Key Takeaways

- Mandatory IFRS Compliance: All UAE companies are required to prepare financial statements following International Financial Reporting Standards, with IFRS 15 governing revenue recognition for trading operations.

- VAT Registration Threshold: Trading companies exceeding AED 375,000 in annual taxable supplies must register for Value Added Tax with the Federal Tax Authority.

- Corporate Tax Rate: UAE Corporate Tax applies a 9% rate to taxable profits above AED 375,000, effective for financial years starting on or after June 1, 2023.

- Record Retention Period: The UAE Commercial Companies Law requires businesses to maintain accounting records for a minimum of five years from the end of the relevant tax period.

- Annual Audit Requirement: Mainland trading companies must conduct annual audits, while companies registered in free zones follow jurisdiction-specific audit requirements.

- Economic Substance Reporting: Trading companies often qualify as relevant activities under Economic Substance Regulations and must file annual ESR notifications with the UAE Ministry of Finance.

Overview of Accounting Requirements in the UAE for General Trading Companies

The UAE Commercial Companies Law (Federal Law No. 2 of 2015 on Commercial Companies) establishes the foundational accounting obligations for all commercial companies operating across the UAE. Every company in the UAE must maintain comprehensive accounting records that accurately reflect financial position, trading operations, and compliance with internationally recognized accounting standards. The Federal Tax Authority mandates that businesses in the UAE preserve complete documentation supporting all financial transactions, including purchase invoices, sales contracts, customs declarations, and bank statements.

Trading companies in the UAE must implement systematic bookkeeping practices capable of tracking inventory movements, supplier payments, customer receipts, and operational expenses. According to FTA guidance stipulated in the Tax Procedures Law (Federal Decree-Law No. 7 of 2017), companies must retain accounting records for five years following the end of the tax period to which they relate. This retention period applies to both electronic and physical documentation, covering general ledgers, subsidiary ledgers, trial balances, and supporting vouchers.

The UAE accounting framework requires trading businesses to prepare financial statements that provide a true and fair view of their financial performance. Companies registered in mainland Dubai must comply with UAE accounting standards aligned with International Financial Reporting Standards, while free zone entities typically follow IFRS standards directly. The accounting system employed must enable accurate tracking of trade receivables, payables, inventory valuation, and cost of goods sold across diverse product categories and trading channels.

| Accounting Obligation | Legal Requirement | Retention Period |

| General ledger and subsidiary records | Federal Law No. 2 of 2015 | 5 years minimum |

| Purchase and sales invoices | Tax Procedures Law | 5 years minimum |

| Customs documentation | Federal Tax Authority regulations | 5 years minimum |

| Bank statements and reconciliations | Commercial Companies Law | 5 years minimum |

| Inventory records and stock counts | IFRS compliance standards | 5 years minimum |

IFRS Application for General Trading Companies

International Financial Reporting Standards provide the accounting framework that UAE companies must follow when preparing financial statements. Trading companies in the UAE must apply IFRS 15 (Revenue from Contracts with Customers) to ensure accurate revenue recognition across sales transactions, distribution agreements, and consignment arrangements. IFRS 15 requires trading businesses to recognize revenue when control of goods transfers to customers, which typically occurs upon delivery or shipment, depending on contractual terms.

IFRS 9 (Financial Instruments) governs the accounting treatment for trade receivables, requiring trading companies to assess expected credit losses and establish provisions for doubtful debts. Trading operations involving foreign currency transactions must comply with IAS 21 (The Effects of Changes in Foreign Exchange Rates), recognizing exchange gains or losses at settlement dates or reporting period ends. Companies holding significant inventory must apply IAS 2 (Inventories), valuing stock at the lower of cost or net realizable value and selecting appropriate cost formulas such as IFRS-compliant weighted average or first-in-first-out methods.

Trading companies operating from leased warehouses or office spaces must implement IFRS 16 (Leases), recognizing right-of-use assets and corresponding lease liabilities on the balance sheet. According to the IFRS Foundation, this standard eliminates the previous distinction between operating and finance leases, requiring trading businesses to capitalize substantially all lease arrangements exceeding 12 months. Companies engaged in providing credit terms to UAE customers must assess whether financing components exist within revenue contracts, potentially requiring the separation of financing elements under IFRS 15 guidance.

Bookkeeping Framework and Financial Records Structure

Trading companies must establish a comprehensive chart of accounts tailored to the trading sector’s operational requirements. The accounting system should include distinct account categories for inventory by product line, trade receivables by customer segment, trade payables by supplier, and operating expenses segregated by functional area. General trading companies in the UAE typically structure their chart of accounts to enable tracking of gross profit margins across different product categories, supporting management decision-making and tax compliance.

The general ledger serves as the central repository for all financial transactions, with subsidiary ledgers providing detailed breakdowns of customer accounts, supplier balances, and inventory movements. Trading businesses must implement controls ensuring every transaction is supported by appropriate documentation, including tax invoices compliant with UAE VAT requirements, purchase orders, goods received notes, and delivery documentation. Best practices for trading companies include daily bank reconciliations, weekly inventory counts for high-value items, and monthly reconciliation of trade receivables and payables.

Accounting software systems employed by trading companies should generate audit trails tracking all journal entries, modifications, and user access. The Federal Tax Authority requires businesses to maintain accounting records in Arabic or English, with electronic accounting systems meeting technical specifications for data extraction during tax audits. Cloud-based accounting platforms have become standard among UAE trading businesses, offering real-time financial visibility, automated VAT calculations, and integration with customs systems for import-export documentation.

Essential Documentation for Trading Company Bookkeeping:

- Sales Documentation: Tax invoices, delivery notes, export declarations, customer contracts

- Purchase Documentation: Supplier invoices, import customs forms, purchase orders, payment vouchers

- Inventory Records: Stock cards, warehouse receipts, goods received notes, stock count sheets

- Banking Records: Bank statements, payment confirmations, foreign exchange contracts, letter of credit documentation

- Operational Records: Employee payroll records, utility bills, rental agreements, insurance policies

Financial Statements Preparation Requirements

Companies in the UAE must prepare a complete set of financial statements annually, comprising a balance sheet (statement of financial position), profit and loss statement (income statement), cash flow statement, statement of changes in equity, and notes to financial statements. The balance sheet must present trading company assets, including inventory, trade receivables, prepayments, and fixed assets, alongside liabilities such as trade payables, accrued expenses, and loan obligations. Equity sections should reflect share capital, statutory reserves, and retained earnings in accordance with the UAE Commercial Companies Law requirements.

The profit and loss statement for trading businesses displays revenue from sales, cost of goods sold (including opening inventory, purchases, and closing inventory), gross profit, operating expenses, and net profit before and after tax. Trading companies often face revenue recognition complexities when dealing with multiple delivery terms (FOB, CIF, DDP), requiring careful application of IFRS 15 to determine the appropriate timing of revenue recognition. Cost of goods sold calculations must account for inventory valuation methods, freight charges, customs duties, and any purchase discounts received from suppliers.

The cash flow statement categorizes cash movements into operating activities (customer collections, supplier payments), investing activities (equipment purchases, disposal proceeds), and financing activities (loan receipts, dividend payments). Trading operations typically generate substantial cash flows from operating activities, with working capital movements significantly impacting cash position due to inventory purchases and trade credit terms. Notes to financial statements must disclose accounting policies, significant estimates and judgments, related party transactions, contingent liabilities, and compliance with specific IFRS standards relevant to trading operations.

| Financial Statement | Primary Purpose | Key Trading Metrics |

| Balance Sheet | Shows financial position at year-end | Inventory turnover, receivables collection period |

| Profit & Loss Statement | Displays annual trading performance | Gross profit margin, operating profit ratio |

| Cash Flow Statement | Tracks cash generation and usage | Operating cash flow, working capital changes |

| Notes to Accounts | Provides disclosure and context | Accounting policies, contingent liabilities |

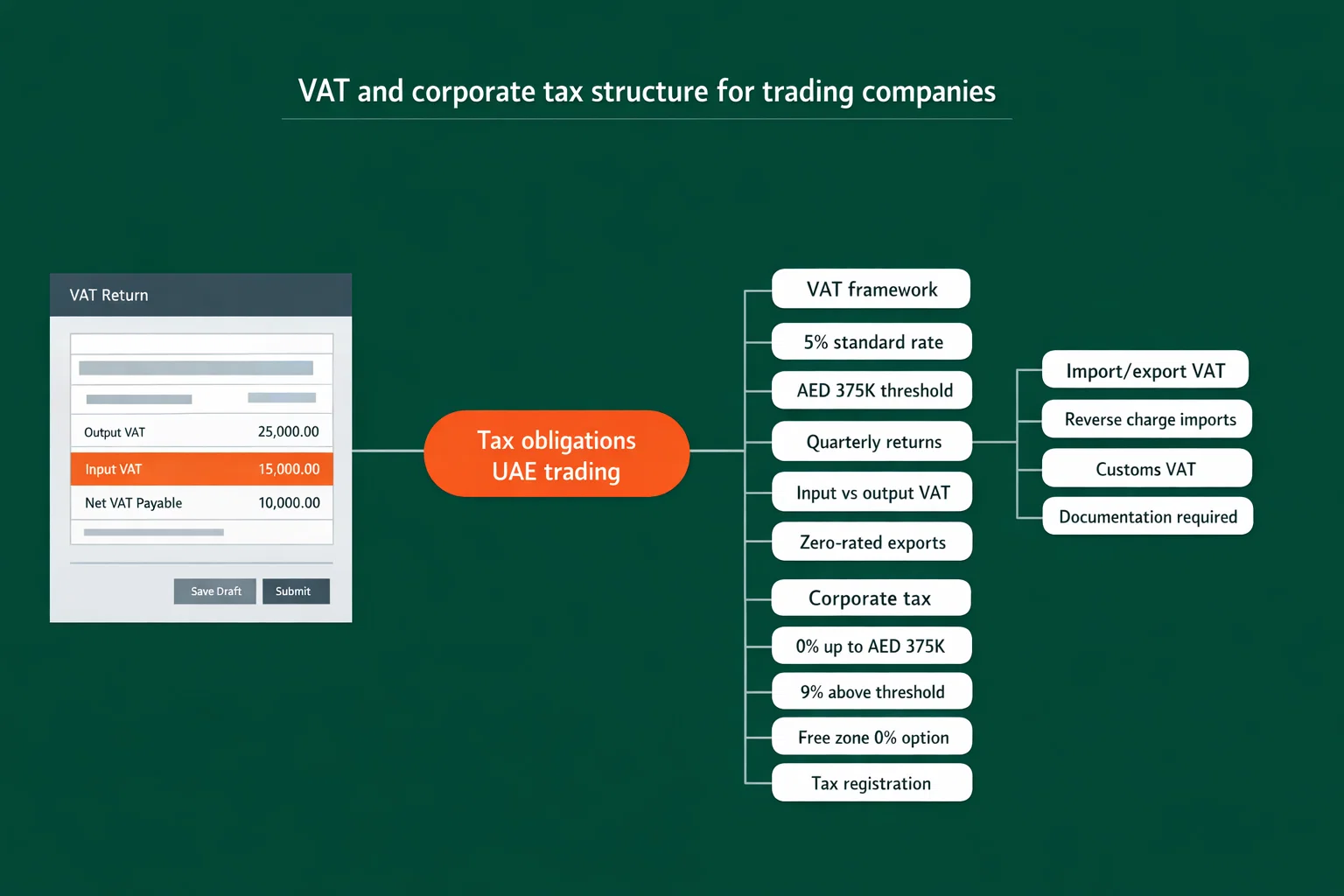

VAT Compliance for General Trading Companies in the UAE

The UAE Value Added Tax system, implemented under Federal Decree-Law No. 8 of 2017, imposes a standard 5% VAT rate on most goods and services supplied within the UAE. Trading companies must register for UAE VAT when their annual taxable supplies exceed AED 375,000 (mandatory threshold) or may opt for voluntary registration when supplies exceed AED 187,500. The Federal Tax Authority administers VAT registration through the EmaraTax portal, requiring trading businesses to submit detailed information about business activities, estimated annual turnover, and bank account details.

VAT accounting for trading companies requires distinguishing between output VAT (charged on sales to UAE customers) and input VAT (paid on business purchases and expenses). Trading businesses can typically recover input VAT on inventory purchases, warehouse costs, transportation expenses, and professional fees, provided these expenses relate to taxable supplies. Companies must issue tax invoices containing prescribed information, including supplier name and Tax Registration Number (TRN), customer details, invoice date, description of goods, taxable amount, and VAT charged at 5%.

VAT return filing occurs quarterly for most trading companies, with businesses reporting total output VAT collected, total input VAT paid, and remitting the net amount to the Federal Tax Authority within 28 days of period end. Trading companies engaged in import activities must account for reverse charge VAT on goods imported from outside the GCC, while exports to non-GCC countries qualify for zero-rating, allowing input VAT recovery without charging output VAT. Penalties for late VAT return filing start at AED 1,000 for the first offense, escalating for repeated non-compliance.

VAT Treatment Scenarios for Trading Companies:

- Local Sales: Standard 5% VAT applies to sales within the UAE

- GCC Imports: The reverse charge mechanism requires the trading company to account for VAT

- Non-GCC Exports: Zero-rated supplies (0% VAT charged, input VAT recoverable)

- Free Zone Sales: Generally outside the UAE VAT scope if goods remain in the free zone

- Business Expenses: Input VAT recoverable on expenses supporting taxable supplies

Corporate Tax Framework in the UAE

UAE Corporate Tax, established through Federal Decree-Law No. 47 of 2022, represents a fundamental shift in the UAE tax landscape, introducing taxation on business profits for financial years beginning on or after June 1, 2023. Trading companies subject to corporate tax face a two-tier rate structure: 0% on taxable income up to AED 375,000 and 9% on taxable income exceeding this threshold. The UAE Corporate Tax Law defines taxable income as accounting profit adjusted for specific additions and deductions outlined in the legislation and supporting Cabinet Decisions.

General trading companies calculate corporate tax liability by starting with net profit per audited financial statements, then applying tax adjustments for non-deductible expenses (such as entertainment exceeding limits, penalties, and certain provisions), exempt income, and allowable deductions. According to the UAE Ministry of Finance Corporate Tax Guide (2023), businesses must maintain audited financial statements for accurate tax determination, with tax returns filed within nine months following the financial year-end through the EmaraTax platform.

Free zone entities may qualify for 0% corporate tax on qualifying income, provided they meet substance requirements and do not conduct business with the mainland UAE. Qualifying free zone persons must maintain adequate assets, sufficient full-time employees, and incur adequate operating expenditure in the UAE. Trading companies operating both mainland and free zone operations must carefully allocate income and expenses to ensure correct tax treatment, maintaining detailed transfer pricing documentation for inter-company transactions.

Corporate Tax Registration Timeline for Trading Companies:

- Pre-June 2024: Companies with financial years starting before June 1, 2023 (transitional rules apply)

- March 1, 2024 onwards: Corporate tax registration portal opened for all UAE businesses

- Within 3 months of license: New companies must register for corporate tax from the formation date

- 9 months after year-end: Corporate tax return filing deadline for each financial year

- 9 months after year-end: Corporate tax payment deadline (no installment payments required)

| Income Level | Corporate Tax Rate | Example Calculation |

| AED 0 – 375,000 | 0% | Taxable profit AED 300,000 = AED 0 tax |

| Above AED 375,000 | 9% on excess | Taxable profit AED 500,000 = AED 11,250 tax [(500,000-375,000) × 9%] |

| Qualifying Free Zone Income | 0% | Subject to meeting substance requirements |

Accounting for Revenue and Expenses in Trading Operations

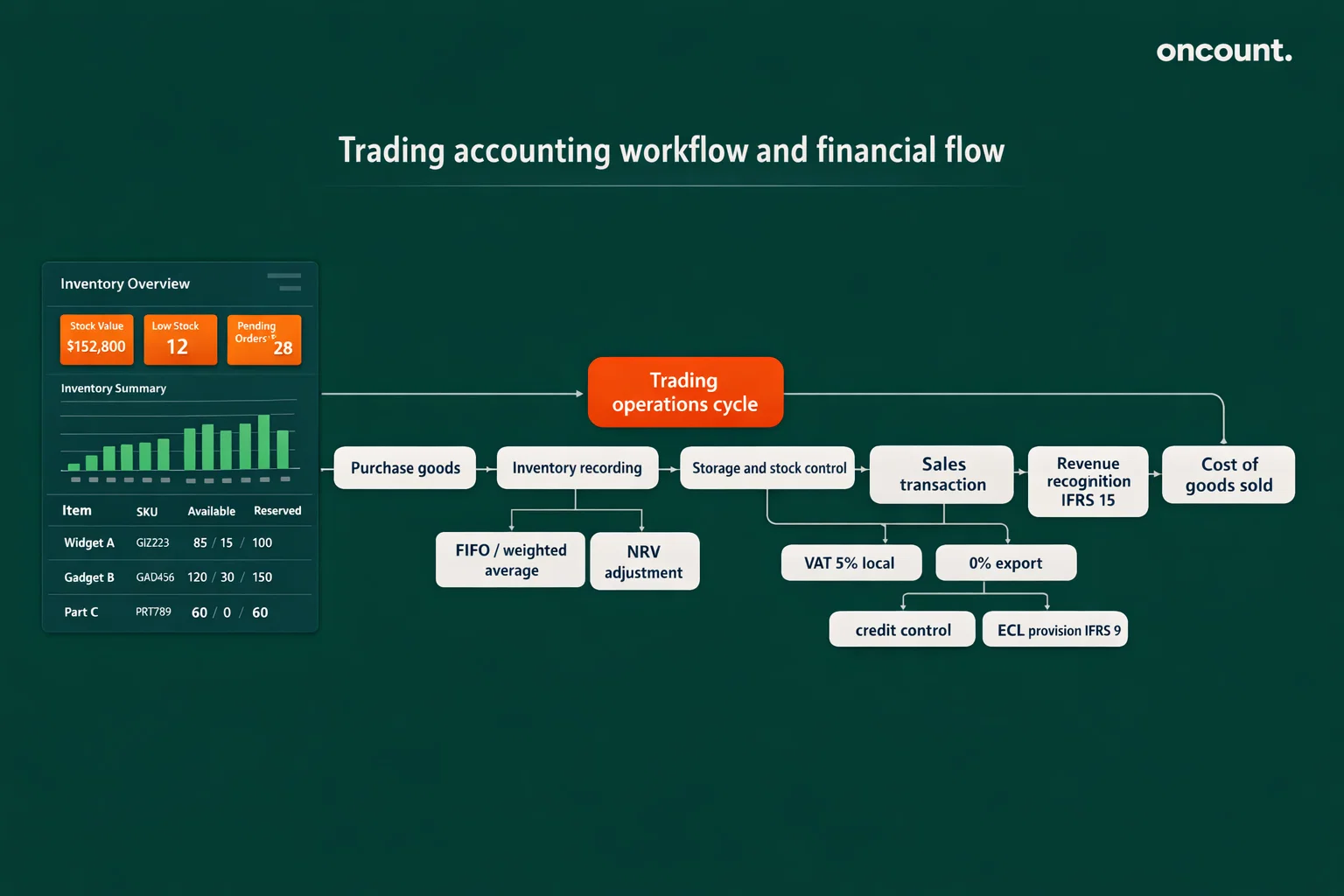

Revenue recognition for trading companies follows IFRS 15 principles, requiring identification of performance obligations, determination of transaction price, and recognition of revenue when control transfers to customers. General trading companies typically recognize revenue at the point of delivery when goods are shipped to customers under agreed Incoterms. Companies operating under consignment arrangements cannot recognize revenue until the consignee sells goods to end customers, maintaining inventory on their balance sheet until the final sale occurs.

The trading sector cost of goods sold comprises the inventory opening balance, plus purchases and import-related costs (customs duties, freight, insurance), minus closing inventory valuation. Trading companies must apply consistent inventory valuation methods, with weighted average and FIFO (first-in-first-out) being most common under IFRS-compliant accounting practices. Inventory write-downs to net realizable value must occur when market prices decline below cost, particularly relevant for trading companies holding fast-moving consumer goods or technology products subject to obsolescence.

Operating expenses for trading businesses include warehouse rental, staff salaries, utilities, marketing costs, bank charges, and professional fees. The UAE Corporate Tax Law permits the deduction of expenses incurred wholly and exclusively for business purposes, requiring trading companies to maintain detailed expense documentation supporting business use. Depreciation on assets such as warehouse equipment, vehicles, and office furniture follows IFRS-compliant useful life estimates, with UAE Corporate Tax allowing tax depreciation aligned with accounting depreciation in most circumstances.

Regulatory Compliance and Reporting Obligations

Economic Substance Regulations impose reporting obligations on UAE companies conducting relevant activities, with trading businesses potentially qualifying as distribution or service center activities. Companies meeting ESR relevant activity criteria must file annual notifications and, if applicable, Economic Substance Reports demonstrating adequate substance in the UAE through core income-generating activities, adequate employees, and appropriate operating expenditure. The UAE Ministry of Finance reviews ESR submissions, with penalties reaching AED 50,000 for failure to file notifications and AED 300,000 for non-compliance with substance requirements.

Anti-Money Laundering regulations under Federal Decree-Law No. 20 of 2018 require trading companies to implement customer due diligence procedures, particularly when establishing relationships with new suppliers or customers. Trading businesses must identify and verify beneficial owners, maintain transaction records for at least five years, and report suspicious transactions to the UAE Financial Intelligence Unit. Companies handling high-value goods or cash transactions face enhanced AML scrutiny, requiring robust internal controls and compliance monitoring.

Ultimate Beneficial Owner requirements mandate that all UAE companies maintain accurate UBO registers identifying individuals holding 25% or more ownership interest or exercising control through other means. Trading companies must submit UBO information to the relevant licensing authority and update records within 15 days of any ownership changes. According to Cabinet Resolution No. 58 of 2020, failure to maintain accurate UBO records can result in administrative penalties and potential license suspension.

Audit Requirements for General Trading Companies in the UAE

Mainland trading companies operating in Dubai and across the UAE must conduct annual audits performed by auditors licensed by the UAE Ministry of Economy. The annual audit requirement applies regardless of company size or turnover, with audit reports forming part of mandatory annual return filings with the Department of Economic Development. Auditors examine whether financial statements present a true and fair view, assess accounting system adequacy, verify asset existence, and confirm compliance with UAE accounting standards and IFRS requirements.

Companies registered in free zones face varying audit requirements depending on specific free zone regulations. Dubai Multi Commodities Centre (DMCC) requires annual audits for all companies, while certain other free zones may exempt small companies from mandatory audits, subject to turnover thresholds. Free zone companies should consult their specific free zone authority to determine applicable audit requirements and ensure compliance with jurisdiction-specific regulations.

The trading company audit process typically spans two to four weeks, involving planning, interim testing, year-end fieldwork, and report finalization. Auditors review inventory count procedures, test trade receivables through customer confirmations, examine purchase and sales transactions, verify bank balances, and assess accounting estimates for reasonableness. Company audits in Dubai must be completed and filed within specified timeframes, typically within three to four months following the financial year-end, to avoid penalties for late submission.

Audit Deliverables for Trading Companies:

- Independent auditor’s report expressing an opinion on financial statements

- Audited balance sheet, profit and loss statement, and cash flow statement

- Notes to financial statements with detailed disclosures

- Management letter highlighting internal control weaknesses (if any)

- Audit file documentation supporting audit conclusions

Industry-Specific Accounting Considerations for Trading Businesses

Inventory Valuation and Management

Trading companies often maintain diverse inventory portfolios across multiple product categories, requiring sophisticated inventory management systems tracking stock levels, movements, and valuations. IFRS-compliant inventory accounting requires trading businesses to apply lower of cost or net realizable value testing, particularly critical during economic downturns when market prices may fall below historical purchase costs. Trading companies must implement regular stock count procedures, ideally conducting full physical counts annually and cycle counts quarterly for high-value inventory categories.

Multi-Currency Transaction Accounting

Trading operations frequently involve transactions in US Dollars, Euros, and other foreign currencies alongside UAE Dirhams, requiring careful application of IAS 21 exchange rate accounting. Trading companies must record foreign currency transactions at spot rates on transaction dates, with monetary items (receivables, payables) retranslated at period-end rates. Exchange differences arising from settlement or retranslation flow through profit or loss, potentially creating volatility in trading company financial results during periods of currency fluctuation.

Import Duty and Customs Accounting

General trading companies importing goods into the UAE must account for customs duties as part of inventory cost under IFRS standards. Import accounting requires tracking customs declaration values, duty rates applicable to specific Harmonized System codes, and additional charges such as municipality fees. Trading companies should maintain detailed customs documentation supporting duty calculations, as these records form part of both financial audit requirements and potential Federal Tax Authority VAT audits.

Credit Risk and Provision for Doubtful Debts

Trading businesses extending credit terms to UAE customers must assess expected credit losses under IFRS 9, establishing provisions for trade receivables unlikely to be collected. Provision calculations typically consider customer payment histories, current economic conditions, and forward-looking information affecting customer creditworthiness. Trading companies should implement credit control procedures, including customer credit assessments, aging analysis reviews, and collection follow-up processes, to minimize bad debt exposure.

Common Accounting Challenges for Trading Companies

Trading companies in the UAE frequently encounter challenges related to inventory record accuracy, particularly when managing high transaction volumes across multiple warehouse locations. Discrepancies between physical stock counts and accounting records often arise from unrecorded damages, theft, or data entry errors, requiring robust inventory control procedures and regular reconciliation processes. Companies lacking proper warehouse management systems struggle to maintain real-time visibility of stock levels, leading to stockouts, overstocking, and inaccurate cost of goods sold calculations.

VAT compliance complexity represents another significant challenge, especially for trading companies handling mixed supplies, free zone transactions, and cross-border movements. Common errors include incorrect VAT treatment of exports, failure to apply reverse charge mechanisms on imports, and improper documentation of tax invoices. These errors can trigger FTA audits, resulting in VAT assessments, penalties, and interest charges that significantly impact trading company cash flow and profitability.

Inadequate segregation of duties within accounting functions creates risks of fraud and error, particularly in smaller trading operations lacking sufficient staff to implement proper internal controls. Trading businesses should separate purchasing, receiving, payment authorization, and bank reconciliation functions to prevent unauthorized transactions and detect errors promptly. Weak internal controls become especially problematic during corporate tax compliance, as the Federal Tax Authority expects businesses to maintain adequate systems preventing tax evasion and ensuring accurate tax determinations.

Financial Consequences of Common Errors:

| Error Type | Regulatory Impact | Financial Consequence |

| Late VAT filing | FTA penalties | AED 1,000 – 10,000 per offense |

| Incorrect VAT treatment | Tax assessment | Additional VAT plus 5-10% penalty |

| Missing audit deadline | DED penalties | License suspension risk |

| Poor inventory controls | Audit qualification | Investor confidence loss |

| Inadequate ESR filing | MOF penalties | AED 50,000 – 300,000 |

Best Practices for Accounting and Financial Management

Implementation of cloud-based accounting software systems enables trading companies to maintain accurate, accessible financial records while supporting remote access for stakeholders. Leading platforms such as Zoho Books, QuickBooks, and Xero offer UAE VAT compliance features, multi-currency support, and integration capabilities with banking systems and e-commerce platforms. Trading businesses should select accounting software providing robust inventory management modules, automated bank reconciliation, and financial reporting aligned with IFRS presentation requirements.

Regular internal financial reviews strengthen trading company financial management, with management accounts prepared monthly to track performance against budgets and prior periods. Trading companies benefit from implementing key performance indicator (KPI) monitoring covering gross profit margins by product line, inventory turnover ratios, debtor days outstanding, and working capital ratios. Monthly financial reviews should include variance analysis explaining significant deviations from the budget or forecast, enabling management to take corrective action promptly.

Engagement of qualified accounting professionals, whether through in-house hiring or outsourcing to specialized accounting and bookkeeping services in UAE, ensures compliance with complex UAE regulations while maintaining accurate financial reporting standards. Professional accountants bring expertise in IFRS application, tax planning strategies, and regulatory updates affecting trading businesses. Periodic compliance audits conducted by external advisors help identify gaps in tax compliance, ESR reporting, or AML procedures before regulatory examinations occur.

Financial Management Best Practices:

- Automate routine processes: Bank feeds, invoice scanning, expense categorization

- Implement approval workflows: Purchase order approvals, payment authorizations, journal entry reviews

- Conduct regular training: Staff education on VAT rules, IFRS updates, and system usage

- Maintain document management: Organized digital filing of contracts, invoices, and customs documents

- Schedule periodic reviews: Quarterly management accounts, semi-annual compliance reviews, annual strategy sessions

Comparison: Free Zone vs Mainland Accounting Requirements

| Aspect | Mainland Trading Companies | Free Zone Trading Companies |

| Corporate Tax Treatment | Subject to 9% corporate tax on profits above AED 375,000 | May qualify for 0% tax on qualifying income if substance requirements are met |

| Audit Requirements | Mandatory annual audit for all companies | Varies by free zone; DMCC requires audits, others may have thresholds |

| VAT Registration | Mandatory if turnover exceeds AED 375,000 | Same threshold applies; exports outside the UAE are typically zero-rated |

| Accounting Standards | UAE accounting standards aligned with IFRS | IFRS standards are directly applicable |

| ESR Obligations | Subject to ESR if conducting relevant activities | Subject to ESR, many trading activities qualify as relevant |

| License Renewal Process | Annual renewal with DED; audit report required | Annual renewal with free zone authority; audit report if applicable |

| UBO Reporting | Required through DED systems | Required through the free zone authority |

| Operating Restrictions | Can trade throughout the UAE and internationally | May face restrictions on mainland UAE trade depending on license type |

| Banking Requirements | Corporate accounts with UAE banks | Corporate accounts required; some free zones have bank partnerships |