Key Takeaways

- IFRS Compliance: All UAE import and export companies must prepare financial statements following International Financial Reporting Standards, particularly IFRS 15 for revenue recognition based on Incoterms

- Corporate Tax Registration: Businesses must register for UAE Corporate Tax when taxable profits exceed AED 375,000, with a 9% rate applicable above this threshold

- VAT Registration Mandatory: Import-export operations typically exceed the AED 375,000 annual supply threshold, requiring businesses registered for VAT to file returns and account for import VAT

- Customs Documentation: Proper accounting requires maintaining customs declaration records, certificates of origin, import permits, and freight documentation for a minimum of five years

- Duty Rate Calculation: The standard duty rate of 5% applies to CIF (Cost, Insurance, Freight) values, with an additional 5% VAT on imported goods

- Free Zone Benefits: UAE free zone entities may qualify for 0% corporate tax on qualifying income when meeting substance requirements

- Record Retention: Businesses operating in the UAE must maintain comprehensive documentation, including invoices, contracts, shipment records, and customs clearance papers

Overview of Accounting Requirements in the UAE For Import-Export Companies

The UAE Commercial Companies Law establishes mandatory bookkeeping obligations for import–export entities, requiring accurate records that reflect financial position and trading activities. The Federal Tax Authority mandates retention of all accounting and transactional documentation for at least five years.

Import–export companies must maintain comprehensive records, including ledgers, invoices, banking data, and customs documentation. Accounting systems must support international trade complexity, including multi-currency transactions, duties, freight, and insurance costs.

Mainland entities follow UAE-aligned IFRS standards, while free zone companies apply IFRS directly, including DIFC and ADGM frameworks. Systems must ensure accurate tracking of cross-border transactions and compliance with both tax and reporting requirements.

Customs regulations require full documentation for each shipment, including declarations, invoices, bills of lading, and certificates of origin. Additional regulatory approvals apply to controlled goods, requiring companies to maintain compliance records with relevant UAE authorities.

IFRS Application for Import-Export Companies

International Financial Reporting Standards provide the accounting framework for UAE import-export businesses preparing financial statements. The UAE Ministry of Finance mandates IFRS compliance for all commercial entities, ensuring consistent financial reporting across domestic and international operations. Trading companies must apply specific IFRS standards addressing revenue recognition, inventory valuation, financial instruments, and foreign currency transactions.

IFRS 15 Revenue from Contracts with Customers establishes when import-export companies recognize sales revenue. Revenue recognition timing depends critically on Incoterms specified in sales contracts, which determine when control of goods transfers from exporter to importer. Under FOB (Free on Board) terms, the exporter recognizes revenue when goods pass the ship’s rail at the port of shipment. CIF (Cost, Insurance, Freight) terms similarly recognize revenue at shipment, though the seller includes insurance and freight in the transaction price. DDP (Delivered Duty Paid) terms defer revenue recognition until goods arrive at the buyer’s premises, as the seller retains responsibility for delivery, customs duties, and import clearance.

IAS 2 Inventories governs how trading companies value imported goods. Inventory must be measured at the lower of cost or net realizable value. For imported goods, cost includes purchase price, import customs duties, non-refundable taxes, freight charges, insurance, and handling costs necessary to bring the inventory to its present location and condition. Businesses must consistently apply either FIFO (First-In, First-Out) or weighted average cost formulas. The duty rate of 5% on CIF value forms part of inventory cost, as does import VAT when not immediately recoverable.

IFRS 9 Financial Instruments requires import-export companies to measure trade receivables at amortized cost and apply an expected credit loss model. Businesses must provision for doubtful debts based on customer credit risk, considering factors such as payment history, country risk, and economic conditions in export markets. Letters of credit reduce credit risk, but the accounting system must track exposure by customer and geographic region.

IFRS 16 Leases affects trading companies leasing warehouse facilities, vehicles, or containers for international trade. Long-term leases create right-of-use assets and lease liabilities on the balance sheet, with depreciation and interest expense recognized over the lease term. Short-term leases (12 months or less) and low-value asset leases may be expensed as incurred, simplifying accounting for temporary storage or transportation arrangements.

IAS 21 The Effects of Changes in Foreign Exchange Rates addresses how businesses account for transactions in foreign currencies common in import and export operations. Monetary items such as trade receivables and payables denominated in foreign currencies must be retranslated at each reporting date, with exchange gains or losses recognized in profit or loss. Non-monetary items like inventory remain at historical exchange rates unless carried at fair value.

Bookkeeping Framework and Financial Records Structure

Import-export businesses must establish robust bookkeeping systems capturing the full cycle of international trade transactions. The accounting framework must accommodate customs procedures, multi-currency transactions, complex cost allocations, and regulatory reporting to customs authorities and the Federal Tax Authority.

General Ledger Structure

The chart of accounts should include specialized accounts for import and export activities. Asset accounts must separately track inventory by product category, location (warehouse, in-transit, bonded storage), and status (cleared, pending customs clearance). Liability accounts should include import duties payable, customs clearance fees payable, and advance payments from customers. Revenue accounts distinguish between local sales, GCC exports, and exports outside the Gulf Cooperation Council, as VAT treatment differs. Expense accounts must separately capture customs duties, freight inward, freight outward, insurance, customs brokers’ fees, and penalties for non-compliance.

Multi-Dimensional Accounting

Trading companies benefit from adding dimensions to account codes, allowing analysis by product line, customer segment, or geographic market. A typical account structure might use formats like Account-Location-Product, enabling management to track profitability by UAE mainland versus free zone operations, or by import source country.

Source Documents

Every accounting entry requires supporting documentation. Import transactions demand purchase orders, proforma invoices, commercial invoices from suppliers, packing lists, bills of lading or airway bills, customs declaration forms, customs duty payment receipts, and customs clearance certificates. Export transactions require sales contracts, export invoices, packing lists, shipping documents, certificates of origin, export permits when applicable, and proof of delivery to customers.

Invoice Management

Businesses registered for VAT must issue tax invoices meeting FTA requirements. Each invoice must display the company’s Tax Registration Number (TRN), customer TRN (for B2B transactions), invoice date, and unique sequential number, description of goods, quantity, and unit price, subtotal before VAT, applicable VAT amount, and total amount due. Import-export companies often convert commercial invoices from suppliers (which may lack VAT details) into proper tax invoices when recording purchases.

Bank Reconciliation

Trading companies typically maintain multiple bank accounts for different currencies. The bookkeeping system must reconcile each account monthly, identifying foreign exchange differences between bank statements and ledger balances. Payments for import customs duties through customs authorities’ payment systems must be matched with bank statements and customs clearance records.

Purchase and Sales Ledgers

Subsidiary ledgers track individual supplier and customer accounts. For import operations, the purchases ledger records payables to foreign suppliers, customs brokers, freight forwarders, and other service providers. The sales ledger tracks receivables from customers, including export customers in GCC countries and other international markets. Aging reports help monitor credit risk and ensure timely collection, particularly important for export sales where enforcement may be challenging.

Financial Statements Preparation Requirements

Import-export companies must prepare annual financial statements complying with IFRS and the UAE Commercial Companies Law. These statements provide stakeholders—including customs authorities, banks, investors, and regulatory bodies—with reliable information about financial position and performance.

Balance Sheet (Statement of Financial Position): This statement presents assets, liabilities, and equity at the reporting date. For trading companies, key assets include inventory (raw materials, finished goods, goods in transit), trade receivables from export customers, cash and bank balances in multiple currencies, and right-of-use assets for leased warehouses. Liabilities typically include trade payables to import suppliers, customs duties payable, VAT payable to the Federal Tax Authority, corporate tax provisions, and lease liabilities. The balance sheet must separately disclose current and non-current items.

Profit and Loss Statement (Statement of Comprehensive Income): This statement shows revenue, cost of sales, operating expenses, and profit for the period. Import-export revenue appears net of VAT and sales returns. Cost of goods sold includes purchase cost, customs duties, freight inward, insurance, and landing charges. Operating expenses encompass freight outward, customs brokers’ fees, warehousing costs, salaries, and administrative expenses. The statement must clearly show gross profit margin, which varies significantly depending on the type of goods traded and supply chain efficiency.

Cash Flow Statement: This statement reconciles profit with cash movements, critical for businesses involved in international trade, where working capital fluctuations can be substantial. Operating activities include cash received from customers (including export proceeds), payments to suppliers for imported goods, customs duty payments, VAT payments to FTA, and corporate tax payments. Investing activities capture purchases of equipment or vehicles. Financing activities include loan proceeds, repayments, and dividend distributions.

Notes to Financial Statements: Comprehensive notes explain accounting policies and provide detailed breakdowns. Import-export companies must disclose:

- Revenue recognition policy, including how different Incoterms affect timing

- Inventory valuation method (FIFO or weighted average) and any write-downs

- Trade receivables aging and expected credit loss provisions

- Customs duties, accounting and any disputes with customs authorities

- Foreign currency translation policies and exchange gains/losses

- Commitments such as outstanding letters of credit or forward purchase contracts

- Related party transactions, including import or export dealings with group entities

- Contingent liabilities from customs penalties or regulatory disputes

Financial statements enable external auditors to verify compliance with IFRS and UAE regulations. Banks require audited statements when extending trade finance facilities. Free zone authorities use them to assess economic substance compliance. The Federal Tax Authority relies on them to verify corporate tax calculations.

VAT Compliance for Import-Export Companies in the UAE

Value Added Tax fundamentally shapes how trading companies account for import and export transactions. Federal Decree-Law No. 8 of 2017 establishes VAT obligations, with detailed guidance from the Federal Tax Authority on compliance requirements for businesses engaged in international trade.

VAT Registration

Businesses must register when annual taxable supplies exceed AED 375,000, which most import-export operations quickly surpass. The standard VAT rate is 5%, applied to local sales of goods within the UAE. Companies register through the FTA’s EmaraTax portal, receiving a Tax Registration Number required on all tax invoices. Voluntary registration is possible for businesses with taxable supplies between AED 187,500 and AED 375,000.

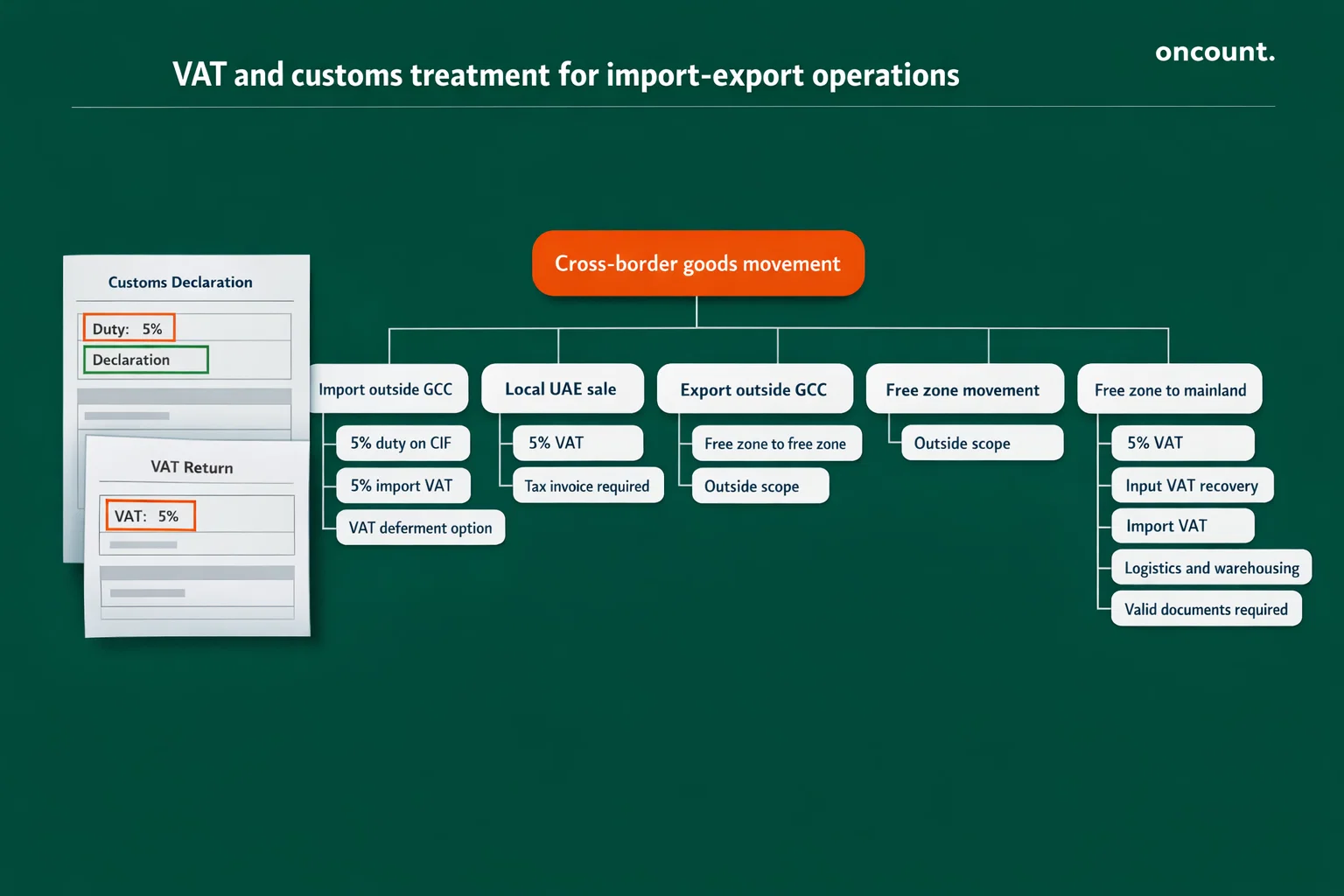

Import VAT Treatment

When importing goods into the UAE from outside the GCC countries, businesses must account for import VAT equal to 5% of the customs value (typically CIF value plus customs duties). The Federal Customs Authority collects VAT at the point of customs clearance. However, businesses registered for VAT can use a VAT deferment scheme, allowing them to self-account for import VAT on their VAT return rather than paying cash upfront. This significantly improves cash flow for trading companies with high import volumes.

Export VAT Treatment

Exports outside the UAE and GCC territories qualify as zero-rated supplies, meaning a 0% rate applies rather than the standard rate of 5%. Zero-rating allows businesses to recover input VAT on costs while charging no VAT to international customers, making UAE exports competitive globally. To support zero-rating, companies must retain export documentation, including:

- Export customs declaration stamped by customs authorities

- Commercial invoice to the foreign customer

- Bill of lading or airway bill showing goods left the UAE

- Proof of payment from the customer

Sales to GCC countries receive special treatment under the GCC VAT framework. The World Trade Organization principles apply, but specific rules depend on whether goods cross GCC internal borders or remain in customs-bonded facilities.

Input VAT Recovery

Import-export companies can reclaim input VAT on business expenses, including import VAT (via deferment or refund), freight and logistics costs, warehousing, customs brokers’ fees, equipment purchases, and utilities. However, input VAT must relate to taxable activities. Businesses making some exempt supplies must apportion input VAT, though this rarely affects pure trading operations.

VAT Returns and Filing

Businesses operating in the UAE must file VAT returns quarterly or monthly, depending on expected annual turnover. Returns are due within 28 days of the period end through the EmaraTax portal. Each return requires businesses to report:

- Total output VAT on local sales (Box 1)

- Import VAT under reverse charge or deferment (Box 3)

- Total input VAT recoverable (Box 7)

- Net VAT payable or refundable

Late filing attracts penalties: AED 1,000 for up to 14 days late, AED 2,000 for 15-30 days, escalating to AED 10,000 beyond 30 days. Repeat violations can result in higher penalties and FTA investigations.

Free Zone VAT Considerations

UAE free zone businesses enjoy special VAT treatment. Supplies of goods between designated free zones are outside the scope of UAE VAT, provided goods remain within free zone areas. However, when a free zone entity sells goods entering the UAE mainland, the transaction becomes a standard taxable supply subject to the 5% rate. Businesses must carefully track whether goods physically enter the UAE customs territory to determine the correct VAT treatment.

| Transaction Type | VAT Treatment | Documentation Required |

| Local UAE Sales | 5% Standard Rate | Tax invoice with TRN |

| Exports outside GCC | 0% Zero-Rated | Export customs declaration, shipping docs |

| Imports from outside the GCC | 5% Reverse Charge/Deferment | Customs declaration, payment receipts |

| GCC Imports | 5% (treated as domestic purchase) | Commercial invoice, transport docs |

| Free Zone to Free Zone | Outside Scope (0%) | Movement certificates, free zone docs |

| Free Zone to Mainland | 5% Standard Rate | Customs entry, tax invoice |

Corporate Tax Framework in the UAE

Federal Decree-Law No. 47 of 2022 introduced corporate tax to the UAE from fiscal years beginning on or after June 1, 2023. This legislation fundamentally changed tax compliance obligations for import-export companies previously operating in a zero-tax environment.

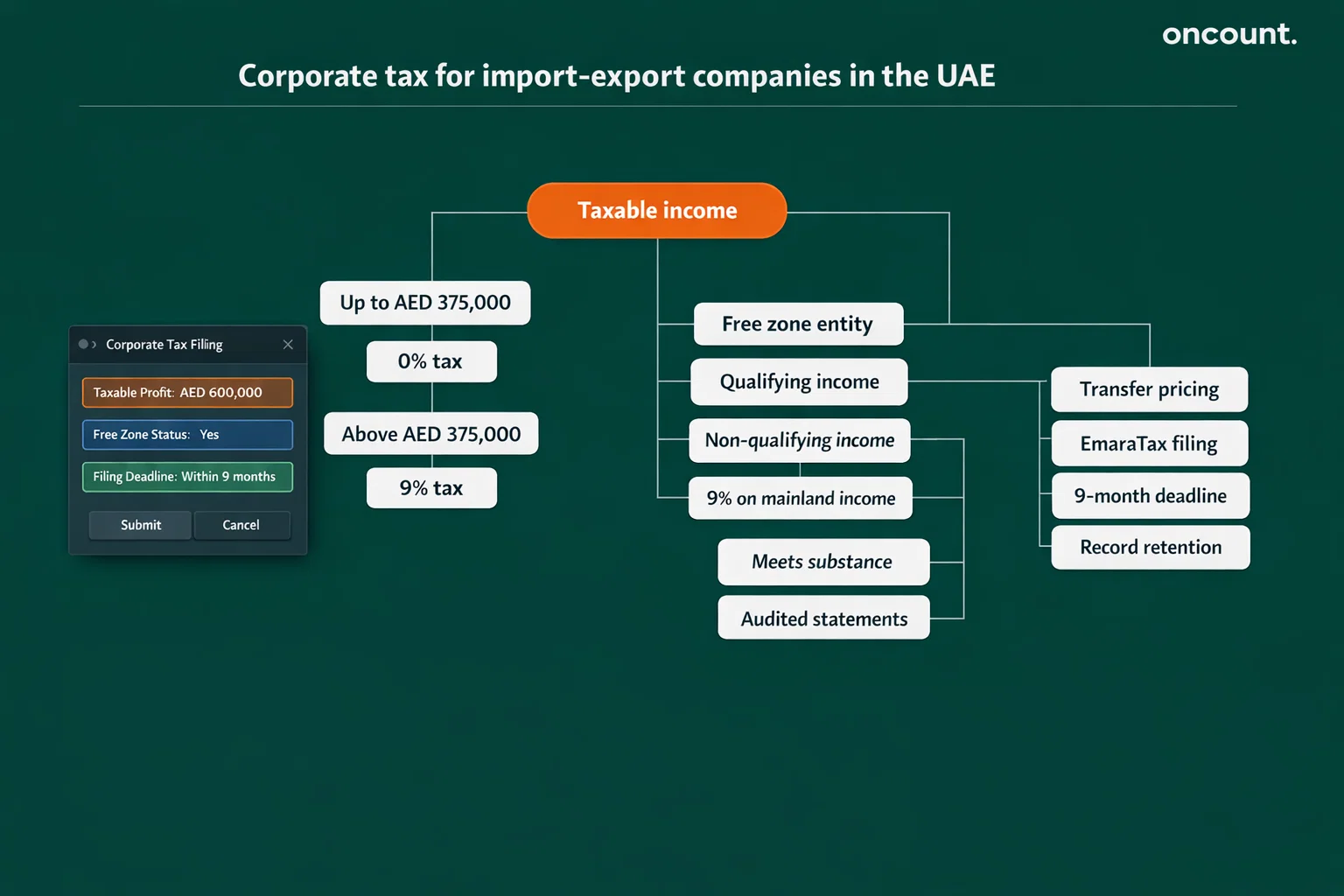

Tax Rates and Thresholds

UAE Corporate Tax applies a two-tier structure. Taxable income up to AED 375,000 faces a 0% rate, while profits exceeding this threshold incur a 9% rate on the excess. This structure benefits smaller trading companies while ensuring larger operations contribute. For example, a company with AED 1,000,000 taxable profit pays zero on the first AED 375,000 and AED 56,250 (9% of AED 625,000) on the remainder.

Taxable Income Calculation

Corporate tax liability begins with accounting profit per IFRS financial statements, then applies adjustments specified in the Corporate Tax Law. Common adjustments for import-export businesses include:

Additions to taxable income:

- Fines and penalties paid to customs authorities or FTA

- Entertainment expenses exceeding reasonable limits

- Related-party expenses without proper documentation

- Provisions not meeting tax deductibility criteria

Deductions from taxable income:

- Capital allowances on depreciable assets

- Actual bad debt write-offs (replacing accounting provisions)

- Qualifying research and development expenses

- Donations to approved charitable organizations

Import-export businesses must distinguish between accounting treatment per IFRS and tax treatment per the Corporate Tax Law. For instance, inventory write-downs under IAS 2 are added back until inventory is actually disposed of at a loss, at which point the tax loss becomes deductible.

Free Zone Qualifying Income

Qualifying free zone entities can maintain a 0% corporate tax rate on qualifying income when meeting substance requirements. The UAE offers this benefit to encourage free zone businesses and maintain competitiveness as a global trade hub. Qualifying income includes revenue from transactions with non-UAE persons or other qualifying free zone entities. To qualify, businesses must:

- Hold valid free zone licenses

- Derive adequate income (de minimis rule allows up to 5% non-qualifying revenue)

- Maintain substance in the UAE (adequate employees, assets, and operating expenditure)

- Prepare audited financial statements

- Not elect mainland tax treatment

Non-qualifying income from free zone entities (such as sales into the UAE mainland) faces the standard 9% rate above the AED 375,000 threshold. Trading companies in free zones must segregate income streams and allocate costs appropriately between qualifying and non-qualifying activities.

Transfer Pricing Requirements

Import-export companies frequently transact with related parties across borders—importing from group suppliers or exporting to group distributors. The Corporate Tax Law mandates arm’s length pricing for related-party transactions. Prices charged must reflect what independent parties would agree in comparable circumstances. Businesses must prepare transfer pricing documentation, including:

- Master file describing the group structure and business activities

- Local file analyzing specific UAE entity transactions

- Justification for pricing methods (comparable uncontrolled price, cost plus, resale price method)

Improper transfer pricing can result in tax adjustments, penalties of up to 50% of additional tax due, and reputational damage. Import-export businesses should benchmark their import purchase prices and export selling prices against market comparables, maintaining evidence to satisfy FTA inquiries.

Registration and Filing

Businesses must register for corporate tax on the FTA’s EmaraTax portal within specified deadlines. Tax returns are due within nine months of the financial year end. For example, a company with a December 31 year-end must file by September 30 the following year. Late filing attracts penalties starting at AED 500, escalating based on delay duration.

Accounting for Revenue and Expenses in Import-Export Operations

Trading companies face unique challenges in recognizing revenue and expenses due to the complexity of international trade transactions, diverse Incoterms, and multi-stage supply chains.

Revenue Recognition Under IFRS 15: Import-export businesses must identify performance obligations in customer contracts and recognize revenue when control transfers. The delivery terms specified in sales contracts directly determine revenue timing:

- FOB (Free on Board): Revenue recognized when goods pass the ship’s rail at the origin port. Seller’s responsibility ends at loading; buyer arranges and pays for ocean freight and insurance. The importer records freight-in as part of the inventory cost.

- CIF (Cost, Insurance, Freight): Revenue recognized at the shipment point, but the exporter includes insurance and freight costs in the selling price. These costs flow through the exporter’s profit and loss as operating expenses, offsetting revenue.

- CFR (Cost and Freight): Similar to CIF but excludes insurance. The exporter pays freight to the destination port; the buyer arranges insurance separately.

- DDP (Delivered Duty Paid): Revenue deferred until goods reach the buyer’s premises. The exporter remains responsible for import customs duties, taxes, and delivery costs, which reduce gross profit margin.

Trading companies must consistently apply revenue recognition based on contract terms. For instance, if a Dubai trading company sells to a European customer under DDP terms, it cannot recognize revenue when goods leave Dubai. Revenue recognition waits until customs clearance in Europe is complete and goods are delivered, even though the shipment departed weeks earlier.

Cost of Goods Sold: For import-export operations, COGS includes all costs to bring goods to saleable condition: purchase price from supplier, customs duties (5% standard rate), import VAT (recovered separately), international freight, marine insurance, local transportation from port to warehouse, customs brokers fees, port charges and storage, and inspection or fumigation costs when required by the Ministry of Climate Change and Environment.

Consider a container of textiles imported into Dubai. The FOB purchase price is USD 100,000 (AED 367,000 at the exchange rate). Ocean freight adds AED 18,000, insurance AED 3,500. At Dubai Customs, the CIF value for customs purposes becomes AED 388,500. Customs duties at 5% equal AED 19,425. Import VAT at 5% totals AED 20,396 (on AED 407,925), which is recoverable through VAT returns. The landed cost for inventory valuation: AED 388,500 + AED 19,425 = AED 407,925. When sold, this becomes COGS.

Operating Expenses: Trading companies incur substantial operating costs beyond COGS. Freight outward on export sales (unless built into selling price under Incoterms), warehousing and storage fees, customs brokers and agents, salaries for procurement and logistics staff, rent for offices and warehouse space, marketing and customer acquisition costs, bad debt expenses from uncollectible export receivables, bank charges for letters of credit, and penalties for late customs declarations all flow through the profit and loss statement.

Foreign Exchange Impact: International trade transactions create constant foreign exchange exposure. When an import-export company invoices customers in USD, EUR, or other currencies, it must retranslate receivables at each reporting date per IAS 21. Exchange gains or losses appear in profit or loss. Similarly, payables to foreign suppliers require retranslation. Many trading companies use forward contracts to hedge exchange risk; such derivatives require fair value accounting under IFRS 9, adding complexity.

Treatment of Advances and Deposits: Import operations often require advance payments to suppliers. When a Dubai trading company pays a 30% deposit on a container order, it records a prepayment asset (DR Prepayments, CR Bank). On receiving goods and customs clearance, the prepayment transfers to inventory. Export operations may receive customer advances, recorded as a contract liability until goods ship and revenue recognition criteria are met.

Regulatory Compliance and Reporting Obligations

Beyond financial reporting and taxation, UAE import-export businesses face multiple regulatory frameworks requiring specific compliance measures and documentation.

Economic Substance Regulations (ESR)

Cabinet Resolution No. 57 of 2020 implements Economic Substance Regulations affecting relevant activities, including distribution and service center business. Trading companies conducting import-export operations through UAE free zones or other jurisdictions must assess whether they conduct relevant activities. If so, they must demonstrate adequate substance: core income-generating activities performed in the UAE, adequate qualified employees, adequate operating expenditure in the UAE, and adequate physical assets in the UAE.

Entities conducting relevant activities must file an Economic Substance Notification and, if required, an Economic Substance Report annually. The Ministry of Finance reviews submissions and can impose penalties from AED 10,000 to AED 300,000 for non-compliance. Trading companies should maintain records proving substance, including employee contracts, office lease agreements, and operational expense invoices.

Ultimate Beneficial Owner (UBO) Reporting

Federal Decree-Law No. 20 of 2018 requires all UAE mainland and free zone companies to maintain a register of ultimate beneficial owners—individuals owning 25% or more, or exercising control through other means. Import-export businesses must submit UBO information to licensing authorities and update it within 15 days of changes. Penalties for non-compliance reach AED 100,000. This transparency measure aligns UAE practices with global anti-money laundering standards.

Anti-Money Laundering (AML) Compliance

Federal Decree-Law No. 20 of 2018 on Anti-Money Laundering and Combating the Financing of Terrorism establishes obligations for businesses in the UAE. Trading companies must implement AML procedures, including customer due diligence (know your customer), identifying beneficial owners of corporate customers, monitoring transactions for suspicious patterns, reporting suspicious activities to the Financial Intelligence Unit, and maintaining records of customers and transactions for five years.

Import-export operations face heightened AML risk due to cross-border fund flows, dealings with entities in multiple jurisdictions, and potential for trade-based money laundering. Customs authorities and FTA may investigate unusual trading patterns, such as goods repeatedly imported and re-exported without a clear commercial rationale, or pricing significantly diverging from market norms.

Customs Compliance: Businesses importing or exporting goods must comply with Federal Law No. 7 of 2017 on Customs Procedures. Key obligations include:

- Appointing customs brokers or obtaining direct clearance authorization

- Submitting accurate customs declarations with correct HS codes and valuations

- Maintaining supporting documents (commercial invoices, packing lists, certificates of origin)

- Paying customs duties and fees before releasing goods

- Complying with import permits and regulations for restricted goods

- Following procedures for bonded storage, transit, and temporary admission

Non-compliance attracts penalties varying by violation severity. Incorrect declarations may incur fines from AED 1,000 to AED 100,000. Smuggling or evading duties risks criminal prosecution. Dubai Customs and other customs authorities conduct post-clearance audits, reviewing importers’ records to verify proper duty payment and classification accuracy.

Product-Specific Regulations: Certain goods require additional compliance. The Ministry of Climate Change and Environment regulates food products, plants, animals, and pesticides, requiring import permits and certificates demonstrating safety and compliance. Pharmaceuticals and medical devices require Ministry of Health and Prevention approval. Telecommunications equipment needs Telecommunications and Digital Government Regulatory Authority certification. Trading companies handling such goods must factor permit costs and processing time into their operations.

| Compliance Area | Regulatory Body | Key Requirement | Penalty Range |

| Corporate Tax | Federal Tax Authority | Registration, filing returns, paying tax due | AED 500 – 50% of tax due |

| VAT | Federal Tax Authority | Registration, monthly/quarterly returns, and maintaining records | AED 1,000 – AED 10,000+ |

| Customs | Federal Customs Authority | Accurate declarations, duty payment, and document retention | AED 1,000 – AED 100,000 |

| ESR | Ministry of Finance | Substance demonstration, annual reporting | AED 10,000 – AED 300,000 |

| AML | Central Bank / FIU | Customer due diligence, suspicious transaction reporting | Varies by violation |

| UBO | DED / Free Zone Authority | Register maintenance, timely updates | Up to AED 100,000 |

Audit Requirements for Import-Export Companies in the UAE

Statutory audits provide independent verification of financial statements, offering assurance to stakeholders, including customs authorities, banks, investors, and regulatory bodies.

Mainland Audit Requirements

UAE Commercial Companies Law requires all mainland limited liability companies (LLCs) and public/private joint stock companies to appoint external auditors and prepare audited financial statements annually. Import-export businesses structured as mainland companies must engage auditors licensed by the UAE Ministry of Economy. Auditors examine financial records, test internal controls, verify inventory counts, confirm receivables and payables, and review compliance with IFRS and UAE regulations.

Audited financial statements must be filed with the Department of Economic Development or the relevant mainland authority. The annual audit provides a clean opinion when financial statements present fairly in accordance with IFRS, or qualified, adverse, or disclaimer opinions when issues arise. Banks extending trade finance facilities to import-export companies require audited statements before approving letters of credit or working capital loans.

Free Zone Audit Requirements

Most UAE free zones mandate annual audits. Requirements vary by free zone but generally include preparing IFRS-compliant financial statements and engaging auditors from the free zone’s approved list. Dubai Multi Commodities Centre (DMCC), Jebel Ali Free Zone (JAFZA), and others maintain registers of approved audit firms. Free zone businesses must submit audited statements to the free zone authority within specified deadlines, typically 6-9 months after year-end.

Free zone audits support Economic Substance Regulations compliance, as auditors verify operating expenditure, asset ownership, and other substance indicators. Qualifying free zone entities seeking 0% corporate tax must provide audited statements demonstrating they meet qualifying income requirements.

DIFC and ADGM Requirements

Companies operating in Dubai International Financial Centre or Abu Dhabi Global Market face enhanced audit standards. These financial free zones apply IFRS as issued by the IFRS Foundation and require audits meeting International Standards on Auditing (ISA). DIFC and ADGM maintain their own auditor registration systems. Trading companies in these zones benefit from sophisticated financial infrastructure but face stricter compliance expectations.

Audit Focus Areas for Import-Export: External auditors examining trading companies concentrate on specific risk areas:

- Inventory Valuation: Auditors attend physical counts, test pricing methodologies, and assess net realizable value write-downs. Import-export businesses with diverse product ranges face complexity in ensuring accurate cost allocation, including customs duties and freight.

- Revenue Recognition: Auditors review sales contracts, verify Incoterms, test cut-off procedures ensuring revenue recognition in the correct periods, and assess whether variable consideration (discounts, returns) is appropriately estimated.

- Trade Receivables: Auditors confirm balances with export customers, evaluate expected credit loss provisions under IFRS 9, and assess foreign exchange risk on foreign currency receivables.

- Customs and VAT Compliance: Auditors review customs declaration records, verify duty calculations, test VAT deferment accounting, and ensure proper documentation supports zero-rated export claims.

- Related Party Transactions: Auditors identify transactions with group entities, assess transfer pricing documentation, and verify arm’s length pricing for import or export dealings with affiliates.

Industry-Specific Accounting Considerations for Import-Export Operations

Landed Cost Calculation and Customs Valuation

Import-export businesses must accurately calculate landed costs to determine true product profitability. Customs valuation determines the base for calculating customs duties and import VAT, following World Trade Organization valuation principles. The transaction value method (actual price paid or payable) applies in most cases, adjusted for items not included in the invoice price but required to be added per customs regulations.

Components of landed cost include FOB purchase price from supplier, international freight charges (ocean, air, or land transport), marine or air cargo insurance, port handling and storage charges at origin and destination, customs duties at the standard duty rate of 5%, customs clearance fees and customs brokers charges, inspection or fumigation when required by Ministry of Climate Change and Environment, and inland transportation from port to warehouse. Import VAT at 5% is calculated on the sum of CIF value plus customs duties but is typically recoverable through VAT returns and thus excluded from inventory cost.

Incoterms Impact on Financial Reporting

International Commercial Terms (Incoterms) published by the International Chamber of Commerce define seller and buyer responsibilities in international transactions. The chosen Incoterm affects when import-export companies recognize revenue, how costs are allocated, and which party handles customs clearance. Common Incoterms for UAE trading companies include:

EXW (Ex Works): Seller makes goods available at their premises. Buyer handles all transportation, insurance, and customs procedures. The exporter recognizes revenue at collection point.

FOB (Free on Board): Seller delivers goods on board the vessel at the port of origin. Risk transfers when goods pass the ship’s rail. Buyers arrange ocean freight and insurance. Exporters recognize revenue at shipment.

CIF (Cost, Insurance, Freight): Seller pays transportation and insurance to the destination port. Risk transfers at the origin port, but the seller bears the freight cost. Exporters recognize revenue at shipment and record freight/insurance as expenses.

DDP (Delivered Duty Paid): Seller delivers goods to the buyer’s premises, paying all costs, including import customs duties and taxes. Risk and cost transfer at final delivery. Exporters defer revenue recognition until delivery and include all delivery costs in COGS.

UAE import-export companies must ensure sales contracts specify Incoterms clearly and accounting policies reflect the chosen terms. Incorrect revenue timing creates IFRS violations and potential corporate tax miscalculations.

Consignment and Drop-Shipping Models

Some trading companies operate consignment arrangements where goods are shipped to an agent or distributor but title remains with the consignor until goods are sold to end customers. Under consignment, the consignor retains inventory on their balance sheet until the agent reports sales. Revenue recognition occurs when the agent sells goods to third parties, not when goods ship to the agent. This defers revenue and complicates inventory tracking, as goods are physically distant but legally owned.

Drop-shipping eliminates the need for traders to hold inventory. A Dubai trading company receives customer orders, places orders with suppliers, and arranges direct shipment from the supplier to the customer. The trading company never physically handles goods. Accounting treatment depends on whether the trader acts as principal or agent. As principal (taking inventory risk, setting prices), the trader records gross revenue and COGS. As agent (arranging transactions for commission), only commission revenue is recognized. IFRS 15 provides indicators: inventory risk, pricing discretion, and credit risk suggest principal status.

Free Zone and Customs Bonded Warehouse Operations

UAE free zones offer special customs and tax treatment beneficial for trading companies. Goods stored in designated free zone areas remain outside UAE customs territory, deferring customs duties and VAT until goods enter mainland UAE. This allows businesses to store inventory, perform light manufacturing, and re-export without paying duties or VAT.

Re-exports from free zones face no UAE customs duties or VAT, supporting the UAE’s role as a global trade hub connecting Asian suppliers with Middle Eastern, African, and European markets. Trading companies leveraging free zone benefits must maintain detailed records proving goods’ movements and locations to satisfy customs authorities and support VAT zero-rating claims.

Common Accounting Challenges for Import-Export Companies

Improper Revenue Recognition and Incoterms Misapplication

Many import-export businesses struggle with IFRS 15 revenue recognition, particularly determining when control transfers under different Incoterms. Recording sales when goods ship under DDP terms (where delivery to the customer’s premises is required) overstates revenue and violates IFRS. Similarly, recognizing revenue before goods clear customs under terms where the seller remains responsible creates compliance risks.

Consequences include IFRS-noncompliant financial statements, corporate tax miscalculations (taxable income overstated in early periods, understated later), VAT timing errors affecting cash flow, and audit qualifications from external auditors. Solutions involve training finance teams on Incoterms implications, implementing system controls triggering revenue recognition based on delivery terms, and documenting contracts clearly specifying when title and risk transfer.

Inadequate Customs Valuation and Duty Allocation

Incorrectly valuing imported goods for customs purposes creates multiple problems. Undervaluing imports to reduce customs duties (a duty rate of 5% creates an incentive to minimize declared value) risks penalties from customs authorities ranging from fines to criminal charges for smuggling. Overvaluing distorts inventory costs and reduces profitability. Common errors include excluding freight and insurance from CIF calculations, failing to add royalties or license fees required under customs valuation rules, omitting assists (materials provided to the supplier), and applying incorrect exchange rates for foreign currency invoices.

The Federal Customs Authority can conduct post-clearance audits examining importers’ records. Discrepancies between declared values and accounting records raise red flags. Businesses should maintain documentation supporting valuations: supplier invoices, freight bills, insurance certificates, and currency conversion calculations. Transfer pricing documentation becomes crucial for imports from related parties, as customs authorities may challenge valuations appearing below market rates.

VAT Deferment Accounting Errors

While VAT deferment improves cash flow, businesses must correctly account for deferred import VAT on returns. Common mistakes include failing to report import VAT in both output tax and input tax boxes (Box 3 and Box 7), resulting in net VAT payable when none should be due for fully recoverable imports, recording import VAT as expense rather than recoverable VAT, missing imports from customs statements leading to understated VAT positions, and mismatching customs declaration dates with accounting periods.

These errors cause VAT returns to be incorrect, potentially triggering FTA audits and penalties. Solutions include reconciling customs declarations monthly with accounting records, using customs authorities’ electronic systems to download import data, implementing controls ensuring all imports are captured, and seeking advice from bookkeeping outsourcing companies with UAE VAT expertise.

Foreign Exchange Management

Import-export operations involve constant foreign currency exposure. Trading companies purchasing in USD or EUR and selling in AED, or vice versa, face exchange rate volatility affecting profitability. Failing to retranslate foreign currency receivables and payables at reporting dates per IAS 21 creates IFRS violations. Not hedging exchange risk through forward contracts or other instruments exposes businesses to unexpected losses.

Challenges include accounting for forward contracts and other derivatives under IFRS 9 (fair value through profit or loss, or hedge accounting), determining appropriate hedge ratios, and managing working capital impacts when exchange rates move unfavorably. Trading companies should establish treasury policies defining acceptable exposure levels and hedging strategies, documenting hedge relationships if applying hedge accounting, and regularly monitoring currency positions.

Best Practices for Accounting and Financial Management

Import–export companies in the UAE should implement structured financial management practices to ensure compliance and operational efficiency. A disciplined approach strengthens financial control, supports accurate reporting, and reduces regulatory risks.

- Cloud-based accounting systems support multi-currency transactions, VAT accounting, customs duty calculations, and integration with Dubai Customs and Federal Tax Authority systems. Real-time access improves visibility over inventory, including in-transit, bonded, and cleared goods.

- Professional accounting services ensure compliance with IFRS, VAT, corporate tax, and transfer pricing requirements. Specialized providers help maintain accurate records, meet deadlines, and manage regulatory interactions effectively.

- Robust internal controls require segregation of duties across procurement, invoicing, and payments. Regular reconciliations and periodic inventory counts improve accuracy and reduce the risk of errors or fraud.

- Comprehensive documentation must include invoices, customs declarations, shipping records, and bank statements. Proper recordkeeping ensures compliance with five-year retention requirements and supports audits and tax reviews.

- Performance monitoring should focus on key indicators such as inventory turnover, receivables days, gross profit margins, customs cost ratios, and VAT recovery efficiency.

- Regulatory monitoring requires tracking updates from the Federal Tax Authority and Ministry of Finance, engaging with industry bodies, and consulting advisors to reflect regulatory changes in accounting practices.

- Periodic compliance reviews through internal audits help assess VAT filings, customs documentation, and tax provisions, allowing early correction of issues before regulatory inspections.

Comparison: Free Zone vs Mainland Accounting Requirements

UAE import-export businesses choose between mainland establishment or free zone licenses based on operational needs and compliance preferences. Accounting and regulatory requirements differ significantly.

| Aspect | Mainland | Free Zone |

| Corporate Tax | 0% up to AED 375,000 profit, 9% above | 0% on qualifying income if substance requirements met; 9% on non-qualifying income |

| VAT Registration | Mandatory when annual supplies exceed AED 375,000 | Same threshold; special treatment for free zone to free zone supplies (outside scope) |

| Customs Duties | Payable on all imports entering the UAE market (5% standard) | Deferred while goods remain in the free zone; due when entering the mainland |

| Audit Requirements | Mandatory annual audit for LLCs and corporations | Mandatory in most free zones; must use approved auditors |

| IFRS Compliance | UAE-adapted IFRS standards | IFRS directly (DIFC/ADGM applies IFRS as issued) |

| Record Retention | Minimum 5 years | 5 years for tax; varies by free zone for other records |

| ESR Reporting | Required if conducting relevant activities | Required; critical for maintaining 0% tax eligibility |

| Operating Flexibility | Can trade anywhere in the UAE and internationally | May face restrictions on mainland trading; varies by free zone |

| Licensing Costs | Generally, lower initial setup | Higher license fees but potential tax savings |

| Office Requirements | Physical office space required | Flexi-desk options are available in many free zones |

Strategic Considerations: Mainland establishment suits businesses focused on the UAE domestic market or requiring unrestricted mainland access. Free zones benefit companies primarily exporting or re-exporting, seeking 0% corporate tax, and operating in bonded storage models. Some trading companies establish both mainland and free zone entities, using the free zone for import, storage, and export while the mainland entity handles domestic distribution.