UAE Financial Reporting Framework

The Legislative Foundation

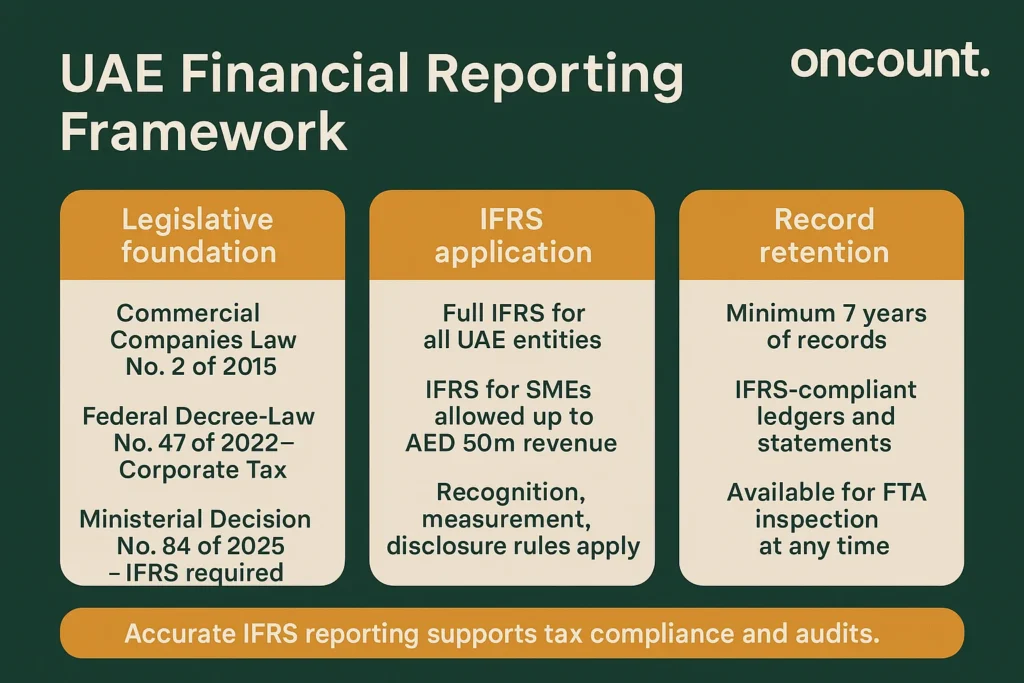

The UAE’s financial reporting requirements rest on three critical pieces of legislation that collectively define the compliance landscape for all business entities. Commercial Companies Law No. 2 of 2015 establishes the foundational requirement for international accounting standards compliance across all mainland and free zone entities. Ministerial Decision No. 84 of 2025 mandates IFRS application without exception, eliminating simplified or local formats and ensuring compliance with international financial reporting standards.

Federal Decree-Law No. 47 of 2022 on Corporate Tax introduces tax-specific reporting obligations and seven-year record retention requirements that UAE must adhere to at all times. Under this legislation, all taxable entities must maintain IFRS-compliant records for inspection by the Federal Tax Authority (FTA) at any time, establishing a direct link between financial reporting and tax compliance that companies in Dubai and FTA approved tax agents must navigate carefully.

IFRS Application in the UAE Context

The adoption of IFRS as the mandatory accounting framework represents a strategic alignment with international business practices. FTA guidance stipulates that the application of IFRS extends beyond mere format compliance—it requires substantive adherence to recognition, measurement, presentation, and disclosure requirements across all financial statement elements.

For entities with annual revenue not exceeding AED 50 million, IFRS for SMEs provides a simplified yet comprehensive reporting framework. In practice, free zone entities often encounter specific challenges when transitioning from simplified accounting systems to full IFRS compliance, particularly when historical records were maintained using alternative frameworks that no longer meet UAE regulations.

Core Financial Statements Required in the UAE

Statement of Financial Position (Balance Sheet)

The Statement of Financial Position captures the company’s financial standing at a specific reporting date, presenting a structured view of assets, liabilities, and equity. This statement is essential to fulfill financial reporting requirements and provides insights into a company’s financial health at a given point in time.

Assets must be classified as current or non-current, with current assets including cash, trade receivables, inventory, and prepaid expenses expected to be realized within twelve months. Non-current assets encompass property, plant and equipment, intangible assets, long-term investments, and deferred tax assets. The liabilities section follows similar classification, while the equity section reconciles to the fundamental accounting equation: Total Assets = Total Liabilities + Total Equity.

Statement of Profit or Loss and Other Comprehensive Income

The income statement serves as the primary reference point for assessing company’s financial performance and calculating corporate tax obligations. FTA regulations require that this statement present revenue figures on a VAT-exclusive basis unless specifically preparing VAT reconciliation documentation, ensuring accurate financial reporting aligned with UAE accounting standards.

Revenue recognition follows IFRS 15 principles, requiring that income be recorded when performance obligations are satisfied rather than when cash changes hands. The statement progresses from revenue through cost of goods sold to gross profit, then deducts operating expenses to arrive at operating profit, adjusts for non-operating items, and concludes with net profit or loss after tax expense. Under IFRS 18, effective January 1, 2027, the income statement format must include segmentation of income and expenses as operating, investing, and financing activities.

Statement of Cash Flows

Cash flow reporting segments cash movements into three distinct categories that illuminate different aspects of financial activities. Operating activities reflect cash generated from core business operations, investing activities capture cash flows from long-term asset transactions, and financing activities encompass cash movements related to borrowings and equity.

This statement reconciles the opening and closing cash positions shown on successive balance sheets. For UAE businesses managing VAT obligations, timing differences between VAT accounting and cash collection create working capital fluctuations that must be carefully tracked to provide financial clarity regarding actual cash generation.

Statement of Changes in Equity

This statement bridges the opening and closing equity balances shown on successive balance sheets, providing transparency into all equity movements during the reporting period. The statement typically presents separate columns for share capital, retained earnings, and other comprehensive income reserves.

Movements captured include net profit for the period, other comprehensive income items such as foreign currency translation adjustments, dividend distributions, and any changes in share capital. This comprehensive view ensures stakeholders understand how the company’s financial position has evolved through both operational results and ownership transactions.

Notes to the Financial Statements

Notes provide critical context and transparency required by IFRS, transforming raw financial data into meaningful business intelligence. The financial statements include these explanatory disclosures to meet compliance with regulatory requirements and provide the detailed financial reporting process documentation that auditors and regulators expect.

Significant accounting policies must be disclosed, detailing specific methods applied for revenue recognition, depreciation, inventory valuation, and other material treatments. Critical accounting judgments and estimates warrant separate disclosure, particularly when management has applied significant assumptions. Complex line items such as provisions, impairments, and related-party transactions require detailed schedules breaking down components and movements during the period.

Step-by-Step Process for Conducting Financial Reporting in the UAE

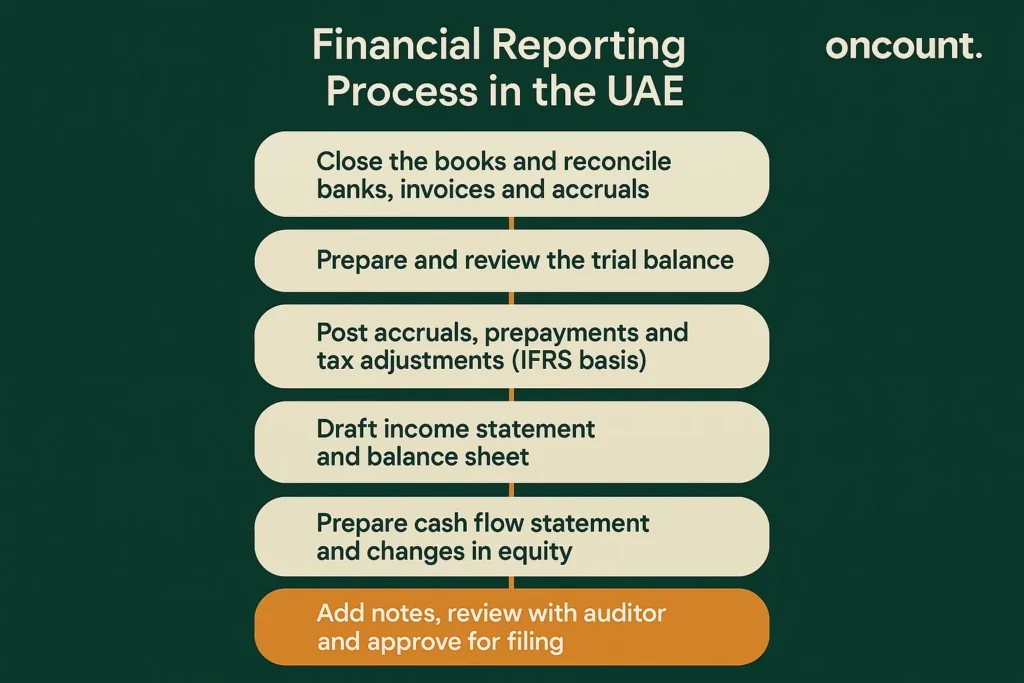

Step 1: Close Your Books for the Period

The financial reporting process begins with ensuring that all transactions for the period have been properly recorded in your accounting system. This foundational step involves reconciling all bank accounts to the general ledger, recording all outstanding invoices and payments, and documenting any accrued expenses and prepaid items that need adjustment.

In the UAE, entities preparing to file corporate tax or submit reports to regulatory authorities must ensure that all records are error-free and fully reconcilable before proceeding. Audited data from 2023 indicates that roughly 40% of statement restatements resulted from incomplete or inaccurate book-closing procedures, highlighting the necessity of this initial step for producing statements that reflect the true position of the business.

Step 2: Prepare the Trial Balance

Generate a trial balance that lists all general ledger accounts with their respective debit or credit balances. This critical checkpoint ensures that total debits equal total credits, confirming the mathematical accuracy of your accounting records and setting the foundation for accurate financial statements.

For UAE companies preparing corporate tax filings or submission to regulatory authorities, a clean trial balance is essential. Any mismatch must be investigated and resolved, as it may indicate journal entry errors, missing transactions, or duplicated postings. Experienced accounting companies emphasize that trial balance verification should occur monthly rather than only at year-end, enabling earlier detection and correction of errors.

Step 3: Adjust for Accruals and Prepayments

Under IFRS and UAE tax law, your financial statements must follow the accrual basis of accounting rather than the cash basis. This fundamental principle creates the primary distinction between accounting profit and cash flow, ensuring that income and expenses are recorded in the period they actually occur.

Key adjustments include revenue recognition following IFRS 15 principles, recording accrued liabilities for expenses incurred but not yet paid, and allocating prepaid expenses to the periods they relate to. For UAE corporate tax purposes, calculate taxable profit by adjusting the accounting profit for non-deductible expenses and exempt income, ensuring proper alignment between financial reporting and tax calculations.

Step 4: Prepare the Income Statement

Develop the Income Statement (Statement of Profit or Loss and Other Comprehensive Income), which is typically the first reference point for investors, auditors, and the FTA to assess profitability and tax obligations. The income statement should present revenue on a VAT-exclusive basis, followed by cost of goods sold to arrive at gross profit.

Operating expenses must be properly classified and presented, with depreciation calculated according to the useful lives of assets. Non-operating items such as interest income and expense should be separately disclosed, enabling readers to distinguish between operational performance and financing costs. The tax expense provision requires careful calculation based on the applicable corporate tax rate applied to taxable profit.

Step 5: Prepare the Balance Sheet

The Balance Sheet (Statement of Financial Position) shows what your business owns and owes as of the reporting date. Assets must be classified as current or non-current based on their expected realization timeframe, with proper presentation ensuring compliance with accounting and auditing standards.

Current assets include cash, receivables, inventory, and prepayments expected to be realized within twelve months. Non-current assets include property, plant and equipment, intangible assets, and long-term investments. The equity section must reconcile to ensure that Total Assets = Total Liabilities + Total Equity, with detailed presentation of share capital, retained earnings, and other comprehensive income reserves.

Step 6: Prepare the Cash Flow Statement

The Cash Flow Statement tracks cash movements across operating, investing, and financing activities, providing essential information about the company’s liquidity and cash management. Operating activities begin with net profit and adjust for non-cash items such as depreciation and amortization, then factor in changes in working capital.

Investing activities capture cash flows from the purchase and sale of fixed assets and investments, while financing activities reflect cash flows from borrowings, loan repayments, dividend payments, and equity transactions. The statement concludes by presenting the net change in cash and reconciling opening and closing cash balances, completing the financial picture of cash generation and utilization.

Step 7: Prepare the Statement of Changes in Equity

This statement reconciles the opening equity balance to the closing balance, showing how retained earnings and other equity components have evolved. The statement shows net profit for the period, other comprehensive income items, dividends paid or distributions made, any changes in share capital, and any other movements in equity reserves.

This transparency into equity movements ensures stakeholders understand how profits have been allocated and how ownership interests have evolved. The statement bridges the income statement results with the equity section of the balance sheet, completing the interconnected web of financial information.

Step 8: Prepare Notes to the Financial Statements

Notes are critical for explaining your financial statements and providing the transparency required by IFRS. Your explanatory notes should include significant accounting policies and methods applied, critical accounting judgments and estimates used in financial reporting, and detailed breakdowns of complex line items.

Additional disclosures include:

- Segment information if your business operates across multiple divisions

- Financial instrument disclosures including fair value measurements and risk exposures

- Related party transactions with full disclosure of nature, amounts, and outstanding balances

- Contingent liabilities and commitments that may affect future financial position

- Post-balance sheet events that provide additional context to the reported figures

Audit Requirements and Procedures

Mandatory Audit Entities

According to Ministerial Decision No. 84 of 2025, audited financial statements are mandatory for specific categories of businesses operating in the UAE. This requirement ensures transparent financial reporting across entities that have significant economic impact or benefit from special tax treatments.

The following entities must submit their audited financial statements:

- Taxable entities with revenue exceeding AED 50 million during the relevant tax period

- Qualifying Free Zone Persons (QFZP), irrespective of revenue level, as a condition to access the 0% corporate tax rate

- All mainland companies under UAE Commercial Companies Law, regardless of revenue size

- Entities registered for corporate tax or VAT, particularly those undergoing statutory audits

Engaging an Accredited Auditor

The first step in the audit process involves engaging an accredited auditing firm approved by relevant regulatory bodies. Audit firms in Dubai must be licensed under Federal Decree-Law No. 41 of 2023, which governs the accounting and auditing profession in the UAE and establishes professional standards and quality control procedures.

For free zone companies, engage only auditors approved by the specific free zone authority—DMCC companies must use DMCC-approved auditors, JAFZA companies require JAFZA-registered auditors, and other free zones maintain their own approved lists. Ensure the auditor has experience in your industry and understands your business structure, as this expertise significantly impacts the efficiency and quality of the audit process.

The Audit Process

The audit process—whether internal audit or external audit—typically unfolds over several weeks and involves multiple stages of document review and verification. The auditor begins by collecting comprehensive documentation including trial balances, general ledgers, bank statements, vendor invoices, employee records, and fixed asset schedules.

An initial review phase follows, during which the auditor conducts preliminary assessments of accuracy and completeness. On-site or remote audit execution involves detailed verification of transactions, reconciliations, and accounting treatments in accordance with IFRS. The auditor performs substantive testing of account balances, analytical procedures to identify unusual fluctuations, and compliance testing to ensure adherence to relevant regulations. Working with the aid of licensed auditing firm professionals ensures that the process meets all regulatory requirements.

Obtaining Necessary Approvals

Before submitting audited financial statements to authorities, obtain approval from your Board of Directors or management, ensuring all reports have been received, reviewed, and formally approved. Many UAE companies hold their annual general assembly meeting to approve financial statements before submission, as required by the Commercial Companies Law.

Any relevant stakeholders identified in your company’s bylaws or governance structure should also review and approve the statements. For companies with foreign shareholders or parent companies, additional approval layers may exist, requiring coordination across multiple jurisdictions to complete the financial statement preparation process.

Key Deadlines for Financial Reporting

Annual Reporting Deadlines

Most UAE-based businesses close their fiscal year on December 31, although entities may select an alternative year-end after completing the required formalities. Adhering to these timelines is important for meeting reporting obligations and maintaining good standing with regulatory bodies.

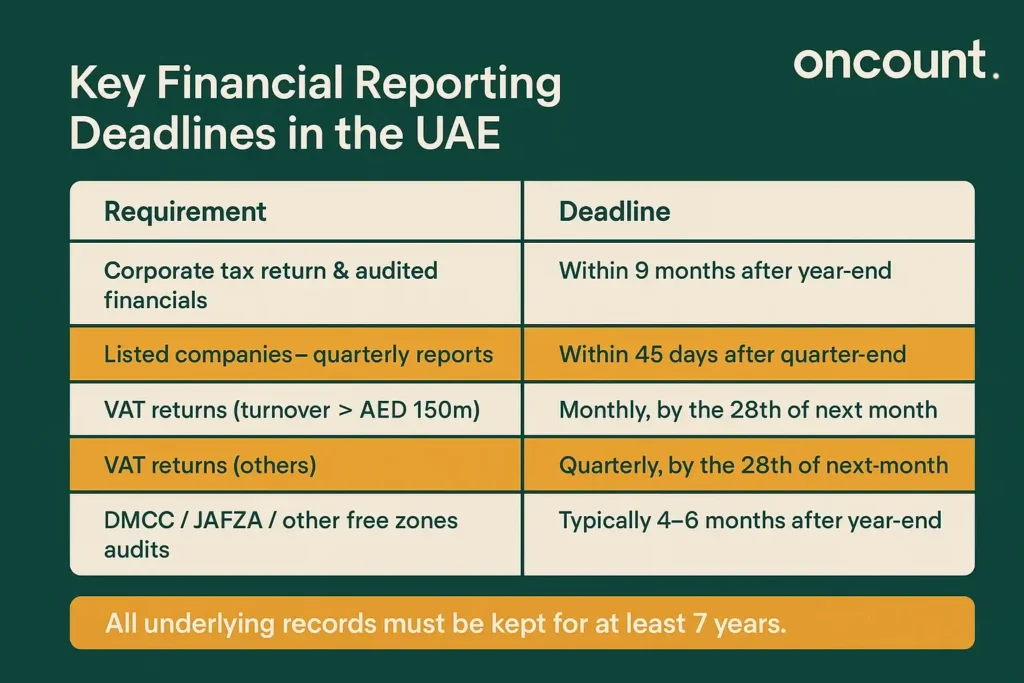

Corporate tax returns and supporting statements must be filed within nine months after the close of the fiscal period. For instance, an entity with a year-end of December 31, 2024 must submit its return by September 30, 2025. Companies in the UAE must also hold their annual general assembly within the prescribed timeframe to approve the accounts and address key governance matters.

Quarterly Reporting Deadlines

Publicly listed companies face additional reporting obligations that exceed the requirements for private entities. These companies must submit their quarterly financial statements within 45 days of the end of each quarter, with an independent auditor review required to guarantee accuracy and conformity.

Additional disclosures regarding material events, segment performance, and forward-looking statements are typically required. This quarterly cycle ensures that investors and market participants have timely access to financial information about the company’s financial performance and emerging trends.

VAT Reporting Deadlines

VAT-registered businesses must adhere to specific FTA reporting guidelines that operate on a different calendar than annual financial reporting. These businesses must fulfill financial reporting deadlines with the aid of systematic processes that track both accounting and tax obligations simultaneously.

Monthly VAT returns are due by the 28th day of the month following the end of the tax period for businesses with annual turnover exceeding AED 150 million. Quarterly returns apply to businesses below this threshold, providing some administrative relief for smaller operations. Businesses must file VAT returns using the VAT 201 form, providing details on VAT on sales, purchases, and net VAT due.

Free Zone Audit Submission Deadlines

Free zone companies face varying submission requirements based on their jurisdiction, creating additional complexity for businesses operating in multiple free zones. Understanding these jurisdiction-specific requirements is essential for maintaining compliance and avoiding penalties that could affect business operations.

| Free Zone | Audit Submission Deadline | Submission Portal | Late Submission Penalty |

| DMCC | 180 days from financial year-end | DMCC Member Portal | AED 5,000 per month |

| JAFZA | 6 months from year-end | JAFZA licensing system | May affect license renewal |

| DAFZA | Varies (typically 6 months) | DAFZA portal | License suspension risk |

| RAKEZ | 6 months from year-end | RAKEZ online system | AED 1,000 initial, escalating |

| DIFC | 4 months from year-end | DIFC Registrar | Significant fines and striking off |

Record Retention and Compliance Obligations

Under Ministerial Decision No. 84 of 2025, all financial records must be retained for at least seven years and be ready for inspection by the Federal Tax Authority at any time. This seven-year retention period applies to all financial statements, ledgers, accounting records, bank statements, payment receipts, invoices both issued and received, contracts and agreements, employee payroll records, and fixed asset registers with depreciation schedules.

The FTA has broad inspection powers and may request access to records at any time during the retention period. Companies should maintain records in organized, accessible formats that enable rapid retrieval during inspections, with digital record-keeping systems offering advantages in storage efficiency, search capability, and backup reliability. For businesses operating across multiple jurisdictions, records must be maintained separately for each entity while enabling consolidated reporting where required, necessitating sophisticated systems that support various financial operations.

VAT Compliance in Financial Reporting

For VAT-registered businesses, preparing accurate financial statements requires incorporating specific VAT considerations that create additional layers of complexity in the financial management process. Revenue figures in financial statements must be VAT-exclusive unless specifically preparing VAT reconciliation documentation, reflecting the principle that VAT represents a flow-through tax collected on behalf of the government.

The FTA requires proper documentation of tax invoices complying with all specifications, including supplier and customer details, tax registration numbers, descriptions of goods or services, amounts, and VAT calculations. Missing or incomplete tax invoices can result in input tax recovery being denied during FTA audits, affecting both the company’s financial health and cash flow. Reconciliation between financial statements and VAT returns represents a critical control procedure that auditors and FTA inspectors examine to identify discrepancies indicating errors or non-compliance.

Special Considerations for Free Zone Companies

Free zone companies face additional reporting layers beyond mainland requirements, reflecting the unique regulatory frameworks governing these jurisdictions. Each free zone maintains its own approved auditor list, requiring companies to engage only auditors who have obtained specific approvals to ensure they understand particular regulations, reporting formats, and compliance obligations.

DMCC requirements include submission of audited financial statements within 180 days via the DMCC Member Portal, use of only DMCC-approved auditors, and exposure to AED 5,000 monthly penalties for late submissions. JAFZA and other zones implement similar audit submission protocols with zone-specific approved auditor lists and consequences for non-compliance. Qualifying Free Zone Persons seeking to maintain 0% corporate tax status must meet heightened compliance requirements including audited financial statements regardless of revenue level and detailed substance documentation demonstrating genuine business activity in the UAE.

IFRS 18: New Standards Effective January 1, 2027

The International Accounting Standards Board (IASB) introduced IFRS 18 on April 9, 2024, with mandatory application beginning January 1, 2027. This new standard fundamentally changes how companies present their income statements, requiring more structured and comparable financial reporting across entities and providing clearer insights into a company’s financial performance.

Income and expense classification under IFRS 18 requires segmentation of all items as operating, investing, or financing activities, mirroring the cash flow statement structure. Structured profit or loss reporting establishes uniform income statement formats with mandatory subtotals for operating profit, profit before financing and income tax, and profit before income tax. UAE businesses should begin planning for IFRS 18 adoption well in advance, as the changes affect core financial reporting systems and processes, requiring system modifications, staff training, and early auditor communication.

Common Penalties for Non-Compliance

Failing to meet compliance with regulatory requirements in the UAE can result in significant penalties that escalate based on severity and duration of non-compliance. Understanding these penalties underscores why businesses must prioritize timely and accurate financial reporting to maintain their financial standing and operational licenses.

Late audit filing penalties range from AED 5,000 to AED 500,000 depending on jurisdiction and delay length. Failure to maintain records as required under UAE laws creates legal consequences and audit complications, potentially resulting in estimated tax assessments based on industry benchmarks rather than actual results. Inaccurate financial reporting triggers fines and potential business license suspension, while late corporate tax filing attracts additional penalties on top of the tax obligation itself.

| Violation Type | Penalty Range | Additional Consequences |

| Late audit filing (mainland) | AED 20,000 – 500,000 | Potential license suspension |

| Late audit filing (DMCC) | AED 5,000 per month | Accumulates monthly until submission |

| Late corporate tax filing | AED 1,000 – 10,000 | Plus interest on unpaid tax |

| Failure to maintain records | Variable | Estimated tax assessments |

| Inaccurate financial reporting | Up to AED 50,000 | License suspension risk |

| Free zone non-compliance | Varies by zone | Trade license non-renewal |

Best Practices for Successful Financial Reporting

Professional support from qualified accounting and auditing professionals should be engaged from the outset to ensure compliance with accounting rules and accuracy in the detailed financial reporting process. Experienced professionals bring knowledge of UAE regulations, FTA expectations, and industry best practices that prove invaluable in navigating the complex regulatory environment and ensuring that businesses follow the international financial reporting standards correctly.

Timely record keeping throughout the year, with monthly reconciliations for bank accounts, inventory, and general ledger balances, streamlines the year-end process and enables earlier identification of issues. Companies should maintain comprehensive documentation supporting all significant accounting transactions, estimates, and judgments, providing the foundation for efficient audit procedures. Advance planning by beginning the audit process early allows sufficient time to review your financial records, make necessary adjustments, and verify compliance before reporting deadlines with the aid of systematic workflows and professional guidance.