Key Takeaways

- IFRS Compliance: UAE property management companies must prepare financial statements using International Financial Reporting Standards, particularly IFRS 15 for revenue recognition and IFRS 16 for lease accounting

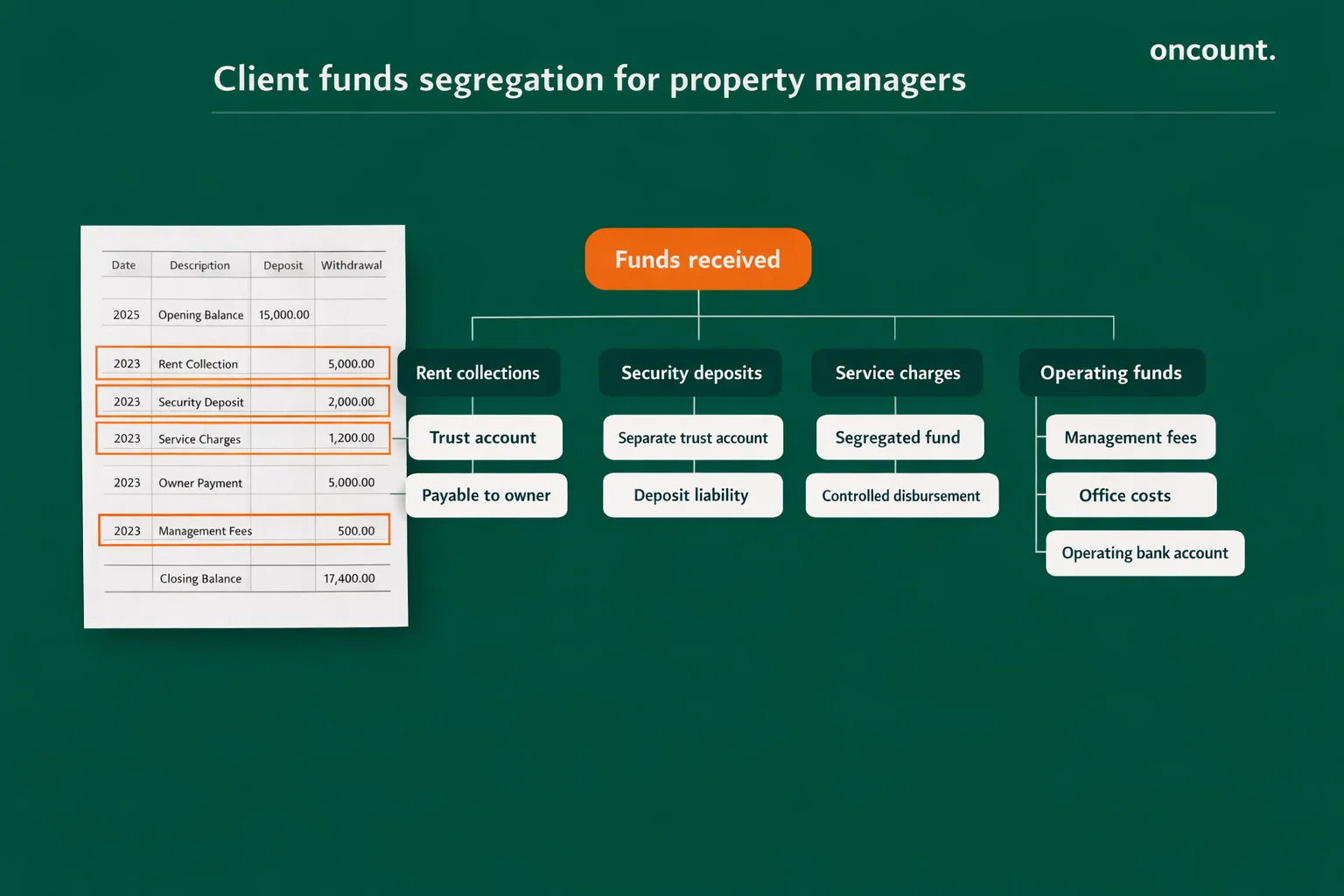

- Client Funds Segregation: Trust accounts for rent collections, security deposits, and service charges must remain separate from operating accounts, with full reconciliation

- VAT Registration: Mandatory registration applies when taxable management fees exceed AED 375,000 annually; residential rent is typically exempt, while commercial rent and service charges are standard-rated at 5%

- Corporate Tax: Federal Decree-Law No. 47 of 2022 imposes 9% tax on taxable income above AED 375,000, with 0% on qualifying free zone income

- Platform Compliance: Dubai Land Department’s Ejari and Abu Dhabi’s DARI systems require property management agreement registration as operational prerequisites

- AML Requirements: Property management firms conducting real estate brokerage fall under the Ministry of Economy’s DNFBP supervision with goAML reporting obligations

Overview of Accounting Requirements in the UAE for Property Management Companies

The UAE Commercial Companies Law and Federal Tax Authority regulations require property management companies to maintain complete accounting records aligned with internationally accepted standards. The UAE corporate tax framework explicitly states that tax computations start from accounting income based on financial statements prepared under accounting standards accepted in the UAE, making IFRS adoption a compliance necessity rather than an optional practice.

Property management entities licensed in Dubai, Abu Dhabi, or UAE free zones must maintain financial records for a minimum of five years covering all transactions, contracts, and supporting documentation. The UAE Federal Tax Authority enforces these retention requirements through audit programs targeting service industries with complex client fund arrangements.

Financial record systems must capture two distinct accounting layers: the company’s operating ledger tracking management fees, payroll, and overhead expenses, and a client funds sub-ledger reconciling to segregated bank accounts holding tenant deposits, rent collections, and service charge pools. This dual-layer architecture reduces misstatement risk and supports VAT and corporate tax audit trails required by FTA guidance.

IFRS Application for Property Management Companies

International Financial Reporting Standards govern financial statement preparation for UAE property management companies, with three standards carrying particular operational significance: IFRS 15 Revenue from Contracts with Customers, IFRS 16 Leases, and IAS 16 Property, Plant and Equipment.

IFRS 15 Revenue Recognition

IFRS 15 establishes a principles-based framework requiring property managers to distinguish between principal and agent relationships when recognizing revenue. Management fees earned for providing property administration services represent the company’s revenue and should be recognized as services are delivered over time, typically monthly, based on contract terms. Rent collected on behalf of property owners does not constitute revenue of the management company because the manager acts as agent rather than principal in these transactions.

The five-step model under IFRS 15 requires identifying performance obligations in management contracts, determining transaction prices including variable consideration components such as leasing commissions, and recognizing revenue when control of promised services transfers to customers. Property managers offering bundled services must allocate transaction prices to distinct performance obligations based on standalone selling prices.

IFRS 16 Lease Accounting

IFRS 16 requires property management companies to recognize right-of-use assets and lease liabilities for office premises, vehicle leases, and equipment rental arrangements exceeding twelve months. This standard transforms balance sheet presentation by bringing operating leases onto the statement of financial position and affects EBITDA calculations used in financial analysis.

The UAE corporate tax law bases taxable income computations on IFRS-compliant financial statements, meaning IFRS 16 lease expense timing directly impacts corporate tax positions. Property managers must implement lease accounting systems tracking contract commencement dates, payment schedules, and incremental borrowing rates for initial measurement.

Principal-Agent Considerations

Determining whether a property management company acts as principal or agent in specific transactions carries significant accounting implications. When managers simply facilitate rent collection and remit net proceeds to owners after deducting agreed fees, the agent classification applies, and only management fees appear as revenue. Conversely, if contract terms transfer control of rental income streams to the manager who then assumes payment obligations to owners, principal accounting may apply, requiring gross revenue recognition.

Bookkeeping Framework and Financial Records Structure

Effective bookkeeping systems for UAE property management companies require property-centric dimension structures rather than creating standalone charts of accounts per building. This approach limits account proliferation while improving owner reporting accuracy and financial controls.

Chart of Accounts Design

A properly structured chart of accounts separates trust account controls from operating accounts:

| Account Category | Operating Accounts | Trust Accounts |

| Bank Accounts | Operating Bank AED | Client Trust Bank – Rent Collections |

| Bank Accounts | Petty Cash | Client Trust Bank – Security Deposits |

| Receivables | Accounts Receivable – Management Fees | Client Trust Bank – Service Charges |

| Liabilities | Accounts Payable – Trade | Client Funds Payable – Owners (Control) |

| Liabilities | Output VAT Payable | Tenant Security Deposits Payable |

| Liabilities | Corporate Tax Payable | Service Charge Funds Payable |

Supporting Documentation Requirements

The FTA requires tax invoices, contracts, and payment evidence supporting VAT positions and corporate tax deductions. Property management documentation standards include:

- Signed property management agreements registered on Ejari or DARI platforms

- Tax invoices showing management fees with valid Tax Registration Numbers (TRN)

- Bank statements evidencing segregated trust account deposits and disbursements

- Tenant lease agreements with Ejari/DARI certificates

- Deposit receipt confirmations and move-out settlement statements

- Service charge approval documentation and owners’ association meeting minutes

- Contractor invoices with TRN validation for input VAT recovery

Financial Statements Preparation Requirements

UAE property management companies must prepare annual financial statements demonstrating a true and fair view of their financial position and performance. Required statements include Statement of Financial Position (balance sheet), Statement of Profit or Loss and Other Comprehensive Income, Statement of Changes in Equity, Statement of Cash Flows, and Notes to Financial Statements explaining accounting policies and significant judgments.

Balance Sheet Structure

The Statement of Financial Position must clearly separate operating assets and liabilities from client fund control accounts. Right-of-use assets under IFRS 16 appear in non-current assets alongside any property, plant, and equipment owned by the management company. Current assets include management fee receivables, prepaid expenses, and recoverable VAT balances.

Client trust bank accounts appear as assets with corresponding liability accounts representing amounts owed to property owners and tenants. This presentation ensures stakeholders understand that trust funds represent custodial holdings rather than company resources.

Profit and Loss Reporting

The Statement of Profit or Loss reflects only the property management company’s operating activities. Revenue consists of management fees, leasing commissions, administrative charges, and any maintenance coordination fees contractually earned by the manager. Rent collected as an agent does not appear in revenue.

Operating expenses include employee salaries subject to MOHRE wage requirements, office rent, IFRS 16 depreciation and interest, software costs for property management systems, and professional fees for audit and tax compliance, and non-recoverable VAT expense where mixed supply apportionment results in blocked input VAT.

VAT Compliance for Property Management Companies in the UAE

Federal Decree-Law No. 8 of 2017 establishes Value Added Tax obligations for UAE property management companies. The Federal Tax Authority VAT guidance provides detailed frameworks for real estate sector compliance, including specific rules for residential versus commercial property supplies.

VAT Registration Thresholds

Mandatory VAT registration applies when taxable supplies exceed AED 375,000 in the preceding twelve months. Voluntary registration becomes available above AED 187,500 under specified conditions. For property managers, taxable supplies typically include management fees charged to property owners, leasing commissions earned, and commercial property rent if the manager supplies commercial leasing services directly.

Place of Supply Rules

The UAE VAT Executive Regulations specify that services related to real estate are supplied where the property is located. This place-of-supply rule proves decisive for cross-border arrangements because property management fees relating to UAE properties remain subject to UAE VAT regardless of where the service provider is established. Foreign property management companies invoicing for Dubai or Abu Dhabi properties must therefore consider UAE VAT registration obligations.

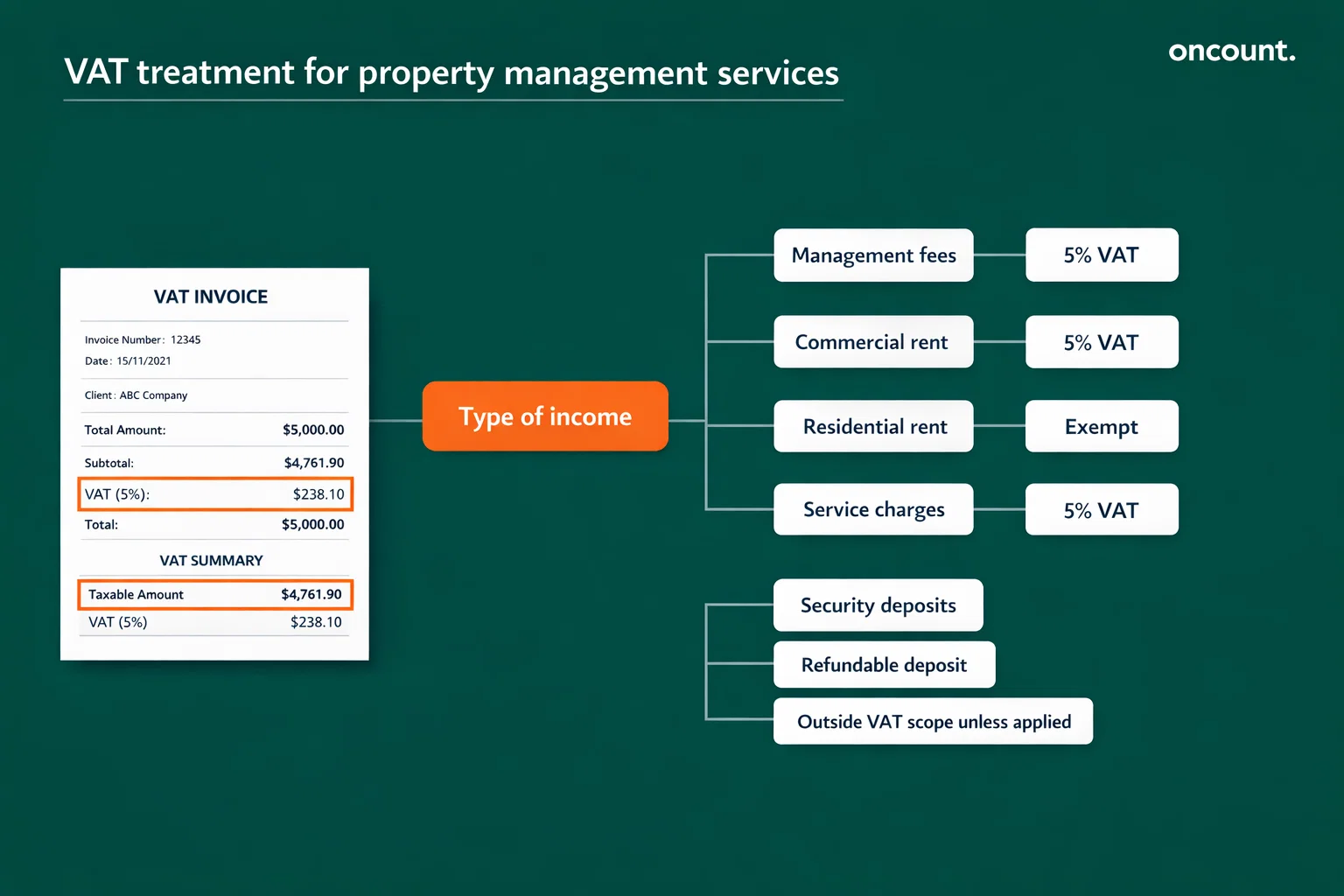

Residential vs Commercial VAT Treatment

| Supply Type | VAT Rate | Key Conditions |

| First supply of new residential building (within 3 years of completion) | 0% Zero-rated | Sale or lease qualifying as first supply |

| Subsequent supplies of residential buildings | Exempt | After initial supply period |

| Commercial property rent | 5% Standard-rated | Office, retail, industrial properties |

| Service charges (residential or commercial) | 5% Standard-rated | Charges for maintaining communal areas |

| Property management fees | 5% Standard-rated | Services supplied in UAE |

The FTA Real Estate VAT Guide clarifies that service charges relating to maintaining communal areas attract the standard VAT rate even when linked to residential buildings because service charges represent consideration for services rather than the supply of residential property itself. Owners’ associations and management entities administering service charges must register for VAT when taxable supplies exceed registration thresholds.

Input VAT Recovery and Apportionment

Property managers incurring VAT on overhead expenses supporting both taxable supplies (commercial management, taxable service charges) and exempt supplies (certain residential activities) face partial exemption rules. The FTA Input Tax Apportionment guide explains direct attribution methods for costs clearly related to specific supply types, residual input tax apportionment formulas, and annual adjustment requirements.

The FTA Real Estate VAT Guide highlights the floorspace method as a special apportionment approach relevant to businesses with mixed commercial and residential property portfolios. This method allocates residual input VAT based on the proportion of floor area dedicated to taxable versus exempt activities, subject to FTA approval when departing from standard apportionment calculations.

Security Deposit VAT Treatment

FTA Public Clarification VATP001 establishes that payments not constituting consideration for supplies fall outside VAT scope. Tenant security deposits held as refundable guarantees do not attract VAT upon receipt. However, when deposits are applied to unpaid rent or other contractual consideration, the applied amounts become consideration for relevant supplies requiring VAT treatment matching the underlying supply classification (standard-rated for commercial rent, exempt for qualifying residential rent).

When deposits are retained as compensation for property damage, VATP001 analysis determines whether retained amounts represent outside-scope damages or consideration for supplies. Documentation of the legal retention basis becomes critical audit evidence supporting VAT positions on deposit forfeitures.

Corporate Tax Framework in the UAE

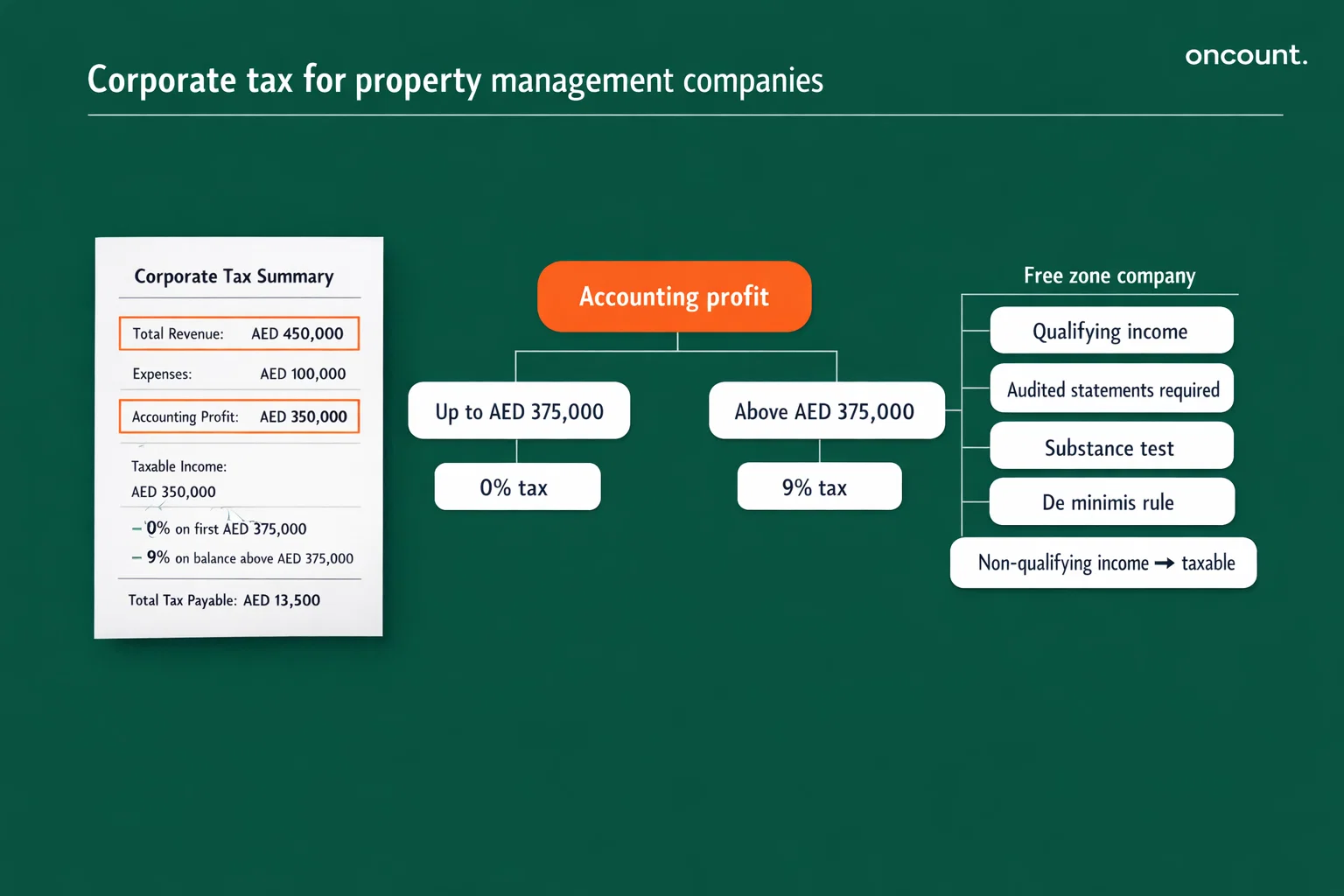

Federal Decree-Law No. 47 of 2022 introduces corporate tax on taxable income for UAE-resident legal persons, including property management companies incorporated in Dubai, Abu Dhabi, or free zones. The tax regime establishes a 0% rate on taxable income up to AED 375,000 and a 9% rate on taxable income – missing indefinite articles exceeding this threshold, with separate rules for Qualifying Free Zone Persons (QFZP).

Taxable Income Computation

UAE corporate tax law requires starting computations from accounting income reflected in financial statements prepared under accounting standards accepted in the UAE. This alignment with IFRS-based accounting means property managers must maintain compliant financial statements as a foundation for corporate tax compliance.

Taxable income equals accounting income adjusted for specific additions and deductions prescribed by corporate tax legislation. Tax-deductible expenses must satisfy business purpose requirements and be supported by valid documentation, including tax invoices meeting FTA standards. Non-deductible items include entertainment expenses exceeding prescribed limits, certain related-party payments not meeting arm’s length standards, and penalties imposed by UAE authorities.

Free Zone Corporate Tax Treatment

Property management companies established in Dubai or Abu Dhabi free zones may qualify for 0% corporate tax rate on qualifying income, defined as income derived from transactions with other free zone persons or foreign persons, excluding non-qualifying activities. The FTA Free Zone Persons guide sets explicit Qualifying Free Zone Person conditions:

- Maintenance of audited financial statements regardless of revenue levels

- De minimis compliance requiring non-qualifying revenue not to exceed the lower of AED 5,000,000 or 5% of total revenue

- Transfer pricing documentation demonstrating arm’s length pricing

- Adequate substance in the UAE, including sufficient qualified employees and operating expenditure

Failure to satisfy QFZP conditions results in standard corporate tax rates applying to all income, making ongoing compliance monitoring essential for free zone property managers claiming preferential tax treatment.

Small Business Relief

Ministerial Decision No. 73 of 2023 provides small business relief for entities with revenue not exceeding AED 3,000,000, applicable for tax periods ending on or before 31 December 2026. This relief mechanism offers simplified compliance for early-stage property management companies and small portfolio operators, though formal elections and documentation discipline remain necessary.

Accounting for Revenue and Expenses in Property Management

Property management revenue streams and expense classifications require careful accounting treatment, aligning with IFRS standards and supporting accurate VAT and corporate tax compliance.

Revenue Recognition Models

Management fees earned for recurring property administration services typically represent a series of distinct services satisfied over time under IFRS 15, supporting monthly revenue recognition based on time elapsed. Management agreements commonly specify fixed monthly fees calculated as a percentage of rental income or flat amounts per unit, sometimes including variable consideration components tied to occupancy rates or expense savings.

Leasing commissions earned when securing new tenants may constitute point-in-time revenue recognition if performance obligations are satisfied upon lease execution, or allocated over lease terms if contractual terms indicate ongoing obligations. Variable consideration constraints under IFRS 15 require estimating probable commission amounts when transaction prices include contingent elements.

Maintenance coordination fees require principal-agent analysis, determining whether the property manager acts as principal supplying maintenance services or as agent facilitating owner procurement of contractor services. When managers simply coordinate contractor engagement on behalf of owners, only coordination fees represent revenue. Conversely, contractual arrangements transferring control of maintenance obligations to managers may require principal accounting with gross revenue and cost recognition.

Expense Classification and Controls

Property management operating expenses fall into direct costs supporting property operations and general administrative overhead. Direct payroll costs for property coordinators, leasing agents, and facilities staff should be tracked against property portfolios, enabling owner cost allocations where contractual agreements permit expense recovery.

Contractor costs for maintenance, repairs, and utilities typically represent pass-through expenses charged to property owners rather than property manager expenses when the manager acts as an agent. Accounting systems must clearly separate reimbursable disbursements from company operating costs to prevent revenue misstatement and support accurate VAT treatment.

Software subscriptions for property management platforms, portal fees for Ejari and DARI registrations, and bank charges on trust accounts constitute ordinary business expenses deductible for corporate tax purposes when properly documented. Professional fees for statutory audits, VAT compliance, and corporate tax advisory similarly qualify as deductible expenses supporting business operations.

Regulatory Compliance and Reporting Obligations

UAE property management companies face regulatory requirements beyond taxation, including Economic Substance Regulations, Anti-Money Laundering frameworks, and Ultimate Beneficial Owner reporting obligations differing between mainland and financial free zones.

Economic Substance Regulations

UAE Cabinet Resolution No. 57 of 2020 establishes Economic Substance Regulations (ESR) requiring certain entities conducting relevant activities to demonstrate adequate substance in the UAE through sufficient employees, operating expenditure, and physical assets. While typical property management operations may not constitute relevant activities triggering full ESR compliance, entities should evaluate whether specific service arrangements or holding company structures create ESR exposure.

ESR notifications and reports must be filed within specified timeframes through the Ministry of Finance portals, with penalties applying to late submissions or substantive deficiencies. Property management groups with complex ownership structures or cross-border service delivery models should conduct annual ESR assessments confirming compliance positions.

Anti-Money Laundering Requirements

Federal Decree-Law No. 10 of 2025 updates the UAE AML frameworks with Cabinet Resolution No. 134 of 2025, providing executive regulations. Real estate agents and brokers fall within Designated Non-Financial Businesses and Professions (DNFBP), subject to Ministry of Economy supervision requiring customer due diligence, suspicious transaction reporting, and governance mechanisms, including compliance officer appointment.

Property management companies conducting leasing agency activities must implement risk-based AML programs addressing customer identification, beneficial ownership verification, ongoing monitoring, and record retention for a minimum of five years. The Ministry of Economy requires DNFBP registration on the goAML platform for suspicious transaction reporting, making AML compliance infrastructure necessary for property managers with brokerage exposure.

Ultimate Beneficial Owner Reporting

Cabinet Resolution No. 109 of 2023 regulates Real Beneficiary procedures for UAE legal persons, requiring the maintenance of registers identifying individuals owning or controlling 25% or more of shares or voting rights. The resolution explicitly excludes financial free zones from scope, creating distinct compliance paths for DIFC and ADGM entities versus mainland and non-financial free zone companies.

Mainland property management companies must maintain current Real Beneficiary registers and submit changes to licensing authorities within prescribed time limits. Cabinet Resolution No. 132 of 2023 establishes administrative penalties for violations, including delayed updates and inaccurate disclosures.

ADGM imposes separate beneficial ownership obligations requiring change reporting within fifteen days, while DIFC operates its own Ultimate Beneficial Ownership regime outside federal frameworks. Property management groups operating across jurisdictions must therefore implement jurisdiction-specific UBO compliance processes aligned with each regulatory framework.

Audit Requirements for Property Management Companies in the UAE

Audit requirements for UAE property management companies depend on jurisdiction, revenue levels, and free zone qualifying person status. The FTA Free Zone Persons guide mandates audited financial statements for all Qualifying Free Zone Persons regardless of revenue, making statutory audits a corporate tax compliance prerequisite rather than an optional assurance for free zone entities claiming preferential tax treatment.

Mainland Audit Thresholds

The Dubai Economic Department and the Abu Dhabi Department of Economic Development establish audit requirements for mainland companies based on legal form and revenue thresholds. Limited liability companies and joint stock companies typically require statutory audits, while certain sole proprietorships and civil companies may operate below audit thresholds absent specific licensing conditions mandating audited accounts.

Free Zone Audit Requirements

DIFC and ADGM maintain distinct audit frameworks aligned with international corporate governance standards. DIFC registered companies must file audited financial statements with the DIFC Registrar of Companies within prescribed timeframes, while ADGM Companies Regulations similarly mandate annual audited accounts for most registered entities.

Non-financial free zones, including Dubai Multi Commodities Centre (DMCC), Jebel Ali Free Zone (JAFZA), and Abu Dhabi Global Market, apply varying audit requirements depending on license type and company classification. Property management companies operating in these jurisdictions should confirm specific audit obligations through licensing authority guidance.

Audit Planning and Documentation

External auditors conducting statutory audits require comprehensive documentation including bank reconciliations, trust account movement schedules, VAT returns and apportionment workpapers, corporate tax computations, and platform compliance evidence linking Ejari or DARI registrations to rent rolls.

Property managers should implement audit readiness controls, including monthly trust reconciliations tying bank balances to owner payable and tenant deposit subsidiary ledgers, VAT invoice registers supporting output VAT positions and input VAT recovery claims, and Real Beneficiary register maintenance demonstrating UBO compliance where applicable.

Industry-Specific Accounting Considerations for Property Management

Client Funds Segregation and Trust Account Management

The highest operational risk for property management accounting involves proper segregation and reconciliation of client monies collected on behalf of property owners. UAE banking regulations and professional standards require property managers handling tenant deposits, rent collections, and service charge funds to maintain separate trust accounts distinct from operating accounts.

Accounting systems must support property-level and owner-level sub-ledgers reconciling to trust bank balances monthly. The trust reconciliation process confirms that client funds payable equals trust bank balances plus legitimate timing differences, such as outstanding checks. Discrepancies indicate potential misappropriation, accounting errors, or unauthorized use of client monies requiring immediate investigation.

Ejari and DARI Platform Compliance Integration

Dubai Land Department’s Ejari system and Abu Dhabi’s DARI platform function as operational prerequisites for compliant property management workflows because downstream processes, including utility connections, tenancy dispute resolution, and regulatory reporting, depend on registered contract data.

Accounting controls should validate that tenancy contracts appearing in rent rolls match Ejari or DARI-registered agreements, terminated contracts have been properly unregistered on platforms, and management agreement registrations remain current. Platform compliance failures create revenue collection risks when utility providers or owners challenge unregistered tenancy arrangements.

Service Charge Administration and Owners’ Association Accounting

Property managers administering service charges for owners’ associations or building maintenance entities must implement separate accounting treatments recognizing that service charge collections typically represent funds held on behalf of owner collectives rather than property manager revenue.

When the property management company itself operates as the registered owners’ association or maintenance entity, service charges collected become the entity’s revenue subject to the standard VAT rate and corporate tax rules. Conversely, when managers merely administer funds for separate owner associations, agency accounting applies with service charge balances reflected as trust liabilities.

Common Accounting Challenges for Property Management Companies

Insufficient Client Funds Segregation

Many property management startups fail to implement proper trust account separation from inception, instead commingling client rent collections with operating funds in single bank accounts. This creates serious regulatory exposure under AML frameworks, makes accurate owner reporting impossible, and prevents clean audit opinions when companies later require statutory audits for corporate tax or licensing compliance.

VAT Misclassification Across Mixed Portfolios

Property managers handling both residential and commercial properties frequently misapply VAT rules by treating all rent as exempt or all service charges as exempt when correct treatment requires property-by-property analysis. Residential rent typically qualifies as exempt after initial supply periods, while commercial rent attracts the standard VAT rate, and service charges generally carry standard VAT regardless of property classification.

Input VAT recovery errors compound when companies fail to implement proper apportionment methodologies for shared overhead costs supporting both taxable and exempt activities. The FTA expects documented apportionment calculations with annual adjustments, yet many property managers apply arbitrary allocation percentages without supporting analysis.

Inadequate Revenue Recognition Documentation

Failure to properly analyze principal-agent relationships in management contracts creates revenue recognition errors with downstream corporate tax implications. Companies recording gross rent as revenue instead of net management fees overstate income and may trigger premature mandatory VAT registration when only management fee revenues actually exceed thresholds.

Platform Compliance Gaps

Property managers failing to maintain current Ejari or DARI registrations face operational disruptions when owners or tenants encounter utility connection denials or dispute resolution barriers. Accounting systems disconnected from platform compliance create reconciliation failures when rent rolls include unregistered units or reflect terminated contracts not properly closed on platforms.

Best Practices for Accounting and Financial Management

Implement Cloud-Based Property Management Systems

Modern property management software platforms integrate tenancy management, rent collection tracking, owner reporting, and accounting ledgers in unified systems supporting platform compliance workflows. Cloud systems enable real-time bank feed imports, automated rent posting, and mobile access for property coordinators conducting tenant move-in inspections.

Integration between property management platforms and accounting software (such as QuickBooks, Xero, or NetSuite) reduces manual data entry errors and accelerates month-end close processes by automating trust reconciliations and owner statement generation.

Establish Monthly Reconciliation Controls

Property management accounting requires disciplined monthly reconciliation routines covering:

- Bank reconciliations for operating accounts and each trust account

- Client funds reconciliation, tying trust balances to owner payable and tenant deposit sub-ledgers

- VAT control account reconciliation linking output VAT to the sales ledger and input VAT to the purchase ledger

- Platform reconciliation confirming Ejari/DARI registered contracts match active rent roll entries

Controller sign-off on reconciliation packs before owner statement distribution prevents compounding errors and demonstrates governance to external auditors.

Segregate Duties for Client Money Handling

Effective internal controls separate contract setup, cash receipt processing, reconciliation responsibilities, and disbursement approvals. Leasing teams creating tenancy records should not process bank deposits, while staff matching receipts to ledgers should not approve refunds or owner payouts. Authorized signatories for trust account disbursements must remain separate from transaction preparers.

Engage Qualified Accounting Professionals

Property management companies benefit from periodic professional accounting reviews confirming IFRS compliance, VAT treatment accuracy, and corporate tax computation correctness. Outsourced accounting services specializing in UAE property management provide expertise in trust accounting, platform compliance integration, and FTA audit defense without requiring full-time finance team hiring for smaller portfolios.

Comparison: Free Zone vs Mainland Accounting Requirements

| Requirement Category | Mainland (Dubai/Abu Dhabi) | Financial Free Zones (DIFC/ADGM) | Non-Financial Free Zones |

| Accounting Standards | IFRS expected for corporate tax; the UAE Commercial Companies Law applies | IFRS mandatory; specific rulebooks and annual accounts regulations | IFRS expected; free zone authority-specific rules |

| Corporate Tax Rate | 0% up to AED 375,000; 9% above threshold | 0% on qualifying income for QFZP; 9% on non-qualifying income | 0% on qualifying income for QFZP; 9% on non-qualifying income |

| Audit Requirements | Based on legal form and revenue thresholds | Mandatory audited accounts for most entities | Varies by free zone; QFZP status requires audits |

| VAT Registration | Mandatory above AED 375,000 taxable supplies | The same federal VAT rules apply | The same federal VAT rules apply |

| Property Management Licensing | Ejari (Dubai) or DARI (Abu Dhabi) registration required | ADGM requires specific property manager licensing for ADGM properties; DIFC uses business category guides | Free zone authority approval may require mainland property licensing |

| Employment Framework | MOHRE Wage Protection System (WPS); UAE Labor Law gratuity | DIFC: DEWS-funded model; ADGM: separate employment regulations, WPS not applicable | Typically, MOHRE WPS applies; verify free zone specifics |

| Beneficial Ownership | Federal Real Beneficiary procedures (Cabinet Resolution 109/2023) apply | Excluded from the federal framework; separate DIFC/ADGM UBO regimes | Federal Real Beneficiary procedures apply |

| Record Retention | Minimum 5 years | Minimum 5 years; specific registrar requirements | Minimum 5 years |