to align their books with global accounting standards rather than simplified cash-basis methods.

IFRS 15 Revenue from Contracts with Customers governs how e-commerce businesses recognize sales. Revenue recognition occurs when control of goods or services transfers to the customer—typically upon delivery for physical products or immediate download for digital goods. Online retailers selling through marketplaces must determine whether they act as principal (recognizing gross sales) or agent (recognizing net commission), directly impacting reported turnover and VAT calculations. A Dubai-based electronics retailer shipping AED 1 million in products through Amazon while paying AED 150,000 in marketplace fees must recognize AED 1 million revenue and AED 150,000 expenses if operating as principal, whereas an agent model would report only AED 150,000 net revenue.

IFRS 9 Financial Instruments applies to e-commerce companies holding foreign currency balances or offering customer financing options. Payment gateway accounts denominated in USD, EUR, or GBP require classification as financial assets measured at amortized cost. Expected credit loss provisioning becomes mandatory when online retailers extend payment terms beyond standard card processing—relevant for B2B e-commerce platforms offering net-30 or net-60 payment arrangements to corporate buyers.

IFRS 16 Leases impacts e-commerce businesses leasing warehouse space, fulfillment centers, or office facilities. Operating leases exceeding 12 months must appear on the balance sheet as right-of-use assets with corresponding lease liabilities. A three-year warehouse lease in Dubai Logistics City valued at AED 500,000 annually generates a right-of-use asset of approximately AED 1.4 million (present value of future payments), affecting both asset base and debt ratios used in financial analysis.

IAS 21 The Effects of Changes in Foreign Exchange Rates establishes translation rules for multi-currency operations. E-commerce platforms selling globally must translate foreign sales to AED at transaction-date spot rates. Unrealized gains or losses on unsettled foreign receivables or payables must be recognized in profit or loss at each reporting period.The UAE Dirham’s peg to USD (3.6725 rate) stabilizes most international transactions, but sales in EUR, GBP, or other currencies expose businesses to exchange rate volatility requiring systematic hedging or acceptance of translation adjustments.

IAS 2 Inventories dictates valuation methods for e-commerce stock. Cost includes purchase price, import duties, freight charges, and other costs necessary to bring inventory to its present location and condition. Dubai-based online retailers importing goods from China must capitalize 5% customs duty and 5% import VAT into inventory cost basis. Net realizable value testing at period-end requires write-downs for slow-moving or damaged stock—a critical consideration for fashion and electronics e-tailers facing rapid obsolescence.

Bookkeeping Framework and Financial Records Structure

E-commerce accounting systems must handle high transaction volumes, multiple payment channels, and complex inventory flows while maintaining FTA-compliant audit trails. The general ledger serves as the central data repository, structured through a chart of accounts adapted to online retail operations.

Chart of Accounts Structure for E-commerce

Asset accounts include bank balances segmented by currency (AED, USD, EUR) and payment processors such as Stripe or PayPal. Inventory must be classified into goods in transit, warehouse stock, and fulfillment center holdings. Accounts receivable tracks amounts due from marketplaces and customers, while VAT recoverable records input tax pending offset.

Liabilities include:

- VAT payable

- customs duties

- marketplace settlement balances

- advance customer payments

- deferred revenue (gift cards, loyalty programs)

- accounts payable (segmented into local and international suppliers)

Revenue accounts require segmentation by sales channel, product category, and VAT treatment. This structure supports accurate tax reporting and analytical insights. Cost of goods sold mirrors revenue categories, enabling margin analysis across channels and product lines.

Operating expenses include:

- payment gateway fees (2.5–3.5%)

- marketplace commissions (10–20%)

- digital advertising

- shipping costs

- software subscriptions

- third-party logistics services

Supporting Documentation Requirements

Tax invoices must meet UAE VAT standards, including supplier details, TRN, customer data, pricing, VAT amount, and date. Domestic invoices require bilingual headers. Most e-commerce systems automate invoice generation through integration with accounting platforms.

Procurement and import documentation—purchase orders, supplier invoices, customs declarations—support inventory records and input VAT claims. UAE Customs systems enable direct data exchange with the FTA for verification.

Bank statements and payment processor reports require regular reconciliation. Platforms such as Stripe or PayPal provide detailed breakdowns of sales, refunds, fees, and settlements. Inconsistencies between platform data and accounting records increase audit risk and potential penalties.

Digital Record-Keeping Systems

Cloud-based accounting systems provide real-time visibility, integration with sales channels, and multi-user access. Solutions must support Arabic language requirements, AED as the functional currency, multi-currency transactions, and FTA-compliant VAT reporting formats, including the Financial Audit File.

Data retention policies require secure storage for up to seven years. Automated daily backups in separate locations reduce operational risks. Access controls and audit logs ensure compliance with UAE Data Protection Law when processing financial and customer data.

Financial Statements Preparation Requirements

E-commerce companies in the UAE must prepare full financial statements in accordance with IFRS. The standard package includes a balance sheet, profit and loss statement, cash flow statement, and notes, each supporting compliance and financial analysis.

Balance Sheet Components

The balance sheet reflects financial position at a specific date. Current assets include multi-currency cash balances, receivables from marketplaces and customers, inventory valued at the lower of cost or net realizable value, and prepaid expenses. Non-current assets cover leased warehouse rights-of-use, IT equipment, and capitalized development costs under IAS 38.

Current liabilities include supplier payables, VAT payable net of input tax, customs duties, marketplace settlements, deferred revenue, and short-term lease obligations. Non-current liabilities consist of long-term leases and financing. Equity includes share capital, statutory reserves, retained earnings, and foreign currency translation adjustments.

Profit and Loss Statement Structure

The income statement begins with revenue segmented by channel and product category. Returns, marketplace commissions, and processing fees are deducted to determine net revenue. Cost of goods sold includes procurement costs, import duties, logistics, and fulfillment expenses.

Gross profit indicates operational efficiency before expenses. Operating costs include marketing, salaries, software, warehousing, depreciation, and administrative overhead. Non-operating items include foreign exchange differences and financial income or expenses.

Cash Flow Statement Preparation

The cash flow statement uses the indirect method, reconciling net profit with cash movements. Operating activities adjust for non-cash items and working capital changes. Investing activities reflect capital expenditures, while financing activities include capital injections, dividends, and lease payments under IFRS 16.

E-commerce companies often experience negative operating cash flow during expansion due to inventory buildup and marketing spend. Favorable cash cycles, where marketplace payments precede supplier obligations, improve liquidity.

Notes to Financial Statements

Disclosure notes outline accounting policies, assumptions, and additional details. Key disclosures include revenue breakdowns, inventory valuation methods, related party transactions, contingent liabilities, and post-reporting events.

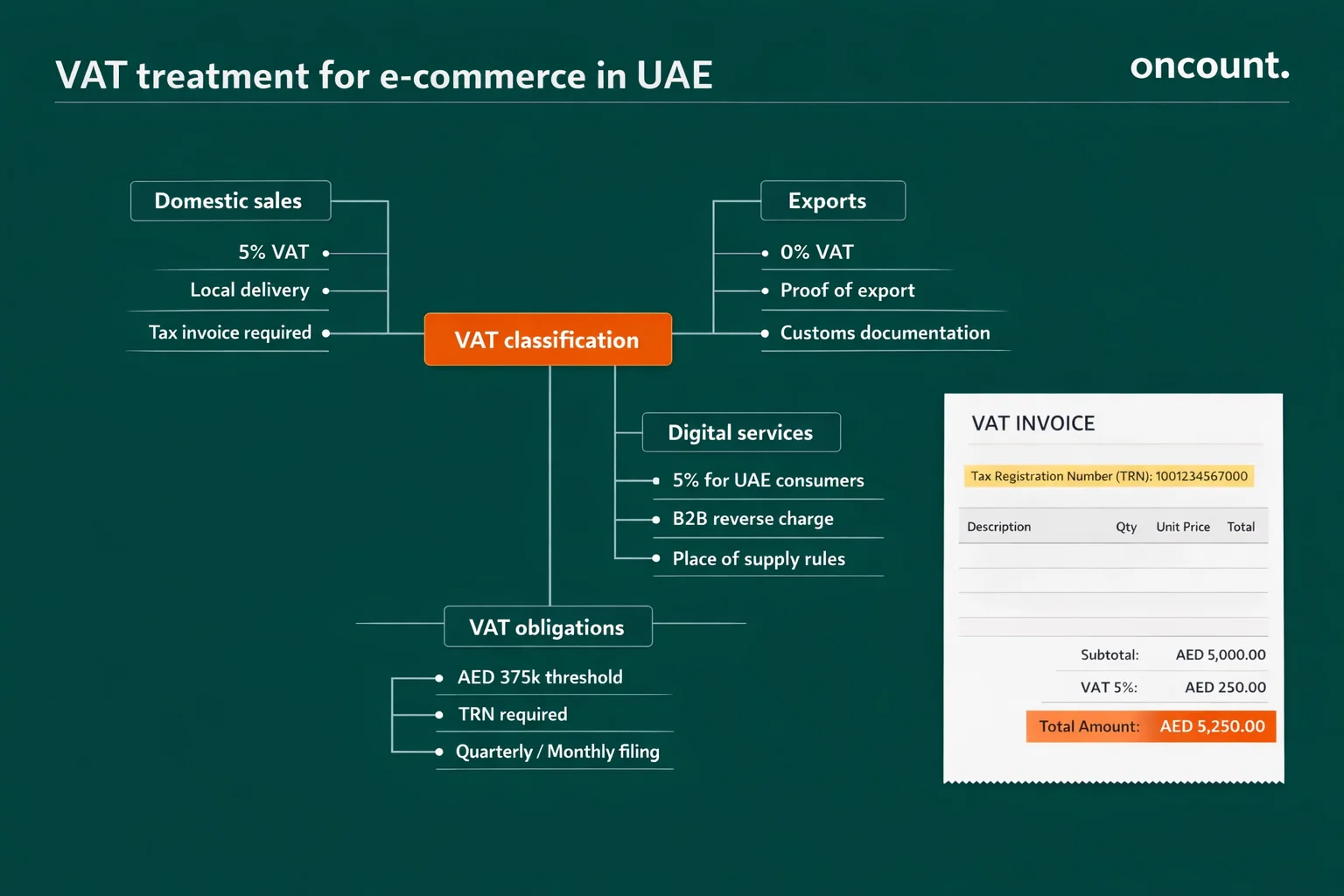

VAT Compliance for E-commerce Companies in the UAE

Value Added Tax regulations under Federal Decree-Law No. 8 of 2017 impose comprehensive obligations on online retailers regardless of their physical presence or operational structure. The Federal Tax Authority administers VAT through the EmaraTax portal, requiring systematic tracking of output tax on sales, input tax on purchases, and accurate reporting across diverse e-commerce transaction types.

VAT Registration Thresholds and Requirements

Mandatory registration applies when taxable supplies exceed AED 375,000 within any rolling 12-month period or are expected to exceed this threshold in the next 30 days. Voluntary registration becomes available at AED 187,500 of taxable supplies. Non-resident businesses making taxable supplies to UAE customers must register immediately regardless of turnover—particularly relevant for international digital service providers selling software, subscriptions, or downloadable content to UAE consumers.

The registration process through EmaraTax requires submission of trade license, Emirates ID or passport copies for owners, bank account details, and estimated annual turnover. Processing typically completes within 20 business days, after which the FTA issues a Tax Registration Number (TRN) that must appear on all tax invoices. E-commerce businesses should register proactively before crossing thresholds to avoid penalties for late registration, which start at AED 10,000.

Output VAT Treatment for Different Sale Types

Domestic sales of physical goods delivered within the UAE are standard-rated at 5%. An online electronics retailer selling a laptop for AED 3,000 charges AED 150 VAT (5% of AED 3,000), collecting AED 3,150 total from the customer. The VAT invoice must detail the net amount, VAT percentage, VAT amount in Dirhams, and total consideration.

Zero-rated supplies include exports of goods to international destinations outside the GCC. Documentation requirements include customs export declarations, shipping bills of lading or airway bills, and proof of payment from foreign customers. A Dubai-based fashion e-tailer shipping orders to European customers applies 0% VAT on these sales while maintaining the right to recover input VAT on related costs—creating potential refund positions when export sales dominate.

Digital goods and services follow place-of-supply rules under UAE VAT Executive Regulations. B2C supplies of electronic services (streaming content, software downloads, mobile apps, cloud storage) to UAE-based consumers are taxable at 5% regardless of supplier location. International platforms like Netflix, Spotify, and Adobe must register for UAE VAT and charge tax on subscriptions to UAE users. B2B digital services may qualify for reverse charge treatment where the UAE business customer accounts for VAT rather than the foreign supplier.

Input VAT Recovery and Restrictions

E-commerce businesses recover input VAT on purchases directly attributable to taxable supplies. Recoverable amounts include VAT on inventory purchases, import VAT paid at customs, shipping costs for taxable goods, payment processing fees, marketing and advertising expenses, and professional fees for accounting or legal services. The input tax must be supported by valid tax invoices or customs documentation showing the supplier’s TRN and VAT amount.

Non-recoverable input VAT includes tax on blocked expenses specified in UAE VAT law—primarily entertainment, personal expenses, and specific motor vehicle costs. Input tax on business assets or goods used for both taxable and exempt supplies requires apportionment based on proportional use. The partial use of passenger vehicles for personal purposes by owner-managers creates restriction scenarios that require careful calculation.

Import VAT paid on goods entering UAE free zones destined for export remains recoverable even though the zone import itself may be zero-rated. This mechanism prevents tax cascading while maintaining FTA oversight of international trade flows. E-commerce fulfillment centers in Dubai South or Jebel Ali Free Zone must track import VAT payments and recovery claims with precision to optimize working capital.

VAT Return Filing and Payment Obligations

Tax periods operate quarterly for most small and medium e-commerce businesses, with returns due by the 28th day following the period end. Large enterprises exceeding AED 150 million annual turnover file monthly returns. The VAT return calculates net tax payable (output VAT less input VAT) or refund due, with payment required by the same deadline. Electronic filing through EmaraTax is mandatory—paper returns are not accepted.

The return format follows the standardized VAT 201 form containing 14 boxes covering standard-rated supplies, zero-rated exports, exempt supplies, output VAT, input VAT recoverable, and net VAT due. Supporting schedules detail tourism refunds, capital assets purchases, and corrections from prior periods. E-commerce businesses with complex operations spanning multiple categories must maintain detailed workpapers supporting each return line item.

Late filing triggers administrative penalties of AED 1,000 for the first offense, increasing to AED 2,000 for subsequent violations. Late payment incurs interest at 4% annual percentage rate calculated daily from the due date until payment receipt. Voluntary disclosure of errors before FTA detection qualifies for reduced penalties under the penalty mitigation framework introduced in 2023.

Marketplace and Deemed Supplier Rules

Special provisions apply when non-resident sellers use UAE-based fulfillment services. Under Article 10 of the UAE VAT Executive Regulations, electronic marketplaces become “deemed suppliers” responsible for VAT when facilitating sales of goods physically located in the UAE by non-resident vendors. Amazon FBA sellers storing inventory in Dubai warehouses shift VAT responsibility to Amazon, which collects and remits tax on sales to UAE customers.

This mechanism simplifies compliance for international sellers while ensuring VAT collection on cross-border transactions. The marketplace issues tax invoices, files returns, and remits VAT to FTA on behalf of non-resident sellers. UAE-based marketplace sellers retain direct VAT obligations on their sales, with marketplace commissions subject to separate VAT treatment as agent services.

Corporate Tax Framework for E-commerce Businesses in the UAE

Federal Decree-Law No. 47 of 2022 establishes the UAE’s first federal corporate tax regime, effective from June 1, 2023 for financial years beginning on or after that date. E-commerce businesses face a two-tier rate structure combined with complex rules for free zone entities, transfer pricing obligations, and substance requirements affecting online retailers across different jurisdictions within the UAE.

Tax Rates and Threshold Structure

The corporate tax applies a 0% rate on taxable income up to AED 375,000, with a 9% rate on profits exceeding this threshold. This dual-rate structure provides relief for small e-commerce startups while ensuring larger operations contribute to federal revenues. A Dubai-based online retailer generating AED 1 million taxable profit pays zero tax on the first AED 375,000 and AED 56,250 (9% of AED 625,000) on the excess, resulting in an effective tax rate of 5.625% on total profit.

Large multinational enterprises meeting specified criteria face an additional 15% minimum tax under Pillar Two rules implementing global tax reform. This affects major international e-commerce platforms but remains largely irrelevant for domestic online retailers and regional players below EUR 750 million consolidated group revenue.

Taxable Income Calculation Principles

Taxable income begins with accounting profit calculated under IFRS, adjusted for tax-specific rules. The starting point uses audited financial statements as the basis for corporate tax computations, establishing a direct linkage between accounting practices and tax obligations. E-commerce businesses must maintain consistency between financial reporting and tax positions to avoid disputes during FTA examinations.

Deductible expenses include cost of goods sold, employee salaries and benefits, rent for warehouses and offices (including IFRS 16 lease interest), depreciation on capital assets following UAE tax depreciation rules, marketing and advertising costs, professional fees for accounting and legal services, and interest expense within thin capitalization limits. The Federal Tax Authority’s Corporate Tax Guide clarifies that ordinary and necessary business expenses incurred wholly and exclusively for generating taxable income qualify for a deduction.

Non-deductible expenses include fines and penalties imposed by regulatory authorities, costs related to exempt income, entertainment expenses exceeding specified limits, and non-arm’s length payments to related parties that fail transfer pricing tests. Charitable donations exceeding regulatory limits and certain reserves or provisions not meeting recognition criteria also face disallowance. E-commerce businesses must carefully document expense purposes to substantiate deductibility during audits.

Free Zone Tax Advantages

Qualifying Free Zone Persons (QFZPs) eligible for preferential treatment pay 0% corporate tax on qualifying income—defined as income from transactions with other free zone entities or from activities outside the UAE, provided adequate substance exists. A Dubai CommerCity e-commerce company selling exclusively to international markets through its free zone entity potentially pays zero UAE corporate tax on export profits while maintaining recovery rights for input VAT.

Non-qualifying income—such as UAE mainland sales—faces the standard 9% rate even for free zone entities. This bifurcation requires meticulous tracking of income sources, with separate accounting for qualifying versus non-qualifying revenue streams. Free zone companies must file detailed returns demonstrating which income qualifies for 0% treatment, supported by customer location data, transaction documentation, and substance evidence.

Substance requirements under the Economic Substance Regulations (ESR) overlay free zone tax benefits. E-commerce distribution businesses—categorized as relevant activities—must demonstrate adequate operations in the UAE, including a qualified workforce, appropriate physical premises, and actual conduct of core income-generating activities. Token-free zone presence with all substantive operations performed elsewhere risks losing preferential tax treatment and potentially facing penalties under the ESR framework.

Transfer Pricing Obligations

Related party transactions—common when e-commerce businesses operate across multiple UAE entities or have foreign parent companies—must meet arm’s length principles following OECD Transfer Pricing Guidelines. UAE Corporate Tax Law requires taxpayers to maintain transfer pricing documentation when connected person transactions exceed AED 40 million or when specific related party payments exceed AED 500,000 annually.

Documentation requirements include functional analysis describing each entity’s activities and risks, economic analysis supporting pricing methodology, and financial data demonstrating arm’s length outcomes. Master file and local file preparation becomes mandatory for large enterprises meeting revenue thresholds (consolidated group revenue exceeding AED 3.15 billion or UAE revenue above AED 200 million). E-commerce groups with shared services arrangements, intellectual property licenses, or inventory transfer pricing between entities face heightened scrutiny requiring robust documentation.

Advance Pricing Agreements (APAs) provide certainty by pre-approving transfer pricing methodologies with the Federal Tax Authority. Available from late 2025, APAs particularly benefit e-commerce businesses with complex intra-group arrangements seeking to avoid future disputes over arm’s length pricing of platform fees, royalty arrangements, or cost allocation methodologies.

Accounting for Revenue and Expenses in E-commerce Operations

E-commerce business models create unique revenue recognition patterns and expense structures requiring specialized accounting treatment. The diversity of sales channels, payment methods, and fulfillment models demands flexible accounting frameworks that capture operational complexity while maintaining IFRS compliance.

Revenue Recognition Timing and Measurement

Revenue from online sales of physical goods is recognized when control transfers to the customer—typically upon delivery to the shipping carrier for FOB shipping point terms or upon customer receipt for delivered-duty-paid arrangements. A Dubai electronics retailer using Aramex for UAE deliveries recognizes revenue when the carrier scans packages, while international shipments via DHL recognize revenue upon proof of delivery abroad. This timing affects period-end cutoff procedures and requires systematic integration between e-commerce platforms and accounting systems.

Digital product sales (software downloads, e-books, music files, online courses) recognize revenue upon customer access or download completion. Subscription-based digital services spread revenue over the subscription period, creating deferred revenue liabilities for prepaid annual subscriptions. A SaaS e-commerce platform charging AED 12,000 annually recognizes AED 1,000 monthly revenue, deferring the unearned portion as a liability until services are provided.

Marketplace commission models require principal versus agent analysis under IFRS 15. E-commerce businesses acting as principals (taking inventory risk, setting prices, and being responsible for fulfillment) recognize gross sales revenue. Companies operating as agents (merely facilitating transactions between buyers and third-party sellers) recognize net commission revenue. This distinction fundamentally alters reported turnover and impacts VAT treatment, bank lending capacity, and marketplace positioning.

Multi-Currency Transaction Recording

International sales denominated in foreign currencies translate to AED at transaction-date exchange rates following IAS 21 standards. A USD 1,000 sale recorded when the exchange rate is 3.67 books as AED 3,670 revenue. Subsequent currency fluctuations before cash collection create foreign exchange gains or losses recognized in profit or loss. If the customer pays when the rate moves to 3.70, the business receives AED 3,700, recognizing AED 30 as foreign exchange gain.

Payment processor accounts holding balances in USD, EUR, or GBP require period-end revaluation. Unrealized gains or losses from translating foreign currency financial assets to closing-date rates flow through profit or loss, creating earnings volatility for e-commerce businesses with substantial foreign currency exposure. Hedging strategies using forward contracts or natural hedges (matching foreign currency revenues with foreign currency expenses) mitigate this volatility.

Payment Gateway Fee Treatment

Processing fees charged by Stripe, PayPal, or local providers represent operating expenses deducted from revenue to calculate gross profit. The fee structure typically combines percentage charges (2.5-3.5% of transaction value) plus fixed per-transaction amounts. A AED 1,050 sale (including AED 50 VAT) with 2.9% + AED 1 fee incurs AED 31.45 in processing costs [(1,050 × 0.029) + 1], with the merchant receiving net settlement of AED 1,018.55.

Accounting entries record gross revenue, full VAT, and processing expense separately rather than netting settlement amounts. This gross presentation provides accurate expense visibility and ensures proper VAT accounting on the full transaction value rather than net proceeds. Chart of accounts should include dedicated expense accounts for payment processing to facilitate margin analysis and channel profitability assessment.

Refund and Chargeback Accounting

Product returns and refunds reverse original sale entries, reducing revenue and VAT payable. An AED 525 refund for a returned AED 500 item (plus AED 25 VAT) records as a debit to Sales Returns and VAT Payable, with a credit to Accounts Receivable or Bank, depending on whether the original transaction has settled. Refund patterns by product category inform inventory planning and highlight quality or description issues driving returns.

Chargebacks from disputed credit card transactions create additional complexity. Unlike voluntary refunds, chargebacks involve payment processor intervention, typically incurring AED 50-100 chargeback fees in addition to reversing sale proceeds. High chargeback rates (exceeding 1% of transactions) trigger enhanced monitoring from payment processors, potentially leading to account termination or reserve requirements. E-commerce businesses must track chargeback reasons, implement fraud prevention measures, and maintain evidence (tracking confirmations, customer communications) to dispute invalid chargebacks.

Shipping Revenue and Expense Allocation

Shipping fees charged to customers represent separate performance obligations requiring revenue recognition when delivery occurs. Free shipping promotions constitute sales discounts, reducing the transaction price allocated to goods sold. Actual shipping costs paid to carriers (Aramex, Emirates Post, DHL) are operating expenses, with the spread between shipping revenue and actual costs contributing to gross margin.

Accounting systems should track shipping profitability separately, particularly for businesses using shipping charges as revenue drivers. A merchant charging AED 25 shipping while incurring AED 15 actual costs generates AED 10 gross profit contribution from delivery services. Conversely, free shipping with AED 15 fulfillment costs per order effectively reduces product margins, requiring adjustment to pricing strategy or order minimums to maintain profitability.

Regulatory Compliance and Reporting Obligations

E-commerce businesses in the UAE operate within a comprehensive regulatory framework extending beyond taxation to encompass economic substance, anti-money laundering controls, beneficial ownership transparency, and consumer protection measures. These overlapping compliance requirements demand systematic controls and documentation practices supporting both FTA obligations and broader regulatory objectives.

Economic Substance Regulations (ESR) Impact

The UAE Economic Substance Regulations (Cabinet Resolution No. 57 of 2020) apply to e-commerce businesses conducting relevant activities—particularly distribution and service center operations common in online retail fulfillment. Companies storing inventory in UAE warehouses and distributing to regional or international markets potentially fall under the ESR scope, requiring a demonstration of adequate local presence and activity.

ESR notification filing occurs within six months of the financial year-end through the Federal Tax Authority portal. Distribution businesses must submit detailed ESR reports within 12 months demonstrating core income-generating activities performed in the UAE, adequate qualified employees, appropriate annual operating expenditure relative to activity level, and physical presence, including offices or warehouses. Failure to file ESR notifications or reports triggers penalties starting at AED 20,000 for late submission and escalating to AED 400,000 for non-compliance after three years.

Free zone e-commerce entities benefit from presumed ESR compliance if maintaining adequate substance within their licensed free zone. However, shell companies lacking genuine operational activity face potential substance challenges regardless of free zone location. The test focuses on actual business conduct rather than mere licensing presence—requiring payroll records, rental agreements, utility bills, and operational evidence supporting substance claims.

Anti-Money Laundering (AML) Requirements

E-commerce platforms processing customer payments fall under AML obligations enforced by the UAE Central Bank and Financial Intelligence Unit. Customer due diligence procedures must verify identity for transactions exceeding specified thresholds, with enhanced due diligence for high-risk customers or jurisdictions. Online retailers accepting large-value orders (exceeding AED 55,000) must implement customer verification procedures including Emirates ID validation for UAE residents or passport verification for international customers.

Suspicious transaction reporting obligations require e-commerce businesses to monitor for unusual patterns—such as multiple small transactions designed to avoid detection thresholds, purchases using multiple payment cards, or orders shipped to high-risk jurisdictions. Designated non-financial businesses and professions (DNFBPs) regulations extend AML obligations beyond traditional financial institutions to include certain e-commerce activities, particularly luxury goods merchants and businesses processing substantial cash-equivalent payments.

Record retention for AML purposes extends five years beyond relationship termination, encompassing customer identification documentation, transaction records, and internal suspicious activity evaluations. This overlaps with tax record retention periods but potentially extends beyond them for customer relationship documentation.

Ultimate Beneficial Owner (UBO) Disclosure

Cabinet Resolution No. 58 of 2020 requires all UAE companies to maintain registers identifying ultimate beneficial owners—individuals ultimately controlling 25% or more of shares or exercising control through other means. E-commerce businesses structured as limited liability companies must file UBO information through the relevant economic department (DED for Dubai mainland, specific free zone registries for free zone entities).

UBO reporting encompasses direct and indirect ownership structures, requiring disclosure of intermediate holding companies and trust arrangements. Multi-tiered e-commerce groups with foreign parent companies must trace ownership through all layers to identify natural persons meeting UBO criteria. Annual confirmation of UBO information accuracy is mandatory, with updates required within 15 days of any changes in beneficial ownership.

Penalties for non-compliance include fines up to AED 100,000 and potential license suspension for repeated violations. The Central Bank maintains the UBO register for financial institutions, while economic departments administer registers for commercial companies. E-commerce platforms and payment processors increasingly verify supplier UBO information as part of merchant onboarding procedures, requiring sellers to maintain accurate disclosure for ongoing payment processing access.

Audit Requirements for E-commerce Companies in the UAE

External audit obligations for UAE e-commerce businesses depend on legal structure, turnover, and jurisdiction—with mainland companies, free zone entities, and financial free zone businesses facing different requirements. The UAE Ministry of Finance maintains the register of approved auditors authorized to conduct statutory audits, and firms must be licensed accounting professionals meeting educational and experience standards.

Mandatory Audit Thresholds and Exemptions

UAE Commercial Companies Law generally requires annual audits for all limited liability companies and joint stock companies regardless of size. However, the Ministry of Finance introduced small business exemptions allowing qualifying entities to waive audit requirements when meeting criteria, including annual revenue below AED 50 million, total assets under AED 25 million, and fewer than 50 employees. E-commerce startups and small online retailers often qualify for exemption, substantially reducing compliance costs during growth phases.

Free zone regulations impose zone-specific audit requirements. Dubai CommerCity, Dubai Multi Commodities Centre (DMCC), and Jebel Ali Free Zone (JAFZA) mandate annual audited financial statements for all license holders regardless of turnover. DIFC and ADGM companies follow their respective regulatory frameworks, requiring audited IFRS financial statements reviewed by DIFC or ADGM-registered audit firms. These financial free zones maintain separate audit firm registers with stringent qualification requirements exceeding mainland standards.

Corporate tax regulations effectively mandate audits for businesses exceeding audit exemption thresholds, as the Federal Tax Authority requires tax returns to be based on audited financial statements when filing obligations apply. E-commerce companies approaching AED 50 million annual revenue should anticipate audit requirements even if technically qualifying for exemptions, as FTA compliance verification increasingly relies on audited figures for tax assessment purposes.

Audit Scope and Focus Areas

Statutory audits examine financial statements for compliance with IFRS standards and applicable UAE regulations. For e-commerce businesses, auditors focus on revenue recognition cutoff testing (ensuring sales are recorded in appropriate periods), inventory existence and valuation (often through observation of cycle counts or year-end stock takes), accounts receivable collectability (particularly marketplace settlement receivables), and VAT calculations underlying tax liability positions.

Multi-currency operations receive scrutiny regarding translation methodology, exchange rate sources, and foreign exchange gain/loss calculations. Auditors test currency balances through bank confirmations and verify translation rate application against the Central Bank of UAE published rates or Bloomberg/Reuters data. Material currency misstatements directly impact reported profit and consequent tax obligations.

Related party transactions undergo detailed examination, with auditors verifying arm’s length pricing, adequate disclosure in financial statement notes, and transfer pricing documentation supporting cross-border payments to associated enterprises. E-commerce groups with shared services arrangements, intellectual property licensing, or inter-company trading must maintain transaction documentation supporting audit verification and potential FTA transfer pricing examinations.

Internal Controls and Audit Readiness

E-commerce businesses benefit from implementing robust internal controls before audit engagement, accelerating audit completion, and potentially reducing fees. Key controls include segregation of duties between sales recording, cash collection, and reconciliation functions; daily reconciliation of payment gateway settlements to recorded sales; regular inventory counts with investigation of discrepancies; and approval workflows for supplier payments exceeding specified thresholds.

Technology controls become critical given high transaction volumes and reliance on integrated systems. Access controls restricting accounting software permissions to authorized personnel, automatic backup procedures with off-site storage, and audit logging of system changes satisfy auditor expectations for IT general controls. Integration testing between e-commerce platforms (Shopify, WooCommerce, custom systems) and accounting software ensures transaction completeness and accuracy.

Documentation organization significantly impacts audit efficiency. Businesses maintaining organized digital filing systems with tax invoices, customs declarations, bank statements, and contracts readily accessible complete audits faster than those requiring extensive document searches. Cloud storage with intuitive folder structures and naming conventions reduces auditor hours spent on information requests, directly translating to lower audit fees.

Industry-Specific Accounting Considerations for E-commerce Companies

Online retail operations introduce specialized accounting challenges beyond traditional brick-and-mortar commerce. The unique characteristics of digital sales channels, virtual inventory management, and technology-dependent operations require accounting approaches adapted to e-commerce realities.

Marketplace Seller Accounting and Reconciliation

E-commerce businesses selling through Amazon, Noon, or other marketplaces face complex reconciliation requirements. Marketplaces typically pay sellers periodically (weekly or bi-weekly), remitting net proceeds after deducting commissions, shipping contributions, storage fees, and advertising costs. A AED 50,000 sales week might result in AED 35,000 net settlement after 20% marketplace fees (AED 10,000), FBA fulfillment charges (AED 3,000), and sponsored product advertising (AED 2,000).

Accounting entries must decompose bundled settlements into component parts: gross revenue (AED 50,000), cost of sales, marketplace commissions as operating expense (AED 10,000), fulfillment fees (AED 3,000), and advertising expense (AED 2,000). This granular recording enables accurate gross margin calculation and channel profitability analysis. Automated data feeds from marketplace APIs into accounting systems reduce manual entry errors and ensure transactional completeness.

Marketplace reserves and chargebacks create timing mismatches between sales recognition and cash collection. Platforms often hold reserves (10-30% of sales) for 90-180 days covering potential refunds or chargebacks. These reserves are recorded as accounts receivable upon sale, with cash recognition deferred until reserve release. Extended settlement cycles require careful working capital management, particularly for businesses with limited capital reserves.

Dropshipping Model Financial Treatment

Dropshipping e-commerce eliminates inventory holding, with suppliers shipping directly to customers on behalf of the retailer. This model simplifies inventory management but creates unique accounting patterns. Revenue recognition occurs upon customer order placement (control transfer), while cost of goods sold is booked when the supplier confirms shipment. Brief timing gaps between customer payment and supplier invoice settlement must be tracked.

Import VAT and customs duty responsibility depend on the shipment structure. If the UAE dropshipper acts as importer of record (supplier ships to the UAE address), the business pays import duty and VAT before customer delivery, capitalizing these costs into COGS. Alternatively, if suppliers ship internationally with the customer as the consignee, import obligations may fall on the customer—though this typically creates poor customer experiences for UAE-based buyers.

Transfer pricing considerations arise when dropshipping involves related party suppliers. The FTA examines whether margins achieved through dropshipping arrangements reflect arm’s length outcomes, particularly when related party suppliers are in low-tax jurisdictions. Documentation supporting pricing decisions becomes critical when UAE-based e-commerce platforms earn substantial margins from dropshipped goods supplied by affiliated foreign entities.

Subscription and Recurring Revenue Models

Subscription-based e-commerce (monthly product boxes, membership programs, auto-replenishment services) creates deferred revenue obligations. An AED 600 annual subscription collected upfront recognizes AED 50 monthly as subscription boxes ship or services are delivered. The unearned balance appears as deferred revenue liability on the balance sheet, systematically reducing as performance obligations are satisfied.

Subscriber acquisition costs (SAC) incurred for marketing and onboarding may qualify for capitalization under IFRS when directly attributable to obtaining specific contracts and expected to be recovered. However, most e-commerce businesses expense SAC immediately, given the difficulty of proving direct attribution and recovery probability. Tracking customer lifetime value (LTV) against SAC provides management insight even when full capitalization isn’t supported.

Churn accounting—recognizing revenue from cancelled subscriptions—requires systematic monitoring. When customers cancel mid-period, unearned revenue must be measured and potentially refunded, with appropriate VAT adjustments. High-churn periods (post-Ramadan, back-to-school season) create predictable revenue patterns requiring accurate forecasting for cash flow management.

Digital Goods and Services Revenue Recognition

E-commerce platforms selling downloadable products (software, e-books, digital art, online courses) recognize revenue upon customer access without physical fulfillment costs. Variable consideration adjustments account for refund guarantees common in digital product sales—particularly relevant for online course providers offering satisfaction guarantees or trial periods.

Licensing versus sales distinction impacts accounting treatment. Perpetual software licenses transfer control immediately, recognizing revenue upon download. Time-limited licenses or software-as-a-service arrangements spread revenue over access periods. An accounting software subscription sold for AED 1,200 annually recognizes AED 100 monthly, while a perpetual license for AED 1,200 recognizes full revenue immediately, despite potentially providing ongoing support services.

Digital services sold to international customers require a place-of-supply determination under VAT rules. Software sold to a Saudi customer for use in Saudi Arabia potentially qualifies as export (zero-rated), while the same software sold to a UAE-based business customer triggers reverse charge mechanisms. Accurate customer location tracking through IP addresses, billing addresses, and contractual terms ensures correct VAT treatment and avoids compliance penalties.

Common Accounting Challenges for E-commerce Companies

UAE online retailers frequently encounter operational and compliance difficulties stemming from business model complexity, regulatory interpretation uncertainties, and system integration limitations. Recognizing these challenges enables proactive mitigation through improved controls and professional advisory engagement.

Multi-Channel Inventory Synchronization Issues

E-commerce businesses selling across their own websites, Amazon, Noon, and physical retail simultaneously face inventory synchronization challenges. A product showing 10 units available across all channels risks overselling when simultaneous purchases occur before the inventory systems update. Accounting implications include revenue overstatement if unfulfillable sales remain recorded, excess refund provisions, and customer satisfaction impacts affecting repeat purchase rates.

Solutions require real-time inventory management systems with API connections to all sales channels, updating available quantities immediately upon each sale. Perpetual inventory systems under IAS 2 principles maintain continuous records of stock movements, with periodic physical counts verifying system accuracy. Discrepancies between physical counts and perpetual records require investigation—potential indicators of theft, damage, or system recording errors.

Payment Gateway Reconciliation Complexity

E-commerce merchants using multiple payment processors (credit cards via Network International, digital wallets via PayPal, buy-now-pay-later via Tabby, bank transfers via local accounts) face challenging reconciliation requirements. Each processor settles on different cycles (daily, weekly, bi-weekly), complicating cash flow forecasting and creating numerous reconciliation tasks. Processing fees vary by method—typically 2.5-3.5% for cards, 4-5% for PayPal, and higher rates for buy-now-pay-later services.

Automated reconciliation tools match payment processor settlements to recorded sales, flagging variances requiring investigation. Common discrepancies include processing fee calculation errors, refunds not reflected in accounting records, and chargebacks initiated by customers. Unreconciled differences accumulating over time create audit issues and potentially understate revenue or overstate assets if payments received aren’t properly recorded.

VAT Treatment Uncertainties for Cross-Border Transactions

International e-commerce sales create VAT complexities around place-of-supply determination, especially for digital services, goods in transit, and marketplace-facilitated transactions. A Dubai-based platform selling software to a Saudi business raises questions: is this an export (zero-rated), a business-to-business international supply (outside UAE VAT scope), or a UAE supply subject to 5% VAT? Incorrect treatment triggers penalties, interest, and potential audit risk.

Professional guidance from VAT specialists familiar with Federal Tax Authority positions helps navigate ambiguous scenarios. Conservative approaches presuming UAE VAT applicability when uncertainty exists minimize compliance risk but potentially overstate tax costs. Advance rulings from FTA provide definitive guidance on specific fact patterns, particularly valuable for high-volume transaction types central to the business model.

Transfer Pricing Documentation for Related Party Transactions

E-commerce groups with related entities in multiple jurisdictions face transfer pricing requirements when transactions exceed AED 40 million annually or specific connected party payments exceed AED 500,000. Common related party transactions include:

- Management service fees paid to foreign parent companies

- Trademark or technology licensing fees

- Inventory purchases from related suppliers

- Shared costs allocation for centralized services (IT, marketing, back-office)

Documentation requirements include functional analysis describing each entity’s contribution, comparability analysis benchmarking against independent third-party transactions, and financial outcome testing demonstrating arm’s length results. Small e-commerce businesses often lack resources for sophisticated transfer pricing studies, creating compliance gaps when crossing documentation thresholds. Early engagement with transfer pricing specialists before reaching thresholds enables proactive documentation and potentially optimal structure design, minimizing future compliance costs.

E-Invoicing Transition Challenges

The phased implementation of electronic invoicing through the Federal Tax Authority’s system requires technical preparation. Phase one (July 2026) mandates businesses exceeding AED 50 million turnover to issue structured electronic invoices through FTA-approved software. Phase two extends requirements to all VAT-registered businesses by mid-2027. E-commerce platforms must ensure accounting and e-commerce systems generate invoices in XML format, meeting FTA technical specifications, integrate with FTA API endpoints for invoice transmission, and maintain fallback procedures for system outages.

Investment in e-invoicing-compliant software represents a high cost for small e-commerce businesses. However, failure to comply triggers penalties starting at AED 5,000 per violation. Early adoption during pilot phases provides time for technical issue resolution before mandatory compliance deadlines, reducing implementation risk and potential penalties from technical failures during initial rollout.

Best Practices for Accounting and Financial Management

E-commerce businesses optimizing accounting practices and financial controls position themselves for sustainable growth while minimizing compliance risks. Professional accounting infrastructure establishes a foundation supporting operational scaling, investor confidence, and regulatory examination readiness.

Implement Cloud-Based Accounting Systems with E-Commerce Integration

Modern accounting platforms designed for online retail provide significant advantages over generic bookkeeping software. Zoho Books, QuickBooks Online, and Xero offer native integrations with major e-commerce platforms (Shopify, WooCommerce, Amazon), payment gateways (Stripe, PayPal), and shipping providers. These integrations automatically import sales transactions, reconcile payment settlements, and track inventory movements—eliminating manual data entry and reducing recording errors.

System selection should prioritize UAE VAT compliance features including automatic VAT calculation on sales, input VAT tracking on purchases, and FTA-compliant VAT return generation. Arabic language interface support, AED as primary currency while handling multi-currency transactions, and local customer support responsive to UAE time zones further enhance platform utility. Annual software costs (AED 1,000-5,000 for most e-commerce businesses) are substantially lower than the time saved through automation and error reduction.

Establish Daily Reconciliation Routines

Financial accuracy requires systematic daily procedures rather than month-end scrambles. Key daily reconciliation tasks include:

- Bank account reconciliation matching deposits to payment gateway settlements

- Payment gateway reconciliation, verifying recorded sales to processor reports

- Inventory movement verification, ensuring stock system updates for all sales and receipts

- Accounts receivable aging review, identifying overdue marketplace settlements or customer payments

- tracking VAT output and monitoring accumulated VAT liability for cash flow planning

Automated reconciliation features in modern accounting software flag discrepancies exceeding tolerance thresholds (e.g., AED 10 per transaction), enabling focused investigation on material variances while accepting de minimis rounding differences. Unreconciled items persisting beyond seven days should trigger escalation procedures—either resolution through additional investigation or formal recording of unexplained differences.

Maintain Separate Operating and Tax Reserve Accounts

Cash flow management for e-commerce businesses should segregate operating capital from tax obligations. A dedicated bank account accumulating VAT collected on sales ensures funds availability for quarterly or monthly VAT payments without impacting operational cash flow. Businesses collecting AED 50,000 monthly output VAT less AED 30,000 input VAT should transfer AED 20,000 monthly to the tax reserve account, maintaining a buffer for the quarter-end payment.

Similarly, corporate tax reserve accounts accumulating estimated quarterly tax obligations prevent cash shortfalls when annual tax payments fall due. E-commerce businesses projecting AED 1 million annual taxable profit should reserve approximately AED 56,250 (9% on profit above AED 375,000 threshold), ideally through monthly transfers of AED 4,688 to tax reserve accounts. This discipline separates taxation from business profit and ensures tax deadlines don’t create working capital crises.

Engage Qualified Accounting Professionals Proactively

E-commerce businesses benefit from professional accounting guidance before issues arise rather than reactive problem-solving after FTA inquiries or audit qualification. Monthly or quarterly engagement of professional accountants provides several advantages:

- Technical interpretation of UAE tax regulations applied to specific business facts

- Financial statement preparation meeting IFRS requirements and audit standards

- Tax planning identifying legitimate deductions and structure optimization opportunities

- Representation during FTA audits or inquiries reducing business disruption

Accounting firm fees vary based on transaction volume, entity complexity, and service scope. Small e-commerce businesses (under AED 5 million revenue) typically spend AED 2,000-5,000 monthly for bookkeeping, VAT compliance, and financial reporting. Larger operations exceeding AED 50 million revenue require comprehensive services including audit, tax planning, and CFO advisory, potentially costing AED 15,000-30,000 monthly but delivering proportional value through optimization and risk mitigation.

Implement Robust Internal Controls Despite Small Team Size

Small e-commerce businesses often operate with limited staff, creating segregation of duty challenges. Nevertheless, essential control procedures remain feasible:

- Dual authorization for supplier payments exceeding AED 5,000

- Monthly bank statement review by business owner independently of bookkeeper

- Surprise inventory counts by owner rather than exclusively by warehouse staff

- Password protection of accounting systems with individual user credentials (not shared logins)

- Regular backup verification through test restoration procedures

Technology enables control effectiveness despite lean staffing. Accounting software with multi-level approval workflows prevents unauthorized payments. Bank account alerts for transactions exceeding specified amounts provide real-time monitoring. Video surveillance in warehouses and fulfillment centers deters inventory theft while providing investigation tools when discrepancies arise.

Conduct Periodic Internal Financial Reviews

Quarterly internal reviews beyond routine bookkeeping provide management insight and identify emerging issues before they become material. Review procedures should include:

- Variance analysis comparing actual results to budget or prior periods

- Gross margin analysis by product category and sales channel identifying profitability shifts

- Working capital assessment tracking days sales outstanding, inventory turnover, and payables aging

- Tax position review verifying adequate reserve accrual for VAT and corporate tax obligations

- Compliance checklist confirmation covering VAT filing, ESR reporting, and UBO updates

Professional accountants conducting quarterly reviews often identify planning opportunities—such as accelerating deductible expenses or deferring income to optimize tax outcomes within legal boundaries. These tactical decisions deliver direct financial benefits exceeding review costs while positioning businesses favorably for year-end audits and tax filings.

Comparison: Free Zone vs Mainland Accounting Requirements

E-commerce businesses choosing between UAE mainland, designated free zones, and financial free zones operate under different tax, accounting, and compliance regimes. The comparison below outlines key distinctions relevant for structure selection and planning.

| Aspect | Mainland (DED Licensed) | Designated Free Zone (Dubai CommerCity, DMCC, JAFZA) | DIFC / ADGM |

| Corporate Tax Rate | 9% on profits above AED 375,000 | 0% on qualifying income; 9% on non-qualifying UAE income | 0% on qualifying income (subject to substance requirements) |

| VAT Treatment | 5% domestic; 0% exports | 5% UAE mainland; 0% intra-zone and exports | 5% UAE supplies under federal VAT rules |

| Customs Duty | 5% on imports (CIF value) | 0% into free zone; 5% when entering mainland | 0% while goods remain in zone |

| Audit Requirement | Mandatory above AED 50 million turnover | Mandatory annual audit (zone rules) | Mandatory audit by registered firms |

| Accounting Standards | IFRS required | IFRS with additional zone disclosures | IFRS with enhanced governance requirements |

| Economic Substance | Generally not applicable | Required for distribution/service activities | Required with stricter substance criteria |

| Ownership | 100% foreign ownership allowed | 100% foreign ownership | 100% foreign ownership (separate legal framework) |

| Regulatory Oversight | DED + Federal Tax Authority | Free zone authority + FTA | DIFC/ADGM authority + FTA (VAT) |

| Banking | UAE mainland accounts required | Free zone or mainland accounts allowed | DIFC/ADGM or mainland accounts |

| License Cost (Annual) | AED 15,000–30,000 | AED 15,000–50,000 | AED 20,000–75,000 |