VAT in the UAE: Regulatory Framework and Tax Authority

Value Added Tax is an indirect consumption tax applied incrementally throughout the supply chain. Unlike direct taxes, this system operates through a chain of tax credits where businesses collect tax on behalf of the UAE government, charging it on their sales (output tax) while paying it on purchases (input tax). The net difference between these amounts determines your tax liability or refund position.

Role of the Federal Tax Authority (FTA)

The FTA serves as the governmental body responsible for managing, collecting, and enforcing federal taxes across the UAE. Established under Federal Law by Decree No. 13 of 2016, the FTA maintains comprehensive oversight of VAT compliance through several core functions:

- Legislative development: Drafting and implementing federal tax regulations that provide clear frameworks for collection and compliance

- Taxpayer management: Maintaining the national taxpayer database and facilitating business registration through the FTA portal

- Assessment and collection: Evaluating tax liabilities and implementing robust collection mechanisms

- Audit and investigation: Conducting systematic reviews to ensure adherence to VAT regulations and deter evasion

- Dispute resolution: Providing formal mechanisms for objections and appeals

Recent regulatory developments have significantly enhanced the VAT framework. In January 2023, the UAE amended 24 articles of the Value-added tax Law, introducing compliance enhancements across registration, filing, and record-keeping requirements. More recently, Federal Decree-Law No. 16 of 2024 established the roadmap for mandatory electronic invoicing implementation by 2026, representing the most substantial shift in VAT administration since the tax’s introduction.

Current VAT Rates and Supply Classifications

Understanding how VAT applies to your goods and services determines both your registration obligations and your ability to recover input VAT. The UAE employs three distinct tax treatments:

Standard Rate (5%)

The standard VAT rate applies to the vast majority of taxable supplies within the UAE, encompassing consumer electronics, fashion, dining, entertainment, professional services, and most commercial transactions.

Zero-Rated Supplies (0%)

Zero-rated supplies carry significant strategic advantages. While technically subject to VAT at 0%, businesses making zero-rated supplies retain the right to reclaim input Value-added tax on related purchases. FTA guidance identifies specific categories eligible for zero-rating:

- Export of goods and services outside Gulf Cooperation Council (GCC) implementing states

- International transportation services for passengers and goods, including ancillary supplies such as pallets and safety equipment

- First supply or lease of residential buildings intended for human occupation

- Investment-grade precious metals (gold, silver, and platinum with 99% or higher purity)

- Specific educational services provided by accredited institutions

- Preventive and basic healthcare services meeting FTA criteria

- Crude oil and natural gas supplies within the sector

Exempt Supplies

Exempt supplies differ fundamentally from zero-rated supplies. While no Value-added tax is charged on exempt supplies, businesses cannot reclaim input VAT associated with these transactions. Common exempt supplies include:

- Financial services without explicit fees (provision of loans or credit where no commission is charged)

- Life insurance and reinsurance contracts

- Residential property transactions beyond the first supply

- Bare land transactions (undeveloped land without completed structures)

- Local passenger transport services including buses, trams, and taxis

VAT Registration Thresholds: When Your Business Must Register?

Registration requirements depend on your annual turnover, business structure, and geographic presence. The FTA establishes clear thresholds that trigger mandatory or voluntary registration obligations.

Mandatory Registration Threshold

Businesses operating in the UAE must register for VAT when taxable supplies and imports exceed AED 375,000 annually. This mandatory registration threshold applies under two specific circumstances:

- Retrospective assessment: When your taxable supplies during the past 12 months have exceeded AED 375,000

- Prospective assessment: When you reasonably expect your taxable supplies to exceed AED 375,000 within the next 30 days

For resident businesses, the registration threshold is AED 375,000 in annual taxable supplies. Non-resident businesses making taxable supplies in the UAE must register regardless of the value of supplies, provided no other person is obligated to account for VAT on those transactions.

Critical compliance requirement: Failure to register for VAT within 30 days of crossing the mandatory registration threshold results in an administrative penalty of AED 10,000. This penalty applies immediately upon late registration, independent of any subsequent VAT liabilities.

Voluntary Registration Threshold

Businesses with lower turnover may choose to register for VAT voluntarily when their annual taxable supplies and imports exceed AED 187,500—exactly 50% of the mandatory threshold. The voluntary registration threshold serves two strategic functions:

Standard voluntary registration: Available when your taxable supplies during the past 12 months exceeded, or are expected to exceed within the next 30 days, AED 187,500.

Expense-based voluntary registration: Particularly relevant for new companies, this provision allows registration when taxable expenses exceed AED 187,500, even if the business has generated no revenue. Start-ups with significant capital expenditure can voluntarily register for VAT to reclaim input VAT paid on purchases, improving cash flow during the establishment phase.

Strategic Considerations for Voluntary Registration

Business owners frequently question whether voluntary registration serves their commercial interests when turnover falls between AED 187,500 and AED 375,000. Consider these factors:

Advantages of voluntary registration:

- Immediate recovery of input Value-added tax on business expenses, directly improving working capital

- Enhanced credibility when dealing with VAT-registered clients who prefer suppliers capable of providing input tax credits

- Improved competitive positioning when responding to government tenders and contracts with large corporations

- Early establishment of VAT compliance infrastructure before mandatory registration

Potential disadvantages:

- Administrative burden of filing regular VAT returns and maintaining comprehensive records

- Need to charge VAT on taxable supplies, which may affect price sensitivity in consumer markets

- Requirement to continue VAT obligations even if turnover subsequently falls below thresholds

Registration Requirements for Non-Resident Businesses

Non-resident businesses face distinct registration obligations. Under UAE VAT law, a non-resident business making taxable supplies in the UAE must register regardless of turnover value when:

- The supplies are made within the territorial scope of UAE VAT

- No tax representative or agent in the UAE is required to account for the VAT

- The supplies would be taxable if made by a UAE-established business

In practice, non-resident businesses often appoint tax representatives to manage VAT compliance. The FTA requires formal documentation establishing the representative relationship, and both parties bear joint responsibility for VAT obligations.

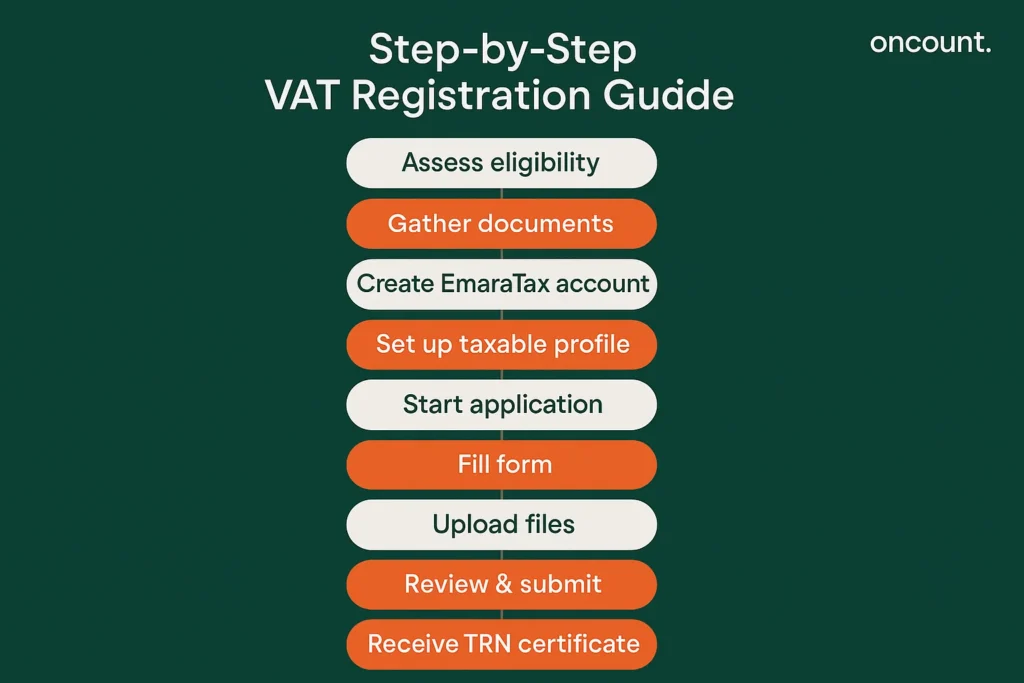

VAT Registration Process: Step-by-Step Implementation

Registering for VAT in the UAE follows a structured digital process through the FTA portal. Business owners should anticipate a registration timeline of 20 to 30 business days, though complete and accurate applications may receive faster approval.

Step 1: Assess Your Registration Eligibility

Before initiating registration, conduct a comprehensive assessment of your VAT position. Calculate your trailing 12-month taxable supplies by aggregating:

- Standard-rated supplies at 5%

- Zero-rated supplies (exports, international transport, first residential property sales)

- Imports of goods into the UAE

- Anticipated supplies for the next 30 days if approaching the threshold

Exclude exempt supplies from this calculation, as they do not count toward registration thresholds. If your business operates across multiple legal entities, each juridical person must evaluate thresholds independently unless qualifying for group registration.

Step 2: Compile Required Documentation

The VAT registration application demands comprehensive business documentation. Incomplete submissions represent the primary cause of registration delays. Gather these essential documents before accessing the FTA portal:

Business Registration Documents:

- Valid trade licence issued by the relevant Department of Economic Development or free zone authority

- Memorandum of Association (MOA) or Articles of Association

- Partnership Agreement (for partnerships)

- Certificate of Incorporation or business registration certificate

Personal Identification:

- Passport copies for all shareholders, partners, and authorized signatories

- Emirates ID copies for all UAE-resident owners and authorized persons

- Power of Attorney documentation if someone other than the business owner will complete the registration

Financial Documentation:

- Bank account details including full IBAN

- Bank letter verifying company bank account details (on bank letterhead)

- Audited financial statements or balance sheet (if available)

- Detailed breakdown of annual turnover for the preceding 12 months

- Revenue projections for the next 30 days if registering based on prospective threshold

Address and Contact Verification:

- Tenancy contract or property title deed for registered business address

- Utility bill or DEWA connection letter confirming physical presence

- Contact email address and registered mobile number

Sector-Specific Documentation:

- Customs registration code for businesses engaged in import or export activities

- Details of operations in other GCC countries for cross-border businesses

- Club, charity, or association registration documents (if applicable)

The FTA may request additional clarification or documentation during the review process. Maintaining organized digital copies of all documents facilitates rapid response to information requests.

Step 3: Create Your EmaraTax Account

The FTA’s digital platform, EmaraTax, serves as the centralized portal for all VAT-related activities. Access the portal through the official FTA website at www.tax.gov.ae:

Navigate to the eServices section and select new user registration. You have two authentication options:

Standard registration: Provide your email address, mobile number, personal details, and create a secure password. The FTA will send verification codes to confirm your contact details.

UAE Pass integration: Leverage the UAE Pass digital identity system for streamlined authentication. This government-issued digital credential simplifies access across federal platforms and represents the preferred method for frequent FTA portal users.

Following successful registration, secure your login credentials through a password management system. You will return to this portal repeatedly for return filing, payment processing, and correspondence with the FTA.

Step 4: Establish Your Taxable Person Profile

Once logged into EmaraTax, establishing your Taxable Person Profile precedes the formal VAT registration application. This profile creates your business identity within the FTA system:

Navigate to the Taxable Person Profile section and enter comprehensive business details including your legal trade name, business category classification, primary activities, and complete contact information. The FTA employs this profile data to assign your VAT return cycle and establish your taxpayer record.

Submit your profile for FTA verification. The verification process typically requires several business days as the authority cross-references your information against commercial registration databases. Monitor your email for verification confirmation before proceeding to VAT registration.

Step 5: Initiate the VAT Registration Application

With your verified Taxable Person Profile established, access the VAT Registration section from your dashboard. Select the appropriate registration type based on your circumstances:

Mandatory Registration: Choose this option when your taxable supplies exceed AED 375,000 annually, or when you operate as a non-resident business making taxable supplies in the UAE.

Voluntary Registration: Select this pathway when your supplies or expenses exceed the voluntary registration threshold of AED 187,500 but remain below the mandatory threshold.

Review all pre-populated information transferred from your Taxable Person Profile to ensure accuracy before proceeding. The system will guide you through the comprehensive registration form in sequential sections.

Step 6: Complete the VAT Registration Form

The VAT registration form requires detailed information across multiple categories. Accuracy in this section directly affects processing time and approval probability:

Business Classification Details:

- Complete legal business name exactly as registered with licensing authorities

- Registered business address with P.O. Box

- Trade licence number and issuing authority

- Comprehensive description of business activities

- Business structure (sole proprietorship, limited liability company, partnership, branch of foreign company)

Financial Information:

- Actual annual turnover for the preceding 12 months, broken down by tax treatment (standard-rated, zero-rated, exempt)

- Expected monthly turnover for the upcoming 12 months

- Details of taxable expenses if registering based on the expense provision

- Projected revenues for the next 30 days if registering prospectively

Operational Geography:

- Confirmation of whether the business operates exclusively in the UAE or maintains establishments in other GCC states

- Details of any permanent establishments, branches, or subsidiaries

- Specific identification of GCC countries where related business activities occur

Banking Arrangements:

- Business bank account number

- Complete IBAN (International Bank Account Number)

- Bank name and branch details

- Confirmation that the bank account is registered in the business’s legal name

Provide realistic, verifiable financial projections. The FTA may request supporting documentation for turnover claims that appear inconsistent with your business profile or industry norms.

Step 7: Upload Supporting Documents

The document upload interface accepts PDF, JPEG, and PNG formats. Ensure all uploaded documents are:

- Clear and legible (avoid poorly scanned or photographed documents)

- Current and valid (expired documents will be rejected)

- Complete (upload all pages of multi-page documents)

- Correctly labeled matching the FTA’s document categories

Common upload errors include submitting documents with insufficient resolution, uploading files in unsupported formats, or providing documents that don’t clearly establish the required information. Before uploading, verify that:

- Trade licences clearly display the business name, activity, and expiration date

- Bank letters include official bank letterhead, account details, and authorized signatures

- Identification documents show clear photos and readable text

- Financial statements bear auditor signatures or official stamps where applicable

Step 8: Review and Submit Your Application

Prior to final submission, conduct a comprehensive review of your entire application. Common errors at this stage include:

- Inconsistencies between financial projections and uploaded financial statements

- Mismatched business names across different documents

- Incorrect authorized signatory designations

- Incomplete mandatory fields

Confirm that you’ve designated the appropriate FTA-authorized signatory for your business. This individual will receive official FTA correspondence and bears responsibility for VAT compliance oversight.

Accept the terms and conditions acknowledging your understanding of VAT obligations, then submit your application. The system will generate a unique application reference number—record this number immediately for tracking purposes.

Step 9: Monitor Application Progress

Following submission, the FTA commences its review process. Access your application status through the EmaraTax portal by navigating to Application Status or My Applications and entering your reference number.

Expected timeline: Standard processing requires 20 to 30 business days, though straightforward applications with complete documentation may receive earlier approval. Complex business structures, unusual activity classifications, or incomplete documentation extend processing time.

During review, the FTA may contact you via email or SMS requesting:

- Clarification of business activities or financial projections

- Additional supporting documentation

- Corrections to submitted information

- Supplementary details about related party transactions or group structures

Respond promptly to FTA queries. Delayed responses restart the processing timeline and may result in application rejection, requiring complete resubmission.

Step 10: Receive Your Tax Registration Number

Upon successful application review, the FTA issues your Tax Registration Number (TRN)—a unique 15-digit identifier that remains with your business throughout its VAT registration period. You will receive notification through:

- Email to your registered email address

- SMS to your registered mobile number

- Direct notification within your EmaraTax dashboard

Download your Value-added tax registration certificate immediately. This official document confirms your VAT-registered status and includes:

- Your complete TRN

- Registration effective date

- Business details as registered with the FTA

- Applicable VAT return filing frequency (monthly or quarterly)

- Assigned VAT return cycle group

Your TRN serves multiple critical functions:

- Must appear on every tax invoice you issue to customers

- Required when filing VAT returns and making VAT payments

- Necessary for input VAT recovery claims

- Used in all official correspondence with the FTA

Communicate your TRN to existing suppliers, customers, and business partners. Update your invoicing systems, accounting software, and business stationery to display the TRN prominently on all commercial documents.

VAT Compliance Obligations: Post-Registration Requirements

Successfully registering for VAT initiates ongoing compliance obligations that continue throughout your business’s operational lifecycle. Non-compliance with these requirements triggers substantial penalties and potential business disruption.

Tax Invoice Requirements

Every VAT-registered business must issue compliant tax invoices when selling taxable goods and services. FTA regulations specify mandatory elements for valid tax invoices:

Essential Invoice Components:

| Invoice Element | Requirement |

| Supplier identification | Full legal name, address, and TRN |

| Customer identification | Legal name, address, and TRN (if VAT-registered) |

| Document designation | Clear marking as “Tax Invoice” |

| Invoice number | Sequential unique identifier |

| Issue date | Date and time of invoice generation |

| Description | Detailed goods/services description |

| Quantity | Units supplied |

| Unit price | Price per unit before VAT |

| VAT rate | Applicable rate (typically 5%) |

| VAT amount | Calculated tax per line item |

| Total amounts | Pre-tax subtotal, total VAT, and gross total including VAT |

For supplies exceeding AED 10,000, full tax invoices with complete customer details become mandatory. Smaller supplies may utilize simplified invoices with reduced information requirements, though full invoices remain acceptable for all transaction values.

The distinction between standard-rated, zero-rated, and exempt supplies must be clearly indicated on invoices. When an invoice includes mixed supplies, separate line items should identify the VAT treatment of each component.

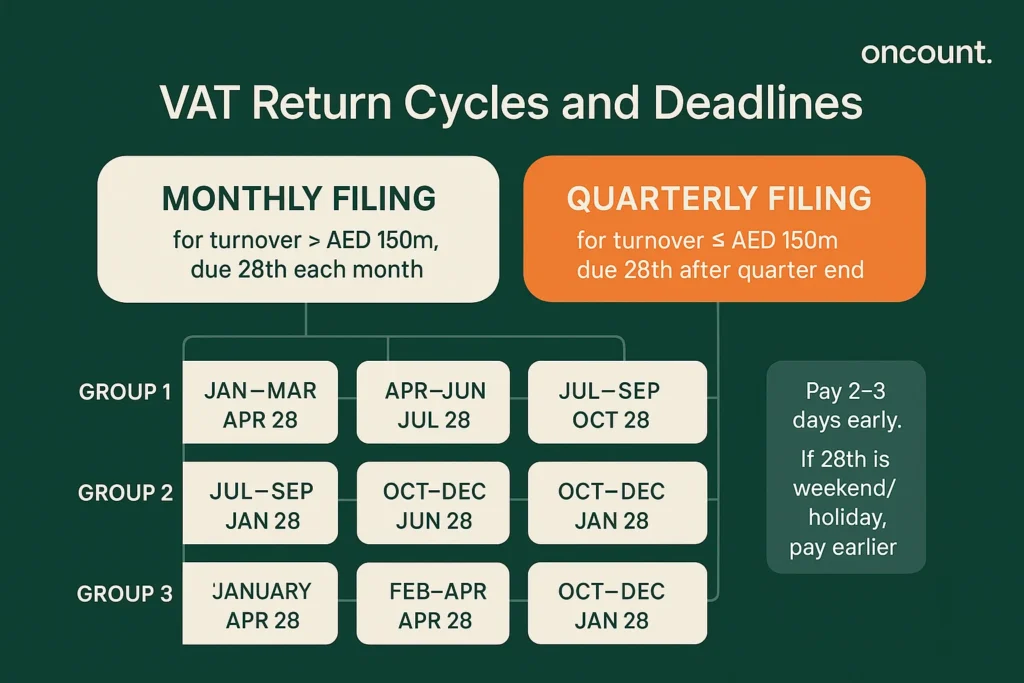

VAT Return Filing Frequency

Your filing frequency depends on annual turnover. The FTA assigns businesses to monthly or quarterly filing schedules:

Monthly Filing: Required exclusively for businesses with annual taxable supplies exceeding AED 150 million. Monthly filers must submit returns and make VAT payments by the 28th day of the following month.

Quarterly Filing: Applies to the majority of UAE businesses—those with annual taxable supplies of AED 150 million or less. Quarterly returns and payments are due by the 28th day following the end of each three-month tax period.

Understanding VAT Return Cycles

The FTA organizes quarterly filers into three distinct groups, each following staggered reporting periods:

Group 1:

- Q1: January through March (deadline: April 28)

- Q2: April through June (deadline: July 28)

- Q3: July through September (deadline: October 28)

- Q4: October through December (deadline: January 28)

Group 2:

- Q1: February through April (deadline: May 28)

- Q2: May through July (deadline: August 28)

- Q3: August through October (deadline: November 28)

- Q4: November through January (deadline: February 28)

Group 3:

- Q1: March through May (deadline: June 28)

- Q2: June through August (deadline: September 28)

- Q3: September through November (deadline: December 28)

- Q4: December through February (deadline: March 28)

The FTA assigns your group during registration based on business registration date and internal distribution requirements. Your assigned group remains consistent throughout your VAT registration period.

Calculating VAT Liability

Understanding how to calculate your net VAT position determines your payment or refund amount each period:

Basic VAT Calculation Formula:

Output VAT (VAT collected on sales)

– Input VAT (VAT paid on purchases)

= Net VAT Liability

Practical Example:

A Dubai-based trading company’s quarterly activity:

- Total sales (including VAT): AED 1,050,000

- Output tax collected (5%): AED 50,000

- Total purchases (including tax): AED 630,000

- Input tax paid (5%): AED 30,000

Net tax payable to FTA: AED 50,000 – AED 30,000 = AED 20,000

If input tax exceeds output tax, creating a negative balance, you may claim a VAT refund from the FTA or carry the credit forward to offset against future tax periods. The Federal Tax Authority processes refund claims following additional verification procedures to prevent fraudulent claims.

VAT Return Submission Process

File VAT returns exclusively through the EmaraTax portal following this sequence:

- Log into your EmaraTax account using your credentials or UAE Pass

- Navigate to the VAT Return section

- Select the applicable tax period from available options

- Enter transaction values:

- Standard-rated supplies (output VAT)

- Zero-rated supplies

- Exempt supplies

- Input VAT on purchases

- Adjustments for previous period corrections

- Review calculated net VAT position

- Submit the return electronically

- Receive confirmation with a unique return reference number

Following return submission, complete payment within the same deadline (28th of the following month). The FTA accepts payments through multiple channels:

- e-Dirham: Direct online payment via credit or debit card through the FAB Magnati gateway

- Local bank transfer: Using your assigned GIBAN (Gulf International Bank Account Number)

- International wire transfer: For payments from overseas accounts

- EmaraTax portal: Direct payment processing within the platform

Critical consideration: Bank transfers may require 2 to 3 business days for processing. To avoid late payment penalties, initiate transfers at least three business days before the deadline. If the 28th falls on a Friday, Saturday, or public holiday, payment must be completed by the preceding business day.

Record Keeping Requirements

VAT regulations mandate comprehensive record retention for specified periods:

General VAT records: Minimum 5 years from the end of the tax period to which they relate

Capital asset records: Minimum 10 years (machinery, equipment, property)

Real estate transaction records: Minimum 5 years

Records may be maintained electronically or in physical format, but must be readily accessible for FTA inspection. Businesses conducting operations across multiple emirates should maintain consolidated records with clear identification of transactions by jurisdiction.

Essential documents to retain:

- All issued tax invoices and credit notes

- All received supplier invoices and import documentation

- Bank statements and payment records

- Accounting ledgers (sales, purchase, general)

- Customs declarations and import/export documentation

- Contracts with suppliers and customers

- Fixed asset registers and depreciation schedules

- Inventory records and stock movement logs

- VAT return submission confirmations

- Correspondence with the FTA

Special VAT Considerations for Free Zones

The UAE designates 23 specific free zones receiving preferential VAT treatment. Understanding how VAT applies within and between designated zones affects registration requirements and compliance obligations.

Designated Free Zones

FTA regulations identify these zones as outside the territorial scope of UAE VAT for specific transactions:

Dubai Free Zones:

- Jebel Ali Free Zone (JAFZA) North and South

- Dubai Airport Free Zone

- Dubai Aviation City

- Dubai Cars and Automotive Zone (DUCAMZ)

- International Humanitarian City

- Additional designated Dubai zones

Abu Dhabi Free Zones:

- Khalifa Port Free Trade Zone

- Abu Dhabi Airport Free Zone

- Khalifa Industrial Zone Abu Dhabi (KIZAD)

Other Emirates:

- Sharjah Airport International Free Zone

- Ajman Free Zone

- Umm Al Quwain Free Trade Zone

- RAK Free Trade Zone, RAK Maritime City, RAK Airport Free Zone

- Fujairah Free Zone and Fujairah Oil Industry Zone

VAT Treatment Within Designated Zones

Movement of goods between designated zones generally does not attract VAT when:

- Goods are transferred without alteration or consumption

- Proper documentation tracks the movement

- The transfer occurs directly between designated zones without mainland intervention

Supply of services within designated zones remains subject to standard UAE VAT law. The preferential treatment applies primarily to goods movement, not service provision.

Businesses operating from designated zones must still register for VAT when they:

- Make taxable supplies to UAE mainland customers exceeding the registration threshold

- Import goods from the free zone to the mainland for consumption

- Provide services with a place of supply in the UAE mainland

VAT Registration in Dubai: Mainland vs. Free Zone

Dubai businesses face distinct considerations based on their licensing jurisdiction. A Dubai mainland company making taxable supplies exceeding AED 375,000 annually must register for VAT regardless of customer location. Free zone companies require registration when supplies to the mainland cross the mandatory registration threshold, but supplies exclusively to other designated zones or international exports may fall outside the VAT scope.

Penalties for Non-Compliance: Financial and Operational Consequences

Understanding penalty structures helps business owners appreciate the importance of timely VAT registration and ongoing compliance.

Late Registration Penalties

Administrative penalty: AED 10,000 fixed penalty for failure to register for VAT within 30 days of exceeding the mandatory registration threshold. This penalty applies independently of any VAT amounts that should have been collected during the non-compliance period.

Additional consequences extend beyond the direct financial penalty:

- Retrospective VAT assessment on all supplies made during the non-compliance period

- Personal liability for directors in cases of intentional non-compliance

- Difficulty securing government contracts and tenders

- Reputational damage affecting supplier and customer relationships

- Enhanced scrutiny during subsequent FTA audits

Late VAT Payment Penalties

The FTA implements an escalating penalty structure for late VAT payments:

- Immediate penalty: 2% of the outstanding VAT amount applies from the first day after the payment deadline

- Monthly penalties: Additional 4% of the outstanding amount for each subsequent month

- Daily penalties: In severe cases, 1% daily penalties may apply

- Maximum penalty: Aggregate penalties can reach 300% of the original VAT liability

Illustrative calculation:

| Timeline | Outstanding VAT | Penalty Rate | Penalty Amount | Cumulative Total |

| Due date | AED 50,000 | – | – | AED 50,000 |

| Day 1-30 | AED 50,000 | 2% | AED 1,000 | AED 51,000 |

| Day 31-60 | AED 50,000 | 4% | AED 2,000 | AED 53,000 |

| Day 61-90 | AED 50,000 | 4% | AED 2,000 | AED 55,000 |

These penalties accumulate rapidly. A business delaying payment by just three months faces penalties of AED 5,000 on an original VAT liability of AED 50,000—a 10% penalty increase. Extended non-payment triggers compound penalties potentially exceeding the original tax liability.

Record-Keeping Violations

Insufficient documentation attracts separate penalties:

- Failure to maintain required records: AED 10,000 (first offense), AED 20,000 (repeated offense)

- Failure to submit records in Arabic when requested: AED 20,000

- Providing incorrect information to the FTA: AED 5,000 minimum

Small Business Relief: Strategic Considerations

The Small Business Relief (SBR) scheme provides Corporate Tax exemptions for eligible small enterprises, though it intersects with VAT obligations in important ways.

SBR Eligibility Criteria

Businesses qualify for SBR when:

- Annual revenue does not exceed AED 3 million in any tax period

- The business is a Resident Natural or Juridical Person

- Operations occur during eligible periods (June 1, 2023 through December 31, 2026)

Exclusions from SBR:

- Members of Multinational Enterprise groups

- Free Zone Persons subject to 0% Corporate Tax regimes

- Non-Resident Taxable Persons

- Businesses artificially structured to maintain revenue below AED 3 million

Interaction Between SBR and VAT Registration

Small Business Relief addresses Corporate Tax, not VAT. Businesses benefiting from SBR must still register for VAT when their taxable supplies exceed the mandatory registration threshold of AED 375,000. These represent separate tax regimes with distinct registration requirements and compliance obligations.

A business with annual revenue of AED 2.5 million making entirely taxable supplies must register for VAT (exceeding AED 375,000) while remaining eligible for SBR (below AED 3 million). The business would charge VAT on taxable supplies and file regular VAT returns, but would not calculate or pay Corporate Tax during the relief period.

Critical consideration: If business revenue exceeds AED 3 million in any single tax period between 2024 and 2026, SBR eligibility terminates permanently. Subsequent revenue declines below AED 3 million do not restore eligibility.

Common VAT Registration Mistakes and Prevention Strategies

Experience working with UAE businesses reveals recurring errors that delay registration or create compliance issues. Understanding these pitfalls enables proactive prevention.

Documentation Errors

Mistake: Submitting applications with incomplete, expired, or illegible documentation

Prevention: Conduct comprehensive document review before accessing the FTA portal. Verify that trade licences show current expiration dates, bank letters include all required elements on official letterhead, and identification documents display clear photographs and readable text.

Mistake: Inconsistent business information across different documents

Prevention: Ensure your trade licence name, MOA business name, bank account name, and registration application name match exactly. Even minor variations (LLC vs. Limited Liability Company) can trigger rejections.

Threshold Calculation Errors

Mistake: Incorrectly calculating taxable supplies when determining whether the registration threshold has been crossed

Prevention: Include all standard-rated supplies, zero-rated supplies, and imports in threshold calculations. Exclude only exempt supplies. For businesses with complex transaction types, maintain a monthly tracking spreadsheet documenting taxable supply values.

Mistake: Failing to register within 30 days when prospective threshold crossing becomes apparent

Prevention: Implement quarterly turnover reviews projecting forward 30 days. When you secure a large contract pushing projected supplies above AED 375,000, initiate registration immediately rather than waiting for actual revenue realization.

Post-Registration Compliance Failures

Mistake: Missing the 28-day deadline for VAT return filing and payment

Prevention: Establish automated calendar reminders at 15 days before deadline (return preparation), 7 days before deadline (return review), and 3 days before deadline (payment initiation). Consider accounting software with integrated deadline alerts.

Mistake: Issuing invoices without mandatory VAT elements

Prevention: Configure accounting systems to auto-generate FTA-compliant invoices including all mandatory fields. Conduct quarterly invoice audits selecting random samples for compliance verification.

Mistake: Inadequate record retention systems leading to missing documentation during audits

Prevention: Implement digital document management systems with automated backup. Organize records by tax period with consistent naming conventions. For paper records, establish indexed filing systems enabling rapid retrieval.

Conclusion: Your Path to Successful Registration in the UAE

Understanding value-added tax in UAE is essential for business success. This guide to registration clarifies when businesses are required to register and how to complete the online registration process efficiently. Companies providing services in the UAE that exceed the threshold must use the online registration form to obtain their certificate and tax number, enabling them to legally charge the applicable rate on taxable supplies.

For new businesses or established companies, knowing when you need to register prevents costly delays. Whether you’re required to register based on current turnover or still need to register due to projected growth, understanding the amount charged and the documentation required for registration is crucial. Businesses that must charge tax face clear obligations, and non-compliance with VAT regulations triggers substantial penalties. Register in UAE promptly, whether independently or through registration services, to fulfill all tax purposes under UAE law and maintain proper compliance with federal tax rules.