Key Takeaways

- IFRS 15 compliance is mandatory for construction revenue recognition, requiring performance obligation analysis and stage-of-completion measurement

- Corporate tax at 9% applies to taxable profits exceeding AED 375,000 for financial years beginning on or after June 1, 2023

- VAT registration becomes mandatory when taxable supplies exceed AED 375,000 in 12 months, with special rules for progress billing and retention

- Project accounting systems must track costs, revenue, and billings at the individual contract level to support WIP schedules

- Contract assets and liabilities replace traditional accounts receivable for unbilled revenue and advance payments

- Free zone entities may qualify for 0% corporate tax rate on qualifying income if specific conditions are met

- Accounting records retention requires a minimum of five years under the UAE Commercial Companies Law, with DIFC requiring six years and ADGM requiring ten years

- Audit requirements vary by jurisdiction but are typically mandatory for construction firms due to licensing authority expectations

Overview of Accounting Requirements in the UAE for Construction Companies

The UAE Commercial Companies Law establishes the foundational obligation for companies operating across the UAE to maintain proper accounting records. Construction companies in the UAE must prepare financial statements that present a true and fair view of financial position and performance, adhering to internationally recognized accounting frameworks.

The UAE Ministry of Finance emphasizes alignment with International Financial Reporting Standards (IFRS) as the primary accounting framework for commercial entities. This requirement ensures construction firms maintain transparent, comparable financial reporting that meets investor and lender expectations.

Construction firms must maintain comprehensive accounting records, including general ledgers, subsidiary ledgers for projects, procurement documentation, subcontractor certificates, payroll records aligned with the Wage Protection System, and bank reconciliations. These records form the foundation for both management decision-making and regulatory compliance.

Record retention requirements mandate that accounting documentation be preserved for a minimum of five years from the end of the financial year to which they relate. Financial free zones impose extended retention periods that construction companies must understand.

The Dubai International Financial Centre (DIFC) requires at least six years under DIFC Companies Law provisions. The Abu Dhabi Global Market (ADGM) mandates a minimum ten-year retention period according to ADGM Registration Authority guidance. Companies operating in these jurisdictions must implement document management systems that ensure compliance with these extended requirements.

Construction companies in Dubai and across the UAE face heightened documentation requirements due to the sector’s project-based nature. Each construction project generates distinct financial flows—mobilization advances, progress certifications, retention withholdings, variation orders, and defects liability provisions. This complexity requires granular tracking to support both management reporting and regulatory compliance.

IFRS Application for Construction Companies in the UAE

International Financial Reporting Standards provide the accounting framework for construction companies operating in the UAE market. Construction companies must follow International Accounting Standards issued by the International Accounting Standards Board, with particular emphasis on standards directly affecting contract accounting and project financial reporting.

IFRS 15 Revenue Recognition Framework

The most critical standard for the construction sector is IFRS 15 (Revenue from Contracts with Customers). This standard fundamentally changed how construction revenue is recognized compared to the legacy percentage-of-completion method under IAS 11. Understanding IFRS 15 is essential for construction accounting compliance in the UAE.

IFRS 15 requires construction companies to follow a five-step model:

- Identify the contract with enforceable rights and obligations

- Identify distinct performance obligations within the contract

- Determine the transaction price, including variable consideration

- Allocate the transaction price to performance obligations

- Recognize revenue when (or as) performance obligations are satisfied

For construction contracts, revenue recognition typically occurs over time rather than at a point in time. This treatment applies because the asset created has no alternative use to the contractor, and the contract grants an enforceable right to payment for performance completed to date. Construction firms must demonstrate these criteria through contract analysis and legal review to justify overtime recognition.

Methods of Measuring Progress in Construction Projects

The measurement of progress requires selecting an appropriate method—either input methods (such as cost-to-cost percentage) or output methods (such as surveys of work performed or milestones achieved).

The cost-to-cost method remains the most common approach in UAE construction. This method calculates progress as costs incurred to date divided by total expected costs, then applies this percentage to the contract value to determine revenue earned. Construction accounting software must support this calculation with real-time cost tracking and forecasting capabilities.

Key considerations for progress measurement:

- Exclude costs that do not represent performance (uninstalled materials)

- Maintain reliable cost-to-complete estimates updated monthly

- Document assumptions and judgments for audit purposes

- Align progress calculations with engineering certifications where available

Variable Consideration and Contract Modifications

Variable consideration represents a significant judgment area for construction companies. Claims for additional compensation, incentive bonuses, penalties, and liquidated damages must be estimated and included in the transaction price only to the extent that a significant revenue reversal is not probable.

Common variable consideration elements in UAE construction:

- Approved and unapproved variation orders

- Performance incentives and bonuses

- Liquidated damages for delays

- Claims for cost overruns or scope changes

- Early completion bonuses

Many companies in the UAE construction sector face challenges in appropriately constraining variable consideration recognition. The IFRS framework requires conservative assessment, recognizing revenue only when entitlement is highly probable and supported by contractual rights or third-party certification.

Other Relevant IFRS Standards for Construction Companies

IFRS 9 (Financial Instruments) affects construction companies through retention receivables and advance payment guarantees. Retention amounts withheld by clients must be assessed for expected credit losses, particularly where release depends on defects liability period completion or client financial stability. Construction businesses must implement Expected Credit Loss (ECL) models for contract assets and retention receivables.

IFRS 16 (Leases) impacts construction firms that lease equipment, vehicles, site offices, or yard facilities. Companies must recognize right-of-use assets and lease liabilities for qualifying leases. This requirement affects both balance sheet presentation and profit measurement through depreciation and interest expense rather than operating lease charges.

| IFRS Standard | Construction Application | Key Judgment Areas |

| IFRS 15 | Revenue recognition from construction contracts | Performance obligations, overtime criteria, measure of progress, variable consideration |

| IFRS 9 | Financial instruments and credit risk | Expected credit loss on retention and contract assets |

| IFRS 16 | Lease accounting for plant and equipment | Lease classification, incremental borrowing rate |

| IAS 2 | Inventory of materials and site stores | Lower of cost and net realizable value |

| IAS 16 | Property, plant and equipment | Capitalization thresholds, depreciation methods |

| IAS 37 | Provisions for warranties and onerous contracts | Probability assessment, measurement of obligation |

Bookkeeping Framework and Financial Records Structure for Construction Projects

Construction accounting requires a dual-layer bookkeeping framework: entity-level accounting for statutory reporting and project-level accounting for operational control and contract performance measurement. This specialized accounting structure allows construction companies to track financial data at both consolidated and granular levels.

Chart of Accounts Design for Construction Companies

The general ledger structure for construction firms typically incorporates dimensional coding: Account–Project–Cost Code–Department. This segmentation enables construction companies to generate project-specific profit and loss statements while maintaining consolidated financial statements that comply with accounting standards in the UAE.

Balance sheet accounts adapted for construction:

- Cash and bank accounts (including escrow for mobilization advances)

- Trade receivables and retention receivable (tracked separately)

- Contract assets (unbilled revenue where performance exceeds billing)

- Inventory—warehouse materials and site-specific materials

- Prepayments and advances to suppliers

- VAT recoverable (input tax awaiting recovery)

- Property, plant, and equipment (owned construction machinery)

- Right-of-use assets (leased equipment under IFRS 16)

Liability accounts specific to construction:

- Trade payables and accrued subcontractor certificates

- Contract liabilities (billings in excess of performance)

- Mobilization advance liability (unearned customer advances)

- VAT payable (output tax collected)

- Provisions for warranties, defects, and onerous contracts

- Bank guarantees and performance bonds

Project-Level Cost Tracking Requirements

Profit and loss accounts require granular categorization for construction operations:

- Contract revenue (segmented by original value and approved variations)

- Direct labor costs (tracked by project and trade classification)

- Subcontractor costs (reconciled to certificates and payment applications)

- Materials consumed (distinguished from materials purchased)

- Plant and equipment charges (depreciation or hire rates)

- Site overheads and preliminaries (allocated to specific projects)

- Head office overhead apportionment (using consistent allocation keys)

Supporting documentation that construction accounting processes must capture includes:

- Signed contracts and approved amendments

- Approved variation orders and change requests

- Engineer certifications and progress certificates

- Subcontractor payment certificates

- Materials delivery notes and supplier invoices

- Timesheet records integrated with the Wage Protection System

- Plant hire agreements and utilization logs

- Bank guarantee registers and expiry tracking

Construction Accounting Software Requirements

Construction accounting software for the UAE market must support project-level transaction capture while automatically consolidating to entity-level financial statements. The accounting module should enable commitment accounting (tracking purchase orders and subcontract values against budget), cost-to-complete forecasting, and automated WIP schedule generation.

Essential software features for construction companies:

- Multi-project tracking with real-time cost allocation

- Integration with procurement and subcontractor management

- Automated progress billing and retention calculations

- VAT compliance tools, including reverse charge flagging

- WIP schedule automation with variance analysis

- Cash flow forecasting by project milestone

- Commitment tracking against approved budgets

Financial Statements Preparation Requirements for Construction Firms

Construction companies in the UAE must prepare complete financial statements comprising the balance sheet, profit and loss statement (income statement), cash flow statement, statement of changes in equity, and notes to the financial statements providing accounting policy disclosures and detailed breakdowns.

Balance Sheet Presentation for Construction Entities

The balance sheet for construction entities reflects contract-specific positions. Contract assets appear when revenue recognized exceeds amounts billed to clients (underbilling position). Contract liabilities arise when billing and cash received exceed revenue recognized (overbilling position, including mobilization advances not yet earned through performance).

This presentation differs from standard accounts receivable because enforceability and billing rights determine classification under IFRS 15. Construction companies must document their classification policy and apply it consistently across all projects.

Retention receivable may be presented separately or included within contract assets, depending on the specific contractual rights. Where retention is only conditional upon time passage (not performance), it may qualify as a receivable under IFRS 9 rather than IFRS 15.

Profit and Loss Statement Structure

The profit and loss statement must disaggregate revenue by contract type, geography, or client classification as required by IFRS 15 disclosure requirements. Construction revenue should be separated from other income sources, with costs presented to enable gross margin analysis at both project and entity levels.

Variable consideration (claims, incentives, penalties) requires separate disclosure when material. Construction services in the UAE frequently involve significant variable consideration elements that impact reported profitability and require detailed note disclosures.

Cash Flow Statement Considerations

The cash flow statement for construction companies often shows significant divergence between profit and cash flow due to working capital movements. Progress billing timing, retention withholding, and mobilization advance receipts create cash positions that differ substantially from revenue recognition timing.

Key cash flow drivers in construction:

- Timing difference between cost incurrence and supplier payment

- Retention withheld by clients (cash outflow deferred)

- Mobilization advances received (upfront cash inflow)

- Progress billing cycles and collection periods

- Bank guarantee cash collateral requirements

Notes to Financial Statements and Disclosures

Notes to financial statements must disclose:

- Significant accounting policies, including the revenue recognition method and progress measurement approach

- Disaggregation of revenue showing contract types and durations

- Contract assets and contract liabilities with reconciliation of opening to closing balances

- Performance obligations and timing of satisfaction

- Significant judgments in applying IFRS 15 (variable consideration constraints, cost-to-complete estimates)

- Related party transactions are common in construction (group company subcontracting, parent company guarantees)

VAT Compliance for Construction Companies in the UAE

The Federal Tax Authority (FTA) administers Value Added Tax in the UAE under Federal Decree-Law No. 8 of 2017. Construction companies face sector-specific compliance complexities around progress billing, retention treatment, reverse charge mechanisms, and real estate-related supplies.

VAT Registration and Filing Obligations

VAT registration thresholds require mandatory registration when taxable supplies and imports exceed AED 375,000 in the previous 12 months or are expected to exceed this amount in the coming 30 days. Voluntary registration is available for businesses with taxable supplies exceeding AED 187,500.

Construction companies typically exceed mandatory thresholds due to contract values, requiring registration and monthly or quarterly return filing. Companies must monitor threshold compliance at both the group and entity level, as project SPVs or separate trade licenses may each have distinct VAT registration status.

Tax periods are assigned by the Federal Tax Authority (monthly or quarterly). Construction firms should align VAT return preparation with monthly WIP close processes to ensure progress billings and tax invoices drive output VAT timing accurately.

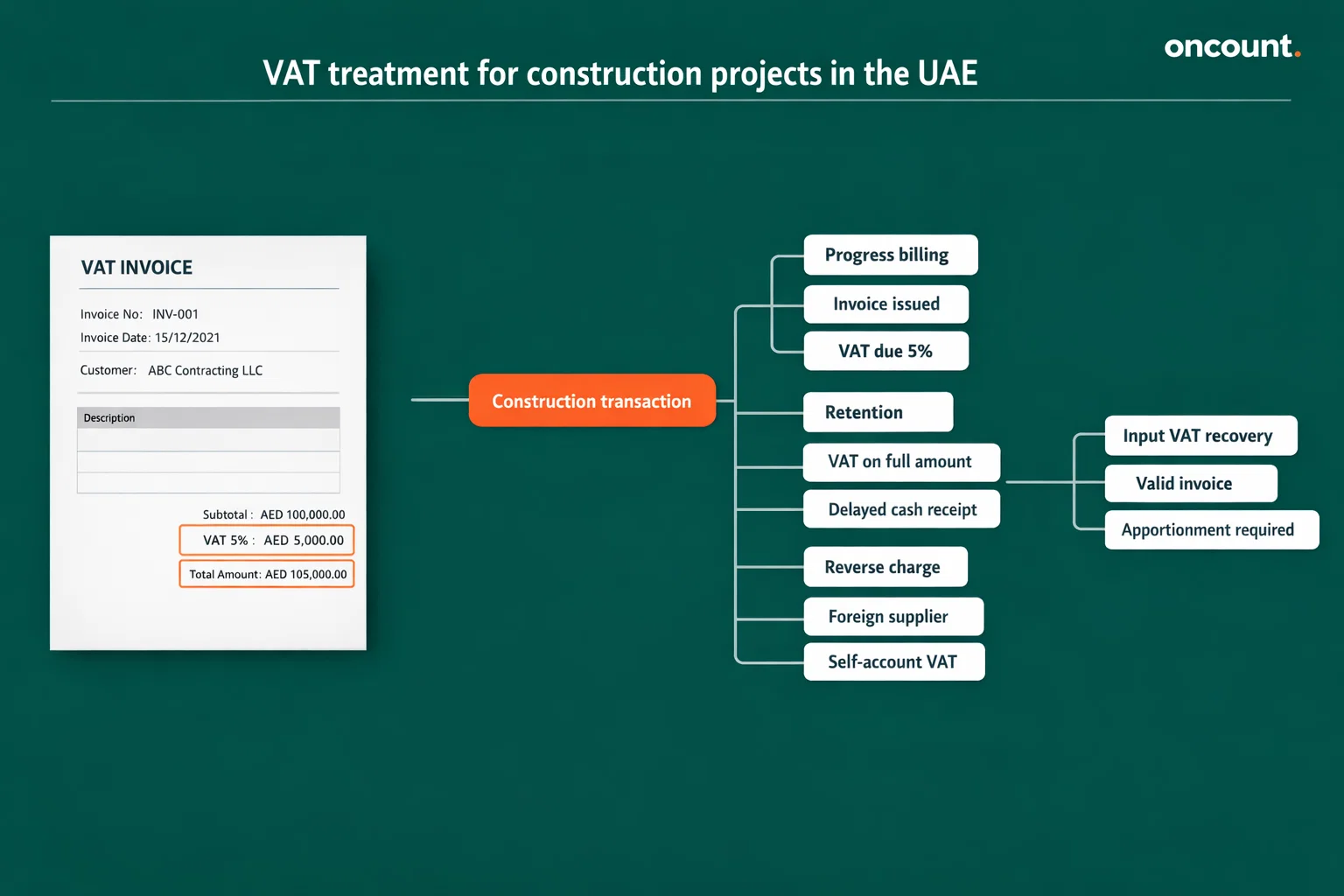

Tax Invoice Requirements for Progress Billing

Tax invoice requirements are critical for VAT compliance. The UAE VAT executive regulations specify mandatory particulars, including:

- Supplier Tax Registration Number (TRN)

- Customer details and TRN (where applicable)

- Tax invoice date and sequential number

- Description of goods or services supplied

- VAT amount shown separately in AED

- Reverse charge notation, where applicable

Construction firms must ensure that progress payment certificates convert into compliant tax invoices. Construction accounting differs from regular accounting in this area—progress billing requires careful coordination between quantity surveyors, commercial teams, and finance to ensure tax invoice timing aligns with VAT legislation.

Progress Billing and VAT Timing

Progress billing and VAT timing: VAT becomes due when the earlier of payment or tax invoice issuance occurs. For construction contracts, this typically aligns with progress certification and billing cycles.

Construction companies must account for output VAT on the full certified amount even where retention is withheld, unless contractual terms explicitly structure retention differently. This creates a cash flow timing difference that construction companies need to track carefully for liquidity management.

Retention treatment for VAT purposes:

- Output VAT is generally due on the gross certified amount (including retention)

- Alternative treatment may apply where retention is contractually treated as a separate supply

- Documentation must support the chosen treatment for FTA audit purposes

Reverse Charge Mechanism for Imported Services

The reverse charge mechanism applies when construction firms procure services from non-UAE-resident suppliers. Design consultancy, engineering services, or project management provided by foreign suppliers trigger recipient accounting obligations.

The UAE construction company must self-assess output VAT and claim corresponding input VAT (subject to recovery rules), with the tax invoice containing a statement that the recipient is responsible for accounting for VAT. This mechanism is common in EPC projects involving international engineering firms.

Zero-Rating and Exemption for Real Estate

Real estate rules are a recurring VAT risk area for contractors and developer-contractors. The Federal Tax Authority guidance explains that supplies of residential properties are generally exempt, while the first supply of residential properties (sale or lease) within three years of completion is zero-rated to allow developers to recover VAT on construction costs.

VAT treatment considerations:

- Contractor supplies to developers are typically standard-rated at 5%

- The developer’s onward supply classification affects input VAT recovery

- Mixed-use developments require apportionment methodologies

- Timing of “completion” affects zero-rating eligibility

Input VAT Recovery and Apportionment

Input VAT recovery is not automatic—it depends on holding valid tax invoices and using costs for recoverable activities. Where a business makes both taxable and exempt supplies, residual input VAT must be apportioned using approved methods.

The Federal Tax Authority’s input tax apportionment guide lists special methods (outputs-based, transaction count, floor space, sectoral) with eligibility tied to business type and FTA approval. Construction companies combining contracting (taxable) with property leasing or sales (potentially exempt) must implement robust apportionment frameworks.

Specified Recovery Percentage (SRP) provides an approval-based approach allowing companies to apply a prior-year recovery rate to subsequent tax periods, reducing the monthly calculation burden while maintaining compliance.

Corporate Tax Framework in the UAE

UAE Corporate Tax Law (Federal Decree-Law No. 47 of 2022) applies to juridical persons for financial years beginning on or after June 1, 2023. Construction companies in Dubai and the UAE must understand how corporate tax applies to their specific entity structure and operational model.

Corporate Tax Rates and Thresholds

Applicable tax rates under the UAE corporate tax law framework:

- 0% rate on taxable income up to AED 375,000

- 9% rate on taxable income exceeding AED 375,000

- Potential 0% rate for Qualifying Free Zone Persons on qualifying income

Construction companies must register for corporate tax through the EmaraTax platform administered by the Federal Tax Authority. Registration deadlines depend on the entity’s financial year-end and incorporation date, with penalties applying for late registration.

Taxable Income Calculation for Construction

Taxable income calculation begins with accounting profit (from audited financial statements prepared under IFRS standards) and adjusts for items treated differently under UAE corporate tax law.

Common adjustments for construction companies:

- Add back: non-deductible expenses (fines, penalties, certain provisions)

- Deduct: tax-exempt income, allowable capital allowances

- Adjust: timing differences in revenue recognition between accounting and tax

- Consider: transfer pricing implications for related party transactions

Construction accounting ensures that financial statements provide the starting point for tax computations, intensifying the need for audit-ready WIP support and reconciliations from operational systems to the general ledger.

Free Zone Qualifying Income Rules

Free zone persons can access preferential treatment through Qualifying Free Zone Person status, subject to meeting specific conditions. Cabinet Resolution No. 100 of 2023 and Ministerial Decision No. 229 of 2025 establish the framework for qualifying activities and de minimis thresholds.

De minimis test for free zone entities: non-qualifying revenue must not exceed the lower of 5% of total revenue or AED 5,000,000 within a tax period.

Construction-specific free zone considerations:

- Main contractor onshore works may create non-qualifying revenue

- Contract counterparty location affects income classification

- Free zone-to-free zone supplies may qualify

- Documentation requirements are extensive for audit defense

Construction companies operating in free zones must perform contract-by-contract tax classification before pricing and invoicing to maintain a qualifying status.

Transfer Pricing and Related Party Transactions

Construction groups with related party transactions must comply with transfer pricing rules. Subcontracting arrangements with group companies, management fee allocations, and head office cost recharges require arm’s length pricing supported by transfer pricing documentation.

The Federal Tax Authority expects construction firms to maintain:

- Transfer pricing policy documentation

- Functional analysis of related party transactions

- Comparable benchmarking for intercompany charges

- Master file and local file (where thresholds met)

Accounting for Revenue and Expenses in Construction Business

Revenue recognition and expense classification in construction accounting follow distinct patterns driven by contract structures, billing mechanisms, and project delivery models prevalent in the UAE construction sector.

Revenue Streams in UAE Construction

Primary revenue categories for construction firms:

- Fixed-price lump-sum contracts

- Cost-reimbursable contracts with fee structures

- Unit-price contracts (rate per measurable unit)

- Engineering, Procurement, and Construction (EPC) turnkey arrangements

- Design-build contracts combining services

Each contract type requires specific accounting treatment under IFRS 15, with revenue recognition timing and measurement dependent on performance obligation analysis and progress measurement methodology selection.

Cost Classification and Allocation

Direct costs traceable to specific projects:

- Labor costs (site workers, engineers, supervisors)

- Subcontractor costs (specialist trades, MEP contractors)

- Materials consumed (cement, steel, finishing materials)

- Equipment costs (owned equipment depreciation or rental charges)

- Site-specific overheads (temporary facilities, utilities, security)

Indirect costs requiring allocation:

- Head office salaries and administrative expenses

- Business development and tendering costs

- Quality assurance and safety department costs

- IT infrastructure and software licenses

- Professional fees (legal, tax, audit)

Construction companies must establish allocation methodologies that appropriately assign indirect costs to projects while maintaining IFRS compliance and tax deductibility.

Variation Orders and Claims Accounting

Variation order treatment depends on approval status:

- Approved variations: include in transaction price immediately, update progress measurement

- Unapproved variations: treat as variable consideration with constraint assessment

- Disputed claims: recognize only when highly probable and reversal risk is minimal

Construction project accounting requires rigorous change order management with finance sign-off gates preventing premature revenue recognition that could require reversal in subsequent periods.

Regulatory Compliance and Reporting Obligations

Construction companies are subject to multiple regulatory frameworks beyond financial reporting and tax compliance. Understanding the complete compliance landscape prevents penalties and supports operational licensing.

Economic Substance Regulations (ESR)

Economic Substance Regulations apply to UAE entities conducting relevant activities. While general contracting may not trigger ESR, construction companies involved in related activities (leasing, holding companies) must assess applicability.

ESR requirements when applicable:

- Demonstrate adequate physical presence in the UAE

- Maintain an appropriate number of qualified employees

- Incur adequate operating expenditures

- Conduct core income-generating activities in the UAE

- File an annual ESR notification and report

Anti-Money Laundering (AML) Compliance

Construction businesses in the UAE fall under AML supervision, particularly where handling significant cash transactions or operating in designated sectors.

AML obligations include:

- Customer due diligence and Know Your Customer (KYC) procedures

- Suspicious transaction reporting to the Financial Intelligence Unit

- Record keeping for customer identification and transactions

- Beneficial ownership verification and documentation

- Staff training on AML risks and red flags

Ultimate Beneficial Owner (UBO) Registration

Companies operating across the UAE must register Ultimate Beneficial Owner information with the relevant authority. Construction companies must identify and register individuals who ultimately own or control 25% or more of shares or voting rights.

UBO compliance steps:

- Identify natural persons meeting ownership thresholds

- Register UBO information through the relevant portal (Mainland, DIFC, ADGM)

- Update information within specified timeframes when changes occur

- Maintain supporting documentation evidencing the ownership structure

Audit Requirements for Construction Companies in the UAE

Audit requirements vary by jurisdiction and entity characteristics, but construction firms typically face mandatory audit due to licensing authority expectations, lender requirements, and corporate tax obligations.

Mainland UAE Audit Requirements

Construction companies licensed on the UAE mainland generally require annual statutory audits. The audit must be conducted by a registered audit firm with licensed auditors holding certificates from the UAE Ministry of Economy.

Audit deliverables typically include:

- Audited financial statements with an independent auditor’s report

- Management representation letter

- Audit completion memorandum

- Tax-related reports (where required for corporate tax filing)

DIFC and ADGM Audit Requirements

DIFC audit framework under DIFC Companies Law provides certain exemptions for small private companies meeting defined criteria. However, construction firms typically exceed size thresholds due to contract values and asset bases.

ADGM audit framework similarly requires statutory audit unless qualifying for exemption. The ADGM Registration Authority provides specific guidance on audit requirements and filing deadlines.

Both financial free zones require the filing of audited financial statements with the respective authority within specified timeframes following the financial year-end.

Auditor Expectations for Construction Companies

Construction auditors focus on high-risk areas, including:

- Revenue recognition policies and IFRS 15 compliance

- Work-in-progress valuation and cost-to-complete estimates

- Contract asset and liability classification

- Retention receivable recoverability and ECL assessment

- Provision adequacy (warranties, defects, onerous contracts)

- Related party transaction disclosures

- VAT compliance and input tax recovery support

Construction companies should maintain robust WIP schedules, project files, and contract documentation to facilitate efficient audit execution and minimize qualification risk.

Industry-Specific Accounting Considerations for Construction Companies

The construction sector presents unique accounting challenges requiring specialized knowledge beyond general IFRS and UAE tax frameworks.

Joint Venture and Consortium Accounting

Construction projects in the UAE frequently involve joint ventures or consortium arrangements where multiple contractors collaborate on large-scale developments. Accounting treatment depends on the legal structure and control assessment.

Joint operation treatment (common in construction):

- Each party recognizes its share of assets, liabilities, revenue, and expenses

- Proportionate consolidation of project-level transactions

- Separate VAT registration may be required for a joint venture

- Corporate tax implications depend on legal form

Joint venture entity treatment:

- A separate legal entity requires standalone accounting

- The parent recognizes the investment using the equity method

- Dividend distributions trigger tax implications

- Transfer pricing applies to transactions with a JV

Retention Accounting and Credit Risk

Retention mechanisms protect clients against defects and incomplete work. Typical retention structures withhold 5-10% of certified amounts, releasing portions at practical completion and final completion after defects liability periods.

Accounting considerations for retention:

- Classification as a contract asset vs receivable depends on conditionality

- Expected credit loss assessment under IFRS 9

- Aging analysis tracking retention release milestones

- Impairment indicators (client financial distress, project disputes)

Mobilization Advances and Customer Funding

Mobilization advances provide upfront funding for project setup and initial procurement. These advances create contract liabilities under IFRS 15, released through subsequent billing or progress certification.

Mobilization advance accounting:

- Initial receipt creates contract liability (not revenue)

- Release mechanism defined in contract terms

- Security instruments (bank guarantees) may be required

- VAT treatment requires specific attention (timing of supply)

Warranty and Defects Liability Provisions

Construction contracts typically include warranty periods and defect liability obligations. Companies must recognize provisions when present obligations exist, the amount can be reliably estimated, and outflow is probable.

Provision estimation considerations:

- Historical defects experienced by project type

- Contract-specific warranty terms and durations

- Complexity and technology risk factors

- Discount rate application for long-term provisions

Common Accounting Challenges for Construction Companies in the UAE

Construction firms frequently encounter specific accounting difficulties that require specialized expertise and robust controls to resolve.

Revenue Recognition Timing and Variable Consideration

Challenge: Determining when to recognize revenue from unapproved variation orders and claims.

Impact: Premature recognition leads to revenue reversal and restated financials. Conservative approaches delay legitimate revenue recognition and understate profitability.

Solution: Implement formal variation approval gates requiring finance sign-off before revenue inclusion. Establish evidence thresholds (engineer certification, client correspondence, contractual analysis) for variable consideration recognition.

Work-in-Progress Valuation Accuracy

Challenge: Maintaining accurate cost-to-complete estimates as projects progress and circumstances change.

Impact: Inaccurate WIP creates profit distortions, leads to misguided management decisions, and increases the risk of audit qualifications.

Solution: Monthly estimate-to-complete reviews involving project managers, quantity surveyors, and finance. Document assumption changes and variance explanations. Implement an independent review for loss-making projects.

VAT Compliance and Documentation

Challenge: Maintaining compliant tax invoices for progress billing while managing retention, reverse charge, and real estate special rules.

Impact: Invalid tax invoices prevent input VAT recovery. Incorrect output VAT timing creates FTA penalties and interest charges.

Solution: Implement tax invoice checklists integrated with billing workflows. Regular VAT health checks reviewing invoice compliance, reverse charge treatment, and recovery documentation.

Cash Flow Management and Working Capital

Challenge: Extended payment cycles, retention withholding, and mobilization advance repayment create liquidity pressure.

Impact: Profitable projects may still face cash constraints affecting supplier payment, subcontractor relationships, and bonding capacity.

Solution: Project-level cash flow forecasting updated monthly. Payment term negotiation with suppliers. Invoice discounting or supply chain finance arrangements, where appropriate.

Best Practices for Accounting and Financial Management in Construction

High-performing construction finance functions implement structured processes that ensure compliance while providing decision-useful management information.

Implementation of Construction-Specific Accounting Systems

Cloud-based construction accounting software enables real-time project tracking, multi-location access, and integration with procurement and project management systems. Leading platforms support:

- Project-level P&L and WIP automation

- Commitment tracking against approved budgets

- Progress billing with retention calculations

- VAT compliance tools and reverse charge flagging

- Corporate tax data pack generation

Monthly Financial Close Discipline

Structured month-end close process:

- Cost cutoff (Day 1-3): Ensure all supplier invoices, subcontractor certificates, and timesheets for the period are captured

- Estimate-to-complete (Day 3-5): Project managers and QSs update forecast costs and completion dates

- WIP calculation (Day 5-7): Finance applies the progress method, calculates revenue and profit to date

- Variance analysis (Day 7-8): Review margin movements, loss-making projects, and significant estimate changes

- Management reporting (Day 8-10): Finalize consolidated results with project-level detail

Internal Controls and Segregation of Duties

Key control points in construction financial management:

- Contract setup: Finance approval required before project activation

- Variation approval: Tiered authorization based on value thresholds

- Procurement: Three-way matching (purchase order, goods receipt, invoice)

- Progress certification: Independent engineer certification for billing

- Cash handling: Segregation between collection, posting, and reconciliation

Professional Advisory Engagement

Construction companies benefit from engaging specialized professional accounting services for:

- IFRS 15 implementation and revenue policy development

- VAT health checks and compliance reviews

- Corporate tax planning and free zone optimization

- Audit preparation and technical accounting support

- Financial system selection and implementation

Comparison: Free Zone vs Mainland Accounting Requirements for Construction

Construction companies must understand the distinct regulatory environments when choosing between a free zone and a mainland establishment.

| Dimension | Mainland UAE | Free Zone (DIFC/ADGM) | Free Zone (Other) |

| Accounting Standards | IFRS commonly applied | IFRS mandatory (DIFC/ADGM regulations) | IFRS is commonly required by authorities |

| Record Retention | Minimum 5 years | DIFC: 6 years; ADGM: 10 years | Varies by free zone authority |

| Audit Requirements | Typically mandatory for construction | Mandatory unless an exemption applies | Generally mandatory |

| Corporate Tax Rate | 0% up to AED 375k; 9% above | Potential 0% on qualifying income if QFZP status is met | Potential 0% on qualifying income if QFZP status is met |

| VAT Registration | Mandatory if threshold exceeded | Mandatory if threshold exceeded | Mandatory if threshold exceeded |

| De Minimis Test | Not applicable | Must not exceed 5% or AED 5M non-qualifying revenue | Must not exceed 5% or AED 5M non-qualifying revenue |

| Operating Restrictions | Can operate onshore throughout the UAE | May face restrictions on mainland activities | Varies by free zone; often limited scope |

| Transfer Pricing | Applies to related party transactions | Applies to related party transactions | Applies to related party transactions |

| ESR Applicability | Based on activity type | Based on activity type | Based on activity type |

Strategic considerations for construction companies:

- Mainland offers operational flexibility for projects across the Emirates

- Free zones may provide corporate tax benefits if the qualifying income criteria are met

- Mixed mainland-free zone structures require careful tax and compliance planning

- Contract-by-contract revenue classification is essential for free zone entities