Key Takeaways

- IFRS 15 Revenue Recognition: Engineering companies must recognize contract revenue over time using cost-to-cost or output methods when performance obligations are satisfied progressively.

- UAE Corporate Tax: The corporate tax regime applies a 9% rate to taxable profits exceeding AED 375,000, with qualifying free zone entities potentially eligible for 0% rates.

- VAT Registration Threshold: Mandatory VAT registration triggers at AED 375,000 in annual taxable supplies, with engineering firms required to account for output VAT on certified progress billings, including retention amounts.

- Retention Receivables: Amounts withheld by clients (typically 5-10% of each certificate) require classification as contract assets or trade receivables with expected credit loss provisions under IFRS 9.

- Project Accounting Systems: Engineering entities must implement dual-layer bookkeeping combining enterprise-level IFRS reporting with granular project-level cost tracking.

- Audit Obligations: Most engineering companies require annual statutory audits with financial statements submitted to the relevant UAE authorities within specified deadlines.

- GPSSA Contributions: Employers hiring UAE nationals must remit 15% of the salary (12.5% for salaries ≥ AED 20,000) plus 11% employee contribution to the General Pension and Social Security Authority.

Overview of Accounting Requirements in the UAE For Engineering Companies

The UAE Commercial Companies Law establishes the legal foundation requiring all companies to maintain accounting records that present a true and fair view of financial position and performance. Engineering firms in the UAE must retain comprehensive documentation, including general ledgers, project contracts, progress certificates, payroll records, and supplier invoices for a minimum of five years from the end of the relevant financial period.

The Federal Tax Authority mandates that accounting records must be sufficient to determine tax liabilities accurately. Engineering companies operating across mainland UAE jurisdictions face identical record-keeping obligations, while entities in the Dubai International Financial Centre (DIFC) must preserve records for six years, and Abu Dhabi Global Market (ADGM) entities for ten years.

The UAE Ministry of Finance requires engineering businesses to prepare annual financial statements under International Financial Reporting Standards. This mandatory IFRS adoption applies regardless of company size, ownership structure, or operational jurisdiction within the UAE market. Engineering companies must establish accounting systems capable of capturing complex project transactions, including mobilization advances, stage payments, variation orders, retention withholdings, and defect liability provisions.

Proper accounting frameworks for engineering entities necessitate integration between project management systems and financial reporting platforms. This integration ensures accurate cost allocation, timely revenue recognition, and reliable work-in-progress valuation essential for stakeholder decision-making and regulatory compliance.

IFRS Application for Engineering Companies

International Financial Reporting Standards issued by the International Accounting Standards Board govern financial reporting for UAE companies, including engineering entities. The framework ensures transparency, comparability, and reliability in financial statements prepared by businesses operating in the UAE.

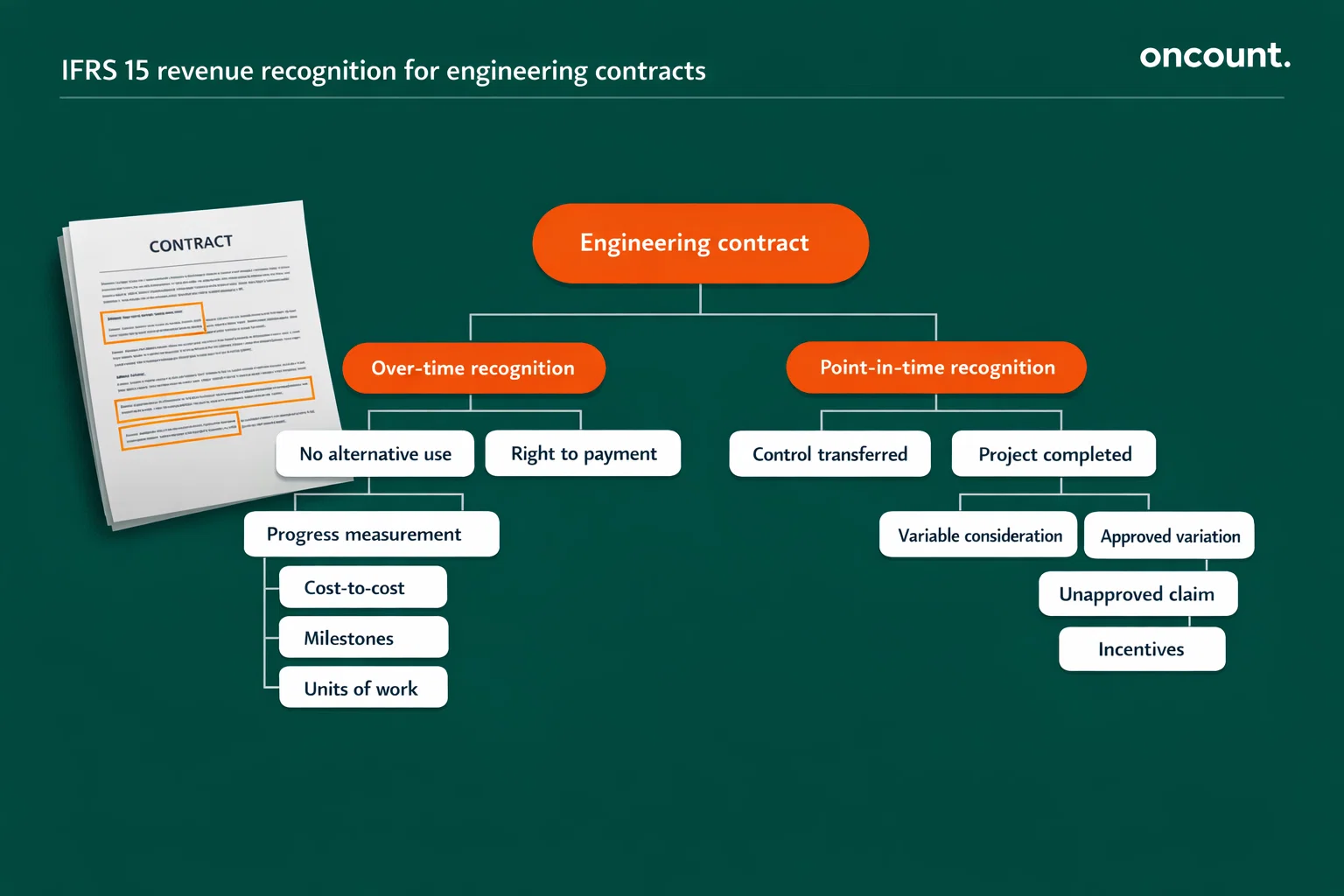

IFRS 15 Revenue from Contracts with Customers establishes the primary revenue recognition framework for engineering companies. The standard requires entities to identify performance obligations within contracts, determine transaction prices, allocate prices to obligations, and recognize revenue when (or as) performance obligations are satisfied. Engineering contracts typically qualify for overtime revenue recognition when the contractor creates an asset with no alternative use and possesses an enforceable right to payment for performance completed to date.

Engineering companies apply progress measurement methods, including cost-to-cost calculations where revenue equals (costs incurred ÷ total estimated costs) × contract price. Alternative output methods based on milestones, surveys, or units of work may be appropriate when they faithfully represent the transfer of control to customers. The Federal Tax Authority expects engineering businesses to maintain detailed documentation supporting revenue recognition judgments for both financial reporting and tax purposes.

IFRS 9 Financial Instruments governs accounting for retention receivables held by engineering companies. These amounts withheld by clients require expected credit loss (ECL) provisioning based on historical collection patterns, client creditworthiness, and current economic conditions. Engineering entities must assess whether retention amounts represent contract assets (conditional on future performance) or trade receivables (conditional only on time passage).

IFRS 16 Leases impacts engineering companies utilizing equipment rentals, vehicle leases, or site office arrangements. Lessees recognize right-of-use assets and corresponding lease liabilities for contracts conveying the right to control asset use for specified periods. Short-term leases (twelve months or less) and low-value asset leases may be exempted from capitalization requirements.

IAS 2 Inventories applies to materials held by engineering firms, including steel, cement, electrical components, and consumables. Engineering companies value inventory at the lower of cost or net realizable value, with cost determination following first-in-first-out (FIFO) or weighted average methods.

IAS 16 Property, Plant and Equipment governs capitalization thresholds, depreciation methodologies, and impairment assessments for construction equipment, vehicles, machinery, and office assets owned by engineering entities.

Bookkeeping Framework and Financial Records Structure

Engineering companies require robust bookkeeping systems capturing financial transactions at both entity and project levels. The general ledger structure should facilitate consolidated financial reporting while enabling project-specific profitability analysis and cost control.

Chart of Accounts Design

A comprehensive chart of accounts for engineering businesses incorporates:

Assets:

- Cash and bank accounts (including project-specific escrow accounts)

- Trade receivables categorized by project and client

- Retention receivables are tracked separately with aging analysis

- Contract assets representing unbilled revenue

- Inventory of materials (site-specific and central warehouse)

- Prepaid expenses (insurance, mobilization costs)

- Property, plant, and equipment (machinery, vehicles, computers)

- Right-of-use assets from lease arrangements

Liabilities:

- Trade payables to suppliers and subcontractors

- Accrued subcontractor costs

- VAT payable to the Federal Tax Authority

- Contract liabilities (billing exceeding revenue recognized)

- Mobilization advance liabilities

- Provisions for warranties, defects, and onerous contracts

- Performance bond obligations

Equity:

- Share capital

- Statutory reserves

- Retained earnings

Revenue:

- Contract revenue from base agreements

- Approved variation order revenue

- Work-in-progress adjustments

Costs:

- Direct labor wages

- Subcontractor expenses

- Materials consumed

- Equipment rental and depreciation

- Site overhead allocations

- General and administrative expenses

Transaction Documentation

Engineering entities must maintain supporting documentation, including signed contracts, approved variation orders, engineer’s certifications, quantity surveyor progress reports, supplier invoices with valid tax registration numbers (TRNs), payroll records compliant with Wages Protection System (WPS) requirements, and bank statements reconciled to accounting records.

Project-level cost tracking requires tagging expenses to specific jobs using project codes and cost categories. This dimensional accounting enables accurate job costing, variance analysis, and performance measurement essential for engineering project management.

Financial Statement Preparation Requirements

UAE companies must prepare annual financial statements comprising a balance sheet, profit and loss statement, cash flow statement, statement of changes in equity, and comprehensive notes disclosing accounting policies and supporting details.

Balance Sheet Components

Engineering companies present their financial position showing assets (current and non-current), liabilities (current and non-current), and equity. Contract assets and contract liabilities appear as separate line items with detailed reconciliations in the notes. Retention receivables may be classified as current or non-current based on expected collection timing.

Profit and Loss Statement

The income statement for engineering entities typically presents revenue from contracts, direct costs (labor, materials, subcontractors), gross profit, operating expenses (administrative, marketing), depreciation, finance costs, and profit before tax. Engineering companies often provide supplementary project-level profit and loss analysis for management purposes.

Cash Flow Statement

Engineering businesses prepare cash flow statements using either the direct or the indirect method. Operating activities include cash receipts from clients (including retention releases), payments to suppliers and subcontractors, employee salaries through WPS, and VAT settlements with the Federal Tax Authority. Investing activities capture equipment purchases and disposals, while financing activities reflect loan drawdowns, repayments, and dividend distributions.

Notes to Financial Statements

Comprehensive disclosures required for engineering companies include:

- Accounting policies for revenue recognition, including progress measurement methods

- Contract asset and liability reconciliations showing opening balances, additions, revenue recognized, billings, and closing balances

- Disaggregation of revenue by contract type, geographic region, or client category

- Expected credit loss methodology and assumptions

- Commitments and contingencies from performance bonds and guarantees

- Related-party transactions with group entities

- Significant judgments affecting variable consideration estimates and cost-to-complete projections

Accurate financial statement preparation supports regulatory compliance, facilitates external audits, enables informed stakeholder decisions, and forms the foundation for corporate tax calculations.

VAT Compliance for Engineering Companies in the UAE

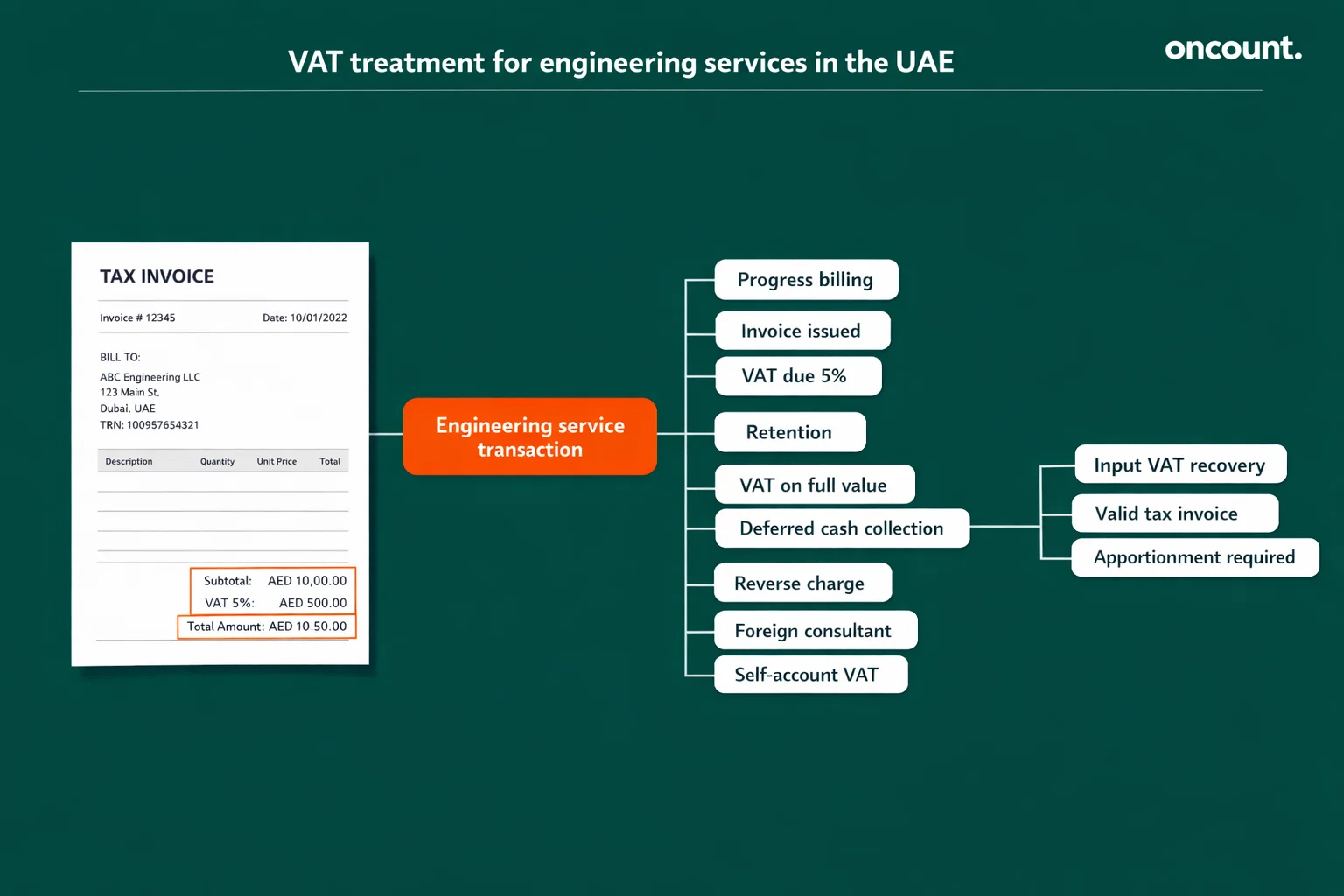

Value Added Tax, administered by the Federal Tax Authority, applies to engineering services and supplies at the standard 5% rate per Federal Decree-Law No. 8 of 2017. Engineering companies must register for VAT when annual taxable supplies exceed AED 375,000, with voluntary registration available at an AED 187,500 threshold.

VAT Registration Process

Engineering entities register through the Federal Tax Authority’s EmaraTax portal, providing trade license details, shareholder information, estimated annual turnover, and authorized signatory documentation. Upon approval, the FTA issues a unique Tax Registration Number (TRN) that must appear on all tax invoices.

Output VAT on Progress Billings

Engineering companies charge 5% VAT on certified amounts invoiced to clients. Output VAT becomes due when the earlier of billing or payment occurs. Progress certificates issued by quantity surveyors or project engineers trigger VAT obligations on the gross certified amount, including retention portions.

Retention amounts withheld by clients remain subject to VAT at the initial certification date. Engineering entities must account for output VAT on retention even when cash collection is deferred. The Federal Tax Authority expects proper documentation showing the VAT calculation on total certified values regardless of payment terms.

Input VAT Recovery

Engineering companies recover input VAT incurred on business purchases, including materials, subcontractor services, equipment rentals, and professional fees. Valid tax invoices containing supplier TRNs, descriptions, amounts, and separate VAT line items are mandatory for input VAT claims.

Mixed-use scenarios involving exempt supplies (such as residential property leasing) may require input VAT apportionment. Engineering firms should calculate recovery percentages based on taxable versus total supplies, subject to Federal Tax Authority approval for specified methods.

Reverse Charge Mechanism

Engineering companies importing services from foreign suppliers (such as design consultants or specialist advisors) apply the reverse charge mechanism. The UAE recipient accounts for both output VAT and corresponding input VAT, with a net nil impact when fully recoverable. Tax invoices must clearly state “reverse charge applies.”

VAT Return Filing

The Federal Tax Authority requires monthly VAT returns for businesses exceeding AED 150 million annual taxable supplies, with quarterly filing available for smaller entities. Engineering companies submit returns through EmaraTax showing output VAT collected, input VAT claimed, and the net payment or refund position.

Late filing or payment attracts penalties, including AED 1,000 for first-time late filing, AED 2,000 for subsequent occurrences within 24 months, plus daily penalties capping at the total tax due. Engineering entities should implement calendar reminders and reconciliation procedures, ensuring timely compliance.

Corporate Tax Framework in the UAE

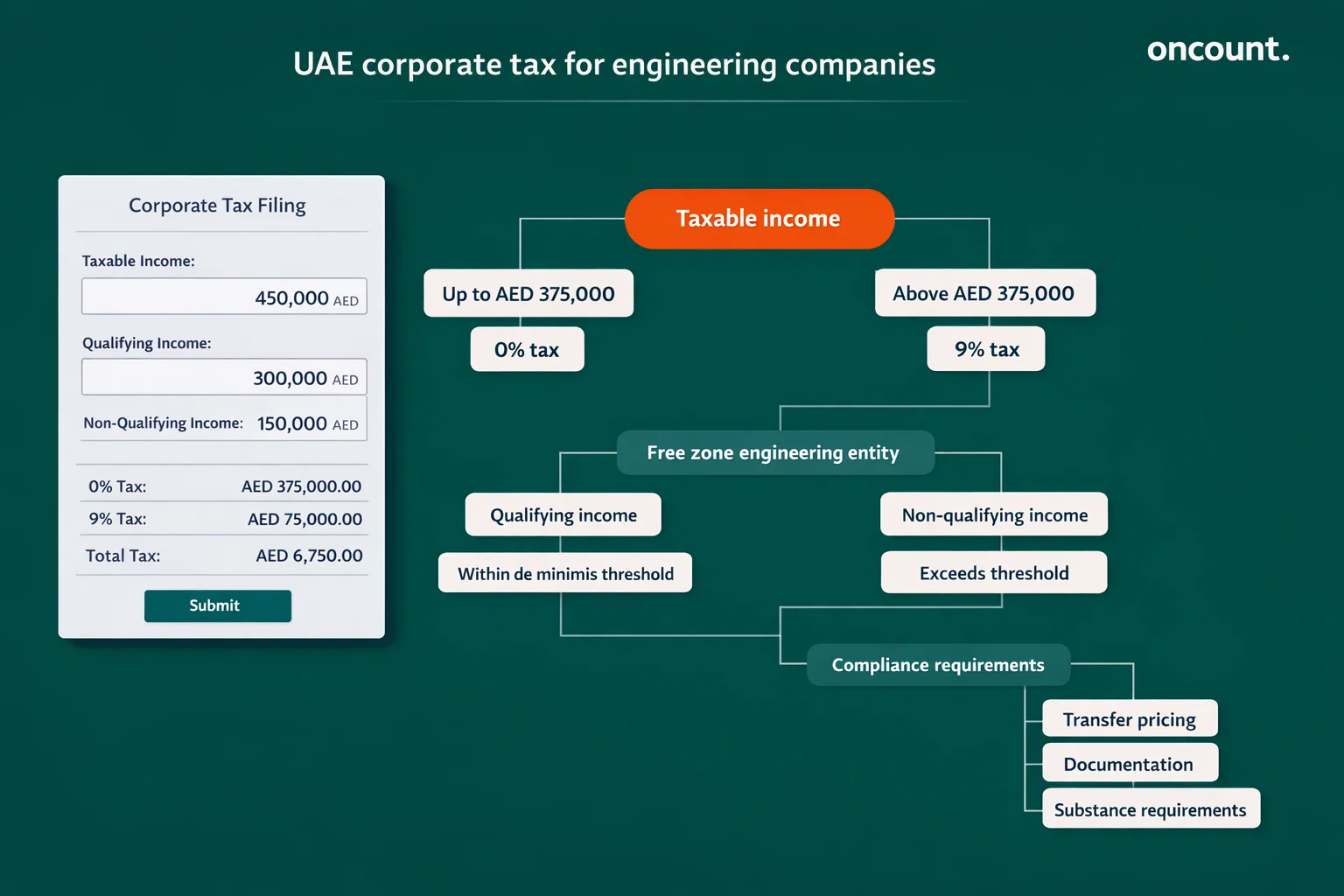

Federal Decree-Law No. 47 of 2022 establishes the UAE corporate tax regime applicable to business profits from financial years beginning on or after June 1, 2023. Engineering companies face corporate tax obligations regardless of ownership structure, with specific rates and exemptions defined by tax laws.

Tax Rates and Thresholds

The UAE corporate tax regime applies:

- 0% tax rate on taxable income up to AED 375,000

- 9% tax rate on taxable income exceeding AED 375,000

Qualifying Free Zone Persons may benefit from 0% tax rate on qualifying income, provided non-qualifying income remains below 5% of total revenue or AED 5 million (de minimis threshold). Engineering companies in free zones must carefully document client contracts to substantiate qualifying versus non-qualifying income classifications.

Taxable Income Calculation

Engineering entities determine taxable income starting from IFRS-based accounting profit and applying tax adjustments. Typical modifications include:

Add-backs:

- Fines and penalties

- Excessive related-party charges above arm’s length pricing

- Provisions not yet crystallized

- Entertainment expenses beyond allowable limits

Deductions:

- Capital allowances on qualifying assets

- Tax depreciation following prescribed rates

- Actual warranty costs incurred

- Doubtful debt write-offs with supporting evidence

Engineering companies must reconcile work-in-progress schedules and contract asset balances from IFRS financial statements to ensure alignment with tax revenue recognition principles. The Federal Tax Authority expects detailed documentation supporting timing differences and permanent adjustments.

Transfer Pricing Requirements

Related-party transactions require arm’s length pricing with documentation including master files (group structure, business activities, intangibles) and local files (transaction details, comparability analysis, pricing justification). Engineering groups with cross-border or intra-group contracts must prepare transfer pricing documentation supporting subcontracting arrangements, management fees, royalties, and financing transactions.

Tax Registration and Filing

Engineering companies register for corporate tax through the EmaraTax portal within specified deadlines. Tax returns are due within nine months following the financial year-end, with payments required within the same timeframe. Penalties apply for late registration (AED 10,000), late filing, and late payment.

Accounting for Revenue and Expenses in Engineering Companies

Engineering businesses recognize revenue using methods aligned with contract structures and performance obligation characteristics under IFRS 15.

Contract Revenue Recognition

Engineering contracts include various types:

| Contract Type | Revenue Recognition Approach | Progress Measurement |

| Lump-Sum Fixed-Price | Over-time (typically) | Cost-to-cost percentage |

| Cost-Plus Reimbursable | Over-time | Costs incurred plus agreed fee |

| Unit-Price | Over-time | Units completed × contract rate |

| EPC (Engineering-Procurement-Construction) | Over-time (single obligation) | Cost-to-cost or milestones |

| Consultancy Services | Over-time | Time expended × hourly rates |

Cost-to-Cost Method

Engineering companies commonly apply cost-to-cost progress measurement: Revenue recognized = (Cumulative costs incurred ÷ Total estimated costs) × Contract price

This method requires monthly updates to cost-to-complete estimates incorporating actual costs, committed purchase orders, subcontractor quotes, and projected site overhead allocations. Engineering project managers collaborate with finance teams to ensure reliable forecasting.

Variable Consideration

Variation orders, claims, incentive payments, and liquidated damages constitute variable consideration requiring constraint analysis. Engineering companies recognize variable amounts only when highly probable that significant revenue reversals will not occur. Approved variation orders increase contract price immediately, while disputed claims require conservative estimation pending engineer certification or adjudication.

Mobilization Advances

Upfront payments received from clients are recorded as contract liabilities and systematically released to revenue as performance obligations are satisfied. Engineering entities should align mobilization advance recognition with actual work progression rather than predetermined schedules.

Expense Classification

Engineering companies categorize costs as:

Direct Costs:

- Labor wages for site personnel and engineers

- Subcontractor charges verified through progress certificates

- Materials consumed with quantity reconciliations

- Equipment rental charges or depreciation allocations

- Site establishment and temporary facilities

Indirect Costs:

- Head office salaries and benefits

- Depreciation on non-project assets

- Marketing and business development expenses

- Professional fees for legal and accounting services

- Information technology and software subscriptions

Overhead allocation to projects follows consistent methodologies such as percentage of direct labor cost or direct cost base, ensuring accurate project profitability measurement.

Regulatory Compliance and Reporting Obligations

Engineering companies in the UAE navigate multiple regulatory frameworks beyond taxation and financial reporting requirements.

Economic Substance Regulations

The UAE’s Economic Substance Regulations (ESR) require certain businesses to demonstrate adequate economic presence relative to activities conducted. Engineering companies may qualify as “relevant activities” if performing construction, installation, or related services. Entities must file annual ESR notifications and reports through the relevant regulatory authority (Ministry of Finance for mainland, DIFC Authority, or ADGM Registration Authority).

ESR compliance necessitates documentation proving:

- Core income-generating activities occur in the UAE

- Adequate full-time employees with necessary qualifications

- Adequate operating expenditure incurred in the UAE

- Adequate physical assets present in the UAE

- Direction and management conducted in the UAE

Engineering firms should maintain evidence including employment records, office lease agreements, equipment purchase documentation, board meeting minutes held in the UAE, and operational expense receipts.

Ultimate Beneficial Owner Regulations

UAE Cabinet Resolution No. 58 of 2020 requires companies to identify and register Ultimate Beneficial Owners (UBOs) holding 25% or more ownership interests. Engineering entities must maintain UBO registers at registered offices, with updates submitted to licensing authorities and the Central Bank of the UAE through the UBO e-Services platform.

Anti-Money Laundering Requirements

Engineering companies fall within the AML regulatory scope when conducting designated non-financial business activities. Entities must implement risk-based AML programs, including customer due diligence, transaction monitoring, suspicious activity reporting, and employee training. The UAE’s Financial Intelligence Unit provides guidance for compliance obligations.

Labor Law Compliance

Federal Decree-Law No. 33 of 2021 governs employment relationships, requiring timely wage payments through the Wages Protection System administered by the Ministry of Human Resources and Emiratisation. Engineering companies must process monthly payroll through WPS-approved financial institutions, maintaining records of employee contracts, visa documentation, end-of-service benefit accruals, and annual leave entitlements.

Audit Requirements for Engineering Companies in the UAE

Most engineering entities require annual statutory audits by UAE-licensed auditors registered with relevant authorities.

Mainland Company Audits

UAE Commercial Companies Law mandates annual audits for limited liability companies and public joint stock companies regardless of size or revenue. Engineering firms must appoint external auditors at shareholder meetings, provide complete accounting records and supporting documentation, and file audited financial statements with the Department of Economic Development within specified deadlines.

Free Zone Audit Requirements

DIFC Companies Law requires annual audits for all companies except qualifying small private companies meeting strict criteria (rarely applicable to engineering entities given asset values and revenue thresholds). ADGM regulations similarly mandate audits with limited exemptions for dormant companies.

Auditor Expectations

External auditors examine engineering companies’ financial statements, focusing on:

- Revenue recognition policies and work-in-progress calculations

- Contract asset and liability classifications

- Retention receivable valuations and ECL provisions

- Provisions for warranties, defects, and onerous contracts

- Related-party transaction pricing and disclosures

- VAT compliance and reconciliations

- Transfer pricing documentation for group transactions

Engineering firms should prepare comprehensive audit files, including:

- Signed contracts with all amendments and variation orders

- Engineer’s certifications and quantity surveyor progress reports

- Subcontractor invoices and payment certificates

- Materials purchase orders, delivery notes, and supplier invoices

- WIP schedules reconciled to general ledger balances

- Board meeting minutes approving budgets and major contracts

Audit Timeline

UAE authorities typically require audited financial statement submission within four to six months following financial year-end, with specific deadlines varying by jurisdiction. Engineering companies should engage auditors early in the closing process to facilitate timely completion.

Industry-Specific Accounting Considerations for Engineering Companies

Contract Assets and Liabilities Management

Engineering entities must carefully distinguish between contract assets (unbilled revenue conditional on future performance), trade receivables (unconditional rights to payment), and contract liabilities (obligations to transfer services for advance payments). The Federal Tax Authority examines these classifications when assessing corporate tax calculations.

Joint Venture Accounting

Engineering projects frequently involve joint operations with multiple contractors sharing project execution. IFRS 11 requires participants to recognize their proportionate shares of assets, liabilities, revenues, and expenses. Unincorporated joint ventures operating in the UAE should establish clear agreements defining cost allocation methodologies, billing responsibilities, and VAT registration approaches.

Retention Receivable Treatment

Retention amounts (typically 5-10% of certified values) withheld by clients require careful accounting treatment. Engineering companies assess whether retentions represent:

- Contract assets (if conditional on defect-free completion)

- Trade receivables (if conditional only on time passage)

Expected credit loss provisions apply to both categories based on client creditworthiness and historical collection patterns. Engineering entities should age receivables and adjust provisions when collection becomes doubtful.

Warranty and Defect Provisions

Engineering contracts commonly include defect liability periods requiring contractors to remedy workmanship deficiencies. Companies recognize provisions when present obligations exist from past events, outflows are probable, and amounts can be reliably estimated. Provision calculations consider historical defect rates, project complexity, and specific warranty terms.

Onerous Contract Provisions

When total contract costs exceed expected revenues, engineering companies recognize provisions for anticipated losses immediately. These provisions require careful judgment assessing cost-to-complete estimates, potential claims, and liquidated damage exposures.

Common Accounting Challenges for Engineering Companies

Inaccurate Revenue Recognition

Engineering entities frequently struggle with revenue timing, particularly when applying cost-to-cost methods without rigorous cost-to-complete updates. Delayed project manager input, unreliable subcontractor quotations, or failure to incorporate scope changes can materially misstate work-in-progress and profitability.

Inadequate Documentation

Missing variation order approvals, unsigned certifications, or incomplete subcontractor records create audit difficulties and tax compliance risks. The Federal Tax Authority may disallow revenue recognition or expense deductions lacking proper supporting evidence.

VAT Compliance Errors

Common mistakes include:

- Failing to account for output VAT on retention amounts

- Claiming input VAT without valid tax invoices

- Incorrect reverse charge applications on imported services

- Missed filing deadlines triggering penalties

Weak Project Cost Controls

Engineering companies without integrated project accounting systems struggle with:

- Delayed cost allocation to projects

- Unrecorded commitments from purchase orders

- Materials charged to incorrect projects

- Overhead allocation inconsistencies

Transfer Pricing Gaps

Engineering groups with related-party subcontracting or shared services often lack documentation proving arm’s length pricing, creating corporate tax risks during Federal Tax Authority reviews.

Best Practices for Accounting and Financial Management

Implement Robust Accounting Systems

Engineering companies should deploy cloud-based ERP platforms with integrated project accounting modules enabling:

- Real-time cost tracking by project and cost code

- Automated progress billing with retention calculations

- Work-in-progress reporting with variance analysis

- VAT accounting, including reverse charge flagging

- Corporate tax reconciliation capabilities

Establish Month-End Close Procedures

Disciplined closing processes ensure timely financial reporting:

Day 1-3: Capture all costs, including supplier invoices, subcontractor certificates, and payroll

Day 3-5: Project managers update cost-to-complete estimates

Day 5-7: Finance calculates WIP applying progress methods

Day 7-8: Variance analysis reviewing loss-making projects and major changes

Day 8-10: Finalize financial statements with project-level profit and loss

Maintain Comprehensive Documentation

Engineering entities should retain organized files containing:

- Executed contracts with all amendments

- Approved variation orders with supporting correspondence

- Engineer’s certifications and quantity surveyor reports

- Subcontractor agreements and progress certificates

- Materials purchase orders with delivery confirmations

- Board resolutions approving budgets and significant contracts

Conduct Regular Compliance Reviews

Quarterly compliance health checks should assess:

- VAT invoice completeness and accuracy

- Transfer pricing documentation currency

- ESR notification filing status

- UBO register updates

- WPS payroll compliance

- Statutory reporting deadline tracking

Engage Professional Advisors

Engineering companies benefit from specialized professional accounting services for:

- IFRS 15 implementation and revenue recognition policies

- VAT structuring on complex mixed-use projects

- Corporate tax planning, optimizing free zone benefits

- Transfer pricing documentation and arm’s length analysis

- Accounting system selection and implementation

- Audit preparation and regulatory liaison

Comparison: Free Zone vs Mainland Accounting Requirements

| Requirement | Mainland Engineering Companies | Free Zone Engineering Companies |

| Corporate Tax Rate | 0% up to AED 375,000; 9% above | 0% on qualifying income if de minimis met; 9% on non-qualifying |

| IFRS Compliance | Mandatory per UAE Ministry of Finance | Mandatory per DIFC/ADGM regulations |

| Audit Requirement | Annual statutory audit mandatory | Annual audit mandatory (limited exemptions) |

| VAT Registration | Mandatory at an AED 375,000 threshold | The same threshold applies |

| VAT Rate | 5% standard rate | 5% standard rate |

| Record Retention | Minimum 5 years | 6 years (DIFC), 10 years (ADGM) |

| ESR Reporting | Through the Ministry of Finance | Through the respective free zone authority |

| Transfer Pricing | Full documentation required | Full documentation required |

| Customs Duty | 5% on imports | Exemptions on re-export; 5% on the UAE market entry |

| Operational Flexibility | Mainland market access | May require a service agent for mainland contracts |

Free zone engineering companies must carefully document contract structures to substantiate qualifying income status. Mainland client contracts may constitute non-qualifying income triggering 9% corporate tax, while free zone-to-free zone services qualify for 0% rates subject to substance requirements.