Key Takeaways

- Property Classification: Real estate assets must be classified under IAS 2 (inventory for development properties), IAS 40 (investment property held for rental income), or IAS 16 (owner-occupied properties), with each classification determining measurement methodology and financial statement presentation.

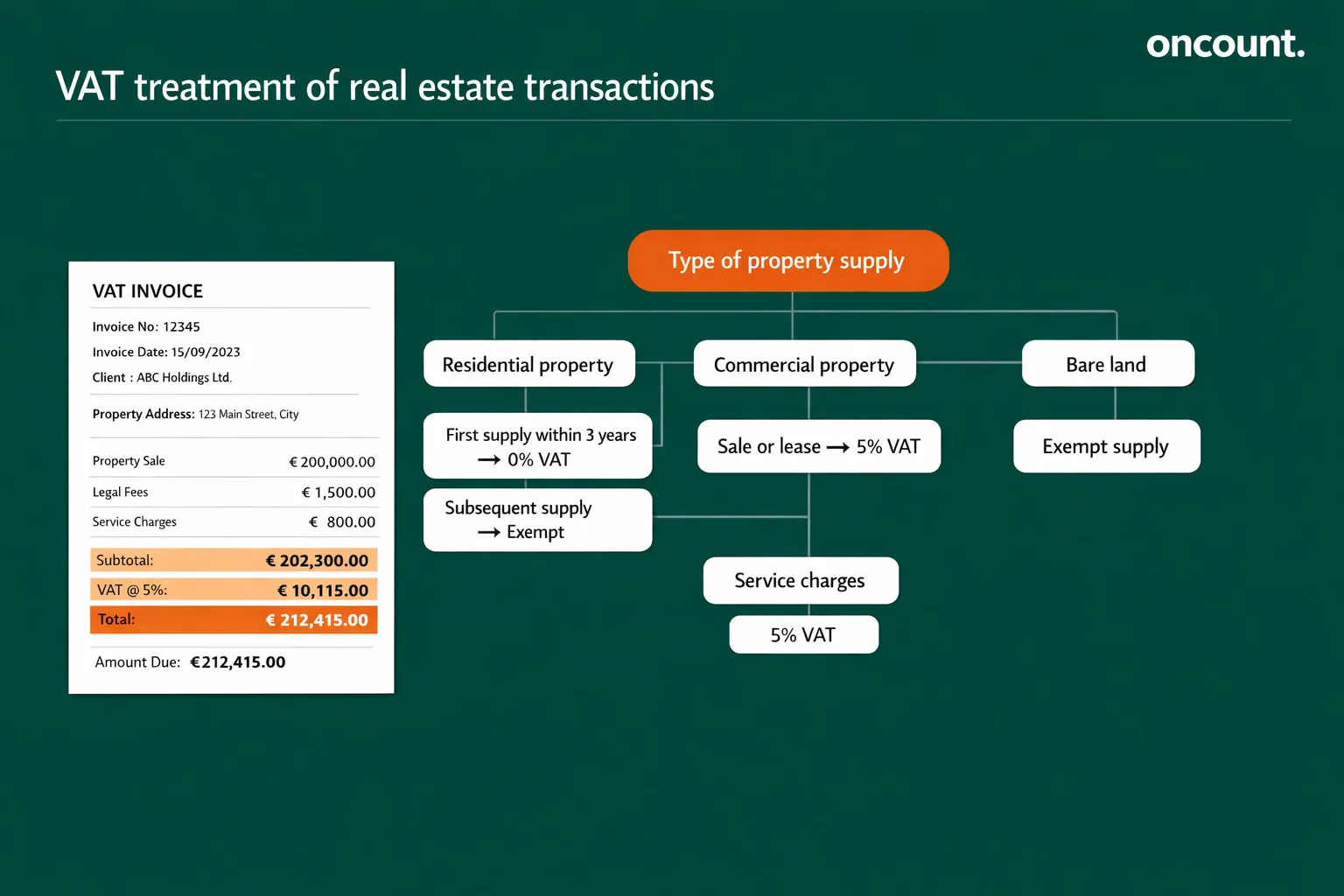

- VAT Treatment Variability: The first supply of residential buildings within three years of completion qualifies for zero-rated VAT treatment at 0%, while subsequent residential supplies are exempt, and commercial real estate transactions are standard-rated at 5%.

- Extended Record Retention: UAE VAT Executive Regulation requires real estate businesses to maintain transaction records for 15 years, significantly exceeding the standard five-year retention period applicable to other industries.

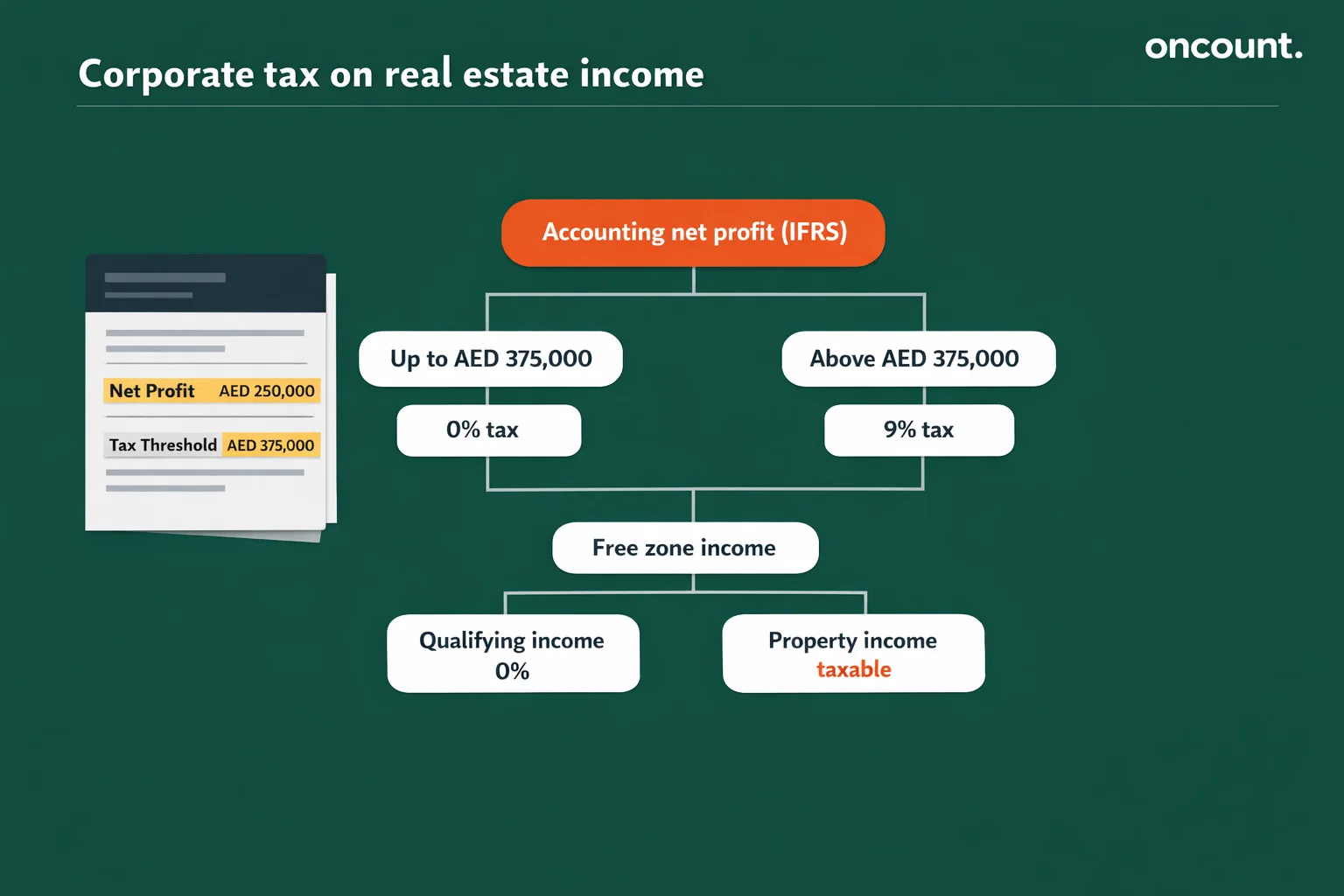

- Corporate Tax Thresholds: UAE Corporate Tax applies a 9% rate to taxable profits exceeding AED 375,000, with specific transitional relief provisions for pre-2023 ownership gains on qualifying immovable property.

- Free Zone Limitations: Cabinet Decision No. 100 of 2023 explicitly treats certain income from immovable property located in free zones as taxable income, limiting traditional free zone tax benefits for real estate operations.

Overview of Accounting Requirements in the UAE

The UAE Commercial Companies Law mandates that all companies maintain proper accounting records reflecting financial position and business operations. Real estate companies must establish accounting systems capable of tracking property acquisitions, development expenditures, customer contract terms, collection schedules, and property handovers across multiple reporting periods.

The Federal Tax Authority requires businesses to retain financial records for a minimum of five years from the end of the relevant tax period. However, real estate transactions trigger an extended 15-year retention obligation under Article 75 of the VAT Executive Regulation, necessitating robust document management infrastructure and electronic archival capabilities.

Real estate businesses must align financial reporting with IFRS standards adopted by the UAE. The Ministry of Finance recognizes IFRS as the foundation for corporate tax calculations, making accounting policy choices directly relevant to tax outcomes. For example, selecting the fair value model under IAS 40 for investment property creates profit and loss volatility from unrealized valuation changes, which may trigger taxable income unless specific elections are made.

| Regulatory Framework | Governing Authority | Primary Obligation | Retention Period |

| Commercial Companies Law | UAE Ministry of Economy | Maintain proper books and records | 5 years minimum |

| VAT Regulations | Federal Tax Authority | Document all taxable, exempt, and zero-rated supplies | 15 years for real estate |

| Corporate Tax Law | Ministry of Finance | Calculate taxable income from accounting profits | 7 years |

| IFRS Standards | IFRS Foundation | Prepare financial statements showing the true financial position | Ongoing compliance |

IFRS Application for Real Estate Companies

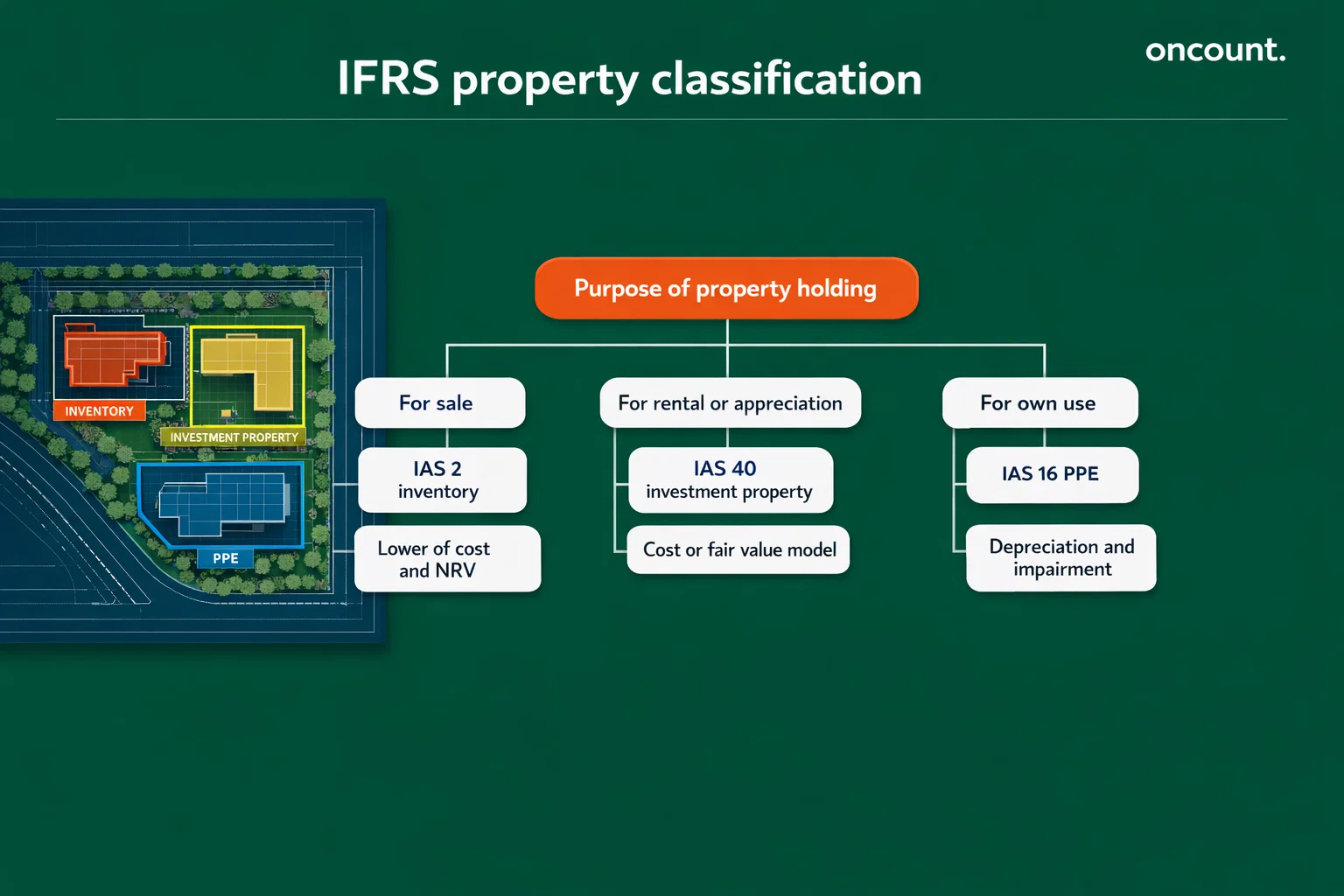

Real estate companies in Dubai apply several interconnected IFRS standards depending on business model and transaction types. The classification decision between inventory, investment property, and property, plant, and equipment represents the most consequential accounting determination affecting measurement, profit recognition timing, and financial statement presentation.

IAS 2 Inventories applies to real estate developers holding land and property under development for sale in the ordinary course of business. Dubai-based developers acquiring land for residential villa projects or apartment towers measure these assets at the lower of cost and net realizable value. Cost accumulation includes land acquisition expenditures, construction costs, borrowing costs for qualifying assets under IAS 23, and directly attributable development expenses. Net realizable value assessments require forecasting selling prices, estimated completion costs, and marketing expenses, with write-downs recognized immediately in profit or loss when carrying amounts exceed recoverable values.

IAS 40 Investment Property governs accounting for properties held to earn rental income or for capital appreciation rather than for sale. A Dubai landlord owning commercial office buildings in Business Bay or residential apartment blocks in Dubai Marina typically applies IAS 40. The standard permits choosing between the cost model (depreciation and impairment testing) and the fair value model (remeasurement through profit or loss). The fair value model eliminates depreciation but creates earnings volatility from market value fluctuations. According to the UAE Ministry of Finance Corporate Tax Accounting Standards Guide, businesses may elect to recognize gains and losses on a realization basis for qualifying capital assets to reduce tax volatility.

IFRS 15 Revenue from Contracts with Customers determines when real estate developers recognize revenue from unit sales, particularly for off-plan transactions where customer payments precede construction completion. The standard requires assessing whether revenue recognition occurs over time during construction or at a point in time upon handover. This assessment hinges on three criteria outlined in paragraph 35 of IFRS 15:

- The customer simultaneously receives and consumes benefits as the entity performs

- The entity’s performance creates or enhances an asset that the customer controls

- An entity creates an asset with no alternative use and has an enforceable right to payment for performance completed to date

For Dubai developers selling off-plan apartments, criterion 35(c) receives intensive scrutiny. The IFRS Interpretations Committee clarified that an enforceable right to payment must compensate for performance completed, not merely reimburse lost profit. This legal determination depends on UAE contract law and specific contractual terms governing customer termination rights and developer payment entitlements.

IFRS 16 Leases applies when real estate companies act as lessees (leasing office space or equipment) or lessors (leasing properties to tenants). Lessees recognize right-of-use assets and lease liabilities, while lessors classify leases as operating or finance leases. A Dubai property management company leasing commercial space to retail tenants applies lessor accounting, recognizing rental income on a straight-line basis unless another systematic method better represents the pattern of benefit consumption.

Bookkeeping Framework and Financial Records Structure

Real estate companies in Dubai require comprehensive bookkeeping systems capturing property-level financial data, customer contract terms, payment schedules, and VAT treatment classifications. The chart of accounts must distinguish between property categories to support accurate IFRS classification and VAT reporting segmentation.

A typical real estate chart of accounts structure includes:

Asset Accounts:

- Land held for development (IAS 2)

- Work in progress by project (IAS 2)

- Completed inventory units (IAS 2)

- Investment property at fair value or cost (IAS 40)

- Right-of-use assets for leased premises (IFRS 16)

- Contract assets for overtime revenue recognition (IFRS 15)

Liability Accounts:

- Contract liabilities for customer advances (IFRS 15)

- Trade payables to contractors and suppliers

- Lease liabilities (IFRS 16)

- Output VAT by category (standard-rated, zero-rated, exempt)

- Corporate tax provisions

Revenue Accounts:

- Unit sales revenue (IFRS 15)

- Rental income from commercial properties (IAS 40, IFRS 16)

- Property management fee income (IFRS 15)

- Service charge income (IFRS 15)

Supporting documentation requirements include sales contracts with customer payment schedules, construction cost invoices, bank statements evidencing fund movements, property completion certificates, and tax invoices showing VAT treatment. The Federal Tax Authority emphasizes that VAT documentation must clearly demonstrate the basis for zero-rated, exempt, or standard-rated treatment, particularly for mixed-use developments containing both residential and commercial components.

Financial Statements Preparation Requirements

Real estate companies in Dubai prepare financial statements following IFRS presentation requirements outlined in IAS 1 Presentation of Financial Statements. The complete financial statement package comprises the statement of financial position (balance sheet), statement of comprehensive income (profit and loss), statement of changes in equity, statement of cash flows, and explanatory notes.

Statement of Financial Position must separately present current and non-current classifications. Development inventory appears as current assets when expected to be sold within the operating cycle, while investment property and owner-occupied property are classified as non-current assets. Contract assets and contract liabilities arising from IFRS 15 require separate disclosure when material.

Statement of Comprehensive Income presents revenue recognized from property sales, rental income, and property management services. For developers applying over-time revenue recognition, significant judgment disclosures explain progress measurement methods, typically using cost-to-cost input methods or output methods based on units delivered. Fair value adjustments on investment property measured under the IAS 40 fair value model appear as separate line items affecting reported profit.

Notes to Financial Statements provide critical context for real estate operations. Required disclosures include:

- Accounting policies for property classification and measurement model selections

- Revenue recognition policies and significant contract judgment areas

- Fair value hierarchy disclosures for investment property (IFRS 13)

- Lease maturity analysis and lease income reconciliation (IFRS 16)

- Expected credit loss methodology for receivables and contract assets (IFRS 9)

According to Ministerial Decision No. 84 of 2025, taxable persons exceeding AED 50,000,000 revenue in a tax period and qualifying free zone persons must obtain audited financial statements. This requirement reinforces the importance of maintaining audit-ready documentation throughout the financial year.

VAT Compliance for Real Estate Companies in the UAE

VAT treatment for real estate transactions in Dubai depends on property type, supply timing, and permitted use classification. The Federal Tax Authority administers VAT under Federal Decree-Law No. 8 of 2017, with sector-specific guidance provided through the Real Estate VAT Guide (VATGRE1).

VAT Registration Thresholds

Real estate businesses must register for VAT when taxable supplies and imports exceed AED 375,000 during the previous 12 months or are expected to exceed this threshold in the next 30 days. Voluntary registration becomes available when taxable supplies and imports exceed AED 187,500. Registration occurs through the EmaraTax portal administered by the Federal Tax Authority.

Property-Specific VAT Treatment

| Property Type | First Supply Within 3 Years | Subsequent Supplies | Leasing Treatment | Input VAT Recovery |

| Residential Building | Zero-rated (0%) | Exempt | Generally exempt | Blocked for exempt supplies |

| Commercial Property | Standard-rated (5%) | Standard-rated (5%) | Standard-rated (5%) | Recoverable for taxable outputs |

| Bare Land | Exempt | Exempt | Exempt | Blocked |

| Mixed-Use Property | Apportioned by floor area | Apportioned by floor area | Apportioned | Proportional recovery |

Residential Buildings: The first supply of a completed residential building within three years of completion qualifies for zero-rated VAT treatment. VATGRE1 defines completion as the earliest of receiving a completion certificate, occupancy occurring, or substantial completion evidenced by factors including utility connections and municipality approvals. Off-plan residential purchases before or during construction also qualify for zero-rating.

Commercial Real Estate: Sales and leases of commercial properties apply the standard 5% VAT rate. A specialized payment mechanism applies to certain commercial property sales where buyers pay VAT directly to the Federal Tax Authority before completing ownership transfer through land departments. This process requires coordination between seller, buyer, and registration authorities, with specific exclusions for developer sales and other carve-outs detailed in the Commercial Property Buyers User Guide.

Service Charges: Property management companies collecting service charges for maintaining communal areas in residential developments must apply standard 5% VAT. VATGRE1 clarifies that these charges represent payment for services rather than consideration for supplying residential buildings, removing them from exempt treatment.

Time of Supply Rules

VAT becomes due at the earliest of invoice issuance, payment receipt, or supply completion. Real estate developers receiving staged payments for off-plan units must account for VAT on each installment as received, creating cash flow implications when projects span multiple years. The continuous supply rules may apply to long-term lease arrangements, requiring careful time of supply tracking.

Input VAT Recovery Challenges

Real estate businesses operating mixed portfolios combining taxable commercial properties and exempt residential properties face input VAT recovery complexity. The Federal Tax Authority permits using floor area apportionment methods for allocating shared costs, but this requires formal approval when applying special methods deviating from standard revenue-based apportionment.

Corporate Tax Framework For Real Estate Companies in the UAE

The UAE implemented corporate tax through Federal Decree-Law No. 47 of 2022, applying to tax periods commencing on or after June 1, 2023. Real estate companies calculate taxable income starting from accounting profit under IFRS, then applying statutory adjustments defined in Ministerial Decision No. 134 of 2023.

Tax Rates and Thresholds

UAE Corporate Tax applies a two-tier rate structure:

- 0% rate on taxable income up to AED 375,000

- 9% rate on taxable income exceeding AED 375,000

Large multinational enterprises meeting specific criteria face a separate 15% rate aligned with Pillar Two global minimum tax requirements, though this rarely applies to domestic real estate operations.

Taxable Income Calculation

Taxable income begins with accounting net profit prepared under IFRS, adjusted for items treated differently under tax law. Key adjustments for real estate companies include:

Non-Deductible Expenses: Corporate tax law restricts deductions for entertainment expenses exceeding limits, certain related-party payments, and penalties imposed by government authorities. Real estate developers paying late completion penalties to customers may challenge deductibility depending on characterization as compensatory versus punitive payments.

Capital vs Revenue Classification: Tax treatment distinguishes between capital account assets (property held for long-term appreciation or operational use) and revenue account assets (inventory held for sale). This classification impacts depreciation deductibility, gain taxation, and transitional relief eligibility.

Realization Basis Elections: The Ministry of Finance permits businesses to elect to recognize gains and losses on capital account assets on a realization basis rather than following accounting fair value adjustments. This election proves valuable for investment property portfolios measured at fair value under IAS 40, eliminating taxable income volatility from annual revaluations. Elections must be consistently applied and properly documented.

Transitional Rules for Pre-Corporate Tax Ownership Gains

Ministerial Decision No. 120 of 2023 establishes transitional adjustments excluding gains attributable to the pre-corporate tax ownership period for qualifying immovable property. The Federal Tax Authority issued Public Clarification CTP009, specifically addressing real estate developers recognizing IFRS 15 revenue over time during construction periods.

Under the valuation method, excluded transitional gains equal the difference between the market value at the start of the first tax period and the higher of original cost or net book value. For off-plan projects where developers recognize revenue during construction, CTP009 treats revenue recognition events as deemed disposals requiring transitional valuation at the first tax period commencement date.

A Dubai developer commencing its first tax period on January 1, 2024 with off-plan units sold in 2022 and revenue recognized progressively through 2023 must perform a transitional valuation as of January 1, 2024. This valuation determines the excluded pre-tax gain component, requiring detailed unit-level apportionment and supporting market value evidence.

Free Zone Corporate Tax Considerations

Cabinet Decision No. 100 of 2023 defines qualifying income requirements for free zone persons seeking 0% tax treatment. Article 6 explicitly states that income from immovable property located in free zones constitutes taxable income subject to corporate tax, significantly limiting free zone benefits for real estate operations.

Ministerial Decision No. 229 of 2025 classifies “ownership or exploitation of immovable property” as an excluded activity, with a narrow exception for commercial property located in a free zone where transactions occur with other free zone persons. The de minimis threshold permits non-qualifying income up to 5% of total revenue or AED 5,000,000 (whichever is lower) without losing qualifying free zone person status.

A free zone real estate holding company leasing residential apartments generates non-qualifying income that jeopardizes 0% tax treatment. Converting the portfolio to commercial properties and restricting tenancy to free zone entities may satisfy the exception criteria, subject to demonstrating genuine commercial substance and business rationale beyond tax avoidance.

Accounting for Revenue and Expenses in Real Estate

Revenue recognition represents the most technically complex accounting area for real estate companies, particularly for developers selling units before construction completion. IFRS 15 requires identifying performance obligations within customer contracts and determining whether control transfers over time or at a point in time.

Off-Plan Sales Revenue Recognition

Dubai developers typically enter contracts with buyers before construction begins, receiving deposits and staged payments throughout the development period. IFRS 15 paragraph 35(c) permits over-time revenue recognition when the entity’s performance creates an asset with no alternative use to the entity and the entity has an enforceable right to payment for performance completed to date.

No Alternative Use: Contractual or practical limitations must prevent the developer from redirecting the property to another customer. Master plan approvals, plot-specific design approvals, and customer-specific customizations may create this restriction.

Enforceable Right to Payment: UAE contract law and specific contractual terms determine whether the developer can require payment for work performed even if the customer terminates the contract. The IFRS Interpretations Committee emphasized that the right to payment must compensate for performance completed, not merely reimburse lost profit or margin.

A developer lacking clear contractual right-to-payment provisions typically recognizes revenue at handover when control transfers to the buyer. This point-in-time recognition defers all revenue and margin until project completion, potentially creating lumpy earnings patterns but reducing judgment risk.

Rental Income Recognition

Property owners leasing commercial space or residential units recognize rental income on a straight-line basis over the lease term under IFRS 16 lessor accounting, unless another systematic method better reflects the timing of benefit consumption. Rent-free periods and stepped rent increases require adjustment to maintain straight-line recognition.

Service charge income from property management activities constitutes revenue from contracts with customers under IFRS 15, typically recognized over time as services are performed on a time-elapsed basis when service delivery occurs evenly throughout the contract period.

Cost Recognition and Capitalization

Development costs including land acquisition, construction expenditures, professional fees, and eligible borrowing costs capitalize to inventory under IAS 2. Borrowing costs for qualifying assets requiring substantial preparation time before intended use or sale must be capitalized under IAS 23.

Administrative overheads, selling expenses, and abnormal waste do not qualify for capitalization. Real estate companies must establish robust cost allocation methodologies distinguishing capitalizable project costs from period expenses, with documentation supporting allocation bases and management judgment.

Regulatory Compliance and Reporting Obligations

Real estate companies operating in Dubai navigate multiple regulatory compliance frameworks beyond VAT and corporate tax, each creating accounting implications and documentation requirements.

Ultimate Beneficial Owner (UBO) Reporting

Cabinet Resolution No. 58 of 2020 requires maintaining registers of beneficial owners and nominees. Real estate companies must identify individuals ultimately owning or controlling 25% or more of shares or voting rights. Compliance with UBO regulations impacts corporate governance documentation and periodic filing requirements with the Registrar of Companies.

Anti-Money Laundering (AML) Requirements

Real estate transactions fall within the scope of UAE AML regulations, requiring businesses to implement customer due diligence procedures, transaction monitoring, and suspicious activity reporting. The Financial Intelligence Unit oversees AML compliance, with real estate developers and brokers classified as Designated Non-Financial Businesses and Professions (DNFBPs) subject to heightened scrutiny.

Economic Substance Regulations Updates

The Ministry of Finance announced in December 2022 that Economic Substance Regulations (ESR) requirements no longer apply to financial years ending after December 31, 2022, following UAE’s removal from the EU list of non-cooperative jurisdictions. However, businesses conducting relevant activities in earlier periods must ensure historical ESR notification and reporting compliance remains documented.

Audit Requirements for Companies in the UAE

Audit requirements vary based on company’s legal form, jurisdiction, and financial thresholds. Ministerial Decision No. 84 of 2025 mandates audited financial statements for taxable persons (excluding tax groups) with revenue exceeding AED 50,000,000 in the relevant tax period and for all qualifying free zone persons regardless of revenue.

Mainland vs Free Zone Audit Obligations

Mainland companies established under the UAE Commercial Companies Law typically face audit requirements when exceeding revenue or asset thresholds specified in license conditions. Public joint stock companies and limited liability companies with significant turnover must appoint external auditors registered with appropriate professional bodies.

Free zone entities face jurisdiction-specific requirements. Dubai International Financial Centre (DIFC) and Abu Dhabi Global Market (ADGM) impose mandatory audit requirements on most licensed entities, with specific exemptions for certain holding companies and small entities meeting defined criteria. Non-financial free zones may require audits based on license category and revenue thresholds.

External auditors conducting UAE real estate company audits must hold membership with recognized professional accounting bodies such as the Association of Chartered Certified Accountants (ACCA), the Institute of Chartered Accountants in England and Wales (ICAEW), or equivalent organizations accepted by regulatory authorities.

Industry-Specific Accounting Considerations for Real Estate

Property Development Inventory Management

Real estate developers must maintain detailed project accounting capturing land acquisition costs, construction expenditures, professional fees, marketing costs, and finance expenses by development phase and individual unit. This granular tracking enables accurate:

- Net realizable value testing under IAS 2

- Progress measurement for over-time revenue recognition

- Contract asset and liability calculation

- Gross profit margin analysis by project and unit type

Project cost accumulation systems should integrate with procurement workflows, contractor payment approvals, and change order management to maintain real-time cost-to-complete forecasts.

Investment Property Fair Valuation

Real estate companies selecting the IAS 40 fair value model must obtain reliable fair value measurements at each reporting period. IFRS 13 Fair Value Measurement requires using valuation techniques appropriate for the circumstances and maximizing observable market inputs.

The income capitalization approach applies to income-producing properties, discounting expected future rental cash flows at market-determined rates. The comparable sales approach uses recent transaction prices for similar properties adjusted for differences in location, size, condition, and lease terms.

Independent professional valuations from qualified surveyors support fair value conclusions, particularly for significant property portfolios or when internal expertise limitations exist. Valuation reports should clearly document assumptions, comparables selected, and sensitivity analysis for key inputs including capitalization rates and rental growth projections.

Mixed-Use Development Accounting

Developments combining residential units, commercial spaces, and retail areas require careful revenue stream segmentation and VAT treatment attribution. Each component may trigger different:

- IFRS revenue recognition patterns

- VAT rates and time of supply rules

- Input VAT recovery percentages

- Corporate tax classification

Floor area apportionment methods typically allocate shared development costs and input VAT across components, requiring formal documentation and Federal Tax Authority approval when applying special methods.

Common Accounting Challenges for Real Estate Companies

Revenue Recognition Timing Disputes

The most frequent challenge involves determining whether off-plan unit sales qualify for over-time revenue recognition under IFRS 15 paragraph 35(c). Weak contractual terms, ambiguous payment-on-termination clauses, and unfavorable legal opinions regarding enforceability force point-in-time recognition, deferring revenue and profit until handover.

Inconsistent application across similar contracts creates audit findings and potential restatement risk. Real estate companies should establish contract review committees evaluating IFRS 15 criteria before execution, with legal counsel providing enforceability opinions addressing specific contract language and UAE law provisions.

VAT Treatment Misclassification

Incorrectly classifying residential buildings as commercial properties or misapplying exempt versus zero-rated treatment creates VAT exposure through incorrect input VAT recovery. Public Clarification VATP018 confirms that VAT treatment depends on permitted use at the date of supply, with subsequent permitted use changes not retroactively affecting prior VAT treatment.

Conservative practice requires documenting permitted use determinations through municipality approvals, completion certificates, and internal property classification records retained for the mandatory 15-year period.

Transitional Relief Documentation Gaps

Real estate companies failing to compile comprehensive transitional valuation evidence at first tax period commencement risk losing substantial tax relief on pre-corporate tax ownership gains. CTP009 emphasizes that revenue recognition under IFRS 15 constitutes deemed disposal requiring valuation at that point.

Best practice involves engaging independent valuers at the first tax period start date, preparing detailed unit-level apportionment schedules linking market values to specific inventory or contract assets, and maintaining cost tracking from original acquisition through construction phases.

Best Practices for Accounting and Financial Management

Implement Integrated Property Management Systems

Real estate companies benefit from cloud-based enterprise resource planning (ERP) systems offering property-specific modules for tracking:

- Unit-level inventory and contract status

- Customer payment schedules and collections

- Construction cost budgets and actuals

- VAT treatment by transaction type

- Lease agreements and rental income schedules

Integration between property management, accounting, and customer relationship management systems eliminates manual data transfers and reduces transaction recording errors.

Establish Quarterly Technical Accounting Reviews

Regular reviews conducted by qualified accountants assess:

- Revenue recognition methodology application consistency

- Net realizable value testing for development inventory

- Fair value movements for investment property

- Expected credit loss adequacy for receivables and contract assets

- VAT classification accuracy and input recovery calculations

These reviews identify emerging issues before year-end close, allowing corrective action and reducing audit adjustment risk.

Maintain Comprehensive Documentation Libraries

Real estate businesses should establish electronic document repositories organizing:

- Customer contracts with IFRS 15 analysis memoranda

- Property completion certificates and permitted use approvals

- Valuation reports for investment property and transitional relief

- VAT classification decisions with supporting FTA guidance references

- Corporate tax election documentation and realization basis tracking

Version control, access logging, and systematic archival ensure compliance with 15-year VAT retention and 7-year corporate tax retention requirements.

Engage Specialized Real Estate Accountants

The technical complexity of real estate accounting, particularly IFRS 15 revenue recognition and IAS 40 investment property, warrants engaging accountants with demonstrated UAE real estate sector experience. Professional certifications from ACCA, ICAEW, CPA, or equivalent bodies combined with practical UAE regulatory knowledge provide essential expertise for navigating developer-specific challenges.

Comparison: Free Zone vs Mainland Accounting Requirements

| Aspect | Mainland Companies | Free Zone Companies | Key Considerations |

| Corporate Tax Rate | 0% up to AED 375,000; 9% above | Potentially 0% for qualifying income | Immovable property income is typically taxable even in free zones, per Cabinet Decision 100 |

| Audit Requirements | Based on legal form and thresholds | Based on the free zone authority requirements | Free zone persons with a qualifying status require audits per MD 84/2025 |

| VAT Treatment | Standard UAE VAT rules apply | Standard UAE VAT rules apply | No VAT differences; property type determines treatment |

| IFRS Compliance | Mandatory for financial reporting | Mandatory for financial reporting | DIFC/ADGM may have additional disclosure requirements |

| Ownership Structure | UAE/GCC nationals required for mainland licenses (except 100% foreign ownership for certain activities) | 100% foreign ownership permitted | Does not affect accounting methodology |

| UBO Reporting | Required per Cabinet Resolution 58/2020 | Required per Cabinet Resolution 58/2020 | Identical compliance obligations |

| Economic Substance | No longer applicable for FY ending after Dec 2022 | No longer applicable for FY ending after Dec 2022 | Historical compliance documentation retained |

The primary distinction lies in the corporate tax treatment of qualifying income. However, Ministerial Decision No. 229 of 2025 classifies immovable property ownership and exploitation as excluded activities, severely limiting free zone tax benefits for traditional real estate operations. Only commercial property transactions between free zone persons may qualify for 0% treatment, subject to substance requirements and de minimis thresholds.

In Conclusion

Accounting for real estate companies in Dubai requires integrating IFRS technical standards with UAE-specific VAT rules and the evolving corporate tax framework. Success depends on establishing robust property classification processes, implementing defensible revenue recognition methodologies, maintaining comprehensive documentation supporting tax positions, and engaging qualified accounting professionals with demonstrated UAE real estate expertise. The Federal Tax Authority’s sector-specific guidance and Ministry of Finance corporate tax clarifications provide essential frameworks, but application to specific transactions demands careful analysis and conservative positioning where regulatory interpretation remains uncertain.